Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

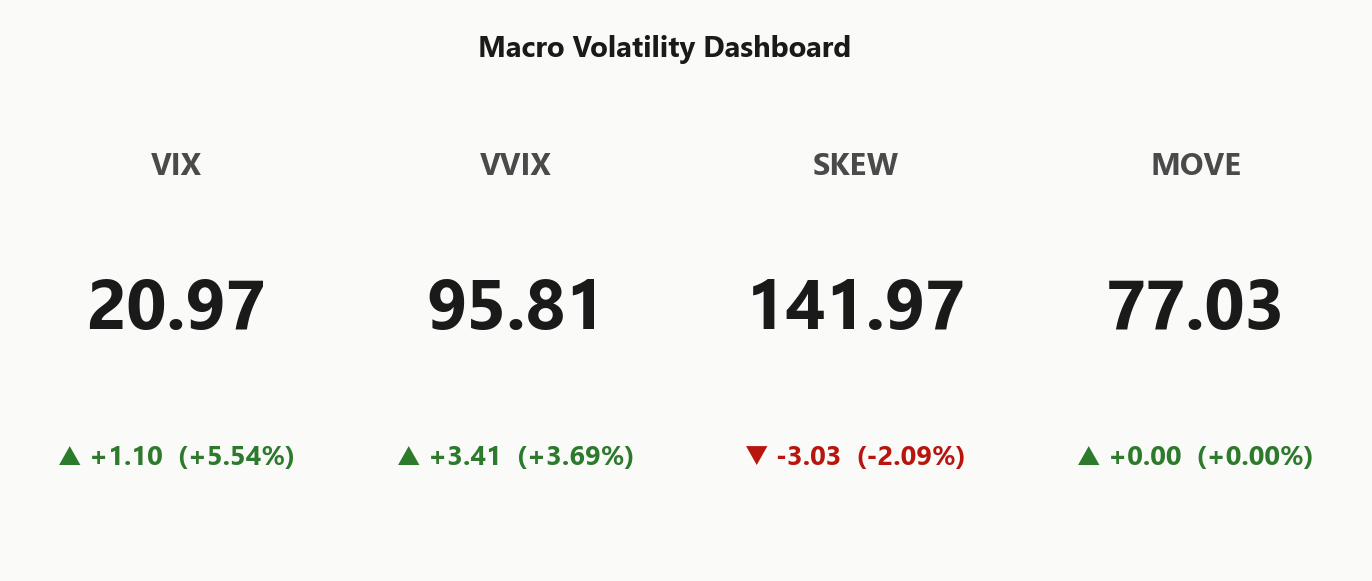

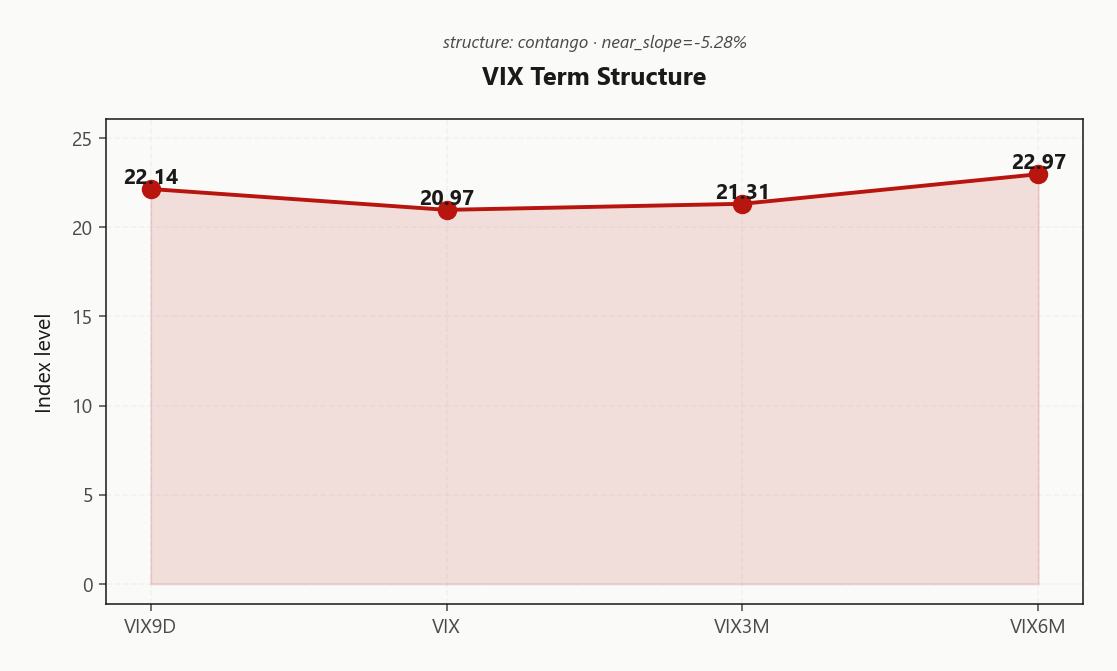

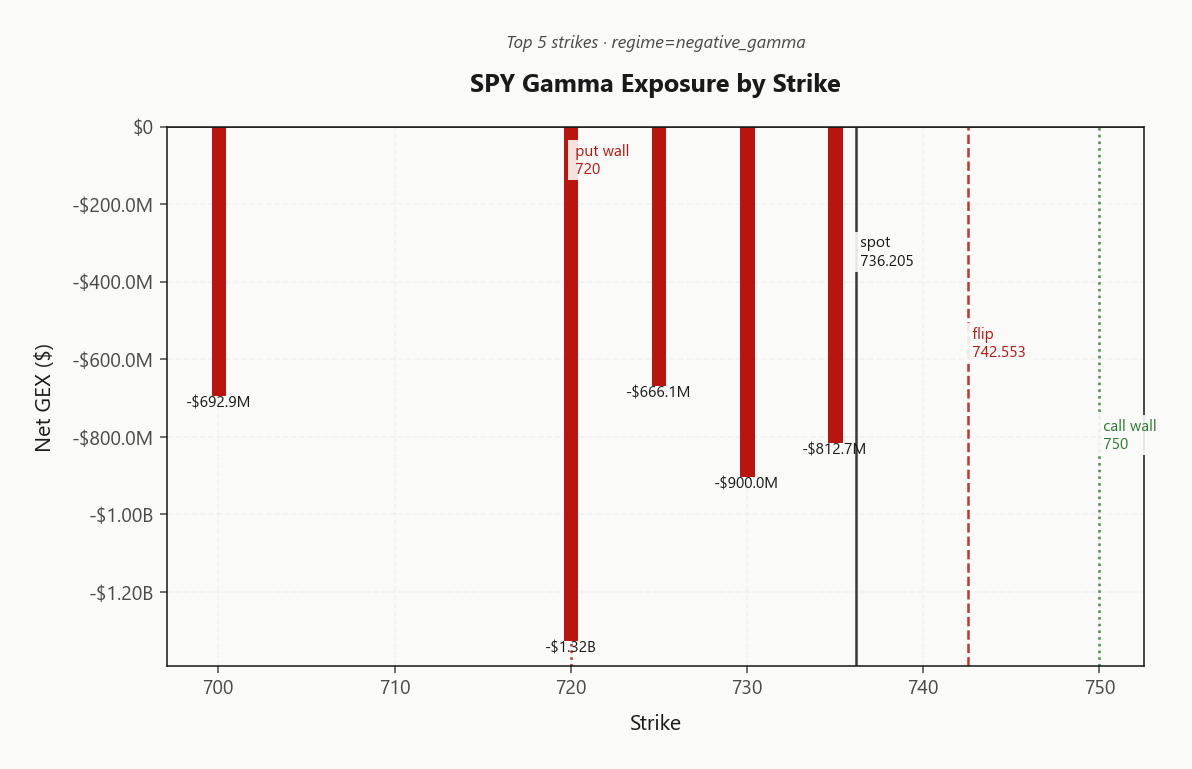

SPY at 736.21 is trading below the gamma flip at 742.55, putting dealers in a negative-gamma regime with net GEX at -$8.12B - moves get amplified, not dampened. Key levels: call wall at 750.00 caps upside, put wall at 720.00 is the next magnet on weakness, and max pain sits at 728.00. Dealer positioning is hostile: net VEX at -$67.76B means vol-up forces additional delta selling, and charm at -$6.1M pressures dealers into the close. Zero-DTE accounts for 16.6% of total gamma - meaningful but not dominant. Vol read: VIX at 20.97 (+5.54%% on Iran tape), term structure still Contango with VIX9D at 22.14 above front VIX - slight near-end backwardation despite overall contango. VRP at 6.85% vol points means options are pricing meaningful premium over realized. Bottom line: don't fade strength inside walls - in negative gamma, trend extends; harvest VRP in 30-45Iron Condor structures and treat 742.55 as the level that flips dealer flow back to supportive.

Negative gamma across index complex with VIX bid - dealers amplify moves, spot below 742.55

SPY at 736.21 sits below the gamma flip at 742.55, putting dealers short gamma across the index complex as Iran headlines bid VIX to 20.97. VIX term structure remains in contango despite the spike, and VVIX at 95.81 signals jump-risk is rising but not extreme. Setup favors carry harvest in the belly - Iron Condor in the 30-45 window - while respecting the destabilizing pivot at 742.5530643637.

Regime Assessment

Regime read: Elevated / Watchful with VIX parked at 20.97. This is the watchful zone - bid enough to respect, not bid enough to chase. The five-session transition probability into panic sits at 0.15, which says the Iran tape is largely priced, not extrapolated. Markets aren't pretending nothing happened; they're also not positioning for the binary.

Half-life on this state is 15 sessions - sticky, but emphatically not permanent. Translation: don't trade this regime like it expires tomorrow, but don't underwrite vol structures that assume it lasts through the back-month either. The belly is where the math works; the wings are where the surprises happen.

Trigger to escalate the playbook: front-end inversion. If 22.14 pulls further above 20.97, the elevated state migrates toward panic faster than the base rate suggests. Until then, stay in Iron Condor structures, respect the pivot at 742.5530643637, and let the half-life do the carrying.

What it means for your trading

Regime is Elevated / Watchful at VIX 20.97 - sticky for 15 sessions but with low 0.15 transition odds into panic. Watch VIX9D vs VIX for the early break.

Trading readVIX bid, VVIX bid, SKEW elevated - equity-vol complex confirming. MOVE flat means bonds aren't worried yet. Divergence to watch: if MOVE catches up, regime shifts from equity-event to credit-event.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The front of the curve is doing the talking. 22.14 on VIX9D printing above spot VIX at 20.97 is textbook event-premium humping - Iran headlines crammed into the next two weeks of expiries while the back of the curve refuses to flinch. VIX3M at 21.31 holds the structural Contango intact, so the carry regime underneath the hump is unbroken.

Forward 30-to-60 at 21.4779817488 prices the belly as Flat - neither rich nor cheap, the cleanest vega real estate on the surface. Edge sits on both sides of the kink: sell front-week vol where the headline tax is being paid in full, own 30-60D vega where the curve is mispriced relative to a still-elevated regime.

Calendars short the front, long the belly carry positive theta and positive vega today - the rare combination this curve hands out only when an acute catalyst is layered on a healthy term structure. Respect the Iran tape; size the front leg defined-risk.

What it means for your trading

Near-end backwardation inside a Contango curve is the Iran-headline footprint - sell the front-week hump, own the Flat belly via calendars.

Trading readContango overall but with VIX9D bid above VIX = front-end hump. Long-vol carry trade still works in the back; tactical short-vol opportunity in the front IF Iran tape calms.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 19.78% against HV20 at 12.93 opens a VRP of 6.85% vol points - options are pricing a materially bigger world than the tape has actually delivered. HV60 at 14.79 sits above HV20, which says the recent calm is a local compression inside a noisier 60-session regime, not a structural shift to a lower-vol world. Read that as: the rich IV is not chasing a phantom - it is paying you to underwrite a known fat tail.

The carry is real, but the negative-gamma backdrop dictates how you collect it. Short premium has structural edge at a VRP this wide, yet selling it naked into a short-gamma tape with the Iran headline overhang is the wrong place to size up - every adverse tick gets amplified by dealer hedging, not dampened. Define the risk, harvest the spread, and let the IV-RV gap do the work without inviting tail convexity onto the book.

What it means for your trading

Wide VRP at 6.85% vol points is a genuine carry edge with IV at 19.78% versus HV20 at 12.93, but HV60 at 14.79 above HV20 plus the negative-gamma regime argues for defined-risk structures over naked short premium.

Skew Convexity

Quarter-delta skew at 5.35% vol points with a smile ratio of 1.22% tells you the put wing is paying a real premium, but the surface is ordered, not panicked. Front-expiry put_25d prints 29.32% against an ATM of 26.18%, while call_25d sits down at 23.97% - the call wing is flat, no inversion, no upside chase. This is a hedger's book, not a speculator's.

SKEW index at 141.97 corroborates the tail bid without screaming dislocation. The practical read: naked downside protection is overpaying for the wing premium baked into 29.32%, so finance the hedge - put-spreads dominate naked puts on cost-adjusted carry, and ratio structures harvest the smile asymmetry without taking the flat call wing as a fade.

Bottom line: respect the steepness but exploit its shape. With call skew refusing to inflate, upside convexity is cheap relative to downside; pair short put-wing premium with long call-wing optionality to ride any reclaim of the destabilizing pivot without paying for protection twice.

What it means for your trading

Put skew at 5.35% is steep but ordered while the call wing stays flat at 23.97% - finance downside protection via spreads, and treat cheap upside convexity as the asymmetric leg.

Vol-of-Vol Structure

VVIX at 95.81 against VIX at 20.97 prints a ratio of 4.57 - squarely in Normal territory. Jump risk is bid on the Iran tape but the second derivative is not pricing a binary regime; the convexity market is paying attention, not panicking.

That distinction matters for sizing. With vol-of-vol contained, derived guidance reads Standard Size - short-premium structures don't need to be cut down here, and the wide VRP can still be harvested through the belly. The risk is that VVIX is the early-warning system: a step-function move above current ratio would force a sizing cut before VIX itself confirms.

Keep the book at normal weight but don't run naked. Cheap OTM convexity - back-month vega tails or far-wing call flies - remains warranted while the geopolitical tape is live. You're paid to carry through Iron Condor in 30-45, not to short gamma into a headline.

What it means for your trading

Vol-of-vol sits in normal range with the VVIX/VIX ratio at 4.57, supporting Standard Size on short-premium books - but hold cheap tail convexity against the Iran tape.

Dispersion Spread

Index ATM IV at 19.78% is doing a lot of pretending. The Mag-7 GEX shifts dominate today's tape - NVDA, AAPL, GOOGL leading the positive deltas - yet SPY vol stays anchored as if the index were one homogeneous beta. It isn't. When single-name realized in the complex is running hot but the index hedge is priced for calm, you're being handed cheap idiosyncratic optionality wrapped inside an expensive-looking index print.

The trade is long single-name vol, not short SPX. Straddles into earnings windows on the Mag-7 names harvest dispersion convexity that the index simply cannot express - correlation has to collapse for the basket to stay quiet while components move. Sell SPX strangles only at standard size; the Iron Condor in the 30-45 window is the cleanest expression of the index VRP, not a license to size up.

What it means for your trading

Index ATM at 19.78% underprices the dispersion bleeding through the Mag-7 GEX rotation - own single-name gamma, rent index gamma at modest clip.

Liquidity & Microstructure

SPY trades below the gamma flip at 742.55, parking dealers in negative-gamma territory where hedges amplify rather than dampen. The book is boxed by the call wall at 750.00 and the put wall at 720.00, with the highest OI cluster at 700 anchoring the gravitational field below spot.

The top strike sits at 720.00 carrying net GEX of -$1.32B - put-heavy and squarely in the air pocket between spot and the put wall. Until 742.55 is reclaimed, weakness gets sold into; the put wall at 720.00 is the next downside magnet, not a floor to lean against.

Trade the box, not the middle: fade strength only at 750.00, and treat a reclaim of 742.55 as the regime flip back to dealer-supportive flow.

What it means for your trading

Spot below 742.55 means dealer hedging is destabilizing - the put wall at 720.00 is the next magnet, and reclaiming the flip is the only level that turns flow supportive again.

Trading readNegative gamma stacked from 720.00 through spot says dealers SELL into weakness - air pocket below until 742.55 is reclaimed. The 700 put-heavy cluster is the next downside magnet.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order greeks are stacked against the tape. Net VEX at -$67.76B is deeply negative - every tick higher in vol forces dealers to sell delta, the textbook vanna feedback loop with Iran headlines bidding VIX to 20.97. This is the accelerant, not the brake.

Charm at -$6.1M compounds it into the bell - short-dated theta bleed drags hedges in the same direction spot is already drifting, and into the close that drift biases lower. Pivot bias reads Destabilizing with spot trading underneath 742.5530643637, the gamma-flip level that gates the regime.

The trade is mechanical. Reclaim 742.5530643637 and dealer flow flips supportive - vanna and charm both reverse polarity. Fail it and the vol-up/delta-sell loop runs unimpeded into expiry. Do not size short premium naked here; harvest VRP in defined-risk Iron Condor structures in the 30-45 window and let the pivot do the work.

The cross-asset tape is telling a coherent story: MOVE at 77.03 sits benign while the equity-vol complex bids - this is a geopolitical equity event, not a credit shock. Bonds are not flinching, which caps the regime ceiling and keeps this from morphing into a systemic risk-off. The moment MOVE starts catching up to VIX is when the playbook changes from harvest to hedge.

Sentiment has already done the work: Fear & Greed at 31 prints Fear, meaning positioning has reset before the headlines fully matured. Across the index complex, QQQ at 707.12 and IWM at 287.84 sit in lockstep negative-gamma posture with SPY - divergence is Aligned, so there is no relative-value wedge to fade between the three.

Geopolitical shocks mean-revert more often than they compound. With credit calm, sentiment washed, and the equity complex aligned rather than fracturing, size the carry trade for reversion - not for the binary tail.

What it means for your trading

Cross-asset confirms an equity-vol event, not a credit event: MOVE flat at 77.03, Fear & Greed washed at 31 (Fear), and QQQ/IWM aligned with SPY in negative gamma. Size for mean-reversion; flip the script only if MOVE starts tracking VIX higher.

Scenario EV

The scoring engine ranks Iron Condor as the dominant structure at 58, edging the put-spread alternative at 56. Wide VRP at 6.85% vol points, an intact contango belly with forward 30-60 at 21.4779817488, and VVIX/VIX in normal territory at 4.57 are the three legs holding the carry thesis up. Condors here harvest the IV-over-RV spread without taking naked exposure to the negative-gamma amplification regime mapped by net GEX at -$8.12B.

The DTE window is non-negotiable: 30-45. Front-week is uninvestable with VIX9D at 22.14 printing above VIX at 20.97 - that near-end hump is pure Iran-headline premium and the gamma-flip pivot at 742.5530643637 sits hostile overhead. Back-month is equally toxic: vega beta to a VIX expansion leaves long-dated short premium exposed to the very tape that bid the term structure overnight. The belly threads it - past 0DTE event risk, short of the vega cliff.

Run standard size per the normal vol-of-vol read; reserve upsize for a clean reclaim of 742.5530643637.

What it means for your trading

Iron condor in 30-45 is the trade - wide VRP and contango belly carry the structure, while the 30-45 window sidesteps both Iran front-week tape and back-month vega beta.

Actionable Summary

Trade: harvest the rich VRP via Iron Condor structures in the 30-45 DTE window. With SPY at 736.21 sitting below the gamma flip at 742.55 and net GEX at -$8.12B, dealers amplify rather than dampen - but the belly carries cleanly because VVIX at 95.81 sits in normal territory and term structure remains Contango.

Level: reclaiming 742.5530643637 flips dealer flow from destabilizing back to supportive - that is the single number worth watching. Below it, expect drift toward the put wall at 720.00; above it, dealer buybacks accelerate into the call wall at 750.00.

Avoid: front-week naked vol into Iran headlines (VIX9D at 22.14 bid above front VIX), and long-dated vega where VIX expansion would punish the book. Step aside if near-end backwardation deepens.

Cramer's morning watchlist references Iran-Trump 'pay the price' rhetoric - that single line is what bid VIX overnight and tilted the index into negative gamma.

Germany recession risk from energy shock is the first sign Iran tape is leaking into growth expectations - if MOVE picks up here, regime shifts from equity-vol to credit-vol.

New US strikes raise the binary regime probability - keep VVIX in view as the second-derivative tell.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.63 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 742.55 against a spot of 736.21. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 19.78% with a volatility risk premium of 6.85%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 20.97. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime