Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

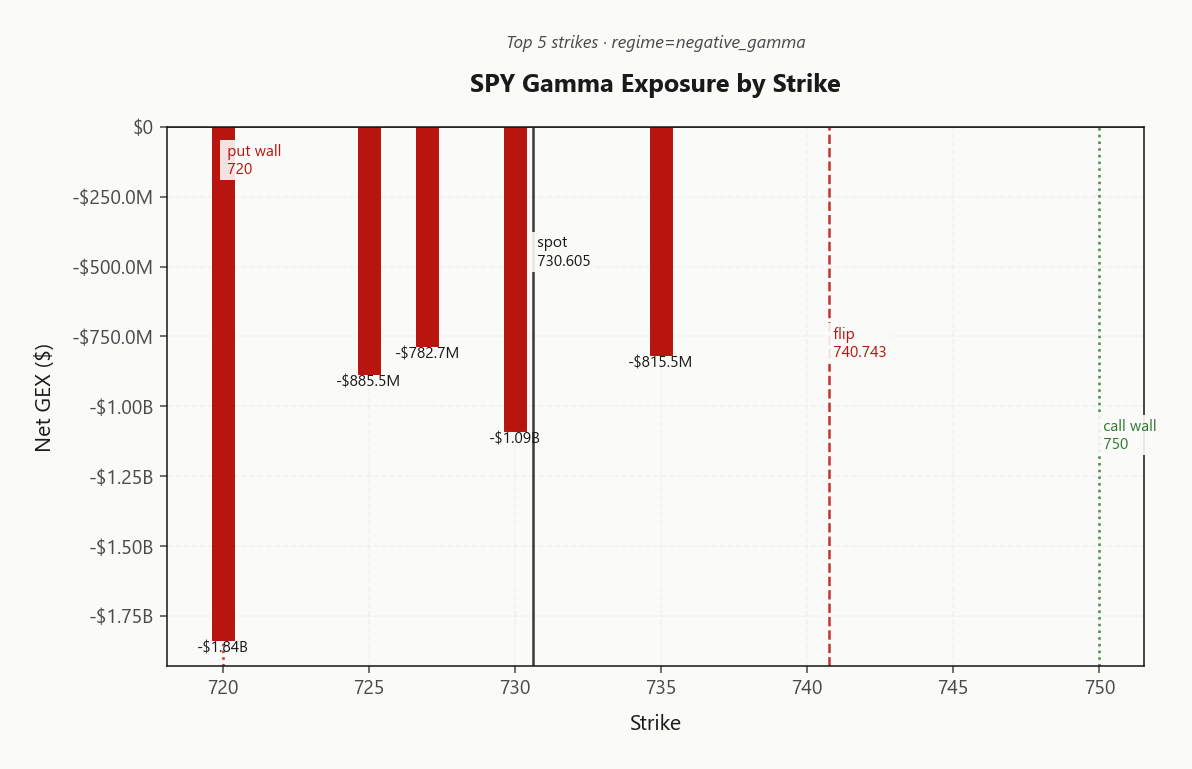

SPY at 730.61 sitting in Negative Gamma with net GEX of -$13.06B - dealers are short gamma and amplifying flow rather than absorbing it. Key levels: call wall at 750.00, put wall at 720.00, gamma flip at 740.74; spot is meaningfully below the flip so any rally toward 740.74 faces dealer selling, while breaks below 720.00 accelerate. Dealer positioning: net DEX -$6.47B with vanna at -$26.86B - vol up means dealers sell delta, a hostile feedback loop. Vol read: VIX 22.18 up 17.23%%, VVIX 108.62 also bid hard, but term structure remains in Contango - the spike is front-loaded fear, not a regime break. VRP at 8.07% vol points is rich vs RV20 of 13.28, so vol sellers get paid - but only with defined risk. Bottom line: iron condor around 728.00 max pain in the 30-45 DTE bucket is the highest-EV structure; avoid naked vol selling while VVIX is bid.

Negative gamma across index complex with VIX spiking - dealers amplify moves, fade only at walls

SPY trades below its gamma flip at 740.74 with dealers net short gamma - every tick gets amplified, not absorbed. VIX jumped 17.23%% with VVIX confirming the vol-of-vol bid, while term structure stays in contango suggesting the spike is tactical not structural. Cross-asset is aligned bearish (QQQ and IWM both in Negative Gamma), so this is a broad de-risk, not a sector rotation.

Regime Assessment

The tape sits in Elevated / Watchful territory with VIX at 22.18 - elevated, but well short of panic. Base-rate transition odds to a panic regime over the next five sessions read 0.15, while the probability of decay back to a low-vol state over ten sessions sits at 0.25. Neither path dominates; this is a watchful state, not a directional one.

Half-life of the current regime runs 15 sessions - roughly three trading weeks before mean reversion takes over. That clock favors premium harvest on the back half, but the front half rewards patience over conviction. 108.62 VVIX is the leading signal to watch: a break higher flips the regime to panic faster than spot VIX ever will, and dictates a sizing-down decision before the price action confirms it.

Operate the book as if elevated persists, not escalates. Standard sizing on defined-risk structures, no naked vol while 108.62 stays bid, and treat any VVIX expansion as the trigger - not the VIX print itself.

What it means for your trading

Elevated but contained: regime half-life of 15 sessions favors mean reversion, but VVIX - not VIX - is the binary trigger for a panic flip. Stay sized standard until that breaks.

Trading readVIX and VVIX both spiking while MOVE and SKEW flat - the divergence says this is positioning-driven equity vol, not a credit or tail-risk repricing. Watch SKEW for confirmation if this turns structural.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

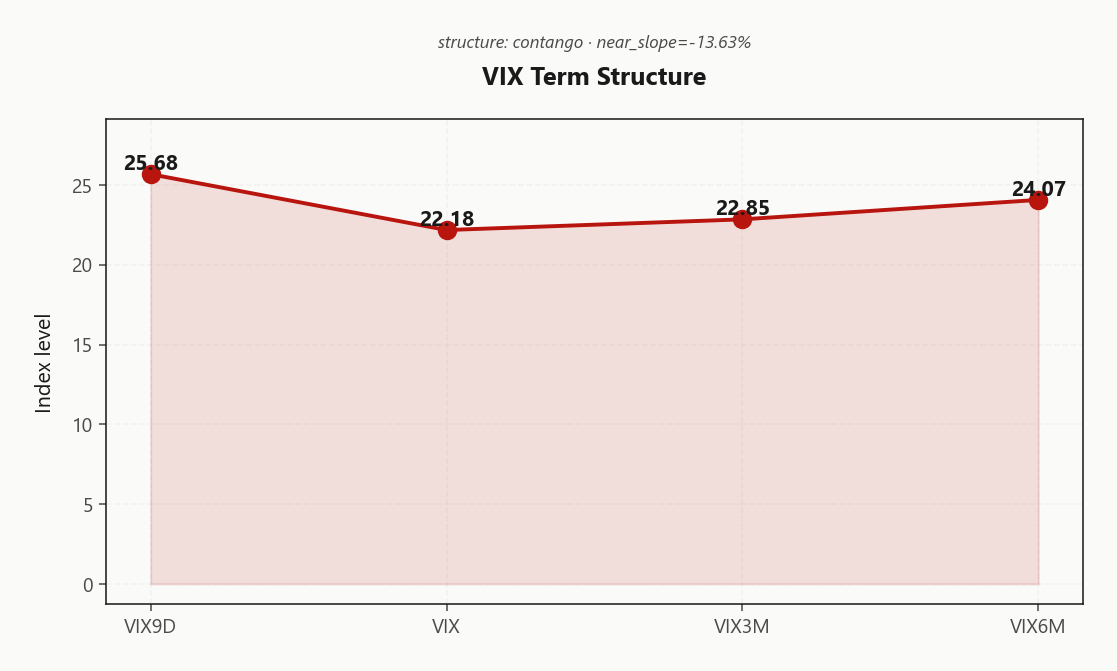

Forward Vol Geometry

Front-end stress is doing the talking: 25.68 on VIX9D prints above spot VIX at 22.18, while VIX3M holds at 22.85 - the curve is in Contango but the nine-day is paying up for tactical event risk, not a structural repricing. The back end refuses to flinch, which is the tell.

That geometry leaves forward vol from one month to two months trading cheap to spot at 23.1777382417, with the sixty-to-ninety window pricing 25.2310780586 - a clean Flat term structure read where the front decays back into the anchored belly. Short-front, long-back calendars harvest that decay directly; selling the nine-day stress and owning the three-month anchor is the cleanest expression.

Sweet spot is the 30-45 DTE bucket - far enough out to bleed the front-end premium, close enough to dodge the back-end stickiness. Regime stays Flat until VIX3M follows the nine-day higher; that's the abandonment signal.

What it means for your trading

Forward vol is cheap to spot with VIX9D above VIX and VIX3M anchored - calendar carry in the 30-45 DTE bucket is the structural edge until the back end joins the move.

Trading readContango with VIX9D above spot VIX - near-term event risk is priced, longer-dated curve unmoved. Short-front/long-back calendars on VIX futures or SPY vol both work; backwardation would be the regime-break signal to abandon them.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 21.35% sits well above 20-day realized at 13.28, with the gap echoed against 60-day at 14.93 - a 8.07% vol-point premium that screams classic VRP harvest. Options are pricing a regime the tape hasn't delivered, and until realized catches up, the carry sits on the short-vol side of the book.

Critically, RV5 hasn't accelerated above RV20 - there is no vol-of-vol expansion validating the implied bid. That asymmetry is the whole trade: premium is rich, realized is dormant, the spread is collectable. But execute it with defined risk only - negative gamma means a single accelerant print can flip RV5 hard, and naked theta books get destroyed before they get paid.

The early-warning signal is RV5 lifting toward RV20. Until then, iron condors and put-spread overlays harvest the spread cleanly; the moment short-window realized starts compounding, cut size and tighten wings before the premium re-prices.

What it means for your trading

Implied at 21.35% versus realized at 13.28 delivers a fat, collectable 8.07%-point VRP - sell premium with defined risk and watch RV5 as the kill switch.

Skew Convexity

The quarter-delta skew sits at 5.27% vol points with put 25d IV at 29.4% against call 25d at 24.13% - the left wing is paying clear premium over the right, and the bid is ordered, not panicked. Smile ratio prints 1.22%, above parity, confirming convexity demand for tails rather than a directional chase.

The chain is asymmetric: put wing well above ATM at 26.65%, call wing flat below it - no upside conviction is being expressed, only downside protection. Hedgers are reaching for convexity but doing it through structure, not raw vega. That is exactly the tape where put debit spreads outperform naked puts: you finance the rich put wing by selling the steep portion of the smile against you, capturing the skew rather than paying it.

Action: express downside through put spreads in the 30-45 DTE bucket - the skew is paying you to give up far-tail convexity you don't need.

What it means for your trading

Steep put skew at 5.27% with smile ratio 1.22% signals ordered hedging demand, not panic - sell the rich wing against your protection via put spreads rather than buying naked puts at 29.4%.

Vol-of-Vol Structure

VVIX ripped 17.55% to 108.62 in lockstep with VIX at 22.18 - vol-of-vol is bid hard, but the 4.90 VVIX/VIX ratio still prints in the Normal band. Traders are paying up to hedge the hedge, yet the relationship between near-term vol and the convexity that sits on top of it has not broken. This is fear extending, not fear capitulating.

The signal cuts cleanly into sizing: Standard Size is the correct read. Half-size is premature while the ratio holds, and full-leverage shorts are reckless while the absolute VVIX print is climbing. Keep the binary trigger explicit - a VVIX print through the upper-cohort threshold flips the regime from Normal to defensive, and that is the moment to cut gross and lean on defined-risk wings only.

What it means for your trading

Vol-of-vol followed VIX higher rather than leading it, leaving the VVIX/VIX ratio at 4.90 inside the Normal band - Standard Size stays the call until VVIX breaks materially higher.

Dispersion Spread

Index IV is bid hard with 21.35% ATM sitting well above realized, while single-name dispersion stays only moderate at 71.37 cross-strike and 2 cross-expiry - the premium is in the index, not the names underneath it.

Cross-asset is Aligned with SPY, QQQ and IWM all in Negative Gamma - a broad de-risk, not a rotation. There is no idiosyncratic story for single-name vol sellers to harvest, and correlation is doing the work index vol is being paid for.

Trade implication: SPX/SPY premium harvest screens cleaner than single-name short vol here, and hedges belong at the index level where the bid actually is. Forward vol regime reads Flat term structure, reinforcing that the richness lives in index expressions - fade dispersion trades, lean into index condors.

What it means for your trading

Index IV at 21.35% is rich while dispersion stays moderate and cross-asset reads Aligned - sell index vol, not single-name, and hedge at the index level.

Liquidity & Microstructure

The order book's center of gravity sits below spot: the highest-OI strike anchors at 700, while the dominant cluster at 720.00 carries net GEX of -$1.84B against 307353 in put OI - a defensive, hedge-heavy print rather than directional chase.

With the gamma flip perched at 740.74 well above spot at 730.61, any rally drags into dealer supply long before the regime turns supportive. The call wall at 750.00 caps the upside ceiling, while the put wall at 720.00 is the trigger - a clean break there releases dealer selling into the tape rather than absorbing it.

Translation: the microstructure is a downside magnet with no built-in mean reversion below flip. Trade the levels, not the narrative - fade rallies into 740.74, respect 720.00 as the accelerant line.

What it means for your trading

Order-book gravity sits below spot with the heaviest cluster at 720.00 dominated by put OI - rallies meet dealer supply into 740.74, while a break of 720.00 accelerates rather than absorbs.

Trading readNegative gamma stacked below spot with the dominant put wall acting as a downside magnet - dealers amplify selloffs into that strike rather than absorb them. Above the gamma flip the regime flips supportive, but spot has work to do to get there.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$26.86B - deeply negative and the hostile feedback loop is live: Vol up = dealers sell delta - downside amplified if vol spikes. With spot below the flip at 740.74, any VIX expansion from 22.18 forces dealers to sell delta into the move rather than fade it. Vanna is no longer a footnote - it's the accelerant.

Charm compounds the problem into the bell. Net CHEX at -$8.3M means Time decay pushing dealers to sell - pressure into close - time decay mechanically pushes dealer sells as the day winds down, layering drift on top of the vanna leak. The single pivot worth marking is max pain at 728; current bias reads Neutral with spot sitting -0.356553815 away. Drift toward it neutralizes flow, drift away accelerates it.

Reclaiming 740.74 is what flips dealer hedging back to supportive - and that level is meaningfully out of reach today. Until then, treat rallies as dealer supply zones and breaks below 720.00 as the release valve.

What it means for your trading

Negative VEX plus charm bleed makes dealers a one-way seller into close unless spot pins 728; the flip at 740.74 is the only level that reverses the loop.

Cross-Asset Confirmation

MOVE sits unchanged at 77.03 while VIX rips higher - credit is calm, this is an equity-only stress event. The fingerprint matters: rates vol decoupling from equity vol historically marks positioning shocks that mean-revert, not credit ruptures that compound. Aligned cross-asset regime, with QQQ at 698.91 and IWM at 284.43 both in Negative Gamma alongside SPY - broad de-risk, no rotation, no leadership cushion.

Fear & Greed prints Fear at 29 - contrarian setup territory. The historical analog for VIX-spikes-without-MOVE is a five-to-ten-session mean reversion in equity vol, provided rates stay anchored. SPY's 720.00 put wall is the gating level: hold it and the fear print becomes the fade; break it and the equity-only thesis dies as dealer selling cascades.

What it means for your trading

Aligned negative-gamma de-risk across SPY/QQQ/IWM with MOVE unchanged at 77.03 defines this as equity-only stress - historically a 5-10 session mean-reversion setup. Trade it as a fade contingent on the put wall holding, not a structural break.

Scenario EV

Scoring across structures puts Iron Condor at the top of the book with a score of 68, edging the put spread alternative at 66. With VRP Unknown and VVIX bid but contained at 108.62 against VIX 22.18, the wing-defined condor harvests premium without taking the naked tail - exactly the structure for elevated-but-not-panic vol-of-vol.

The 30-45 DTE bucket is the sweet spot: far enough out that 0DTE gamma whip doesn't chew through deltas, close enough that front-end IV decays into the back-end Contango curve. Anchor the body around 728.00 max pain with wings outside 750.00 and 720.00 - the dealer walls do the work of containing the body.

Sizing: standard. VVIX/VIX ratio reads Normal, so Standard Size is the playbook. Put spread is the directional-tilt fallback if conviction shifts bearish; otherwise condor wins on expected value.

What it means for your trading

Iron condor at 68 beats put spread at 66 in the 30-45 DTE window - defined-wing VRP harvest is the highest-EV trade while VVIX stays Normal. Half-size only if VVIX breaks higher.

Actionable Summary

SPY sits in Negative Gamma with spot below the gamma flip at 740.74 - dealers amplify, not absorb. Net VEX of -$26.86B means any further VIX expansion forces dealer delta sales, while charm pressure drifts the tape into close. The single pivot is max pain at 728; rallies into the call wall at 750.00 meet supply, breaks of the put wall at 720.00 release acceleration.

DO: harvest the rich VRP with an Iron Condor in the 30-45 DTE bucket, anchored on max pain. Short-front / long-back calendars also score well while the curve holds Contango. AVOID naked vol selling with VVIX at 108.62 bid, and avoid chasing rallies into the call wall - that is dealer sell territory.

WATCH: a break of the put wall is the downside acceleration trigger; a VVIX expansion past the panic threshold is the signal to half-size. Regime read: Elevated / Watchful, cross-asset Aligned.

What it means for your trading

Defined-risk vol harvest around max pain in the 30-45 DTE window is the highest-EV trade while SPY sits below 740.74; the put wall at 720.00 is the line that flips this from harvest to hedge.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.63 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 740.74 against a spot of 730.61. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 21.35% with a volatility risk premium of 8.07%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 22.18. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime