Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

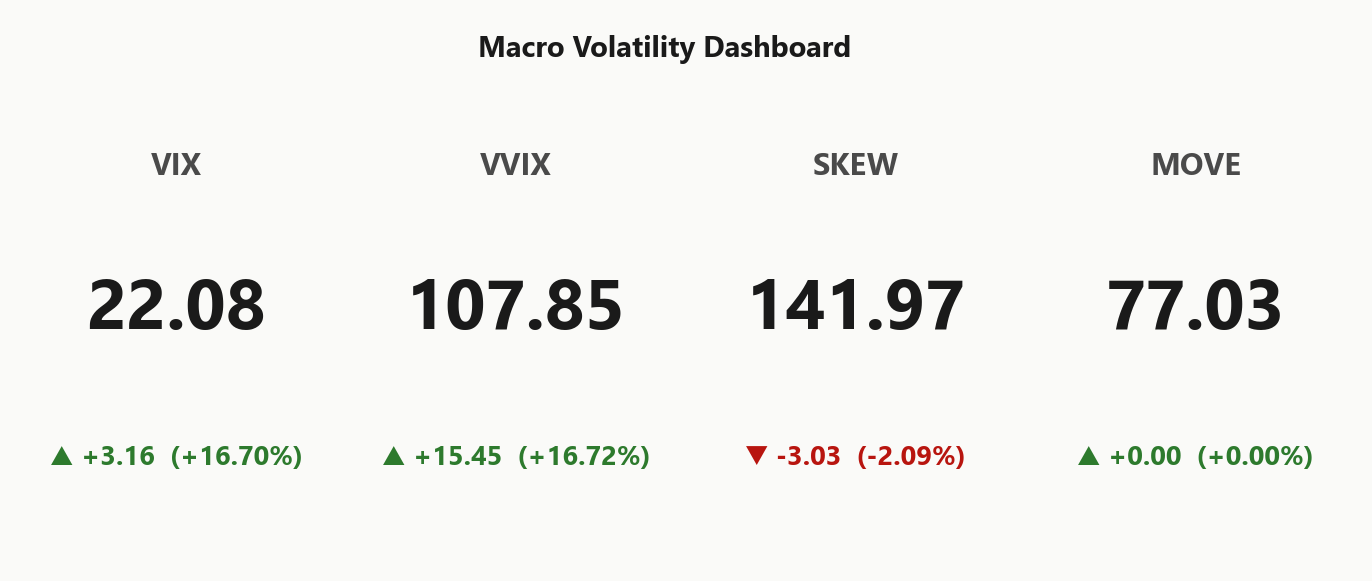

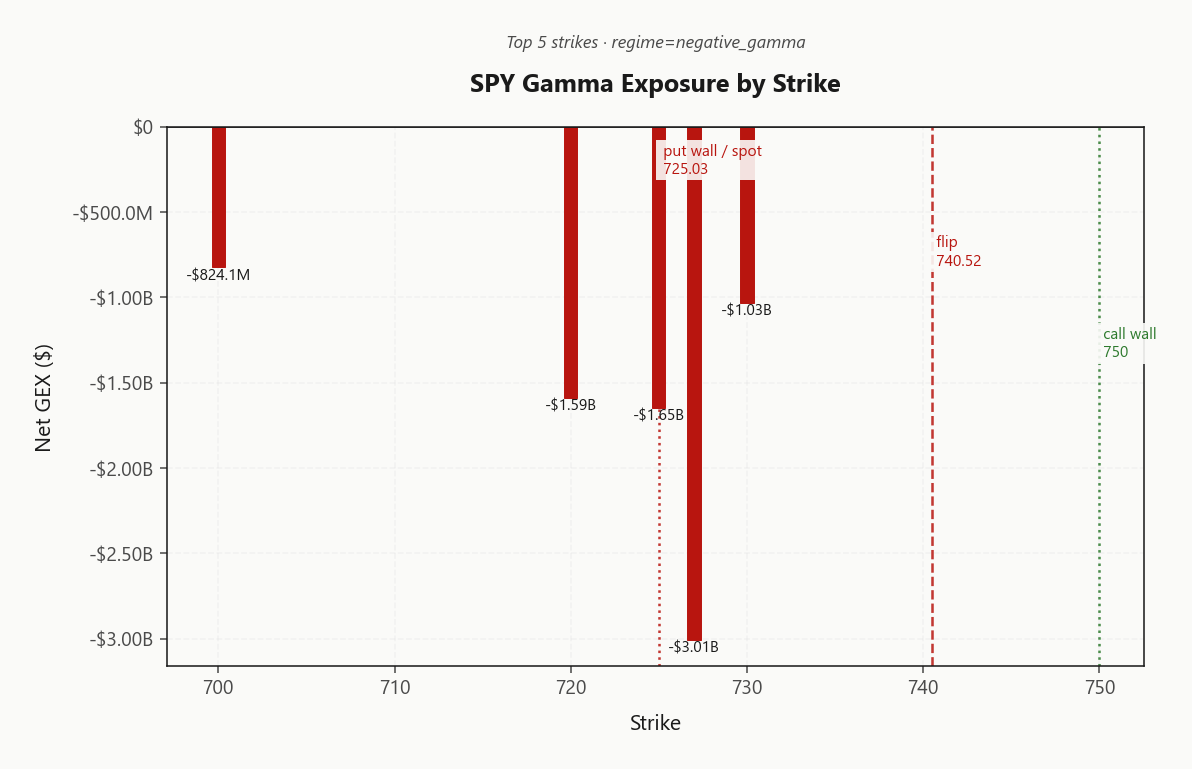

SPY at 725.06 sitting right on the put wall 725.00, with net GEX at -$17.79B - firmly negative gamma, dealers are pro-cyclical hedgers today. Gamma flip sits at 740.52 (above spot), call wall 750.00, max pain 728.00 - anything below the put wall is open air toward 700. Dealer delta-hedging on a 1% down move is -$17.79B of selling - that's the amplifier. Vanna is supportive on a vol spike (dealers buy delta as IV rises) but charm is hostile into the close per Time decay pushing dealers to sell - pressure into close. VIX at 22.08 (+16.7%%) with VVIX at 107.85 (+16.72%%) - vol-of-vol popping faster than vol itself, jump risk is priced. Term structure Contango on the long end but VIX9D > VIX = front-end stress. VRP at 8.44% says options still rich to realized - premium sellers paid, but size down. Trade: iron condor 30-45 DTE per Iron Condor, AVOID selling naked puts below 725.00, watch 740.52 as the regime flip back to dampening.

Negative gamma across index complex with elevated VIX and Flat term structure term - dealers amplify, not dampen

SPY tagged the put wall at 725.00 with dealers firmly in negative gamma below the 740.52 flip, meaning every push lower gets amplified by hedging flows. VIX jumped to 22.08 alongside VVIX at 107.85, and the near-term term structure inverted relative to spot (25.48 > 22.08) while the longer curve holds Contango. Bottom line: reactive regime, fade rallies into the call wall, respect breaks of the put wall as accelerant triggers.

Regime Assessment

Tape sits in Elevated / Watchful with VIX printing 22.08 - not panic, but not a regime that resolves on a single green close. The Markov math is the tell: transition probability to panic over five sessions runs 0.15 while the return path to low-vol over ten sessions sits at 0.25. Asymmetric stickiness - the door out is narrower than the door deeper in.

Half-life of 15 sessions is the number to internalize. This is a two-to-three-week regime, not a two-to-three-day flush. Position sizing, DTE selection, and hedge ladders should all be calibrated to persistence, not mean-reversion-by-Friday. The base case is grind: elevated VIX, dealers pro-cyclical below the flip, premium rich enough to harvest with discipline.

The model's blind spot is the binary - Iran headline escalation breaks the half-life curve entirely and re-prices the panic transition in a single tape. Trade the persistence case, but hold cheap convexity for the tail the regression can't see.

What it means for your trading

Elevated / Watchful at VIX 22.08 is sticky, not transient - half-life 15 sessions argues for sized-for-persistence positioning with tail hedges against the binary headline that the transition model cannot price.

Trading readVIX and VVIX both up double-digit percent while MOVE sits flat - bonds-don't-care-yet divergence. That's the relief tell: if MOVE breaks higher, the regime shifts from geopolitical-equity to credit-systemic, and that's when you cut all short-vol.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

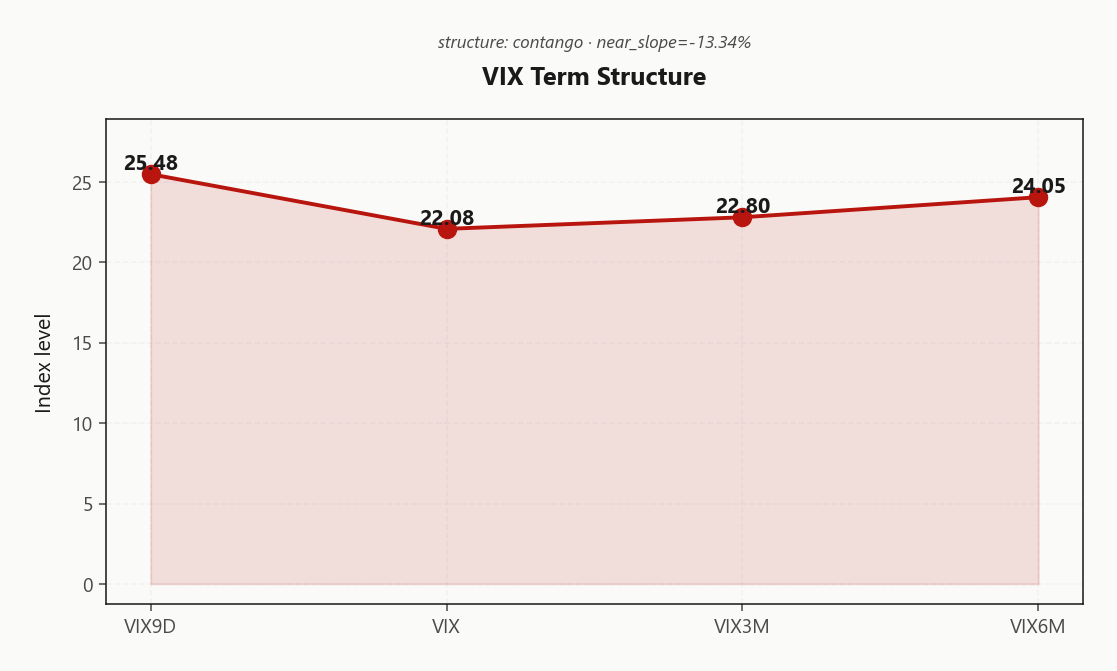

Forward Vol Geometry

Front end is paying event premium: 25.48 on VIX9D prints above spot VIX at 22.08, an inversion that compresses into the next two-week window where Iran and CPI sit. Walk out the curve and the picture flips - VIX3M at 22.80 and VIX6M at 24.05 hold Contango, so structural carry past the front month is intact.

Forward 30→60 at 23.151604696 against a Flat term structure regime (Flat) telegraphs the roll-down: if the event window resolves, the front collapses into the belly and calendars long the back, short the front of the inversion get paid twice - on time decay differential and on curve normalization.

Cleanest harvest window sits at 30-45 DTE, past the inverted nose and into the contango shoulder where premium decays against a structurally downward-sloping forward. Inside two weeks you are short event gamma against a bid front - outside thirty days you are long roll-down against intact carry.

What it means for your trading

Front-end inversion (VIX9D > VIX) is binary-event pricing layered on a Contango belly - fade the nose, harvest at 30-45 DTE where the curve normalizes and forward 23.151604696 embeds the roll-down.

Trading readLong-curve Contango confirms structural carry is intact, but front-end inversion (VIX9D > VIX) signals event premium. Carry trade lives 30+ DTE; near-dated short-vol is fighting the inversion.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 22.51% sits well clear of realized - HV20 at 14.07 and HV60 at 15.21 leave a VRP of 8.44% on the table. Sellers are still being paid, but the cushion is compressing as today's Iran-driven gap drags HV20 toward implied. The premium edge persists only if spot stabilizes from here.

The HV20 - HV60 gap tells the tape: short-window realized is accelerating faster than the longer lookback, so the surplus you're harvesting today narrows by the print tomorrow. Index-level VRP harvest remains the cleanest expression, but with VVIX velocity hot, size discipline is non-negotiable - half-clip what the spreadsheet says, then re-rack.

Cross-check the single-name layer before committing: 10.82% in QQQ runs richer than SPY's 8.44%, while IWM at 9.09% trails on rates-channel drag. Best premium-to-risk lives in QQQ 30 - 45 DTE; SPY is the macro hedge layer, not the alpha layer today.

What it means for your trading

Index VRP at 8.44% still pays, but with HV20 14.07 closing the gap to implied 22.51%, harvest only what stabilization confirms - and prefer QQQ's richer 10.82% over SPY for the cleaner short-vol expression.

Skew Convexity

Quarter-delta skew prints at 3.28% with a smile ratio of 1.13% - the left tail is bid, but the shape is ordered, not panicked. Put 25d IV at 29% trades meaningfully through ATM at 27.1%, while the call wing sits flat at 25.72% - zero upside conviction priced, all the convexity is on the downside wing.

That asymmetry is the trade structure: downside premium is rich enough that naked puts overpay for protection already embedded in the surface. Put spreads dominate - short the steep wing, finance the long leg with the same fat skew, and you stop renting tail vol you don't need. The smile ratio holding below capitulation thresholds says this is hedging flow being absorbed in order, not forced de-grossing.

The bigger tell sits in VIX call skew, not SPX put skew - index put skew steepens on every shock, but negative SKEW (the VIX call wing bidding) is what flags genuine regime panic. Until that breaks, treat the SPY surface as Skew Steep: convex, but tradeable from the short-wing side.

What it means for your trading

Skew is steep and ordered - put 25d IV at 29% versus call 25d at 25.72% argues put spreads over naked puts, with the flat call wing confirming no upside conviction is being paid for.

Vol-of-Vol Structure

VVIX printing 107.85 (+16.72%%) while VIX sits at 22.08 - vol-of-vol is accelerating faster than vol itself, the textbook signature of binary jump pricing. The market isn't repricing a drift higher in realized; it's paying up for the tail of an Iran/CPI bimodal outcome.

VVIX/VIX ratio at 4.88 still sits in Normal territory - the green light per Standard Size hasn't flipped. But the velocity of today's move overrides the static ratio read: the right play is half-size short-vol until VVIX cools, not full size on the green signal. Discretion beats the model when the second derivative is this hot.

The flip side: long-vol convexity - VIX calls, VVIX as proxy - is structurally underpriced relative to the day's drift. If you're carrying iron condors, owning upside vol convexity against them is cheap insurance into the headline tape.

What it means for your trading

VVIX/VIX at 4.88 keeps the regime in Normal band, but today's vol-of-vol velocity overrides the static signal - half-size short-vol and own VIX call convexity as the cheap hedge.

Dispersion Spread

The dispersion trade is the cleanest harvest in this tape. QQQ ATM IV at 34.99% runs hot against SPY at 22.51% - that gap is AI-name idiosyncratic risk leaking into the index wrapper, not a macro repricing. Selling index vol over single-name vol captures the premium without paying the headline tax on any one mega-cap.

With VVIX bid and the equity complex regime Aligned, single-name short-vol is the wrong side of the binary - one NVDA or META gap eats a quarter of harvest. SPY/SPX spreads the same premium across the basket and lets dealers absorb the idiosyncratic tail. Cross-strike dispersion is compressed; the wings are not paying for distortion, so condor geometry beats strangle geometry at every DTE.

IWM ATM IV at 32.18% sits in its own lane - credit and rates sensitivity, not equity dispersion. Don't conflate the IWM bid with the QQQ bid; they trade different shocks and want different structures.

What it means for your trading

Sell SPY at 22.51% against the richer QQQ at 34.99% - index-level harvest, not single-name. Treat IWM at 32.18% as a separate rates/credit book, not part of the dispersion trade.

Liquidity & Microstructure

The book is anchored by a heavy OI cluster at 700, with the top strike at 727.00 carrying 46009 contracts and -$3.01B of negative gex - a magnet, not a barrier. With spot trading below the gamma flip at 740.52, dealers are pinned in amplifier mode; every tick lower compounds the hedging feedback rather than dampens it.

The structural levels frame the day cleanly. 740.52 is the regime line - a close above flips dealers back into a dampening posture and kills the pro-cyclical hedging dynamic. 725.00 is the line between ordered selling and an air pocket; hold it and dispersion stays contained, lose it and the highest-OI magnet at 700 becomes the next reference. The 750.00 call wall caps upside fades.

Trade the band, not the breakout. Fade strength toward 750.00, respect any decisive break of 725.00 as accelerant, and treat reclaim of 740.52 as the all-clear signal.

What it means for your trading

Spot sits below the gamma flip at 740.52 with the put wall at 725.00 as the binary level: hold it and dealers grind, lose it and the OI magnet at 700 opens up.

Trading readNegative gamma blanket from the put wall through the highest-OI strike means dealers amplify every move in that band - fade strength toward the call wall, but respect any break below the put wall as accelerant territory, not a fade.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vex sits at $12.18B - firmly positive, which means any vol spike force-feeds dealer delta buying back into the tape. That's the cushion under price: if IV pops, vanna pulls dealers long, and downside gets dampened mechanically. Per Vol up = dealers buy delta - downside dampened if vol spikes, the support is real - but it's contingent. Crack the vol, and the cushion goes with it.

Net read: vanna gives you a downside floor on vol spikes, charm caps every bounce into the bell. Trade the chop, don't chase the rip, and treat a clean break of 725 as the directional tell - not the prints around it.

What it means for your trading

Positive vex cushions downside on IV jumps while negative chex bleeds rallies into the close - directional conviction lives on the right side of the charm pivot at 725, currently Neutral.

Cross-Asset Confirmation

MOVE pinned at 77.03 is the tell: bond vol isn't confirming the equity tape. This is a geopolitical-equity shock, not a credit shock - and that distinction governs how the next five to ten sessions unwind. Absent a MOVE break higher, the Iran-driven risk premium mean-reverts on the historical clock for headline events.

Across the complex, regimes are Aligned: SPY, QQQ at 693.02, and IWM at 281.78 all sit in negative gamma together. No divergence to fade, no early-warning dissenter - when the complex moves as one, you follow the dominant flow rather than hunt for the leak. The break, if it comes, surfaces first in IWM where rates sensitivity compounds the equity vol layer.

Fear & Greed prints 28 (Fear) - stressed but not yet capitulatory. The contrarian setup arms only if MOVE stays anchored and the gauge pushes deeper. Until then: respect the regime, don't pre-empt the bounce.

What it means for your trading

MOVE flat + Aligned equity regimes = geopolitical premium that mean-reverts in 5 - 10 sessions absent credit damage; watch MOVE as the kill-switch on any short-vol harvest.

Scenario EV

Structure of the day: Iron Condor prints at score 60, optimal window 30-45 DTE. The trade earns its keep three ways - VRP is active, the VVIX/VIX ratio sits in Normal band at 4.88, and the Contango belly funds roll-down past the front-end inversion.

Score gap matters: iron condor 60 vs put spread 56 is thin enough that the runner-up earns the call only if positioning already runs short delta. Otherwise the two-sided structure captures the curve normalization without paying for directional conviction the tape isn't offering. Sizing follows Standard Size discipline - but velocity of today's VVIX print argues for half-size despite the green band.

Avoid short strangles: left-wing risk on Iran headline escalation is uncompensated when MOVE is anchored and oil-corridor risk sits live. Iron condor wings cap that tail; naked strangles do not.

What it means for your trading

Recommended: Iron Condor at 30-45 DTE, half-sized given VVIX velocity - the 60/56 score gap rewards two-sided premium harvest over directional bets while the Contango curve funds roll-down.

Actionable Summary

Bottom line: Elevated / Watchful regime with SPY pinned in Negative Gamma and VVIX at 107.85 means premium sales stay on the menu - but with discipline, not aggression. The scoreboard says Iron Condor at 30-45 DTE wins on score 60 versus the put-spread runner-up at 56, with the curve roll-down funding the carry past the front-end inversion.

The directional tell is the charm pivot at 725 (Put Wall) - current bias Neutral. Watch the gamma flip at 740.52: a close back above it flips dealers from amplifier to dampener. Below the put wall at 725.00 is open air toward the OI magnet at 700 - respect the break, do not fade it.

DO: iron condors at 30-45 DTE, half-size; own VIX call convexity as cheap insurance against MOVE-flat geopolitical drift. AVOID: naked short puts below 725.00, short strangles, single-name premium harvest.

What it means for your trading

Sell index premium structured as Iron Condor in the 30-45 DTE belly where the curve normalizes, sized half given VVIX velocity. The gamma flip at 740.52 is the regime switch and the put wall at 725.00 is the accelerant line - trade around them, not through them.

Trump threatening 'very hard' Iran attack is the singular driver of today's VIX spike and the equity-complex regime flip - this is the binary catalyst sitting under every dealer hedging decision into the close.

Israeli strikes in southern Lebanon widen the Middle East risk surface - markets now pricing not just Iran but full regional escalation, which is what's keeping VVIX bid even as MOVE stays anchored.

US strike on tanker off Oman shows the Hormuz oil-corridor risk is now active, not theoretical - energy supply premium becomes a persistent overlay on equity vol pricing.

Sanctions on China/HK entities over Iran weapons opens a secondary axis: this geopolitical event has US-China spillover potential, which compounds the equity risk premium beyond pure oil.

CPI breaking above 4% on energy-driven inflation is the policy-channel transmission - Fed reaction function gets harder, which is why the back of the vol curve held its bid even as the front spiked.

OPEC output at multi-decade lows tells you the supply-side cushion is gone - any further Iran disruption translates 1-for-1 into oil prices, keeping equity left-tail bid for weeks not days.

Multiple notes about institutional cash-raising flagged today - confirms the supply of marginal buyers is thinning right when dealers need them most below the put wall.

Institutional cash-raise ahead of SpaceX IPO volatility signals positioning de-risking is structural, not just reactive - adds to the persistence case for the elevated regime.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.63 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 740.52 against a spot of 725.06. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 22.51% with a volatility risk premium of 8.44%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 22.08. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime