Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

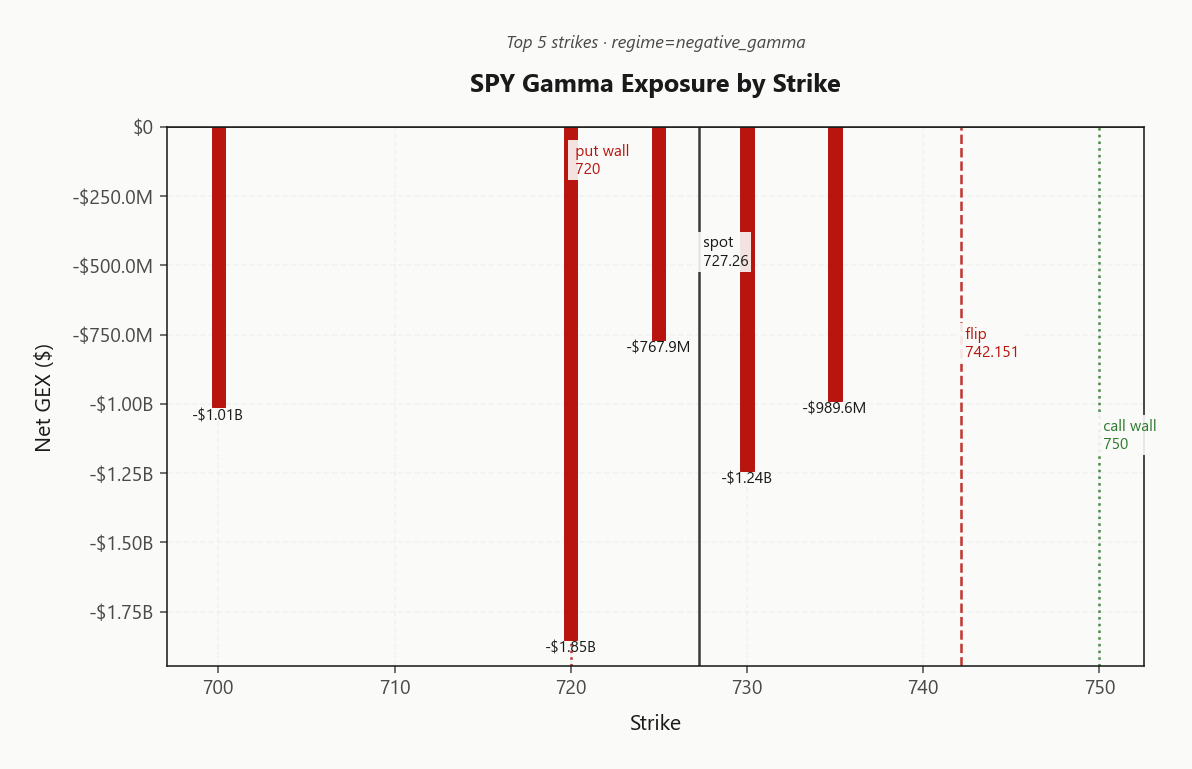

SPY trades at 727.26 in a negative gamma regime with net GEX of -$14.68B - dealers are short gamma and will amplify directional moves. Key levels: gamma flip sits at 742.15 (spot below = amplification zone), call wall 750.00 caps rallies, put wall 720.00 is the immediate downside magnet, max pain 730.00. Dealer positioning is hostile: net DEX -$29.5B means they're short delta and vanna -$330.2M says vol-up triggers more selling - a feedback loop. Vol read: VIX 21.33 popped 12.74%%, VVIX at 98.54, term structure Contango with VIX9D at 24.06 signaling front-end stress. VRP positive at 6.38% so options are still paying over realized 14.14. F&G at 29 (Fear). Bottom line: don't fight the tape below 742.15 - sell defined-risk premium (Iron Condor) in the 30-45 bucket, fade strength into 750.00, watch 720.00 for breakdown acceleration.

Negative gamma across index complex with VIX spiking; dealers amplify moves below 742.15

SPY at 727.26 sits below the gamma flip at 742.15 with dealers short gamma across SPY, QQQ, and IWM - moves get amplified, not dampened. VIX at 21.33 jumped 12.74%% while term structure stays in contango, signaling acute near-dated stress without a regime break. VRP remains positive at 6.38%, making defined-risk premium selling the cleanest expression while spot consolidates between 720.00 and 750.00.

Regime Assessment

Regime prints Elevated / Watchful with VIX anchoring at 21.33 - not a panic tape, but no longer benign. Half-life of 15 sessions says this state is neither sticky nor fleeting: moderate persistence, with mean-reversion as the dominant attractor rather than acceleration into crisis.

The distribution is asymmetric in our favor. Transition probability to panic over the next handful of sessions sits well below the probability of normalization over the following two weeks - more upside in expected value than downside, with the cross-asset tape Aligned rather than fragmenting. That is the configuration premium harvesters want: elevated but contained, with the path of least resistance bending back toward the low-vol regime as front-end stress resolves.

Size accordingly. The trade is not predicting the panic transition - it is surviving one if it arrives. Standard sizing on defined-risk structures, with cheap convex tails carried as insurance rather than expression.

What it means for your trading

Regime is Elevated / Watchful at VIX 21.33 with a 15-session half-life - base case favors normalization over panic, so harvest premium but size for survival, not prediction.

Trading readVIX/VVIX up while MOVE and SKEW unchanged is the divergence to watch - equity vol leading without bond vol confirmation usually mean-reverts within 5-10 sessions.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

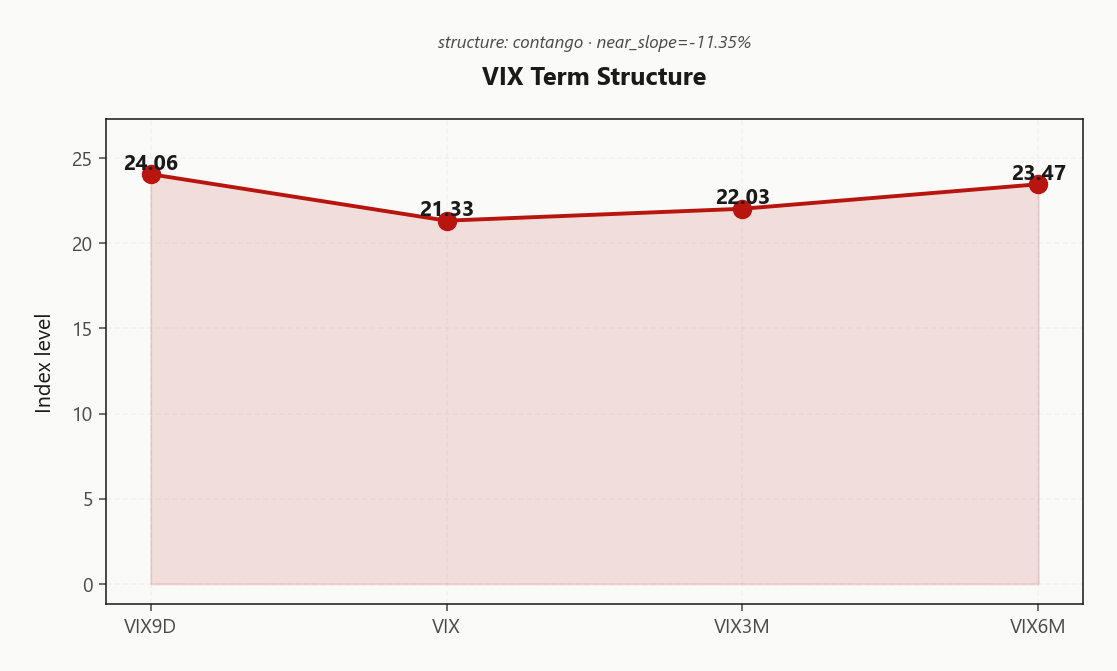

The curve tells two stories at once. 24.06 on VIX9D printing above 21.33 spot VIX is textbook front-end backwardation - the tape is paying up for the next nine sessions of event risk. Yet thirty-day to three-month holds Contango with VIX3M at 22.03, so this is acute, not structural. No regime break, just a kink at the front.

That kink defines the trade. Forward thirty-to-sixty sits cheaper than forward sixty-to-ninety, which means the belly is the structural air pocket - exactly where carry compresses fastest once the front-end stress resolves. The aggregate read is Flat, and a flat back with a bid front is the cleanest setup to harvest mean-reversion in the middle without wearing the gamma of the wing.

Operationally: sell the belly, skip the weeklies. Front-end premium is paying for a reason and shorting it naked into an inverted nine-day is how books blow up; the thirty-to-forty-five DTE bucket is where the curve flattens and the roll-down works for you rather than against you.

What it means for your trading

Front-end inversion inside back-end Contango concentrates event premium in the next nine sessions while leaving the belly structurally cheap - sell 30-45 DTE, avoid weeklies until VIX9D recouples to 21.33.

Trading readContango at the back with front-end inversion = market pricing event risk in the next two weeks, not a structural regime change - short the bump on resolution.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 20.52% sits comfortably above 20-day realized of 14.14 and 60-day at 15.32, leaving VRP firmly bid at 6.38%. Options remain expensive relative to what the tape has actually delivered - the carry edge is intact even as today's drawdown pulls short-window realized higher.

The mechanical convergence is coming: RV5 will rip toward RV20 as today's range gets absorbed into the lookback, compressing the spread before the back-end catches up. That telegraphs the trade - harvest the premium now in defined-risk wrappers rather than chasing it after realized completes the migration. Naked short vol is the wrong expression with vol-of-vol bid; the Iron Condor in the 30-45 DTE belly captures the rich middle without exposing the book to a VVIX leg-up.

VRP assessment reads Unknown but the IV-RV gap speaks plainly: premium is still paying over realized, and defined-risk is the only acceptable wrapper while spot sits below 742.15.

What it means for your trading

IV at 20.52% over realized of 14.14 keeps premium harvest viable, but only through defined-risk structures like Iron Condor given the vol-of-vol bid.

Skew Convexity

The quarter-delta put is bid hard at 30.76% against an ATM of 27.93%, pushing the put-over-ATM premium to 4.99% vol points. That is ordered demand for downside, not panic chasing - the wing is being accumulated by hedgers as VIX rips and dealers sit short gamma below the flip.

The smile ratio at 1.19% confirms the bimodal read: wings are pricing distribution risk while the body stays anchored. Call quarter-delta IV at 25.77% sits below ATM - zero upside conviction, no chase bid, calls are the cheap side of the surface.

Trade the asymmetry, don't fight it. Naked downside is rich; put spreads finance the bid wing with the steepening curve and cap the vega bleed if VIX rolls. Skip outright OTM puts here - you are paying the skew tax twice. Call ratios and call calendars are the structurally cheap expression on any reclaim attempt.

What it means for your trading

Steep skew of 4.99% with smile ratio at 1.19% says the left tail is being repriced while the right tail is given away - sell the wing through spreads rather than buying it outright.

Vol-of-Vol Structure

VVIX at 98.54 printed a 6.65% move against VIX at 21.33, leaving the vol-of-vol read squarely in the Normal band. The ratio sits in territory consistent with orderly hedging demand rather than a binary repricing - the tape is paying for protection, not panicking over the next shock.

Translation for the book: Standard Size on defined-risk premium structures. There is no convexity premium yet that forces de-risking, but the cushion is thin. A VVIX print through the triple-digit threshold - call it the half-size trigger - would tell you the market is starting to price the vol path itself, not just spot, and that is when iron condors get re-sleeved smaller.

Until then, harvest the belly with standard clip. The signal is watchful, not defensive.

What it means for your trading

VVIX at 98.54 versus VIX 21.33 keeps vol-of-vol Normal - Standard Size on premium structures, with the ratio the single tell that would force a half-size pivot.

Dispersion Spread

Index-level IV holds firm at 20.52% while single-stock correlation tightens into the tape - a macro-driven, positioning-led selloff where every name rhymes with the index. With SPY, QQQ, and IWM all flagged Aligned in negative gamma, the dispersion canvas inverts: index hedges underperform single-name protection because cross-correlation is rising, not the basket's idiosyncratic variance.

Dispersion structure reads Moderate with cross-strike dispersion at 68.4 and cross-expiry at 2.39 - informative but not actionable until correlation eases. Short-gamma macro stress is the wrong regime to be long single-name vol versus short index vol; the implicit correlation leg bleeds against you on every additional VIX tick.

Trade the index, not the basket. Prefer SPX/SPY premium selling on bounces - Iron Condor in the 30-45 bucket - and shelve dispersion until VVIX rolls and the correlation premium decays back toward neutral.

What it means for your trading

Rising realized correlation makes dispersion structurally unfavorable here; sell index vol on bounces via Iron Condor, and wait for VIX/VVIX normalization before re-engaging long-single-name / short-index dispersion.

Liquidity & Microstructure

The book pins around the 700 open interest anchor with the heaviest gamma cluster stacked at 720.00, where net GEX prints -$1.85B - the put magnet that any further weakness gravitates toward. Spot at 727.26 sits underneath the gamma flip at 742.15, locking dealers into the amplification zone where hedging flows reinforce rather than dampen direction.

The structural map is tight: 720.00 is the downside magnet and the line where short-gamma hedging accelerates, while 750.00 caps any reflex bounce. Reclaim of 742.15 is the single regime trigger - above it, dealer flow flips back to mean-reverting and the tape mechanically calms. Until then, fade strength into the call wall and respect the put wall as an acceleration trigger, not support.

What it means for your trading

Below the flip at 742.15, dealer hedging amplifies every move toward the 720.00 put magnet; reclaiming the flip is the only mechanical signal that turns dampening flows back on.

Trading readDeep negative gamma stacked at the put wall says dealers amplify every dollar lower - until spot reclaims 742.15, fading bounces into the call wall is the higher-EV play.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX sits deeply negative at -$330.2M - the vanna feedback loop is active and hostile. Every tick higher in 21.33 forces dealers to sell more delta, which pressures spot, which lifts vol further. With VIX up 12.74% on the session and spot below the gamma flip at 742.15, this is the textbook accelerant regime - size accordingly.

Charm offers thin counterweight: net CHEX prints at $4.3M, supplying token end-of-day decay support, but the magnitude is dwarfed by the vanna pressure. Do not lean on charm as a stabilizer if 21.33 keeps climbing into the bell. Pivot bias reads Neutral around max pain at 730.00 - the natural magnet absent fresh vol expansion.

Trade implication: keep structures defined-risk, fade strength into 750.00, and treat any further leg higher in 98.54 as a forced-selling catalyst rather than noise.

What it means for your trading

Negative vanna at -$330.2M dominates token-positive charm at $4.3M - dealers will sell into any vol expansion, leaving max pain 730.00 as the only natural pivot if 21.33 rolls over.

Cross-Asset Confirmation

The cross-asset tape isolates the stress: MOVE sits at 76.98 while VIX rips to 21.33 - equity vol leading without rates or credit confirmation. That divergence is the tell. When bond vol stays anchored through a double-digit VIX print, the shock is positioning-driven, not a macro regime break. QQQ at 693.08 and IWM at 279.80 are aligned negative-gamma with SPY, so the fragility is uniform across the equity complex but quarantined there.

Fear & Greed prints 29 (Fear) - positioning fear without panic capitulation, exactly the contrarian-constructive band where defined-risk premium harvest historically pays. Cross-asset regime read is Aligned: no safe-haven flight, no credit transmission, just an equity-localized unwind looking for an exhaustion print.

Pattern is geopolitical/idiosyncratic shock, not systemic re-rating. Mean-reversion is the higher-EV trade once selling thins - fade VIX strength, sell the belly into the bounce, and let MOVE stay your tell that this stays contained.

What it means for your trading

MOVE flat at 76.98 against a VIX spike to 21.33 isolates this as equity-positioning stress, not credit contagion - a setup that historically mean-reverts. Fear & Greed at 29 confirms the contrarian window without screaming capitulation yet.

Scenario EV

Scenario EV ranks Iron Condor top of the book with a score of 62, edging the put spread alternative - positive VRP with ATM IV at 20.52% over realized 14.14 still pays sellers, and VVIX at 98.54 sits in the normal zone, clearing standard sizing.

Optimal tenor is the 30-45 DTE belly: front-end gamma is too hot with VIX9D at 24.06 inverted to VIX at 21.33, and the back-end Contango flattens carry beyond that window. Structure wings outside the 720.00 put wall and 750.00 call wall - anchored by the 700 OI magnet - to keep short strikes off the dealer hedging path.

Defined risk is non-negotiable: net VEX at -$330.2M means a further VIX leg higher accelerates the move, and naked short vol gets run over. Iron condor over short strangle, every time below 742.15.

What it means for your trading

Iron condor in the 30-45 DTE belly with wings outside 720.00 and 750.00 is the highest-EV expression - positive VRP and normal VVIX clear the trade at standard size, but only in defined-risk form given short-gamma amplification below 742.15.

Actionable Summary

With SPY pinned below the gamma flip at 742.15 and dealers short gamma across the index complex, the cleanest expression is a defined-risk Iron Condor in the 30-45 DTE bucket, structured around the 730 pivot with wings outside 720.00 and 750.00. Positive VRP keeps premium harvest paying, and VVIX at 98.54 sits in the standard-size zone - stay there unless vol-of-vol breaks higher.

Avoid naked vol selling, weeklies, and single-name dispersion: front-end backwardation in Contango term structure makes the belly the only clean canvas. Fade strength into 750.00, hedge tails with put spreads off 720.00 rather than naked puts given steep quarter-delta skew at 4.99%.

The pivotal trigger is a reclaim of 742.15 - that flips dealer flow from amplifying to dampening and unwinds the vanna feedback. Until then, regime stays Elevated / Watchful and short-gamma mechanics dominate.

What it means for your trading

Sell defined-risk premium via Iron Condor in 30-45 DTE around 730; the trade thesis flips on a reclaim of 742.15, which restores dealer dampening and ends the vanna accelerant.

Middle East tension is the macro overlay that explains why VIX is bid even as MOVE stays flat - equity vol pricing geopolitical tail without rates contagion.

Cramer's note on higher open contradicting current tape shows how fast intraday sentiment flipped - supports the mean-reversion thesis if 742.15 reclaims.

Gold up on dollar weakness while oil falls reinforces the geopolitical-de-escalation read - risk-off is equity-positioning, not flight-to-safety panic.

Oil falling on Iran-Israel pause is the cleanest tell that today's vol spike isn't about energy/inflation transmission - limits downside duration.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.78 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 742.15 against a spot of 727.26. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 20.52% with a volatility risk premium of 6.38%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 21.33. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime