Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY at 742.78 sits in Positive Gamma regime with net GEX -$18.87B - dealers long gamma, mean reversion favored above 739.99. Key levels: call wall 749.00, put wall 739.00, gamma flip 739.99 sits just below spot so the cushion is thin - a break through flip flips the regime to short-gamma fast. Dealer vanna net -$6.52B and charm $3.6M - vol-up sells delta (accelerant on a vol pop), charm modestly supportive into close. QQQ at 717.55 and IWM at 284.59 are both in Negative Gamma - that's the cross-asset divergence (Spy Heavier). VIX 18.73 (-12.92%%) in Contango but VVIX jumped to 102.04 (+19%%) - vol carry intact, vol-of-vol bid. VRP 2.8% with ATM IV 15.92% over HV20 13.12 - options modestly rich to realized. Bottom line: short premium structures favored (Iron Condor at 30-45 DTE), but half-size given VVIX bid and tight flip distance - fade rips into 749.00, exit longs below 739.99.

SPY positive gamma above 739.99 while QQQ/IWM short-gamma - index dispersion is the lead story

SPY is camped above 739.99 in a positive-gamma cushion, but QQQ and IWM are sitting in Negative Gamma territory - the index complex is diverging and that Spy Heavier split is today's lead. VIX sits in Contango yet VVIX punched to 102.04 with skew bid, so the tape is calm on the surface and quietly paying up for tail. Iron condor is the recommended structure (Iron Condor) at 30-45 DTE - fade strength into walls, do not chase below the flip.

Regime Assessment

Regime sits Elevated (Elevated / Watchful) with VIX at 18.73 - watchful, not stressed. The transition matrix prices panic-escalation in five sessions at 0.05 while the path back to a low-vol regime over ten sessions runs 0.25. Asymmetry favors decay over escalation, but the gradient is shallow.

Half-life of 15 sessions makes this state moderately sticky - not entrenched, not transient. Translation: the elevated print persists long enough to harvest premium, but transitions, when they arrive, are slow and grinding rather than abrupt. Don't fade a regime change in its first session; the matrix rewards patience on both entries and exits.

Practically: short-premium structures keep working while we sit Elevated, sized to respect the VVIX/skew divergence underneath. The yellow flag is real but the regime math is not yet telling you to flatten.

What it means for your trading

Regime Elevated / Watchful with panic-prob 0.05 over five sessions and half-life 15 - stay short premium, but respect the slow-transition tax on early reversals.

Trading readVIX down hard, VVIX up hard, SKEW up hard, MOVE flat - that's a textbook 'calm on the surface, jumpy underneath' divergence. Confirmations are absent; the dashboard is whispering jump risk while equity vol naps.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

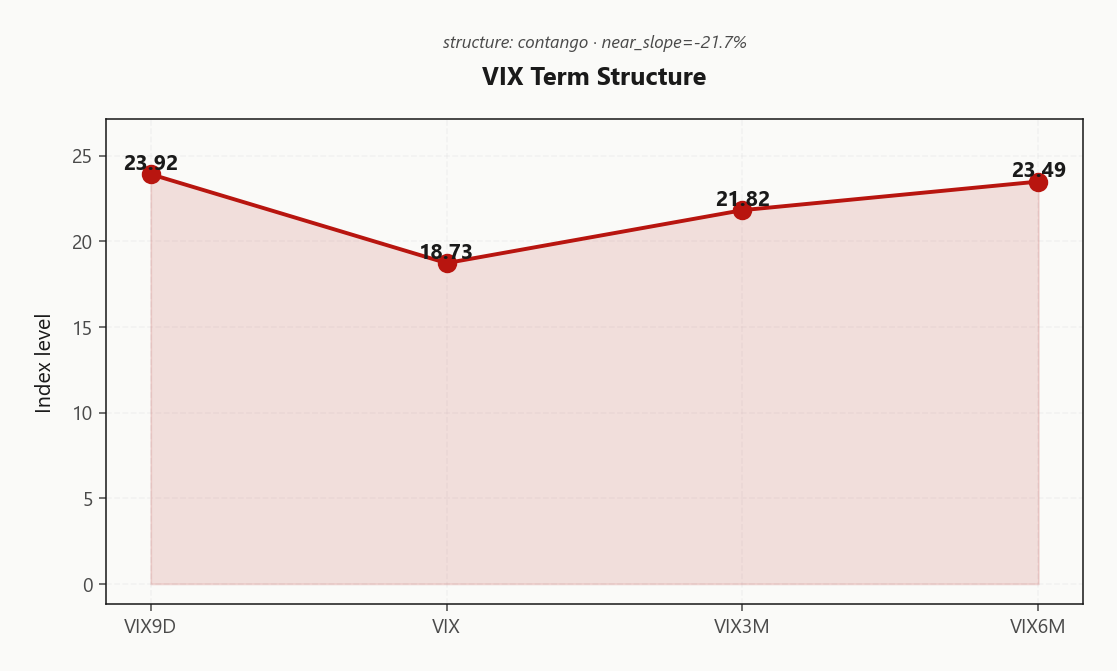

Forward Vol Geometry

The VIX curve carries an Contango shell from 18.73 at the thirty-day node out to 21.82 three-month and 23.49 at six, but VIX9D sits above spot VIX at 23.92 - a front-end kink under the contango shell. Near slope prints -21.7%%, locating the event premium squarely in the next one to two weeks before the curve normalizes through the belly.

Forward 30-to-60 implied lands at 23.2112505049, regime Flat - the belly is neither steep nor inverted, just unremarkable. That flat middle is the cleanest carry zone on the curve: front-week is paying for known headline risk, mid-curve is paying for nothing in particular.

The trade writes itself. Sell the front-week vol bump into the elevated 9D print, own the 30-45 DTE bucket where the curve flattens out. Calendars are the natural expression - short the event-premium hump, long the flat belly - and the structure dovetails with the recommended Iron Condor sizing into the same window.

What it means for your trading

Micro backwardation at the front under an overall Contango shell tells you the event premium is concentrated in the next one to two weeks while the Flat belly offers clean carry. Best edge is selling the front-week pop and owning 30-45 DTE where the curve normalizes.

Trading readVIX9D > 30d VIX inside a contango shell = front-end event hump, mid-curve normalized. Sell the front-week pop, own the 30-45 bucket.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 15.92% carries a measured premium over HV20 13.12 and HV60 14.97 - options are modestly rich to realized, not extreme. With HV20 printing below HV60, realized is decelerating into the calm tape, which is exactly the backdrop that keeps short-premium structures live without inviting size.

VRP at 2.8% sits squarely in the paid-but-not-gifted zone - enough carry to justify the trade, not enough to justify max-size. QQQ tells a richer story: ATM IV 25.23% against HV20 23.08 opens a meaningfully wider spread, and the VRP at 2.15% prints cleaner harvest than the SPY sleeve.

The implication is straightforward: premium selling favors tech where the IV/RV gap is widest, while SPY rewards calendar geometry over outright short vol. Stay disciplined on sizing - the realized deceleration is real, but the carry edge is modest, not generous.

What it means for your trading

SPY VRP at 2.8% is paid-not-gifted with realized decelerating (HV20 13.12 below HV60 14.97), while QQQ's wider IV-to-realized spread (25.23% vs 23.08, VRP 2.15%) makes the tech sleeve the cleaner short-vol harvest today.

Skew Convexity

Quarter-delta skew prints 3.53% with put wing at 22.28% against a call wing at 18.75% and ATM anchored at 19.92% - an ordered, downside-heavy smile with ratio 1.19%. Downside is bid, upside is asleep; there is no convexity premium being paid for a melt-up.

The tape's tell is the CBOE SKEW index ripping to 152.25 (+7.11%%) on a session where spot vol bled lower. Far-tail puts are re-pricing faster than the quarter-delta wing - the curvature is steepening beyond what linear skew captures, and that is the textbook signature of dealers and macro books quietly funding crash protection while the surface looks calm.

Trade implication: spread the protection. Naked long puts overpay for convexity that is already in the strike - put spreads or put ratios harvest the steepness without paying the SKEW tax. Stay away from call-wing longs; flat 18.75% says no one is bidding upside and you would be the only buyer.

What it means for your trading

Quarter-delta skew at 3.53% is steep but the SKEW index jump of +7.11%% to 152.25 shows the deep tail is re-pricing harder than the wing - own downside via spreads, not outright puts.

Vol-of-Vol Structure

VVIX punched to 102.04 (+19%%) while VIX collapsed -12.92%% to 18.73 - the textbook calm-surface, jumpy-underneath divergence. Spot vol is being sold; the vol of that vol is being bid. That's not a coincidence, it's the tape quietly paying up for jump optionality while the headline gauge naps.

The VVIX/VIX ratio at 5.45 still prints Normal, and the mechanical sizing read is Standard Size. We'd lean half of that. The level isn't screaming, but the direction of travel - VVIX ripping on a VIX down day - is the yellow flag short-vol books should respect. Convexity is being accumulated quietly; you don't want to be the marginal seller of it.

Trade implication: harvest premium where the curve pays you, but skip the max-size temptation. Jump risk is being priced in even as realized naps - own the spreads, fade the naked short wings.

What it means for your trading

VVIX bid at 102.04 on a VIX-down session flags jump risk being quietly accumulated - ratio 5.45 reads Normal, but lean half of Standard Size.

Dispersion Spread

SPY ATM IV prints 15.92% against QQQ at 25.23% and IWM at 24.52% - the single-name component embedded in tech and small-cap carries a meaningful premium over the large-cap blend, and that wedge is the cleanest tell that correlation is not collapsing. Cross-strike dispersion at 74.96 confirms it: idiosyncratic moves are clearing on their own merits, not getting washed out by index hedges.

That geometry argues the index vol surface is the cheap leg - SPY/SPX premium is being depressed by passive correlation while QQQ and IWM constituents bid their own vol. Sell index vol, own select single-name vol is the structural pair in this regime, and the QQQ/SPY IV gap is the carry that funds it. Sizing stays measured given the VVIX bid sitting under the calm surface, but the dispersion read itself favors Iron Condor on the index at 30-45 DTE while leaving room to own convexity on the names that actually move.

What it means for your trading

Index-to-single-name vol spread (SPY 15.92% vs QQQ 25.23%, IWM 24.52%) plus cross-strike dispersion at 74.96 says correlation is holding - sell SPY vol against owned single-name vol, do not short the names that are paying for their own jumps.

Liquidity & Microstructure

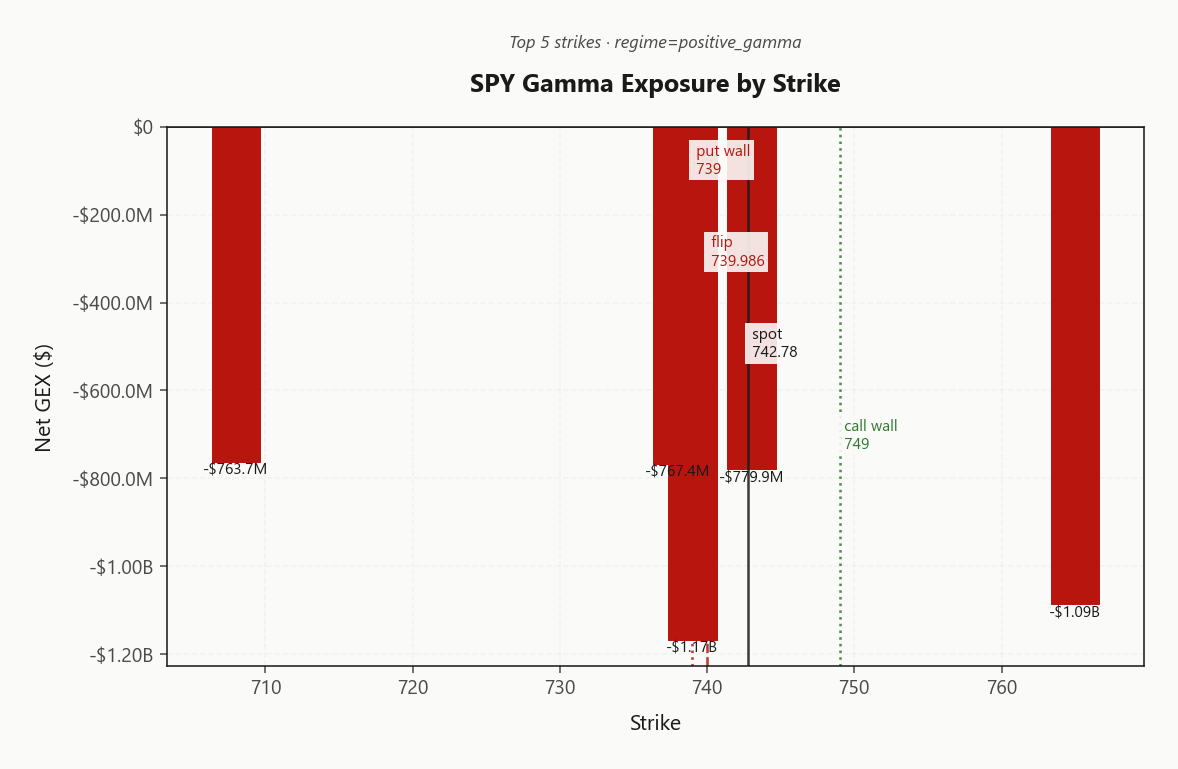

SPY's order book is a study in fragile equilibrium: highest OI still anchors at 580 - deep ITM legacy hedges - but live gamma concentrates at the 739.00 strike carrying net GEX of -$1.17B. That's the pin candidate and it sits effectively on top of spot at 742.78.

The corridor is defined: 749.00 caps upside as the magnet and ceiling, 739.00 backstops the downside. Inside that band dealers mean-revert and the tape chops; outside it the mechanics invert. The catch is the gamma flip at 739.99 sits razor-close to spot - the positive-gamma cushion is paper-thin and a clean break flips the regime to amplification in a single print.

Trade the corridor, respect the flip. Fade strength into 749.00, lean on 739.00 as the backstop, and treat a sustained break of 739.99 as the regime-change signal, not noise.

What it means for your trading

SPY's positive-gamma cushion is real but wafer-thin - the flip at 739.99 sits on top of spot 742.78, with 749.00 the cap and 739.00 the floor. Inside the corridor dealers mean-revert; lose the flip and amplification takes over.

Trading readDeep positive gamma at 749.00 caps upside while 739.00 backstops downside - the corridor between is today's playing field, and dealers will mean-revert any move that stays inside it. A break of 739.99 flips the script to amplification.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order book is a split signal. Net vanna prints -$6.52B - a negative read that means any vol pop forces dealers to sell delta, turning a VIX uptick into an accelerant rather than a brake. Net charm at $3.6M pulls the other way, with time decay nudging dealers to buy into the close: Time decay pushing dealers to buy - supportive into close.

Trade it accordingly: lean on charm support into the bell while spot holds above 739.9857748251, but tighten or flatten short-vol risk on any close below - the vanna accelerant is loaded, not spent.

What it means for your trading

Charm is supportive into the close while spot holds above 739.9857748251, but negative net vanna at -$6.52B means a VIX pop flips dealer flow into a downside accelerant - the pivot is the single line that decides which force wins.

Cross-Asset Confirmation

Cross-asset confirmation is conspicuously absent, and that is the signal. MOVE sits at 75.20 with no daily delta - rates vol is not corroborating the equity-vol calm, nor is it screaming stress. This is an equity-microstructure story, not a credit or rates story, which sharpens the case for index-relative trades over macro hedges.

Sentiment lines up with the muted tape rather than the rip: Fear & Greed reads Fear at 44 - cautious, not euphoric, so positioning is not the squeeze fuel. The split that matters is inside the index complex itself: QQQ at 717.55 and IWM at 284.59 are both short-gamma while SPY holds positive - regime divergence flag True, direction Spy Heavier.

Trade the dispersion: large-cap is the cushion, tech and small-cap are the breaking points. If anything cracks today, it cracks in QQQ first - fade strength there, lean on SPY corridor structures.

What it means for your trading

With MOVE unchanged at 75.20 and Fear & Greed merely Fear at 44, the SPY-positive / QQQ-IWM-negative split is an isolated equity-microstructure divergence (Spy Heavier) - not a cross-asset shock. Pair-trade large-cap cushion against tech/small-cap fragility rather than reaching for macro hedges.

Scenario EV

Scoring lands on Iron Condor as the structure of choice, posting 61 against put spread's 52 - a clean preference, not a coin flip. VRP read is Unknown, but the carry case stands on its own: contango shell, positive-gamma cushion above the flip, and a defined wall corridor doing the containment work.

DTE sweet spot sits at 30-45 - past the front-week event hump where VIX9D is bid, into the bucket where the curve flattens and theta compounds cleanly. Anchor the short call leg at 749.00 and the short put at 739.00; those are the dealer-defined boundaries, not chart-derived guesses.

Size half. VVIX is bid on a VIX-down tape and the gamma flip sits razor-thin below spot - the structure is right, the conviction modifier is not. Harvest the corridor, respect the divergence.

What it means for your trading

Iron condor wins on score (61 vs 52) at 30-45 DTE, anchored 749.00/739.00 - but half-size given the VVIX bid and tight flip distance.

Actionable Summary

Trade structure: Iron Condor at 30-45 DTE, anchored short 749.00 calls and 739.00 puts. Half-size - VVIX bid to 102.04 on a day VIX printed 18.73 is the textbook calm-surface/jumpy-underneath divergence, and the corridor only works while SPY holds the cushion.

Watch level: 739.9857748251. Charm bias reads Supportive above it; lose it and the SPY regime flips from Positive Gamma to amplification, with net vanna at -$6.52B turning dealers into forced delta sellers on any vol pop. Regime backdrop is Elevated / Watchful - sticky but not entrenched.

Avoid: naked long puts (skew is bid, SKEW index ripped to 152.25 - spread the protection); short single-name vol while dispersion stays moderate; chasing strength through 749.00. Own select tail via put spreads while the wing is paying up.

What it means for your trading

Sell the 749.00/739.00 corridor in 30-45 DTE iron condors at half size, defend the 739.9857748251 pivot, and spread any downside tail rather than buying it naked.

CNBC trimming winners pre-emptively echoes the tape's quiet defensiveness - sentiment matches the VVIX bid and SKEW rip even though VIX itself is calm.

Iran-Israel exchange of fire still in the headline rotation - the reason the front-end of the VIX curve hasn't fully collapsed despite the contango shell.

Gold at two-month low on strong jobs + rate-hike bets is the macro counter-narrative to the geopolitical premium - if jobs theme dominates, the front-week vol bid fades.

Weight-loss drug -25% on safety data is a reminder that single-name idiosyncratic shock risk is alive - supports the dispersion read favoring index over single-name short vol.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.51 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 739.99 against a spot of 742.78. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.92% with a volatility risk premium of 2.8%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.73. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime