Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

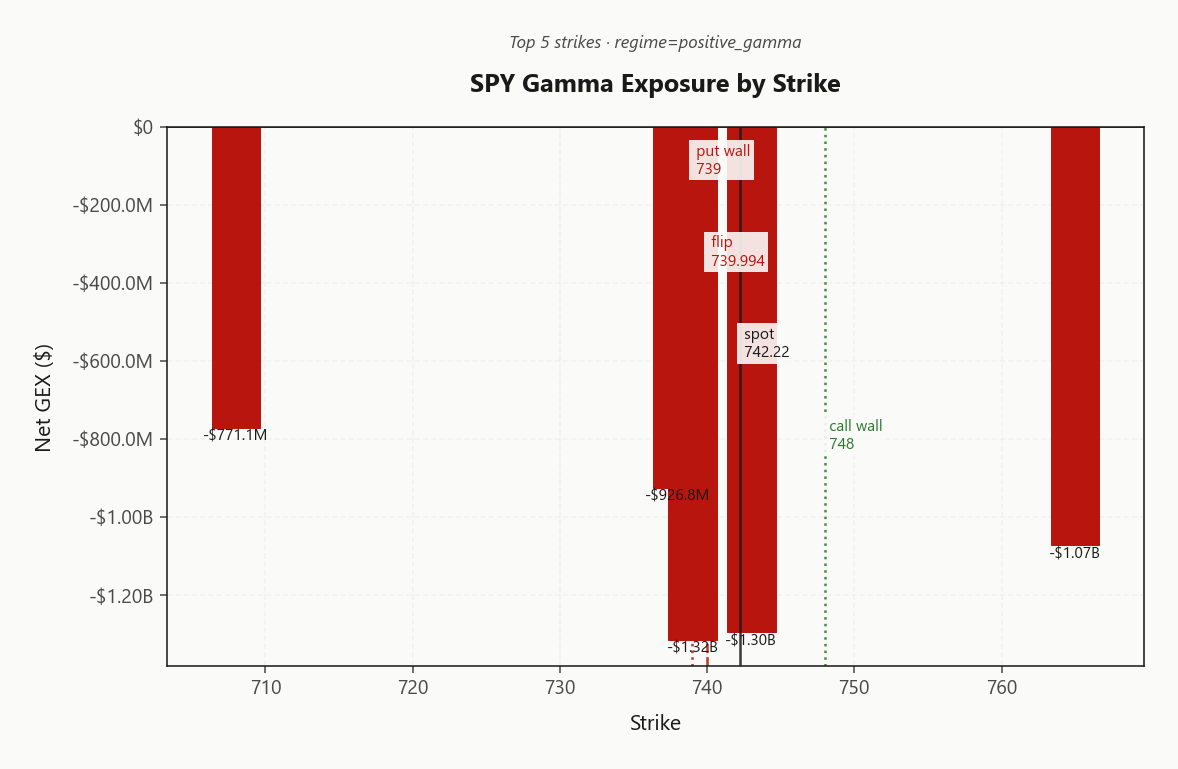

SPY trades 742.22 in Positive Gamma with net GEX at -$18.01B - dealers long gamma, moves get dampened, mean reversion wins until something breaks. Key levels: call wall 748.00, put wall 739.00, gamma flip 739.99 - spot sits -0.2999460764 from the flip, a thin cushion, not a comfortable one. Dealer vanna at -$9.33B is negative meaning a vol spike flips them into delta-selling, and charm at -$1.5M is mildly pressuring into close. VIX cools to 21.51 with VVIX at 94.68 and term structure in Contango - VRP on SPY at 1.98% vol points is live, vol sellers paid. QQQ at 719.30 is the crack: Negative Gamma with spot below flip 728.25 - moves there get amplified, not dampened. IWM mirrors QQQ in Negative Gamma with VRP at -0.16% - single names not paying you for the risk. Bottom line: sell SPX premium in 30-45 iron condors anchored inside the wall structure, avoid naked QQQ/IWM short vol, and treat a SPY break of 739.99 as the regime-change trigger.

SPY positive gamma cushion vs QQQ/IWM short-gamma - divergence is the day's lead story

SPY at 742.22 holds above its gamma flip at 739.99 keeping dealers in dampening mode, but QQQ and IWM both sit below their flips in Negative Gamma territory - that's the cross-asset crack underneath a tape that looks calm on the surface. VIX bleeds to 21.51 with term structure in Contango and VVIX at 94.68 confirming the suppressive regime, but Fear & Greed at Fear and the Hormuz overhang say the macro tail isn't gone. Iron condor remains the EV-positive structure in the 30-45 window while spot stays above SPY's flip.

Regime Assessment

The tape sits in an Elevated / Watchful regime with VIX printing 18.36 - neither the suppressed grind that rewards naked carry nor the panic state that demands defensive posture. The Markov read says the path back to a low-vol regime over the next two weeks carries a 0.25 probability while the jump to panic over the next week sits at just 0.05 - asymmetric in the carry-seller's favor, but the drift home is slow.

Half-life of 15 sessions is the operative number: this regime is sticky, measured in weeks rather than days. Don't trade it like a snap-back to single-digit VIX is imminent - it isn't. The premium is real, the carry is live, but the regime won't collapse on you fast enough to justify aggressive front-month rolls into compressed structures.

Translation for the desk: harvest the carry, refresh structures regularly, don't over-stay. Sell premium where you're paid, take profit early on iron condors as theta accrues, and resist the temptation to add size as VIX bleeds - the elevated/watchful label exists because the tail-bid in MOVE and SKEW says the macro overhang hasn't cleared.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - sticky enough to harvest carry, not so benign that you can ignore the tail. Refresh structures, don't over-stay.

Trading readVIX cooling, VVIX following down, SKEW still elevated, MOVE elevated - they're loosely confirming but SKEW and MOVE staying firm says the tail bid is intact even while front-end vol bleeds. Don't read the VIX drop as all-clear.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

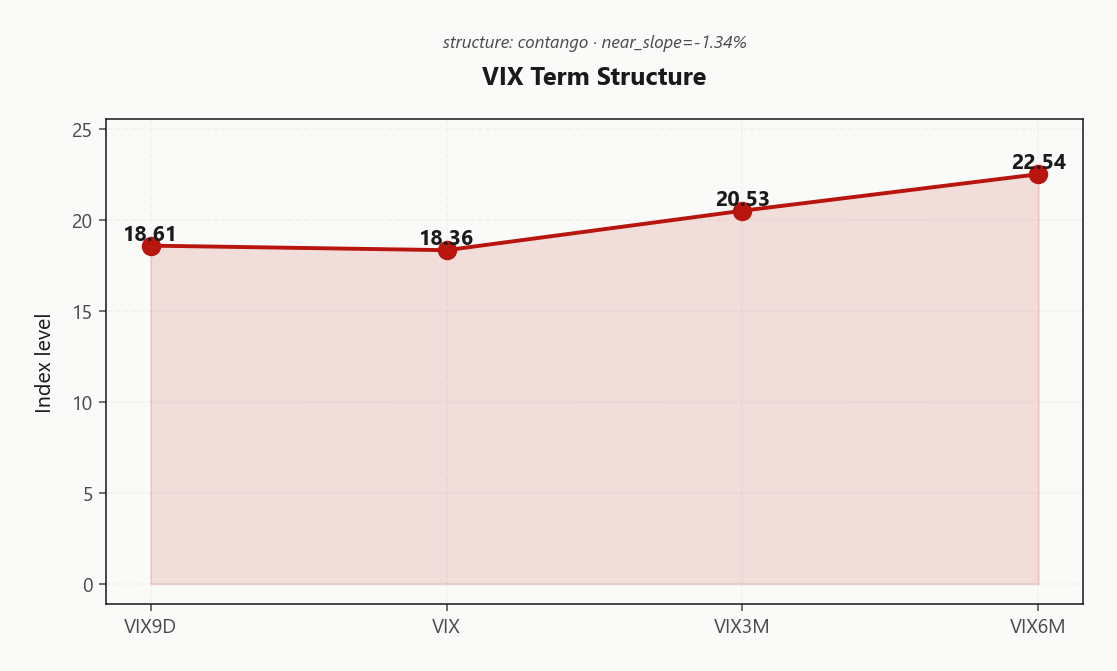

Forward Vol Geometry

The VIX complex prints a clean Contango stack from 18.61 at the front through 18.36, 20.53, and out to 22.54 at the back - near slope at -1.34% confirms front-end suppression while the long end still prices a structural risk premium. The label reads Flat term structure, meaning no event premium is jammed into the curve; this is carry geometry, not a coiled spring.

Forward 21.533150025 in the 30-to-60 window steps cleanly up to 24.3848785111 in 60-to-90 - the densest carry sits in the front forward, and that lines up with the EV engine's 30-45 DTE sweet spot. Fade short-dated vol, own long-dated convexity; calendars earn the slope without paying for a shock that isn't priced.

Translation for the desk: sell the front forward, buy the back, and let Flat do the work. Long-dated SPX puts remain the cheapest sleep money on the screen relative to where the tail still bids.

Trading readVIX9D-to-VIX6M in clean Contango with slope at -1.34%% - carry trade is live, no priced-in stress event, vol sellers paid through the curve.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 15.06% prints meaningfully above both HV20 at 13.08 and HV60 at 14.96 - implied is trading rich to realized across both windows, and the resulting VRP of 1.98% vol points is live carry for index premium sellers. Realized is not accelerating into implied; the spread is structural, not a setup for a snap-back compression.

The single-name picture inverts the trade. QQQ VRP at 0.46% is razor-thin and IWM VRP at -0.16% is outright negative - implied is cheap to realized in the single-name proxies, and short vol there isn't paying you for the gamma risk you're carrying below their flips. With QQQ and IWM both in Negative Gamma territory, you'd be selling vol into the regime that amplifies moves rather than dampens them.

Bottom line: harvest the index VRP in SPX, sit on hands in QQQ and IWM single-name vol. The carry is concentrated where the dealer regime supports it.

What it means for your trading

Index VRP at 1.98% vol points is the real carry trade with implied riding above HV20 and HV60; QQQ at 0.46% and IWM at -0.16% don't pay for the negative-gamma risk underneath.

Skew Convexity

SPY's quarter-delta skew sits at 3.35% vol points with put_25d at 19.8% against ATM at 17.8% and call_25d at 16.45% - downside is paying up but the curve is ordered, not panicked. Smile ratio at 1.2% sits comfortably above parity, confirming a bid for the left tail with the right tail dead - no upside conviction is being priced.

QQQ skew steepens to 5.03% and IWM to 5.16%, both materially above the index - tech and small-cap convexity prices the fragility that SPY's Positive Gamma cushion masks. With QQQ and IWM both below their flips and skew this steep, single-name vol is doing the worrying that index vol won't.

Trade the structure: put spreads dominate naked puts - you're paying for skew you don't need on the wing - and sell upside calls into the 748.00 wall where right-tail demand is absent. Avoid mirroring the structure in QQQ or IWM; the steeper skew there is telling you the protection is fairly priced, not cheap.

What it means for your trading

SPY skew at 3.35% with smile ratio 1.2% says ordered left-tail bid, no right-tail conviction; QQQ and IWM at 5.03% and 5.16% confirm single-name fragility. Put spreads beat naked puts, sell calls into the wall, don't replicate the trade in tech or small-caps.

Vol-of-Vol Structure

VVIX prints 94.68 against VIX at 18.36, putting the ratio at 5.16 - squarely in Normal territory. No jump-risk premium is being bid into the wings, and the -7.21%% bleed in VVIX is tracking VIX lower rather than diverging. The market is not pricing a bimodal outcome.

That clears the runway for Standard Size on the vol-carry book. No half-sizing, no defensive trims - the convexity surface is well-behaved, and the iron condor framework in 30-45 can run at full notional. Vol sellers lean in here; the regime is paying real carry without forcing you to underwrite a tail you can't see.

The trigger to watch is VVIX disconnecting from VIX - a spike in vol-of-vol while front-end VIX stays pinned would be the first read that the wings are getting bid before spot moves. Until then, the ratio confirms the Elevated / Watchful backdrop is sticky, and the dampening regime holds.

What it means for your trading

VVIX-to-VIX at 5.16 is Normal - no bimodal panic priced, so vol sellers can run Standard Size. Early warning is a VVIX spike decoupled from VIX.

Dispersion Spread

Index vol is cheap to single-name vol and the gap isn't subtle: SPY ATM IV at 15.06% sits well below QQQ at 23.82% and IWM at 23.14%. That spread is the dispersion regime - correlation is moderate, idiosyncratic risk is alive, and the index is not a clean proxy for the names underneath it.

The VRP confirms which side you want to be on. SPY VRP runs at 1.98% vol points - a real premium for index sellers - while IWM VRP at -0.16% is flat-to-negative. Single-name implied is fair-to-cheap to realized; you are not paid to be short gamma in QQQ or IWM premium.

Trade: harvest the index side, leave the single-name vol alone. If you need to hedge a single-name book, use single-name puts - index hedges underprice the idiosyncratic tail and will leave you with basis risk when one name breaks while SPY pins.

What it means for your trading

SPY ATM IV at 15.06% versus QQQ at 23.82% and IWM at 23.14% prints a moderate-dispersion regime where index VRP at 1.98% pays carry but IWM at -0.16% does not. Sell index vol, avoid single-name short vol, hedge names with name puts.

Liquidity & Microstructure

SPY's heaviest strike at 739.00 prints a deeply negative -$1.32B, but the highest-OI strike at 580 sits far OTM - legacy protection from prior risk cycles, not today's hedging flow. Read the book by what's active, not what's stuck on the tape.

The level that matters now is the gamma flip at 739.99. Spot trades -0.2999460764 from it - a cushion measured in basis points, not handles, thin enough to respect and wide enough to lean on. Above the flip, regime reads Positive Gamma: dealers buy weakness and sell strength, dampening both tails. Break it, and the same desk flips to amplifying.

The channel is bracketed by the 748.00 call wall and the 739.00 put wall - trade the range inside, fade extensions toward either edge. The flip is the trigger; the walls are the boundaries.

What it means for your trading

Sell defined-risk premium against the wall structure while spot holds above 739.99; a clean break of the flip is the regime-change trigger that converts dealer dampening into dealer amplification.

Trading readSPY's gamma stack is thick around the 748.00/739.00 wall pair with the flip at 739.99 as the pivot - dealers dampen inside the channel, amplify outside it. Trade the range until something breaks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The pivot is the gamma flip at 739.9937402319. Spot sits -0.2999460764 from it - current bias reads Supportive, but that cushion is thin, not comfortable. While SPY holds above, dealer rebalancing dampens; vanna and charm stay latent.

Break the flip and the geometry inverts fast: negative vanna means a vol bid compounds the delta sell, and charm bleed pushes the same direction. Treat 739.9937402319 as the regime-change trigger - above it, harvest carry; through it, flatten condors and let the wings do their job.

What it means for your trading

Vanna and charm sit benign while SPY trades above 739.9937402319, but the negative VEX print means a vol spike below the flip turns dealers into accelerants - bias Supportive, fragility one level away.

Cross-Asset Confirmation

The cross-asset tape is quietly diverging. MOVE at 75.20 says rates-side stress is absent - no bond-market tantrum bleeding into equity vol. Yet Fear & Greed prints Fear at a score of 44 with SPX pinned near highs. Sentiment is lagging price - the marginal buyer is reluctant, which caps how far the positive-gamma ratchet can extend.

Under the hood, the regime split is the day's lead story. SPY holds Positive Gamma above its flip, but QQQ at 719.30 and IWM at 285.27 both sit in Negative Gamma territory below theirs. Per True, the divergence direction reads Spy Heavier - large-cap is carrying the tape while tech and small-caps run fragile underneath.

Risk-on is weaker than SPY implies. Watch for catch-down through QQQ's flip at 728.25 as the early-warning trigger.

What it means for your trading

MOVE calm and SPY positive-gamma mask a real crack: QQQ and IWM below their flips with sentiment in Fear despite a rallying tape. The SPY-heavier divergence biases catch-down risk in tech and small-caps before it reaches the index.

Scenario EV

The EV stack scores Iron Condor at the top with a best score of 42, edging the put spread alternative at 32. With SPY anchored in Positive Gamma above the flip at 739.99 and VRP live at 1.98%, the regime pays you to sell defined-risk premium against the wall structure between 739.00 and 748.00.

Sweet spot sits in the 30-45 window - past front-month event drag, ahead of back-month theta slowdown. VVIX at 94.68 reads Normal, sizing guidance is Standard Size, no need to half-size. Defined wings beat naked strangles here: VVIX isn't compressed enough to give away the tail, and the put spread is the cleaner alternative if you want to layer a directional lean rather than fade both sides.

Avoid the same trade in QQQ and IWM - sub-flip Negative Gamma and thin-to-negative single-name VRP don't pay for the wing risk.

What it means for your trading

Iron condor at 42 beats put spread at 32 in the 30-45 window - sell SPX premium inside the wall channel, standard size, defined wings.

Actionable Summary

Primary trade: sell defined-risk premium against the SPY wall structure. Iron condor in SPY/SPX through 30-45 DTE, wings tucked inside the 748.00 call wall and 739.00 put wall. Recommended structure is Iron Condor with the regime tagged Elevated / Watchful - carry is live, but the channel is the trade, not naked wings.

Avoid short vol in QQQ and IWM. Both sit in Negative Gamma below their flips; VRP at 0.46% and -0.16% does not pay for the amplification risk. Sizing stays Standard Size - VVIX at 94.68 is normal, no half-sizing required.

Regime trigger: a SPY break of the gamma flip at 739.9937402319 flips dealers from dampening to amplifying - spot sits a thin -0.2999460764 above. Hedge: long-dated SPX puts remain cheap relative to the upside event tail per the smile read at 1.2%.

What it means for your trading

Sell Iron Condor in SPX inside the 739.00/748.00 wall channel and treat a SPY break of 739.9937402319 as the regime-change trigger; skip naked single-name vol in QQQ and IWM where the carry doesn't compensate.

Hormuz timeline pushed to year-end - the geopolitical tail that's been suppressing the right-side of equity vol just got longer, supporting MOVE-bid and explaining why long-dated SPX skew won't flatten.

Weight-loss drug maker down 25% on safety data - single-name event reminder that idiosyncratic risk is alive, reinforcing the avoid-short-single-name-vol stance.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.51 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 739.99 against a spot of 742.22. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.06% with a volatility risk premium of 1.98%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.36. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime