Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

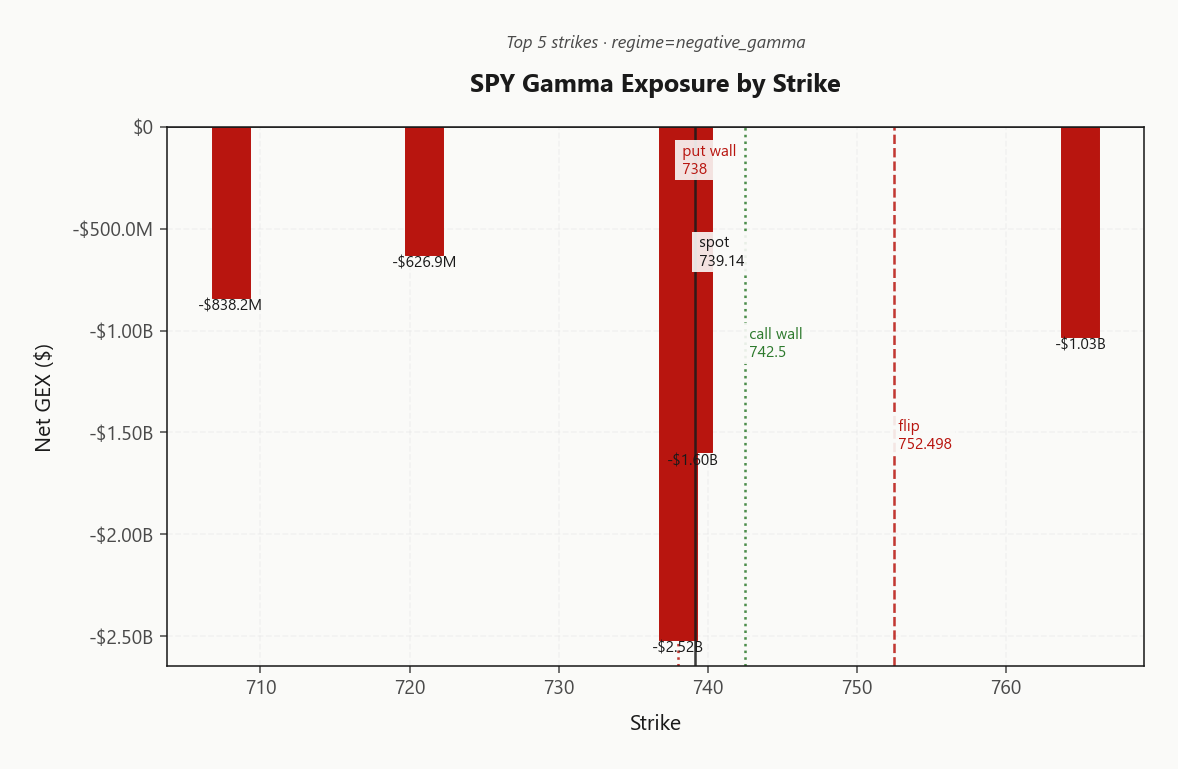

SPY closes at 739.14 sitting just under the gamma flip at 752.50 - dealer positioning is short gamma (-$19.98B) which means today's tape amplifies, not dampens. Call wall stacks at 742.50 and put wall at 738.00, with max pain magnet at 751.00 - spot is essentially pinned at the put wall, a knife's-edge level. Dealer vanna at $6.62B is supportive on vol spikes (short-gamma vanna mechanic), and charm at $254.6M pushes dealers to buy into close - modest end-of-day lift bias. VIX collapsed to 18.69 with VIX9D/3M/6M restored to contango (Contango), VRP at 2.97% keeps option sellers paid but VVIX at 93.09 signals jump risk is not fully priced out. Fear & Greed reading is Fear (40) - disconnect with VIX is the cautionary note. Bottom line: best edge is range-defined premium harvest (iron condor, 30-45 DTE per derived) bracketing 738.00 - 742.50; avoid naked short puts below the flip and avoid lottery call chases above call wall - both punished by amplifying dealer flow.

Negative gamma across SPY/QQQ/IWM with VIX bleeding lower into contango - fragile calm

SPY at 739.14 sits beneath the gamma flip at 752.50, leaving dealers short gamma and primed to amplify moves in either direction. VIX cracked lower to 18.69 with term structure restoring contango, but VVIX at 93.09 and a Fear & Greed reading of Fear keep the underlying tape fragile. The setup favors range-defined premium harvest in the 30-45 DTE window over directional bets, with the 738.00 put wall as the line in the sand.

Regime Assessment

Regime classification reads Elevated / Watchful with VIX at 18.69 - not panic, not benign. The half-life of 15 sessions tells you this state does not collapse overnight; whatever bias you carry into tomorrow is the bias you are stuck with for weeks, not days.

Transition math leans constructive: probability of escalation to panic over five sessions sits at 0.05, while the path to a low-vol regime over ten sessions runs 0.25 - compression is roughly five times more likely than escalation. That is the asymmetry to lean on, but it is not a green light.

Sizing implication is standard with tight stop discipline. Stay in the recommended structure, respect the levels, and resist scaling up just because the tape feels calm - Elevated / Watchful regimes punish complacency more often than aggression.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - compression is materially more likely than escalation, but standard sizing with tight stops is the only defensible posture here.

Trading readVIX collapsed but VVIX and SKEW haven't confirmed - divergence flags the rally as fragile rather than durable. MOVE flat means credit doesn't believe the all-clear yet.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

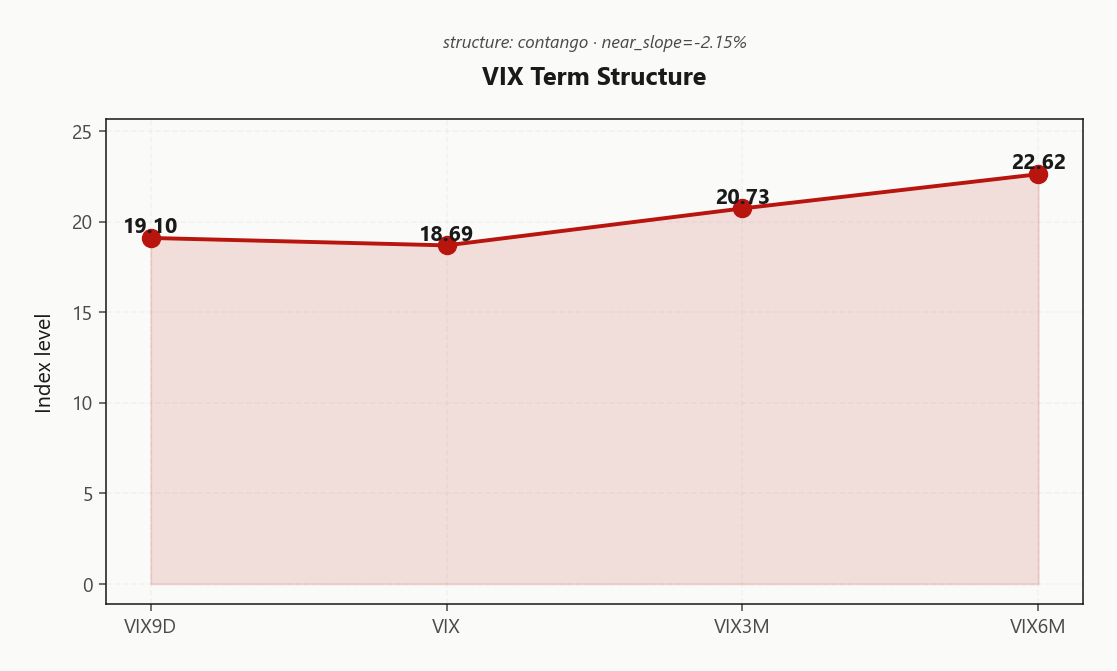

The VIX curve has snapped back to Contango, with the front at 19.10 sitting beneath spot VIX at 18.69 and the three-month at 20.73. The carry trade is alive again - but derived tags the regime Flat (Flat term structure), and that flatness is the tell. A genuine all-clear prints steeper, not this.

Forward thirty-to-sixty at 21.6781295319 and sixty-to-ninety at 24.3638235915 remain stubbornly elevated relative to the front - the back end is not buying the ceasefire bid. Six-month at 22.62 caps the curve well above spot, leaving event premium intact past the immediate window.

Translation: re-engage carry, but at half size. The curve geometry favors calendar spreads - sell the compressed front against the firm back - over outright short vega. One headline flips this back to backwardation.

What it means for your trading

Contango restored at Contango but derived flags the slope as Flat - carry is back on, fragility is not gone. Calendar spreads over naked short vol until the back end relents.

Trading readVIX9D-to-VIX3M contango re-asserted - vol sellers' carry is alive again, but the slope is flat enough that one geopolitical headline flips it back. Half-size on first vol-carry trade post-event.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY HV20 prints at 12.91 against an ATM IV of 15.88%, with HV60 at 14.93 anchoring the longer realized base. The resulting VRP of 2.97% keeps short-vol expectancy positive, but the cushion is modest - enough to fund disciplined premium harvest, not enough to underwrite naked tails.

Across the complex the premium stack is unambiguous: QQQ pays the richest at 1.82% as tech IV continues to embed AI re-rating optionality, while IWM is the thinnest cushion at 0.88% - single-stock dispersion is eating the index VRP and leaving small-caps structurally underpaid for the risk. Realized is trending below implied across the board; sellers sit in the favored seat, but no fat-tail premium remains to be skimmed.

Operationally: route the harvest into QQQ where the spread is real, lean SPY at standard size, and avoid IWM strangles where the realized-versus-implied gap no longer compensates the gamma profile.

What it means for your trading

Vol sellers retain the edge - SPY VRP at 2.97% is positive but modest, QQQ at 1.82% is the prime harvest, IWM at 0.88% is the cushion to avoid. Size standard, skip the tails.

Skew Convexity

SPY's quarter-delta skew sits at 3.91% with a smile ratio of 1.25% - downside vol is structurally bid versus upside, and the wings refuse to flatten despite the headline VIX crush. Put quarter-delta IV prints 19.6% against call quarter-delta at 15.69%, framing ATM at 17.24% - an asymmetric tail bill where the market is paying up for downside convexity and writing off upside chase.

Smile ratio above parity confirms a convex tail bid with no upside conviction priced - the rally tape is buying insurance, not lottery tickets. That makes naked puts an expensive way to express bearish hedges; put spreads dominate the risk-reward, financing the bought downside leg by selling the still-rich wing. On the call side, the flat upside means covered-call premium is thin - wait for a reclaim of the flip before harvesting upside vol.

QQQ skew runs steeper than SPY, a tell that single-name tech hedging is spilling into the index complex - dispersion still asymmetric to the downside. Trade the skew, don't fight it.

What it means for your trading

Downside convexity remains bid with SPY quarter-delta skew at 3.91% and smile ratio 1.25% - express bearish hedges via put spreads, not naked puts, and avoid upside vol selling until spot reclaims the flip.

Vol-of-Vol Structure

VVIX prints 93.09 against a VIX of 18.69, a ratio of 4.98 that the derived layer tags Normal - benign on the surface, but the jump-risk thermometer is still running warm. Sizing guidance lands at Standard Size: short-vol structures are cleared to deploy, but not in size that assumes the tail is dead.

The watch level is VVIX itself, not VIX. With vol-of-vol perched above the ninety handle, optionality-on-optionality is still bid - a single geopolitical headline re-prices the convexity stack before spot vol moves. A break of VVIX through the mid-eighties is the green light for full short-vol sizing; until then, condors and calendars over naked strangles, and let the derived score do the position sizing.

What it means for your trading

VVIX/VIX at 4.98 reads Normal - short-vol is paid at Standard Size, but VVIX above the ninety handle keeps the jump-risk tail live until it cracks the mid-eighties.

Dispersion Spread

Index implied vol sits moderate with SPY ATM at 15.88% against QQQ at 24.74% - the tech premium over the broad index is wide enough to favor index vol selling over single-name shorts in this regime. Correlation reads Moderate, meaning index hedges only partially neutralize the idiosyncratic GEX rotation now scattered across mega-caps.

The mover tape is led by TSLA, whose single-name flow is decoupling from the index bid and dragging dispersion wider beneath the surface. GOOGL and NVDA add to the positive single-stock GEX rotation while AMD cuts the other way - a chip-sector dispersion print that index vol cannot capture.

The textbook dispersion structure - long single-name vol, short index vol - still carries theta drag at these spreads; harvest index VRP via condors first, scale into single-name long-vol only on confirmed correlation break.

What it means for your trading

Index vol selling is the cleaner harvest with QQQ ATM at 24.74% over SPY at 15.88%; TSLA-led single-name GEX rotation flags dispersion that index hedges will miss, but full dispersion structures still bleed theta at moderate correlation.

Liquidity & Microstructure

SPY's near-term gamma is concentrated at 738.00, where dealers carry a massive negative imbalance of -$2.52B - that strike is the put-wall magnet, and pin probability into expiry is elevated as long as spot orbits it. The headline OI cluster at 580 is back-dated LEAPS noise; ignore it for tape mechanics and focus the book on the near-dated structure.

The line that matters for tomorrow is the gamma flip at 752.50. Below it, dealer hedging amplifies directional moves; above it, the same flow dampens them. With the call wall stacked at 742.50 and the put wall anchoring at 738.00, the operative range is well-defined - but the book is structurally negative_gamma, so any breach trades with accelerant, not friction.

Trade the geometry: range-defined premium harvest inside the walls, no naked exposure outside them until spot reclaims the flip.

What it means for your trading

Near-term gamma pins SPY at the 738.00 put wall with dealers deeply short, making the 752.50 flip the single switch between amplified and dampened tape - bracket the 738.00 - 742.50 range, don't fade outside it.

Trading readSPY's gamma profile is heavily negative near spot with the put wall acting as a magnet - dealer flow amplifies any move tomorrow until spot reclaims the flip. Trade range-defined structures, not directional naked.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints $6.62B - positive vanna means any uptick in implied vol mechanically forces dealers to buy delta, a quiet floor underneath the negative-gamma tape. Net CHEX at $254.6M layers a charm bid into the close: overnight gap fills favored, end-of-day drift skews up rather than down as theta bleeds dealers long.

The charm pivot sits at 738 with spot a hair above it - distance -0.1542332982 puts us right on the flow knife-edge. That single level is where dealer hedging flips direction; bias reads Neutral, so neither side owns the tape yet.

Play the asymmetry: a vol spike gets absorbed by vanna-driven dealer buying, while a clean break of 738 flips charm flow against the long side. Lean into premium harvest, not directional bets, until the pivot resolves.

What it means for your trading

Positive vanna and charm quietly cushion the short-gamma book - a VIX pop draws dealer delta-buying and into-close drift tilts long, but 738 is the binary flip level with bias Neutral.

Cross-Asset Confirmation

MOVE holding at 75.20 is the quiet tell - rates vol is not corroborating the equity vol crush, meaning credit hasn't signed off on the all-clear that VIX is broadcasting. Fear & Greed printing Fear at 40 alongside a collapsing VIX is the other disconnect: either sentiment is lagging the tape or smart money is fading the relief rally.

QQQ at 715.95 versus IWM at 284.35 shows small-caps lagging mega-cap tech - no risk-on rotation confirmation, just leadership concentration. IWM sitting in negative gamma with price action trailing is the canary: the index with the thinnest dealer cushion is also the one buyers won't chase.

Cross-asset tone reads Unknown with regimes Aligned across the complex, but the credit/equity divergence is the trade worth watching - if MOVE breaks higher while VIX stays pinned, the rally is the lie.

What it means for your trading

Equity vol crush is unconfirmed by MOVE at 75.20 and a Fear & Greed reading of Fear (40) - IWM's lag versus QQQ at 715.95 flags small-cap fragility as the first crack to watch.

Scenario EV

The book scores Iron Condor as the dominant structure at 39, with the put spread alternative trailing at 31 - a textbook condor setup driven by a live VRP, restored Contango in VIX term structure, and Normal vol-of-vol per VVIX at 93.09. Bracket the 738.00 - 742.50 range and let theta do the work.

The optimal window is 30-45 DTE - far enough out to escape weekly gamma chop around the flip at 752.50, near enough to avoid the vega bleed that would punish a back-month short. QQQ pays the richest premium at 1.82% and deserves a heavier condor allocation than SPY's 2.97%; IWM at 0.88% is the thinnest cushion and stays off the menu.

Avoid naked strangles - IWM's negative_gamma regime and the negative 0DTE share amplify both tails. If the regime cracks bearish through the flip, roll to the put spread as the secondary expression rather than legging defensively. Sizing stays Standard Size per the VVOL read.

What it means for your trading

Iron condor is the highest-EV expression at 30-45 DTE bracketing 738.00 - 742.50, with QQQ the preferred underlying for VRP harvest and IWM excluded on fragility.

Actionable Summary

Bottom line: Iron Condor bracketing the 738.00 - 742.50 range is the cleanest expression of this tape. SPY sits beneath the gamma flip at 752.50 with dealers short gamma - moves amplify in both directions until spot reclaims it, so range-defined premium harvest dominates directional bets. Optimal window is 30-45 DTE, past the weekly gamma noise and ahead of vega decay.

Cross-asset, harvest the richest premium on QQQ where VRP prints 1.82% versus SPY's 2.97%. Avoid naked strangles on IWM - VRP thinnest at 0.88% with negative gamma and lagging price makes it the cross-asset canary. Skip 0DTE chases below 752.50; dealer amplification turns lottery tickets into stop-outs.

Watch 738 as the flow pivot - current bias Neutral. VVIX through the floor and MOVE confirming would green-light full sizing; until then, regime is Elevated / Watchful with half-life 15 sessions - standard size, tight stops.

Strait of Hormuz traffic not normalizing until year-end means oil/MOVE optionality stays structurally bid - energy and credit vol divergence vs equity vol.

Cramer notes chipmakers rebounding from Friday's selloff - confirms the AMD/NVDA dispersion signal in our top movers and a tech-leadership re-engagement risk.

Trump signalling immediate Iran-Israel ceasefire is the headline driving today's VIX crush - but his words alone don't make the regime safe.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.51 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 752.50 against a spot of 739.14. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.88% with a volatility risk premium of 2.97%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.69. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime