Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

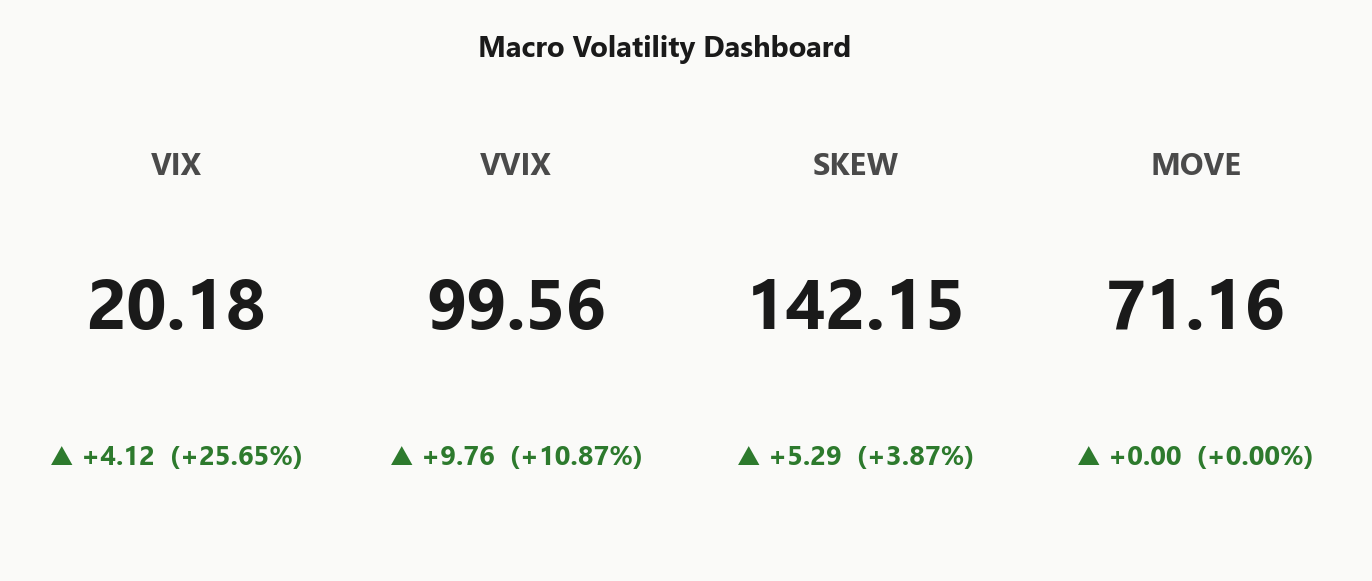

SPY at 734.34 sits in Negative Gamma territory with net GEX at -$14.49B, dealers forced to chase trend rather than fade it. Key levels: call wall at 740.00, put wall at 730.00, gamma flip overhead at 755.99 - spot is currently sub-flip, meaning hedging amplifies any further drawdown. Dealer vanna at -$40.02B is deeply negative - every uptick in vol forces more delta selling, a hostile setup if 20.18 continues to expand from today's 25.65%% pop. VIX term remains Contango with 21.23 vs 21.34, so the curve hasn't fully inverted into panic - VRP at 4.46% still pays vol sellers but at thinner margin. Cross-asset, QQQ remains in Positive Gamma above its flip at 660.99 while IWM mirrors SPY's hostile regime - this divergence is the day's lead. Magnet zone is 731.00 (max pain) and 730.00 (put wall), with 45.3%% of total gamma concentrated in 0DTE. Bottom line: stay light, fade rips into 740.00, only buy dips on a reclaim of the flip - Iron Condor at 30-45 DTE is the cleanest structure for harvest while Normal VVIX keeps sizing standard.

Spot at 734.34 broke beneath the gamma flip at 755.99, dropping the index complex into dealer short-gamma - moves get amplified, not dampened. QQQ alone clings to positive gamma above its flip at 660.99, the lone stabilizer while IWM and SPY drift hostile. With 20.18 ripping 25.65%% and term structure still Contango, this is a fear shock not yet a structural break - but the gap between SPY and QQQ is the lead story.

Regime Assessment

Tape sits in Elevated territory - Elevated / Watchful - with VIX anchored at 20.18. This is the awkward middle: too hot to fade as noise, too cold to treat as a structural break. The regime's half-life of 15 sessions tells you the base case is multi-day persistence, not a one-print spike that mean-reverts by tomorrow's open.

Transition odds frame the risk cleanly. Probability of escalation to panic over five sessions sits at 0.15 - material, not dominant. Probability of cooling back to a low-vol regime within ten sessions is 0.25. Translation: the modal path is more chop, not resolution either way. SPY sub-flip with negative vanna means hostile mechanics persist while VIX stays bid; QQQ above its flip provides the lone offset.

Build the book accordingly. Any structure put on today needs to survive five-to-ten sessions of elevated realized and a non-trivial tail to panic. Size standard per Standard Size, harvest belly premium, skip front-week vol sales, and keep small convex hedges live until the regime resolves down rather than up.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - base case is persistence, not resolution, so trades must survive elevated chop with a 0.15 escalation tail.

Trading readVIX and VVIX both up, MOVE flat - equity vol is isolated from rates/credit. Confirming signal absent: this looks like a sentiment shock, not a systemic break. Watch MOVE for confirmation; absence keeps the regime contained.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

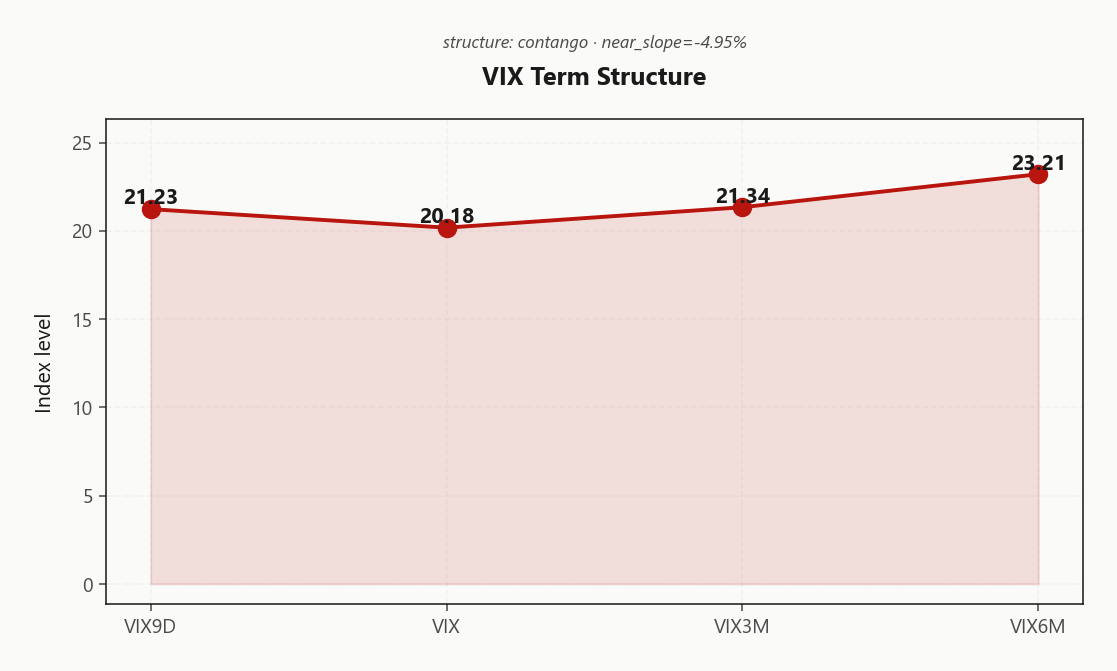

The VIX curve prints Contango on paper, but the front-end hump tells the real story - 21.23 sits above spot 20.18, leaving the near slope flattened and the curve mildly inverted at the wick. This is stressed contango, not relaxed carry - the front popped, the belly held, and the kink is now where the event premium lives.

The tail anchors cleanly: 21.34 at three months and 23.21 at six show no panic embedded out the curve. Forward 30→60 reads Flat term structure per derived, with the cleanest edge concentrated in the belly window - not the front week, where you are now paid only for headline jump risk.

Trade plan: skip front-week vol selling until the front-end hump rolls off. Harvest the belly at 30-45 DTE - that is where carry survives a still-expanding spot VIX without forcing you long gamma into a vanna-hostile tape.

What it means for your trading

Front-end humped above spot, tail unmoved - a stressed contango where carry exists only past the front week. Sell the belly at 30-45 DTE; the front is now compensation for jump risk, not premium edge.

Trading readContango preserved but flattened sharply on the front - carry trade survives in the belly, no longer in the front week. Curve is a stressed contango: don't sell front-week vol until VIX cools and the hump rolls off.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM implied at 17.73% sits cleanly above realized - RV20 prints at 13.27 - leaving VRP at 4.46% as live premium for systematic sellers. The IV-RV spread reads Moderate Premium: rich enough to pay, not so rich the trade is crowded.

But the cushion is thinning. RV20 had been trending beneath the longer-window anchor into today - realized was cooling, past tense. RV5 at 20.02 is the live read, and today's tape acceleration drags it higher into tomorrow's print. If RV5 lifts through RV20, the cushion compresses fast and front-week sellers wake up paying for headline risk they thought they had priced.

Operational read: harvest the belly. The thirty-to-forty-five DTE window offers the cleanest IV-RV spread and survives a one-print vol pop. Front-week IV is now compensation for jump risk, not edge - leave it for the desks paid to wear that tail.

What it means for your trading

VRP at 4.46% still pays sellers, but with RV5 at 20.02 already lifting against RV20 at 13.27, the harvest window is the belly - front-week premium is now jump-risk compensation, not edge.

Skew Convexity

Quarter-delta skew prints 4.52% with a smile ratio of 1.32% - puts paying a meaningful premium over calls, but ordered fear rather than left-tail stampede. The put wing at 18.57% towers over the call wing at 14.05%, while ATM sits at 15.75% - the call side is flat to inverted, pricing zero upside conviction.

Read it as a classic defensive posture: dealers and books are paying for downside protection, not chasing melt-up optionality. With smile ratio holding above the panic threshold but not blowing out, the bid for tails is structural, not capitulatory. Selling upside is the cheap edge here - call premium is barely compensating for path risk.

Trade implication: verticals beat outrights. Skew steepness makes naked puts expensive carry; put spreads finance the long leg by leaning on the bid in the wing. On the call side, short verticals or covered overwrites harvest the flat skew without taking naked short-gamma risk into a hostile vanna regime.

What it means for your trading

Skew at 4.52% with smile ratio 1.32% signals ordered fear - put wing rich, call wing flat. Prefer put spreads over naked puts and sell call verticals; skew geometry rewards spreads, punishes outrights.

Vol-of-Vol Structure

VVIX at 99.56 against VIX at 20.18 pins the ratio at 4.93 - squarely in Normal territory. The distribution hasn't gone bimodal yet; vol-of-vol is bid but orderly, not convex. Sizing guidance holds at Standard Size - full risk allowed, no need to cut book.

That said, today's VVIX print added 10.87% on the session - a yellow flag, not red. The market is paying up for optionality on optionality, which historically precedes either a fast cool-off or a regime escalation. Until the ratio breaks higher, premium-selling structures remain valid; the VVIX move is a tell to watch, not a trigger to act.

Trigger discipline: if VVIX punches through the panic threshold, halve size and overlay convex tails - the harvest game ends when vol-of-vol bifurcates. Below that, the Iron Condor at 30-45 DTE stays the cleanest expression.

What it means for your trading

Vol-of-vol is elevated but contained - VVIX/VIX ratio at 4.93 keeps sizing at Standard Size, with a hard pivot to half-size only if VVIX breaks the panic threshold.

Dispersion Spread

Index ATM IV at 17.73% sits noticeably beneath the single-name complex, with 29.21% in QQQ and 25.75% in IWM both running hotter than the headline tape. Cross-strike dispersion at 53.72 and cross-expiry at 1.48 confirm the spread is in the surface, not just the headline - name-specific risk is doing the work while index correlation stays sleepy.

The trade follows the geometry. Short index vol is the clean harvest: SPY premium is the cheapest leg of the complex while the basket pays you for risk it isn't actually warehousing. Avoid shorting single-name premium - QQQ-basket idiosyncratic vol is where the AI-narrative repricing is concentrated, and the AAPL/NVDA GEX churn at ranks one and four says dealers are still rebalancing names actively.

The risk to the dispersion trade is a correlation jump. If macro flow forces the basket to move together, index vol catches up violently and the spread compresses against you - keep size standard per Standard Size, and lean the structure into Iron Condor at 30-45 DTE where the skew funds the wings.

What it means for your trading

Sell index vol, fade single-name shorts: SPY ATM at 17.73% is the cheapest leg versus QQQ 29.21% and IWM 25.75%, and the spread compresses fast if correlation lifts - size standard, harvest at 30-45 DTE via Iron Condor.

Liquidity & Microstructure

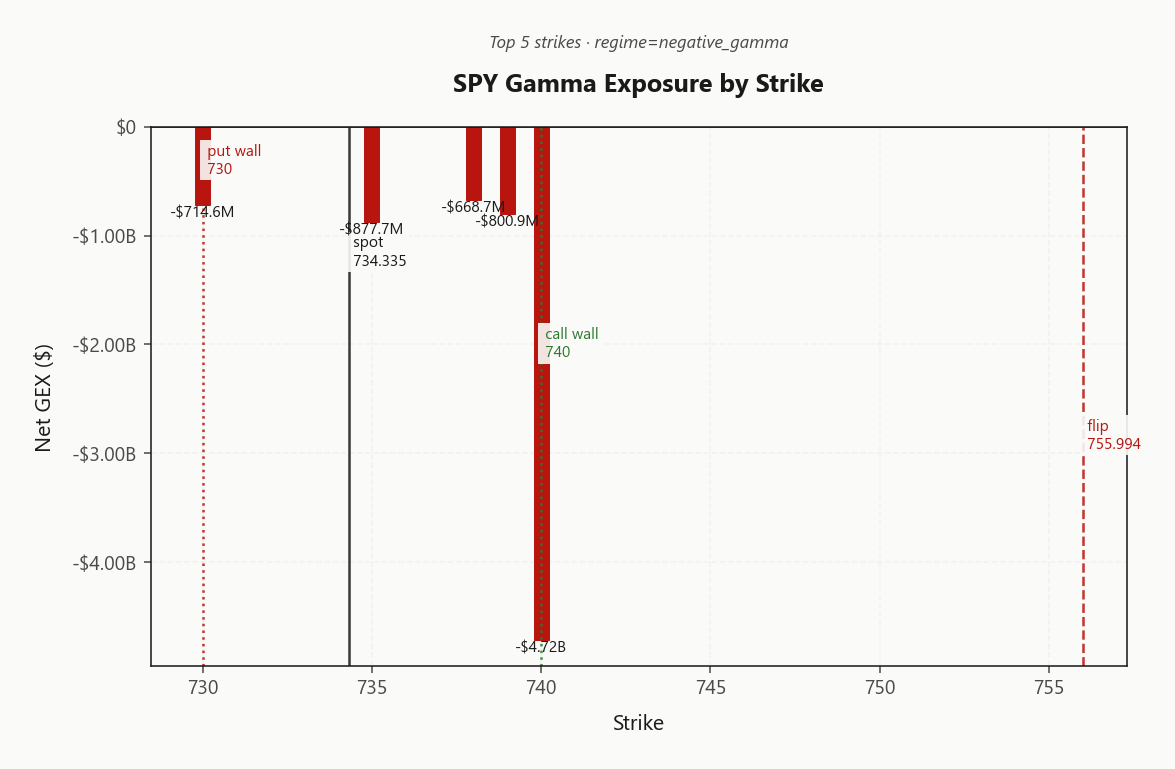

Spot at 734.34 trades beneath the gamma flip at 755.99, dropping the tape into Negative Gamma mechanics - dealer hedging amplifies moves rather than dampening them. The book is dominated by the 740.00 strike carrying -$4.72B net GEX, which acts as the near-term gravity well for hedging flow into the close.

Structural ballast sits well below at the 550 highest-OI shelf, but it is too far from spot to matter intraday. The actionable band is bracketed by the 740.00 call wall above and the 730.00 put wall below - fade rips into the wall, do not chase. A clean reclaim of 755.99 flips the regime; failure to hold 730.00 opens a gamma vacuum to the next OI shelf with no dealer cushion in between.

What it means for your trading

Sub-flip mechanics with concentrated OI at 740.00 mean dealer flow amplifies any directional push; trade the 730.00 - 740.00 band and treat a break of either as a regime event, not a fade.

Trading readHeavy negative gamma stacked at and just above spot in SPY - dealers will sell into rips and chase any break below the put wall. Trade the levels, not the chart: fade 740.00 short-term, only chase downside if 730.00 cracks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$40.02B - deeply negative and the dominant force in the book. Every uptick in 20.18 compels dealers to sell delta, not buy it, turning vol expansion into a self-reinforcing accelerant for the tape. This is the hostile vanna regime: spot weakness begets vol, vol begets more selling, and the loop only breaks when VIX rolls.

Working against that, net CHEX at $1.87B is constructively positive - charm bleeds dealer hedges back toward neutral into expiry and offers a stabilizer if the vol tape flattens through the close. But charm is a slow force; vanna wins any session where 25.65% is doing real work. Today it is.

The flow pivot sits at 731 (Max Pain) with current bias Neutral. Spot is camped on it - distance to pivot -0.4541523964 - so the regime is genuinely two-way. Reclaim flips dealer flow supportive; rejection hands the tape back to vanna.

What it means for your trading

Vanna is the lead force and it is hostile at -$40.02B; charm at $1.87B is a passive stabilizer that only matters if 20.18 stops expanding. Trade the 731 pivot as the regime switch - current bias Neutral, no edge until it resolves.

Cross-Asset Confirmation

The cross-asset tape refuses to confirm the equity vol pop. MOVE at 71.16 sits unchanged on the session (0%%) - rates and credit are not flinching, leaving equity vol as the isolated mover. That's a sentiment shock fingerprint, not a systemic break, and it caps how far this regime can extend without a rates/credit follow-through.

Inside the equity complex, the divergence is the lead. QQQ at 700.96 still trades above its flip at 660.99 in Positive Gamma territory - tech is the anchor holding the index up. IWM at 279.87 mirrors SPY's break, locked into Negative Gamma, confirming small-caps are the fragility tell. Cross-asset tone reads Unknown with regime divergence skewed Qqq Heavier.

Sentiment supports the same read: Fear & Greed at 42 prints Fear - jittery, not capitulating. Room remains for sentiment to drift lower before contrarian extremes signal a buy. Stay defensive, but don't fade the move yet.

What it means for your trading

Equity vol is isolated - 71.16 MOVE flat and QQQ above flip at 660.99 say sentiment shock, not systemic. Watch IWM at 279.87 for confirmation if regime escalates.

Scenario EV

Derived stack lands on Iron Condor with a best score of 47, edging the put spread alternative at 43. Sweet spot is the 30-45 DTE belly - far enough out to dodge the front-week vol hump, close enough to harvest before charm decays out. VRP context flagged Unknown, but with skew steep at 4.52% and call wing flat, the asymmetric wing pricing is the edge that picks condor over strangle.

Iron condor wins precisely because it does not take a directional bet into the Negative Gamma regime where vanna at -$40.02B punishes anyone leaning. Steep puts get sold rich, flat calls get sold cheap, and the body collects time decay while QQQ props the complex above its flip at 660.99. Sizing stays Standard Size per VVIX at 99.56 - normal vol-of-vol means full clip, no need to halve until the ratio breaks.

What it means for your trading

Sell the Iron Condor in the 30-45 DTE window at Standard Size; skew steepness and a Normal VVIX make the asymmetric wings the cleanest premium harvest available.

Actionable Summary

Trade plan: Sell Iron Condor in SPY at the 30-45 DTE window - harvests 4.46% VRP without taking a directional bet, and skew at 4.52% makes the asymmetric wings cheap. Score 47 edges put spreads at 43; sizing stays Standard Size with VVIX at 99.56 still in Normal territory.

Watch: the 731 pivot (Max Pain) - reclaim flips bias positive, loss confirms negative drift below the 755.99 flip. Regime read is Elevated / Watchful, half-life 15 sessions - base case is multi-day chop, not capitulation.

Avoid: front-week vol selling while VIX expands from 25.65% - gamma is asymmetric and the front of the curve already flattened. Skip naked single-name premium; dispersion punishes shorts with QQQ ATM IV running hot. Hedge tails with small SPY put spreads - Fear sentiment has room to fall before contrarian extremes trigger.

Hot jobs report plus deepening tech sell-off is the day's macro setup - supports the elevated regime call and the lack of MOVE confirmation in equity vol

Rotation out of tech into defensives (XLV calls) confirms the divergence: positioning is reshuffling, not capitulating - informs the fear-not-panic read

Geopolitical shock now hitting real-economy data abroad - global growth fingerprint that could shift the regime from idiosyncratic equity vol to broader risk-off

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 21.57 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 755.99 against a spot of 734.34. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 17.73% with a volatility risk premium of 4.46%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 20.18. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime