Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

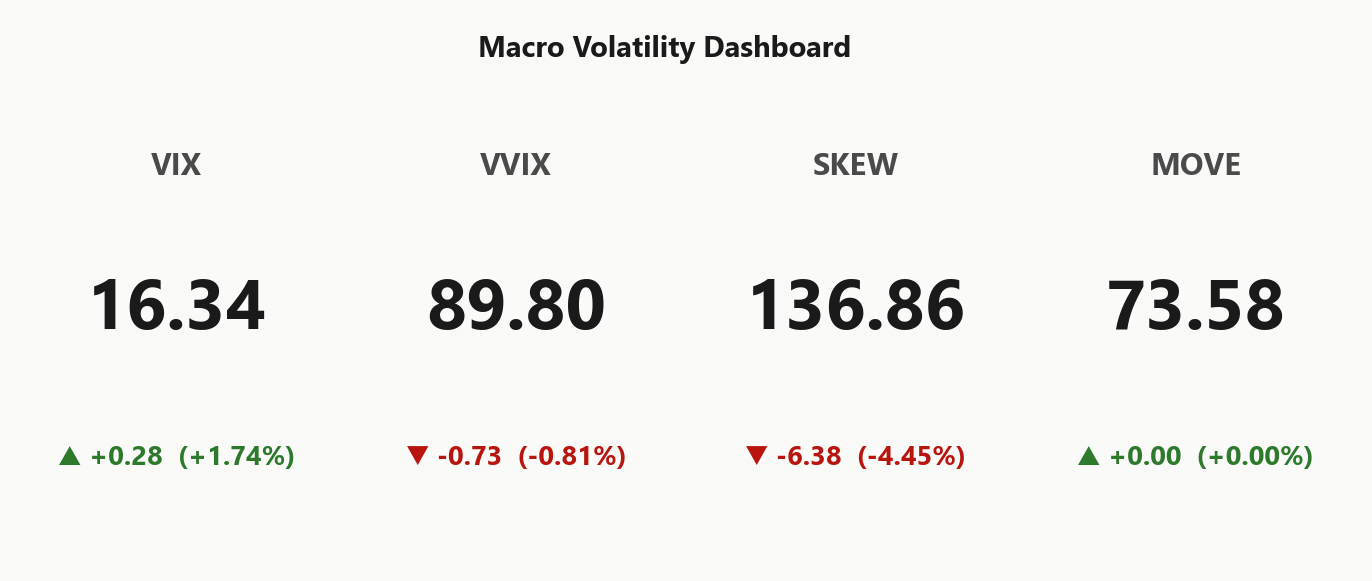

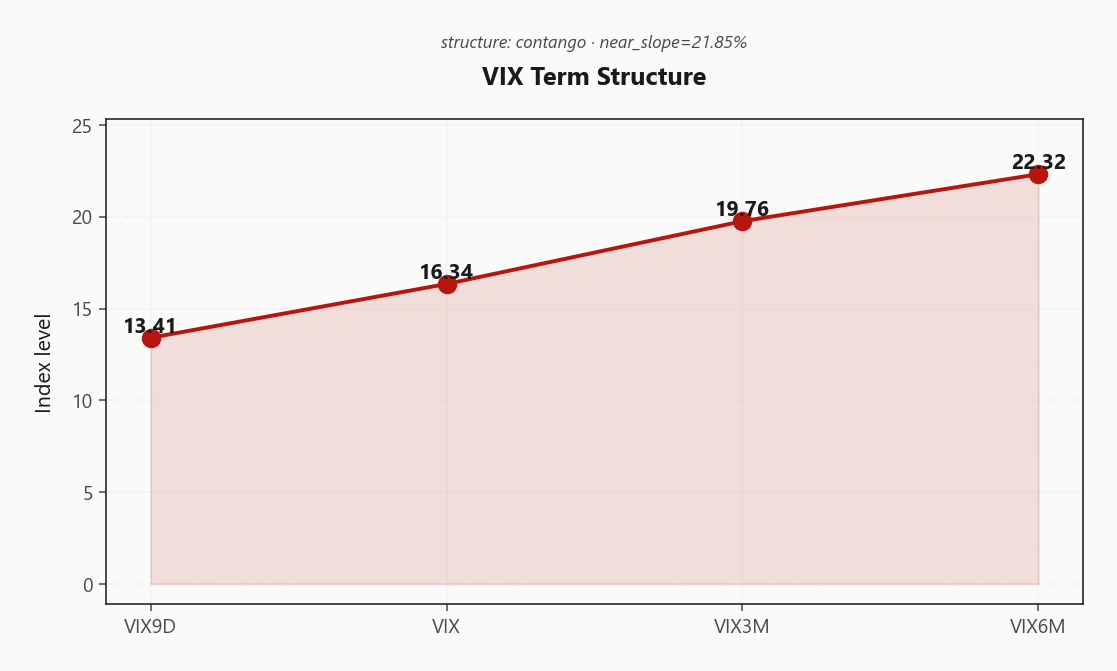

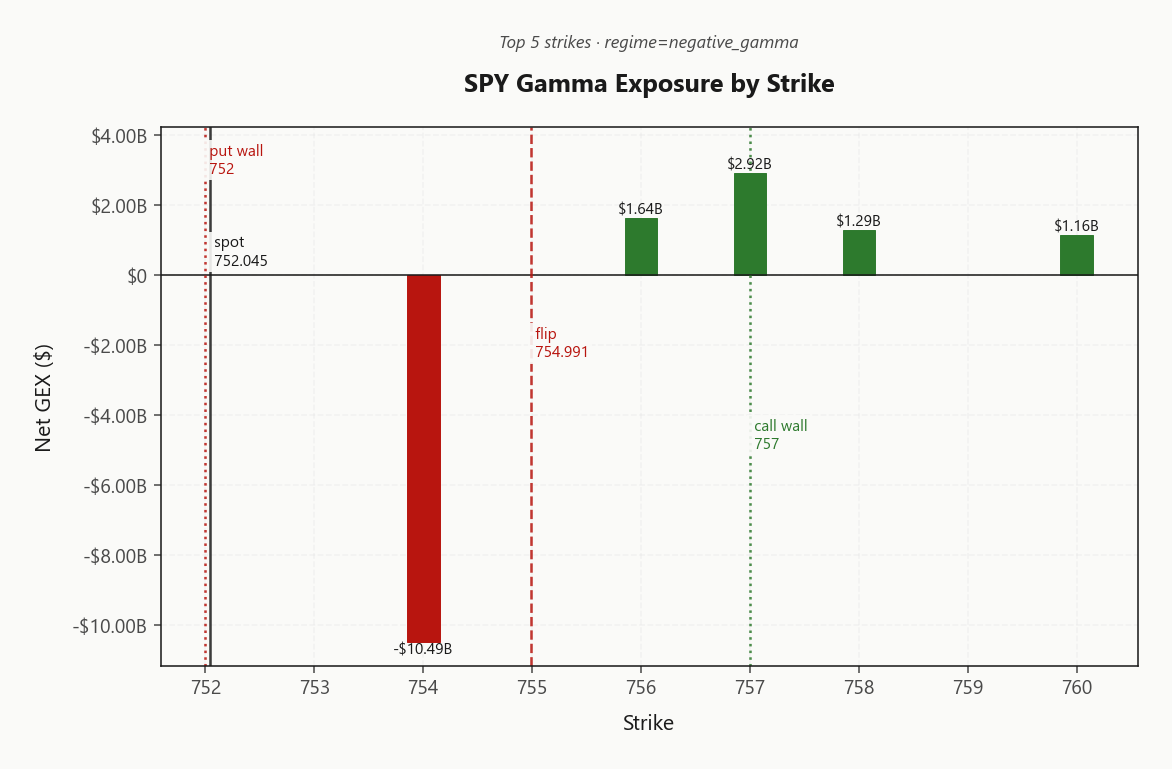

SPY at 752.05 sitting on its put wall and barely below the gamma flip at 754.99 - regime is Negative Gamma with net GEX at -$14.88B, meaning dealers amplify moves rather than dampen them. Call wall 757.00, put wall 752.00, max pain 755.00 - the entire decision zone is compressed inside a few handles, so directional conviction is low and breakout risk is high. 0DTE owns 72.6% of today's net GEX, concentrating dealer flow into the session close. Dealers are short delta (-$26.28B) and short vanna (-$9.1B) - a vol uptick sells more delta, accelerating downside if VIX presses. VIX at 16.34 with VIX9D at 13.41 and VIX3M at 19.76 gives steep contango carrying 21.85% - short-vol carry intact. VVIX at 89.80 with VVIX/VIX ratio at 5.50 signals Low jump risk, supporting standard sizing. IWM diverges with positive gamma above its flip - small caps stable, large caps fragile. Bottom line: fade extremes into 757.00 and 752.00, run Iron Condor in 30-45, abandon mean-reversion if 752.05 loses 752.00 on volume.

Negative gamma at 754.99 with steep contango - dealers amplify moves until 757.00 reclaims

SPY opens straddling its gamma flip at 754.99 with dealers short -$14.88B of gamma - any sustained break amplifies in the direction of travel. Steep VIX contango (Steep contango - vol sellers favored) and low VVIX (Low) keep vol sellers favored, while IWM diverges into positive gamma above its flip. The trade is Iron Condor in the 30-45 window, sized standard until vol-of-vol turns.

Regime Assessment

Regime classification reads Elevated / Watchful with VIX anchored at 16.34 - elevated enough to demand respect, well short of panic. Signal color Yellow says watchful, not defensive: keep risk on, keep size standard, but don't pretend the tape is calm.

The sticky read is the half-life of 15 sessions - this regime doesn't dissolve overnight. Transition math backs it: only 0.05 probability of escalating to panic over five sessions, versus 0.45 of de-escalating to low over ten. Asymmetric, but slow - multi-week hold in Elevated is the base case.

Trade implication: structure for persistence, not transition. Short-vol carry stays paid, defined-risk premium harvest in the 30-45 window remains the vehicle, and tail hedges are cheap enough to layer without conviction. The regime won't break in a week; respect it, don't fight it.

What it means for your trading

Sticky Elevated / Watchful regime with 15-session half-life and asymmetric transitions favors persistence trades over regime-change bets. Signal Yellow - watchful, standard size, harvest the carry.

Trading readVIX up, VVIX down, SKEW down, MOVE flat - partial divergence. Spot vol bid without vol-of-vol confirmation says today's tape is local equity noise, not a systemic risk-off pulse. Stay constructive on short vol.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

The front-end depression is the catch: with VIX9D at the low end of regime, there is no event premium priced into the spike window. Selling the front pays for nothing already in the tape. The edge sits in the belly - 30-45 DTE - where roll-down compounds against a steeper slope without sitting on top of the next gap risk.

Calendar spreads and defined-risk short premium remain favored while Steep Contango holds. The fracture signal is binary: a VIX9D cross above VIX inverts the carry and the regime call shifts the same session.

What it means for your trading

Steep contango with depressed front-end keeps short-vol carry intact in the 30-45 belly; the first sign of regime fracture is VIX9D crossing back above 16.34.

Trading readSteep contango with VIX9D well below VIX and VIX3M - the textbook short-vol carry setup. Slope tells you the market expects no near-term stress; backwardation would be the first red flag for regime change.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.16% prints comfortably above HV20 at 8.99 yet still trails HV60 at 14.26 - the tape has gone quiet, but options remain priced for the prior regime's episodes. That gap is the entire trade: short-vol carry gets paid against the recent calm, while the longer-window realized refuses to let pricing collapse to the floor.

VRP at 3.17% confirms positive but unspectacular compensation - premium harvest works, it doesn't print money. Best edge sits in the 30-45 window where contango roll-down compounds with realized decay, and the Iron Condor structure scoring 46 is the cleanest expression. Skip the front week - IV-HV20 spread doesn't compensate for negative-gamma whipsaw inside expiry.

The risk is asymmetric and fast: if HV5 starts climbing toward IV, the spread collapses in a single session and the carry trade becomes a P&L donor. Watch realized closely - vrp_assessment reads Unknown, so don't oversize on a regime label that hasn't fully validated.

What it means for your trading

IV at 12.16% rich to HV20 8.99 but cheap to HV60 14.26 with VRP 3.17% - harvest in 30-45 DTE, abandon if HV5 turns up.

Skew Convexity

Quarter-delta put IV at 16.01% trades meaningfully rich to ATM at 14.25%, while the quarter-delta call prints 14.43% - barely a tick above the money. The asymmetry reads as an ordered downside bid, not a panic grab. Skew at 1.58% sits steep but well-behaved; smile ratio 1.11% confirms left-wing premium without the convex blow-out that fades in days.

Call wing pancaked against ATM tells you the tape prices zero upside conviction - no melt-up optionality is being paid for, only protection. SKEW at 136.86 corroborates moderate, not extreme, tail demand.

The trade construction follows: put spreads beat outright puts - you're long the rich wing and short an even richer body, financing the convexity. Fund the structure by selling the flat call wing against, since upside premium is offered cheap. Don't pay for naked tail convexity here; the bid is ordered, not hysterical, and the wing is too well-behaved to harvest meaningfully by selling it outright.

What it means for your trading

Put skew steep but ordered at 1.58% with smile ratio 1.11% - express downside via put spreads funded by flat-wing call sales, not naked tail buys.

Vol-of-Vol Structure

VVIX at 89.80 sits at the Low end of regime, and the VVIX/VIX ratio at 5.50 tells you everything: no binary outcome priced in, no vol-of-vol bid, no jump premium being paid. The wing market is not pricing convexity demand, and that is the green light for systematic short premium.

Sizing guidance prints Standard Size - appropriate for the regime but not aggressive. With VIX at 16.34 and the ratio sub-six, tail hedges are cheap on an absolute basis, but there is no convexity bid to fade, so don't expect to harvest by selling the wing. Free-and-clear for short-vol carry until the wing wakes up.

Trigger to revisit: VVIX printing above the century mark. That is the line where vol-of-vol turns from regime support into regime risk, and sizing comes down before the trade does.

What it means for your trading

Vol-of-vol is firmly Low with VVIX/VIX at 5.50 - short premium carries at Standard Size, and the playbook only changes if VVIX reclaims the century mark.

Dispersion Spread

Index vol screens cheap against the basket: SPY ATM IV at 12.16% trades materially under QQQ at 20.33% and IWM at 21.39%. That's the diversification dividend at work - single-name idiosyncratic dispersion (Broadcom-style guide-misses still resetting AI capex expectations) lifts the components while correlation drag pins the index. The trade is short index vol, not single-name premium.

QQQ VRP at 4.69% prints richer than SPY at 3.17% - relative-value short QQQ vol versus long SPY vol harvests the dispersion without taking outright direction. Cross-asset regime reads Aligned, so the basket isn't fracturing - it's just paying you to be the index.

The trap: cheap single-name vol looks like a layup until the next idio print blows through a wing. Keep short premium on SPY/SPX where the basket smooths it out, and buy back single-name optionality if you need convexity. Index hedges will not transmit single-stock pain - wrong tool for the dispersion regime.

What it means for your trading

Index vol is the cheap leg versus QQQ and IWM - sell SPY/SPX premium, fade QQQ vol against it for the dispersion spread, and leave single-name short-vol alone while idiosyncratic prints keep driving the basket.

Liquidity & Microstructure

SPY prints 752.05 against a gamma flip at 754.99 - spot and regime line sit on the same tick, so every print crosses dealers from amplifier to dampener and back. Directional plays die in this overlap; the tape needs to commit before any trend trade earns its premium.

The magnet is 754.00, carrying -$10.49B of negative gamma against 286648 in total OI - that is today's gravitational center, not the highest-OI strike at 565, which sits far below as legacy long-dated paper and contributes nothing to intraday hedging flow.

Walls bracket a handle-tight decision box: put wall 752.00, call wall 757.00. Lose the put wall on volume and dealer hedging sells into the move - pure negative-gamma accelerant. Reclaim the call wall and the regime flips to squeeze fuel as the short-gamma book covers. Trade the breach, not the chop between.

What it means for your trading

The decision zone compresses around the flip at 754.99 with the magnet strike 754.00 dominating intraday dealer flow. Fade chop inside the walls, but treat a volume break of 752.00 or reclaim of 757.00 as a regime change rather than a mean-reversion entry.

Trading readMassive negative GEX cluster at the put wall says dealers amplify any break lower - the call wall above is the only structural roadblock, and crossing it flips the regime to mean-reversion mode.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The single binary is the Put Wall pivot at 752. Spot sits -0.0059836845 from it - a Neutral read where every handle crosses into a different dealer regime. Below the pivot, hedging amplifies the move; reclaim it and dampening returns. Trade the level, not a thesis.

What it means for your trading

Vanna and charm both negative and aligned - dealers are forced sellers into a vol bid or the close. The Put Wall at 752 is the switch between amplification and dampening; respect it.

Cross-Asset Confirmation

Cross-asset tape reads Aligned on the regime axis but bifurcated on the structural one. MOVE at 73.58 sits flat with no Treasury vol shock bleeding through, and Fear & Greed prints Neutral at 53 — neither credit nor sentiment is flagging a systemic episode. This is not a macro risk-off; it is a localized equity-vol event with the rates and sentiment plumbing intact.

The real signal is the small-cap divergence. IWM at 288.32 sits in positive gamma above its own flip while SPY and QQQ — with QQQ at 734.42 — remain pinned in negative-gamma territory. That is leadership rotation, not broad fear: dealer books stabilize small-caps while mega-cap chip-led weakness drives the index pain. Geopolitical premium from Iran and Lebanon has already bled out — oil and gold confirm the peace tape, removing a tail driver.

Bottom line: trade the structural divergence, not the headline. The hedge against this read is IWM rolling negative — until it does, fragility stays isolated.

What it means for your trading

Cross-asset signals are Aligned with MOVE flat and sentiment neutral — this is isolated mega-cap fragility, not a macro pulse. IWM positive gamma above flip is the canary; watch it for the first sign of broad regime change.

Scenario EV

The book scores cleanly to Iron Condor at 46, with the 30-45 DTE window the sweet spot - past front-end event risk, before back-month vol expansion compresses carry. VRP reads Unknown against ATM IV at 12.16%, vol-of-vol prints Low on VVIX 89.80, and the curve carries Steep contango - vol sellers favored - three independent green lights for defined-risk premium harvest.

Naked strangle scoring is materially behind - negative gamma at the flip 754.99 punishes undefended premium when dealers amplify the next break, and that's the structural reason the condor wins on score. Put spread is the directional alternative at 35, and only earns the seat if tape commits below 752.00 on volume.

Sizing stays Standard Size - VVIX/VIX at 5.50 gives the green light, the Elevated / Watchful regime keeps it short of full risk. Re-rack the trade only if VVIX bids or contango fractures.

Trade the regime, not the level. Run Iron Condor in the 30-45 DTE window where contango roll-down compounds with VRP decay - defined-risk premium harvest is the highest-scoring vehicle here, with put spreads as the directional tilt if the tape commits bearish. Naked front-week premium is a trap: VIX9D at 13.41 against VIX 16.34 means no event premium near, and SPY's negative-gamma footing leaves sellers under-compensated for whipsaw.

Watch 752 as the single binary. Spot at 752.05 sits on the Put Wall - break below and dealer flow turns accelerant, reclaim above and dampening returns. IWM diverging into positive gamma above its flip says this is mega-cap fragility, not macro fear; Aligned regime tape lets short-vol carry stay on.

Size Standard Size. VVIX at 89.80 with ratio 5.50 gives the green light; buy cheap convexity in 30-45 DTE while it isn't bid. Regime Elevated / Watchful with half-life 15 sessions stays sticky - re-evaluate only if VVIX prints above 100.

What it means for your trading

Iron condor in 30-45 DTE is the trade, 752 is the line, and Elevated / Watchful regime stickiness keeps the playbook intact until vol-of-vol or VIX9D give a different signal.

Broadcom guide-miss as the headline drag - single-name AI capex disappointment now resets QQQ implied beta and explains the SPY-QQQ-IWM regime divergence we're seeing.

Tax-policy double-taxation risk for top earners is a slow-burn portfolio rebalancing catalyst - watch for after-hours flows in muni and tax-advantaged structures, not immediate index impact.

Iranian oil discounting on weak Chinese demand confirms the geopolitical risk premium has bled out - vol sellers get an additional tailwind as the energy event premium decays.

China cutting domestic fuel prices reinforces the global demand-soft narrative - bearish for commodity-linked equities, supportive for the disinflation trade and the contango carry.

Dollar slipping from two-month highs on Iran de-escalation removes a key drag on multinational EPS - supports the rotation story (IWM strength) but doesn't unwind the chip-led tech weakness.

Oil down on Lebanon-Israel ceasefire confirms the geopolitical premium is being unwound in real time - energy vol sellers get rewarded, but headline risk of re-escalation keeps tail bid asymmetric.

Lebanon-Israel ceasefire implementation is the macro overhang reduction the equity tape needs - combined with chip weakness this is why rotation, not broad selling, is the read.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Neutral, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.99 against a spot of 752.05. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.16% with a volatility risk premium of 3.17%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.34. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime