Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

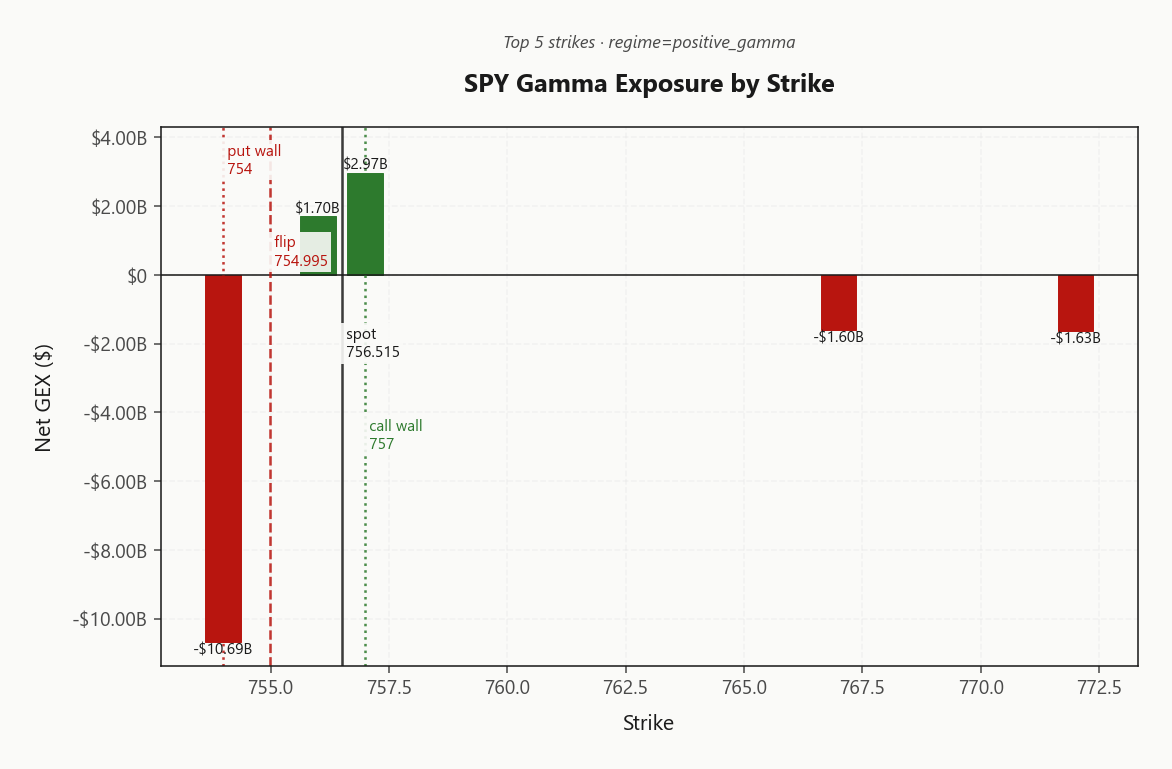

SPY at 756.52 is in a Positive Gamma regime with net GEX of -$16.14B - dealers long gamma, intraday moves dampened. The map: call wall 757.00, put wall 754.00, gamma flip 755.00 - spot is pinned at the call wall, neutral bias with mean-reversion edge. 0DTE drives 70.3%% of GEX, so the close will magnet toward 755.00. Vanna at -$55.03B and charm at -$2.1B mean a vol spike sells dealer delta - downside still has tail risk if VIX leaves 15.55. Term structure is Contango with VIX9D at 12.91 vs VIX3M at 19.36 - front carry is rich, VRP at 2.11% confirms premium sellers paid. The QQQ divergence (Negative Gamma with spot below flip 740.78) is the leading tell - tech weakness amplifies, SPY breadth masks it. Bottom line: harvest the iron condor structure recommended at Iron Condor in the 30-45 DTE bucket, fade strength into 757.00, but pull size if QQQ pierces 739.00.

Positive gamma cushion intact on SPY at 756.52, but QQQ slips below flip - divergence is today's tell

SPY sits a hair under its call wall at 757.00 with dealers long gamma and 0DTE driving 70.3%% of total exposure. QQQ has slipped below its gamma flip at 740.78, flipping dealers short - the cross-index divergence (Spy Heavier) is the actionable signal. Steep VIX contango (Contango) and a low VVIX/VIX ratio (5.71) keep premium sellers in the driver's seat.

Regime Assessment

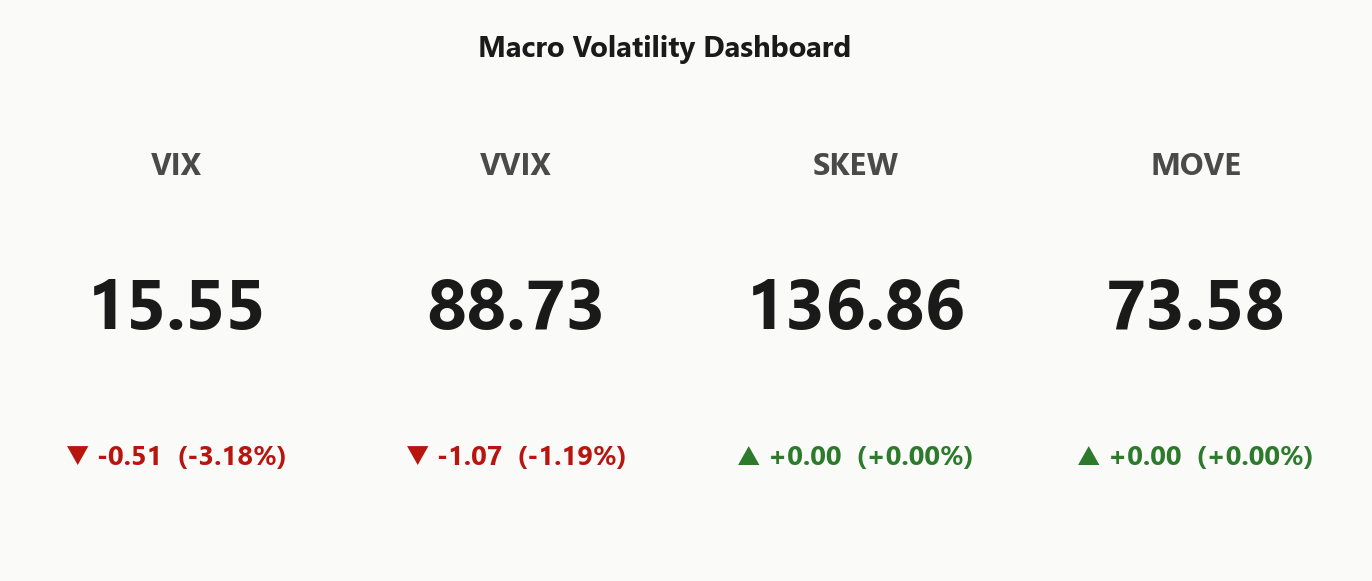

The tape sits in an Elevated / Watchful bucket with VIX at 15.55 - carry edge is real but not generous, and the transition risk into a higher-vol regime is non-trivial enough to size with discipline rather than bravado. This is a regime to harvest, not to lever.

Probability of a jump to panic over the next handful of sessions is 0.05 - low, but not zero, and the QQQ flip into Negative Gamma is precisely the kind of leading edge that precedes a regime break if it spreads. More constructively, the probability of decay into a lower-vol bucket over the next two weeks sits at 0.45 - meaningful tailwind for premium sellers willing to stay structured.

Half-life prints at 15 sessions: sticky, but not permanent. Plan around two weeks of regime persistence, anchor structures to that horizon, and pre-commit to a stop if QQQ pierces 739.00.

What it means for your trading

Elevated/Watchful at VIX 15.55 with a 15-session half-life - short-vol carry is paid, but the 0.05 jump-to-panic probability and live QQQ divergence demand structured risk, not naked size.

Trading readVIX down, VVIX subdued, MOVE quiet, SKEW elevated but stable - all confirming each other on a benign-but-watchful tone. No divergence flag yet, so trust the carry regime.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

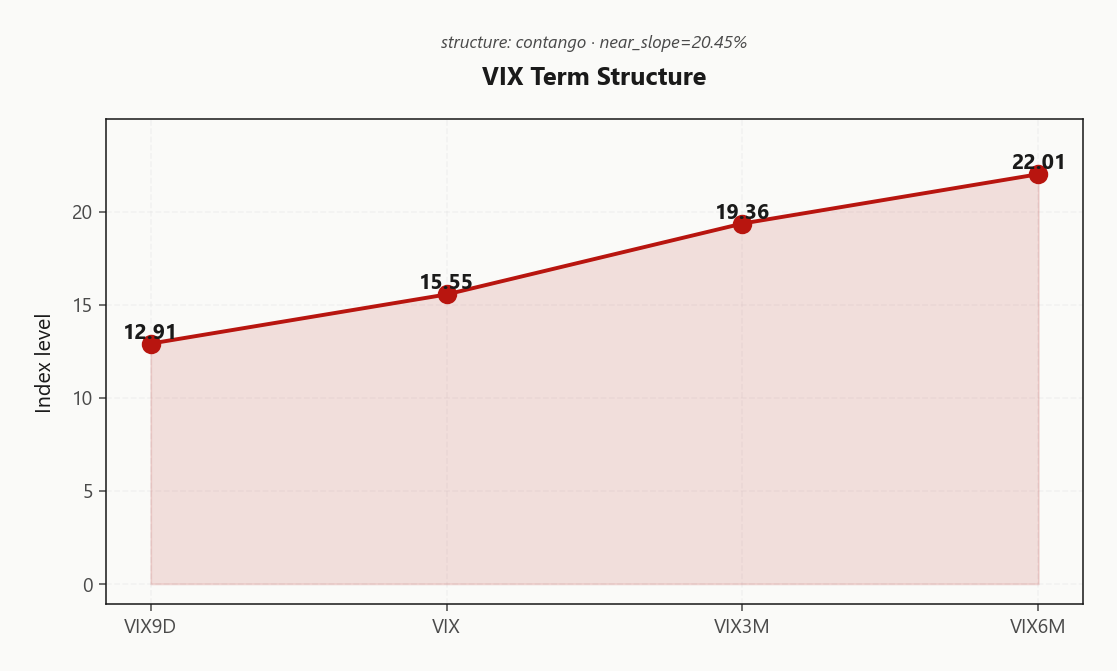

The curve is doing the talking: 12.91 VIX9D against spot VIX at 15.55 is textbook near-term complacency, and the Contango shape pays sellers cleanly at the front. The slope is sharp where it matters - 20.45% of carry edge sits in the front bucket, which is where the theta-to-vega ratio is most favorable.

Roll out and the story changes. VIX3M at 19.36 and VIX6M at 22.01 are not pricing the same complacency - the curve is telling you the market accepts a structurally higher long-run vol floor than today's spot implies. Forward 30-to-60 and 60-to-90 both reprice meaningfully higher, so anything sold past the belly is sitting on a much flatter slope with less carry to compensate the gamma exposure.

Play it tight: harvest in the 7 - 14 DTE window where the Steep Contango regime is most generous, and resist the temptation to extend past 60 DTE where the curve flattens and the edge evaporates.

What it means for your trading

Front-end VIX9D vs VIX gap is the cleanest carry trade on the board, but VIX3M and VIX6M warn that the long-run vol floor is higher than spot - keep short-vol tenor inside the front bucket where Steep Contango pays.

Trading readContango with a sharp near-term slope = carry trade is live, but the curve rolls up fast - limit short-vol tenor to under 30 DTE to avoid sitting in the steep part of the curve.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 10.99% sits well clear of trailing realized - 20-day realized prints 8.88 with 5-day at 6.77, leaving HV20 of 8.88 meaningfully below screen vol. VRP at 2.11% reads Moderate Premium - options are expensive to the moves the tape is actually delivering, and premium sellers have been paid in size.

QQQ tells the same story, louder: ATM IV at 18.33% versus HV20 at 14.78 leaves carry even richer than the broad index - consistent with dealers short gamma below the QQQ flip and bidding for downside protection. IWM is the outlier - VRP at 0.47% is compressed, with small-caps realizing near what they're pricing and almost no edge in selling that vol.

Best harvest sits in SPY and QQQ short-vol structures inside the dealer pocket, sized for the 30-45 DTE bucket. Skip IWM premium selling - the carry isn't there.

What it means for your trading

VRP is live and asymmetric across the complex - SPY ATM IV at 10.99% and QQQ at 18.33% are meaningfully rich to realized, while IWM VRP at 0.47% offers no edge. Sell index vol, leave small-caps alone.

Skew Convexity

Quarter-delta skew sits at 1.44% points with put 25d IV at 13.3% against call 25d IV at 11.86% - a textbook defensive bid, not a panic chase. The smile ratio at 1.12% tells you the upside wing is flat: nobody is paying for convexity into 757.00, the entire convexity premium is concentrated in the downside tail.

QQQ skew is steeper at 2.83%, consistent with its slip below the flip at 740.78 - tech is hedging more aggressively than the broad tape, and the cross-index print is Spy Heavier. ATM IV at 12.78% against the put wing leaves left-tail vol bid but orderly - no kink, no dislocation.

Trade implication: put spreads over naked puts. The tail is bid but not cheap; financing the long leg with a short lower-strike put captures the skew without overpaying gamma. Skip upside calls - the flat call wing is telling you dealers, not buyers, set that price.

What it means for your trading

Skew is defensively bid but ordered - put 25d IV at 13.3% vs call 25d IV at 11.86%, with smile ratio 1.12% confirming no upside conviction. Trade put spreads, not naked puts; QQQ's steeper 2.83% skew is where the real tail bid lives.

Vol-of-Vol Structure

VVIX at 88.73 is sitting well off panic territory, and the VVIX/VIX ratio at 5.71 lands squarely in the Low regime - no bimodal jump risk being priced into the surface, no convexity bid for tail buyers to lean on. The vol-of-vol tape is telling you the same thing the front of the VIX curve is: dealers are not paying up to hedge against a vol shock, and the carry trade is structurally clean.

That permits Standard Size on short-vol structures - no defensive haircut needed against an option-on-vol regime shift. The iron condor and front-week premium sales the rest of the surface argues for go on at full clip here, with VIX anchored at 15.55 and no second-derivative warning flashing.

Caveat worth watching daily: a VVIX drift toward the 110-120 zone would force half-sizing and rebuild the case for buying convexity rather than selling it. Today it is not close, but it is the single number that flips this section from green to yellow - keep it on the screen alongside spot.

What it means for your trading

Vol-of-vol is benign at 88.73 with the VVIX/VIX ratio at 5.71 - Standard Size on short-vol structures is endorsed, but a VVIX push into the 110s flips the signal.

Dispersion Spread

Index vol prints moderate with SPY ATM IV at 10.99% sitting well inside QQQ at 18.33% - the gap is wide enough to flag active dispersion, not a unified vol regime. Cross-strike dispersion at 76.68 versus cross-expiry at 3.37 tells the same story: the surface is being repriced laterally across names, not vertically across tenor.

The mechanical driver sits in single-name flow. MSFT leads the GEX repositioning tape, with AAPL and GOOGL stacked behind it - concentrated mega-cap dealer rebalancing that the index hedge isn't capturing. This is precisely the setup where single-name vol screens rich on a basket-adjusted basis while SPX premium remains the cleaner short.

Trade implication: harvest Iron Condor structures on SPY/SPX in the 30-45 DTE bucket where the surface is well-anchored. Avoid cross-name volatility arbitrage until dispersion compresses - single-name hedges are carrying a premium the index won't pay you for.

What it means for your trading

Dispersion is moderate and concentrated in mega-cap tech - index short-vol is the cleaner expression than single-name structures while MSFT drives the GEX tape.

Liquidity & Microstructure

The book's center of gravity sits at 757.00, where the top dealer obligation - net GEX of -$10.69B at the 754.00 strike - anchors the tape. With spot a hair beneath that wall and dealers carrying a Positive Gamma book, intraday flow dampens moves: rallies meet supply, dips get bought. The wall is simultaneously magnet and ceiling into the print.

Below the action, the highest open-interest strike at 565 sits deep beneath spot - a long-dated hedge stack, structural rather than reactive. That inventory isn't what drives today's flow; it's the gamma cluster above that owns the close. The 754.00 put wall frames the downside pocket where dealer bid persists.

The level that matters is the gamma flip at 755.00. Hold above it and the dampening regime persists; pierce it and dealer flow reverses from suppressing volatility to amplifying it. QQQ already sits on the wrong side of its own flip - the cross-index divergence (Spy Heavier) is the leading indicator. Trade fades into the wall, not breakouts through it.

What it means for your trading

Spot pinned just under 757.00 with dealers long gamma - mean-reversion edge inside the pocket, but 755.00 is the binary: a break flips the regime from dampener to amplifier.

Trading readGamma profile shows a thick positive cluster at the call wall 757.00 acting as a magnet AND ceiling - mean reversion wins inside the wall, but a break flips dealer flow from dampening to amplifying. Trade fades into walls, not breakouts.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna sits deeply negative at -$55.03B, which means any uptick in vol forces dealers to sell delta - the cushion holds in calm tape, but a VIX lift off 15.55 flips the book into an amplifier on the way down. Asymmetry, not symmetry, is the read.

Charm reinforces the same direction. Net CHEX of -$2.1B bleeds long dealer delta as the session ages, so absent a fresh bid the natural close-flow is downward pressure into the print. The charm pivot sits at 757 - the call wall itself - and flow direction inverts through that line.

Current bias resolves Neutral, but neutral here is loaded: vanna asymmetry plus charm decay tilt the edge toward fading strength into 757.00 rather than chasing it. Pull risk if QQQ pierces 739.00 - that is where the negative-vanna cascade gets a real catalyst.

What it means for your trading

Dealers are stable in spot but hostile to vol - a VIX lift off 15.55 turns the -$55.03B vanna stack into a seller, and charm at -$2.1B bleeds delta into the close. Fade the call wall, respect the pivot at 757.

Cross-Asset Confirmation

Cross-asset tape reads Spy Heavier with no credit or rates stress: MOVE sits at 73.58, bond vol quiet enough to rule out a systemic signature, while Fear & Greed prints 55 (Neutral) - dead-center, no contrarian edge to lean against.

The fracture is intra-equity, not macro. QQQ at 740.55 has slipped below its flip into Negative Gamma, yet IWM at 291.22 holds Positive Gamma - small caps absorbing what tech is shedding. SPY's Positive Gamma cushion masks the rotation underneath the index print.

Classification: idiosyncratic mega-cap tech repricing, not a regime break. Trade the divergence (fade strength into 757.00, pull size if QQQ pierces 739.00) - don't position for a macro shock the bond and sentiment tape isn't validating.

What it means for your trading

Cross-asset confirms rotation, not regime break: MOVE at 73.58 and F&G at 55 (Neutral) deny macro stress, while IWM at 291.22 holds positive gamma against QQQ at 740.55 flipping negative - the cascade trigger is tech-internal, not systemic.

Scenario EV

The setup scores Iron Condor as the cleanest carry expression - iron condor edge at 41 dominates the put spread alternative at 28. Active VRP at 2.11%, Contango in the curve, and a subdued VVIX/VIX ratio of 5.71 stack the deck for defined-risk premium harvest.

Pitch the structure in the 30-45 DTE bucket - the sweet spot where theta bleed compounds with curve carry before the contango slope flattens. Anchor call wings around 757.00 and put wings near 754.00, sitting defined-risk inside the dealer pocket with 755.00 as the regime tripwire below.

Run Standard Size - VVIX at 88.73 permits it, but half the book if it pushes toward the panic zone. Cut short-vol exposure if QQQ pierces 739.00; that is the cascade trigger, not the SPY tape.

What it means for your trading

Iron condor in the 30-45 bucket with wings at 757.00 and 754.00 is the highest-EV expression of the Contango plus subdued VVIX regime. Cut exposure on a QQQ break of 739.00.

Actionable Summary

Trade: sell Iron Condor in the 30-45 DTE bucket, anchoring wings to 757.00 on the call side and 754.00 on the put side. Fade strength into the wall - dealers are pinned long gamma at -$16.14B and the charm pivot sits at 757, both reinforcing mean reversion inside the pocket.

Watch: SPY's 757 pivot, the QQQ flip at 740.78, and any VIX departure from 15.55. A QQQ break through 739.00 is the cascade trigger - exit short-vol immediately. Avoid naked long-vol (carry burns under 2.11% VRP), single-name dispersion arb, and chasing calls above the wall.

Size: standard - VVIX at 88.73 permits it; halve if it pushes past the panic threshold. Regime:Elevated / Watchful, sticky for roughly 15 sessions - plan trades around that horizon.

What it means for your trading

Harvest the iron condor inside the 754.00 - 757.00 pocket while dealers remain long gamma; the QQQ break below 740.78 is the only signal that voids the trade.

Supreme Court ruling on SEC disgorgement is a structural regulatory signal - affects enforcement risk pricing for any firm in active SEC proceedings and clarifies the cost of compliance shortcuts.

Dollar slipping from two-month high on Iran talks ties directly into the contango/low-VVIX setup - easing geopolitical premium reinforces the short-vol carry trade.

Cramer flagging Broadcom-led chip weakness directly maps to QQQ's flip below its gamma pivot - semis are the mechanical driver of today's tech-vs-broad-market divergence.

Hormuz oil flow uncertainty keeps an embedded tail premium in vol surface even as headline VIX compresses - explains why 25d put skew hasn't collapsed.

Airline industry summit confronting fuel shock signals corporate guidance risk into earnings - watch transport names for vol expansion ahead of next reporting cycle.

Broadcom-led chip selloff with oil pulling back is the cleanest read on today's setup: idiosyncratic tech weakness, not macro stress - confirms the rotation classification, not regime break.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Neutral, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 755.00 against a spot of 756.52. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 10.99% with a volatility risk premium of 2.11%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.55. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime