Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY at 756.52 is locked inside a positive-gamma corridor - net GEX -$6.65B with spot just below the 757.00 call wall and the 754.97 flip directly beneath. Put wall 754.00, max pain 755.00, and 59.5% of gamma sitting in 0DTE - the tape is pinned by dealer mean-reversion until the flip cracks. QQQ is the fragile leg: spot 739.80 versus flip 740.39 puts it in Negative Gamma, where dealer flow amplifies any directional push. Vanna and charm are net hostile across the complex (negative -$54.12B VEX, negative -$3.48B CHEX) - vol up means dealers sell delta, and time decay leans them short into the bell. VIX at 15.19 with Contango term structure and VVIX at 85.50 keeps the Standard Size regime intact - vol sellers still get paid. Recommended structure: Iron Condor in the 30-45 bucket, anchored on SPY where regime is cleanest. Bottom line: fade strength to 757.00, respect the flip as your stop, and treat QQQ as the canary - if it breaks 739.00 hard, SPY's cushion gets tested fast.

SPY positive gamma cushion intact while QQQ flips negative - Spy Heavier divergence is the lead.

The index complex is split: SPY trades inside a tight positive-gamma corridor while QQQ has slipped under its gamma flip into negative-gamma territory - the textbook setup where dealer amplification leaks through the tech leg. With VIX in Contango and VVIX at Low, carry sellers retain the edge, but the divergence (True) means any QQQ break drags SPY off its anchor. Trade structure tilts toward iron condors on SPY/SPX, not naked vol selling on the Nasdaq.

Regime Assessment

The complex sits in a Elevated / Watchful regime - VIX printing 15.19 places us squarely in the middle of the elevated band, not the panic zone. Half-life clocks at 15 sessions, which is sticky enough to lean into the carry but not stable enough to size to the max. Vol sellers retain the edge; vol buyers are still paying retail.

Transition probabilities favor mean-reversion lower, not a spike higher. To-panic odds over the next five sessions sit at 0.05 - a thin tail - while drift back to the low-vol regime over ten sessions runs 0.45. Base case is grind, not gap. The 85.50 VVIX print and Contango term structure both corroborate the read.

The risk to monitor is the QQQ negative-gamma posture metastasizing into the broader index complex. Cross-asset divergence currently reads Spy Heavier - SPY/IWM anchor positive while QQQ trades below its flip. A QQQ break of 739.00 is the single cleanest invalidator for the carry thesis.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - lean into carry at standard size, but treat QQQ's negative-gamma leg as the canary, not the noise.

Trading readVIX, VVIX, MOVE, and SKEW all sit in their respective neutral-to-low bands - no divergences flashing, no regime-shift warning lights. This is the kind of confluence that lets vol sellers size into the trade without binary-risk haircut.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

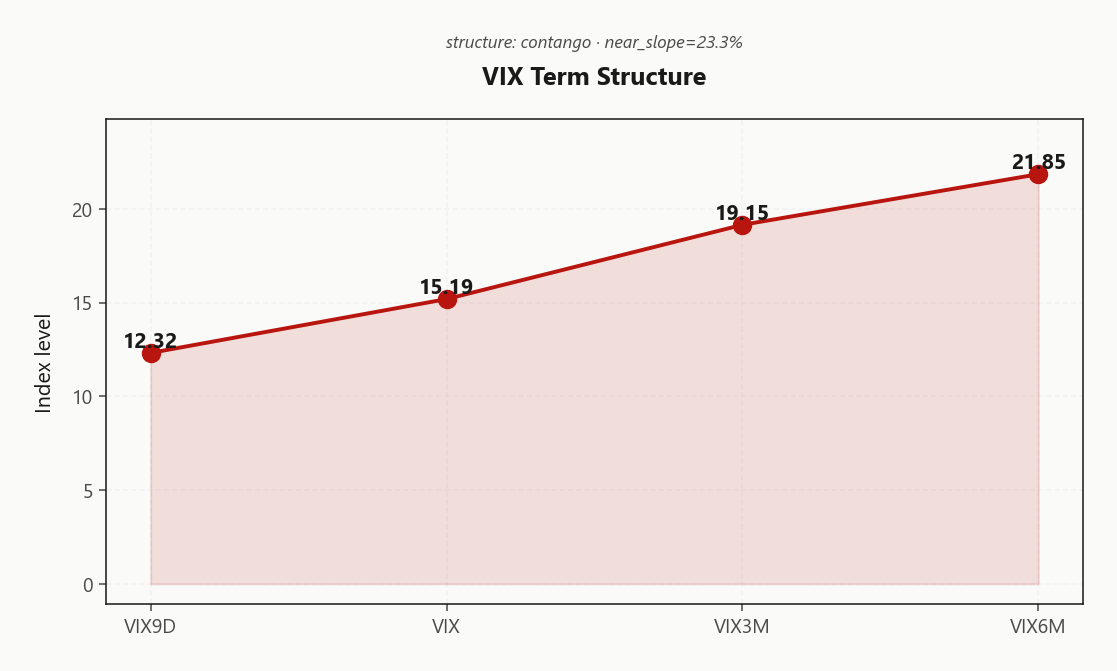

The curve is the trade. Steep contango - vol sellers favored from 12.32 at the front through 15.19 spot VIX and out to 21.85 at six months - this is structural carry, not event-priced stress. The near slope at 23.3% tells you dealers are paying up to roll vol forward, and the futures basis of 26.07% confirms the contango is being defended.

Forward 30-to-60 prints 20.8498369298 - that's where the steepest carry decay lives and where the cleanest calendar edge sits. Short the front, long the belly: the curve is paying you to roll out rather than stay in the front, and the absence of a kink between 19.15 and 21.85 means no specific event is being singled out for premium. With regime tagged Steep Contango, vol sellers retain the edge - but harvest it through 30-45 DTE calendars, not naked front-month shorts.

What it means for your trading

Steep contango from 12.32 through 21.85 with forward 30-60 at 20.8498369298 defines a structural carry regime. Trade it via belly calendars short the front, long the 30-45 DTE bucket - the curve pays you to roll, not to camp.

Trading readSteep contango from 12.32 to 21.85 with a 23.3% near-slope says the market expects stability now and pays up for protection later - the vol carry trade is structurally favored.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Implied is still paying. SPY ATM IV at 11.21% sits well above HV20 of 8.9, leaving a clean VRP cushion of 2.31% for sellers to harvest. The spread has compressed from recent extremes, but the direction of travel matters: HV60 at 14.23 running above HV20 says realized has decelerated, not accelerated - the tape is grinding, not breaking, and theta collection remains the dominant edge.

The trade selector is in the cross-section. QQQ VRP at 3.93% prints richer than SPY despite - or rather because of - its slip into Negative Gamma; the premium is paying you for tech fragility risk, not free carry. IWM tells the opposite story: VRP compressed to 1.09%, vol sellers paid almost nothing on small caps. Rank the pay structure by VRP gap: sell SPY and QQQ vol, leave IWM alone. The Vrp Active signal holds, but the asymmetry across the complex is what determines where the harvester actually deploys size.

What it means for your trading

VRP is alive on the index complex with SPY offering 2.31% of clean carry against decelerating realized, while QQQ's richer 3.93% reflects regime risk and IWM's compressed 1.09% disqualifies small-caps from the trade.

Skew Convexity

Front-expiry quarter-delta skew prints at 1.28% with a smile ratio of 1.11% - wing premium is structural, not flow-driven. Put quarter-delta IV at 12.74% sits only modestly above ATM 12.45%, while call quarter-delta marks 11.46% - below ATM, with zero upside conviction priced. This is ordered downside hedging, not a panic bid.

QQQ tells a different story: its quarter-delta skew runs 2.57%, materially steeper than the index - tech downside is paying up where the regime has already flipped to Negative Gamma. The smile slope is doing the work that spot hasn't yet, consistent with the broader Spy Heavier divergence read.

Trade structure follows the geometry. With convexity dear and the put wing carrying the premium, naked puts are the wrong vehicle - vertical put spreads on QQQ finance the hedge against the steeper wing, while SPY's ordered smile keeps iron condors clean against the 757.00 ceiling. Sell the skew you're paid for; don't buy the convexity you're already overpaying.

What it means for your trading

Quarter-delta skew is steep but ordered on SPY (smile ratio 1.11%) and materially steeper on QQQ at 2.57% - structural hedging, not panic, which makes put spreads the dominant hedge over outright puts.

Vol-of-Vol Structure

VVIX at 85.50 against VIX 15.19 puts the ratio squarely in the Low zone - an orderly vol regime with no binary outcome priced into the curve. The session decline of -4.79% in VVIX confirms jump-risk pricing is bleeding out, not building. This is the configuration where short-vol carry collects cleanly without the regime tax.

Sizing guidance reads Standard Size with signal color Green - full book, no haircut. The ratio breaking above the upper threshold is the line where you halve and lean defensive; staying below it keeps vol sellers paid. With VVIX/VIX at 5.63, the tape is telling you the wing bid is structural hedging, not panic positioning.

Operationally: this is the green light to anchor Iron Condor structures at standard size. The flag to watch is the ratio itself - a break higher would invalidate the carry thesis before any spot level does.

What it means for your trading

VVIX/VIX in the Low zone at 5.63 says size to Standard Size - vol-of-vol confirms the short-carry edge is clean, with ratio expansion as the single tripwire to monitor.

Dispersion Spread

Index vol is doing none of the work. SPY ATM IV at 11.21% sits well beneath QQQ at 18.71% and IWM at 20.73% - the basket is compressed while the components are repricing on their own clocks. That is dispersion, live and paying: correlations have fallen far enough that single-stock vol carries the load, and the index print understates the realized churn underneath.

Trade selection follows the geometry. SPY iron condors capture the compression cleanly - premium without the correlation tax - while QQQ short strangles run straight into the negative-gamma regime where dealer flow amplifies any single-name break. Megacap GEX swings (MSFT, AAPL, GOOGL) are the dispersion engine; the index sits on top, the names move underneath.

Harvesters take the index. Active hedgers isolate the single-name where premium justifies the carry.

What it means for your trading

Index vol compressed at 11.21% versus QQQ 18.71% confirms dispersion is alive - single-stock leaders run their own cycle while the basket pins. Favor SPY iron condors over QQQ short strangles; the regime-adjusted edge is unambiguous.

Liquidity & Microstructure

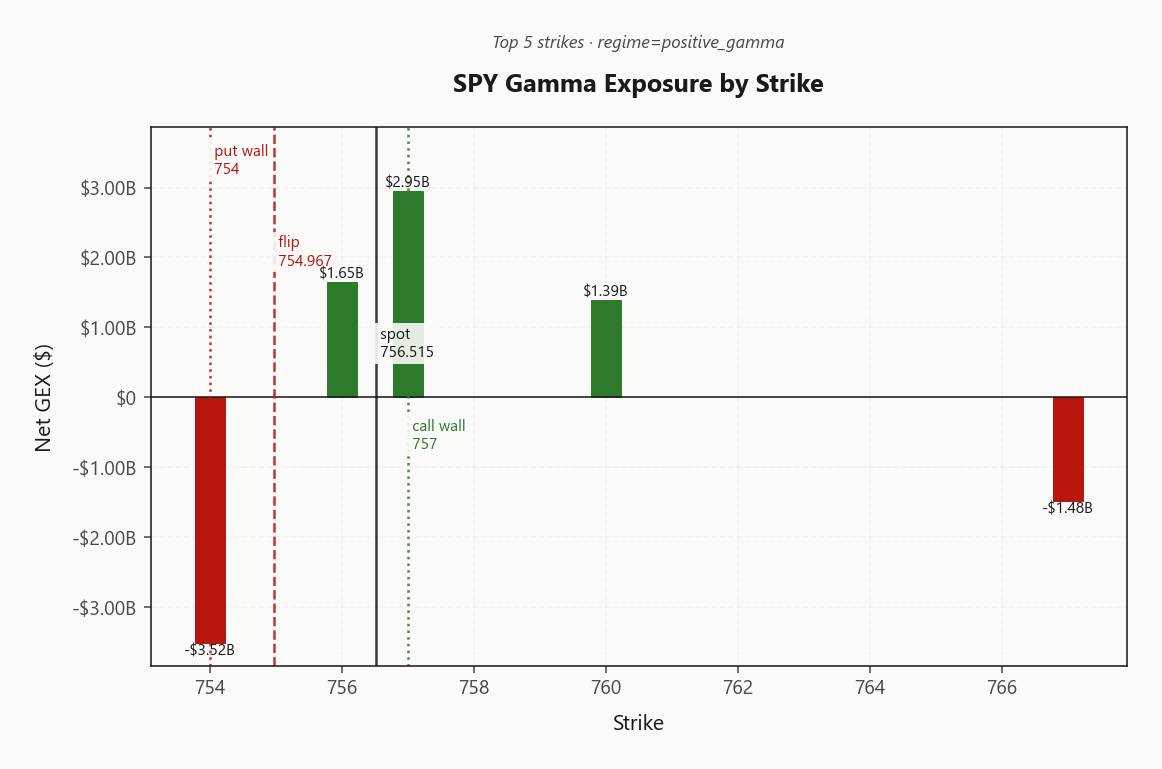

The book is barbelled: the heaviest OI sits parked at 565, deep OTM and long-dated - structural hedging that does not pull the tape. The short-dated gravity is concentrated at 754.00, where -$3.52B of net dealer gamma defines today's pin geometry.

Spot at 756.52 is pressed against the 757.00 call wall with the 754.97 flip sitting inches below - the cushion between dealer-buy-the-dip and dealer-sell-the-rip is razor thin. The 754.00 - 757.00 band is the entire playing field; every print inside it is mean-reversion fuel, and the flip is the trapdoor.

0DTE owns 59.5% of total gamma - intraday mechanics dominate, trend trades do not print, and the close is where charm pressure resolves. Fade strength into the wall, treat the flip as the hard stop.

What it means for your trading

Long-dated wings anchor while short-dated dealer gamma pins SPY in the 754.00 - 757.00 corridor - every level here is live, and a break of 754.97 flips dealer flow from suppressive to accelerant.

Trading readSPY's deep call-wall cluster at 757.00 sits inches above spot with a massive negative-gamma plate at 754.00 just below - dealer mechanics dampen on the way up but flip violently if the 754.97 breaks. Fade strength toward the wall; respect the flip as your hard stop.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

The second-order book is unambiguously hostile: SPY net VEX prints -$54.12B and CHEX -$3.48B, meaning every uptick in vol forces dealers to sell delta while charm bleeds them shorter into the bell. This is the classic pinned-but-fragile geometry - gamma supports the tape, but vanna and charm are wired to amplify any dislocation.

The line in the sand is the charm pivot at 757 (Call Wall), with bias Neutral and spot sitting just 0.0641097665 away. Below it, dealer selling compounds into a reflexive flush; above it, the squeeze risk lives as short-gamma hedgers chase. Tight distance plus negative VEX/CHEX is the textbook breakout-prone configuration.

Trade implication: vanna-aware desks avoid naked short calls here - cap upside risk with verticals, and treat the pivot as the regime switch, not a target.

What it means for your trading

Negative VEX of -$54.12B and negative CHEX of -$3.48B mean the next vol tick or charm decay forces dealers to compound the move, not dampen it. Watch 757 - that pivot is the regime switch.

Cross-Asset Confirmation

Cross-asset tape reads Spy Heavier - and that's the entire story. MOVE at 73.58 is flat, Fear & Greed sits at 55 (Neutral), credit isn't blinking, and the vol-of-vol complex is subdued. None of the macro tells are firing. Whatever is happening today is not a systemic event - it's tech.

The internal split confirms it. SPY and IWM both hold above their gamma flips in positive-gamma posture; QQQ has slipped under at 739.80 while IWM at 291.84 holds regime cleanly. Small caps are the canary that isn't singing - if this were credit or growth contagion, IWM breaks first. It hasn't. That isolates the fragility to the Nasdaq complex: an idiosyncratic re-rating of megacap tech, not a broad risk-off.

Hedge style follows the diagnosis. Short-tech put spreads, not broad index disaster hedges - paying for SPX wings when True screams sector, not system, is the wrong premium to buy.

What it means for your trading

With MOVE at 73.58 and Fear & Greed neutral at 55, the cross-asset complex confirms a Spy Heavier divergence isolated to tech - trade it as a QQQ-specific re-rating, not a macro shock.

Scenario EV

The scoring board hands the trade to Iron Condor on SPY, posting the top mark at 37 versus a put-spread alternative at 25. The edge is structural: SPY sits in Positive Gamma with VRP at 2.31%, so theta capture lands against a tape that dealer mechanics keep tethered to the 757.00 wall and the 754.97 flip.

Anchor in the belly, not the front. The 30-45 DTE bucket is where Contango from 12.32 up through 21.85 actually pays you to roll - the front offers carry without runway, the belly compounds it. Wear SPY because its gamma is positive; QQQ at Negative Gamma below 740.39 is the wrong vehicle for naked short vol.

Size Standard Size. VVIX at 85.50 against VIX at 15.19 keeps the ratio in the Low zone - no binary tax, no jump-risk haircut. Invalidation is clean: QQQ break of 739.00 or VVIX out of regime kills the carry.

What it means for your trading

Iron condor on SPY in the 30-45 belly is the highest-scoring expression at 37, anchored on positive gamma and a Low vol-of-vol regime that supports Standard Size sizing.

Actionable Summary

The complex splits clean down the middle: SPY anchors Positive Gamma with net GEX -$6.65B and spot pressed against the 757.00 call wall, while QQQ has slipped under its 740.39 flip into Negative Gamma. With VVIX/VIX in the Low zone and term structure in Contango, the carry edge is alive - but the divergence (Spy Heavier) makes tech the fragile leg that drags the index if it breaks.

Primary trade:Iron Condor on SPY in the 30-45 DTE belly, anchored where regime is cleanest. Watch level: SPY 757 - the line in the sand for dealer flow reversal. Avoid naked short QQQ vol; negative gamma amplifies any leg-down. Hedge with QQQ put spreads - skew at 2.57% makes outright protection too rich.

Exit conditions: VVIX through the jump-risk threshold or QQQ break of 739.00 - either invalidates the Elevated / Watchful carry thesis.

What it means for your trading

Fade strength to 757.00, respect 757 as the hard stop, and treat QQQ as the canary - a clean break of 739.00 means SPY's cushion gets tested fast.

Iranian oil exports at six-year low matters for headline crude supply - combined with active ceasefire negotiations, this is the primary input keeping energy vol contained and supportive of the broader risk-on tone.

Gold rally on Middle East ceasefire hopes plus pressure on yields confirms the regime read - peace-trade dynamics suppress vol broadly, reinforcing the carry-friendly environment.

Hezbollah rejection of ceasefire framework is the tail-risk reminder - the path to peace is non-linear, and any setback here can trigger the vol-of-vol regime change the tape is currently not pricing.

Gulf markets mixed on US-Iran deal hopes show the geopolitical premium is partially priced - incremental progress now produces diminishing returns while a breakdown would be asymmetric to the downside.

China cutting domestic gasoline and diesel prices signals weak end-demand in the world's second-largest economy - a structural drag on the global reflation trade and a quiet input into the IWM small-cap underperformance.

BOJ expected to raise rates this month is the single biggest macro catalyst on the wire - a confirmed hike re-prices yen carry, USDJPY, and feeds directly into MOVE and global vol-of-vol; this is the trade most likely to shift the regime.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Neutral, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.97 against a spot of 756.52. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.21% with a volatility risk premium of 2.31%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.19. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime