Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

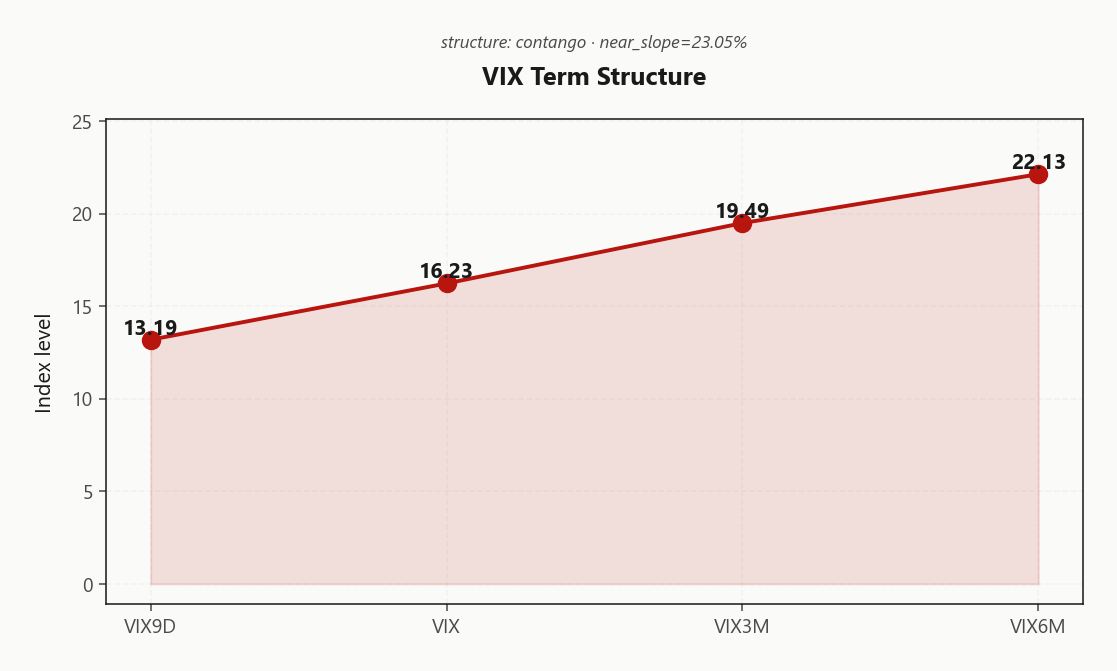

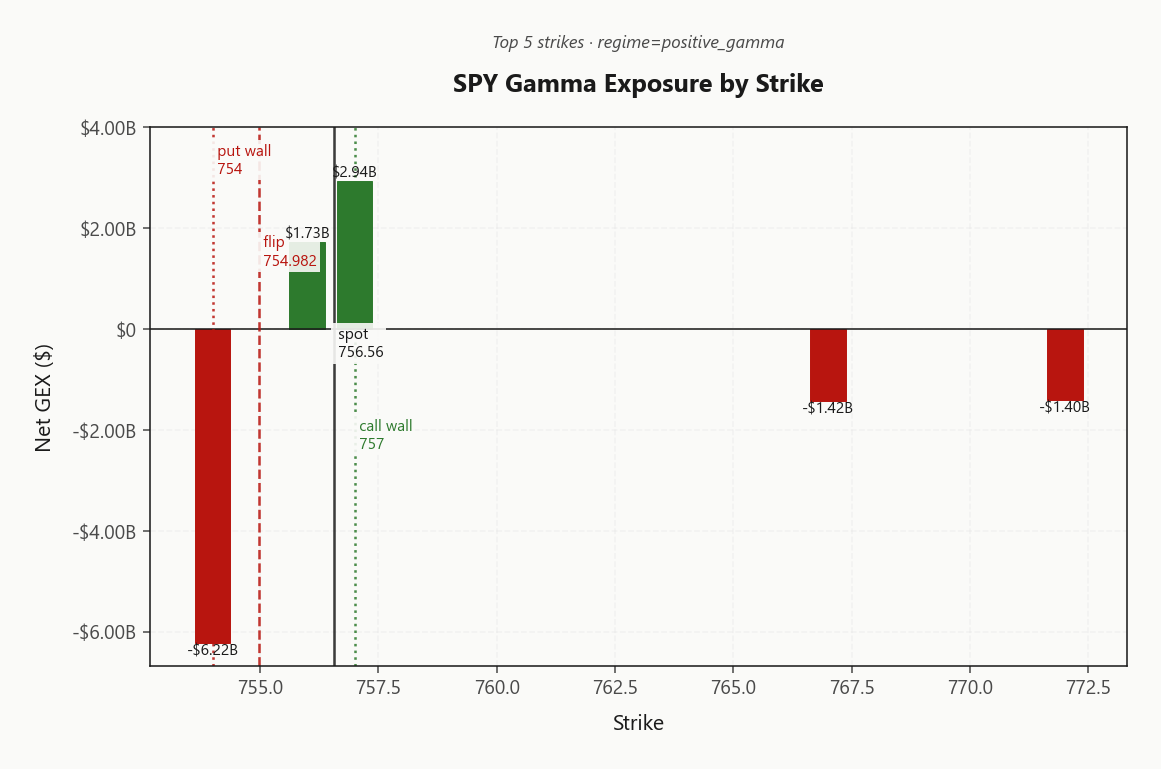

SPY at 756.56 holding above the gamma flip at 754.98 - dealers long gamma with net GEX -$10.61B, mean-reversion regime intact. Call wall stacks at 757.00 with the largest pos-gamma strike there ($2.94B), put wall at 754.00 loaded with put OI (228034 contracts) - spot pinned between the two. Dealer vanna negative (-$37.22B): a vol pop today translates to dealer delta-selling, so the cushion thins if VIX trades through 16.23+. VIX term in steep contango (13.19/16.23/19.49/22.13), near-slope 23.05%% - sellers' carry is the trade, VVIX at 90.53 is calm. ATM IV 12.07% vs HV20 9.57 = VRP of 2.5%, options moderately rich. Bottom line: iron condor 30-45 DTE around 754.00/757.00, half-size if VIX tags 19.49 on Iran headlines.

SPY trades above the 754.98 flip with dealers long gamma - mean-reversion regime intact across SPY/QQQ/IWM. VIX term in Steep Contango (13.19/16.23/19.49) pays vol sellers, but Middle East escalation overnight pushed VIX higher and tilts the bias toward defined-risk over naked premium. VVIX at 90.53 signals no jump-risk panic yet - iron condors in the 30-45 DTE bucket are the highest-EV structure.

Regime Assessment

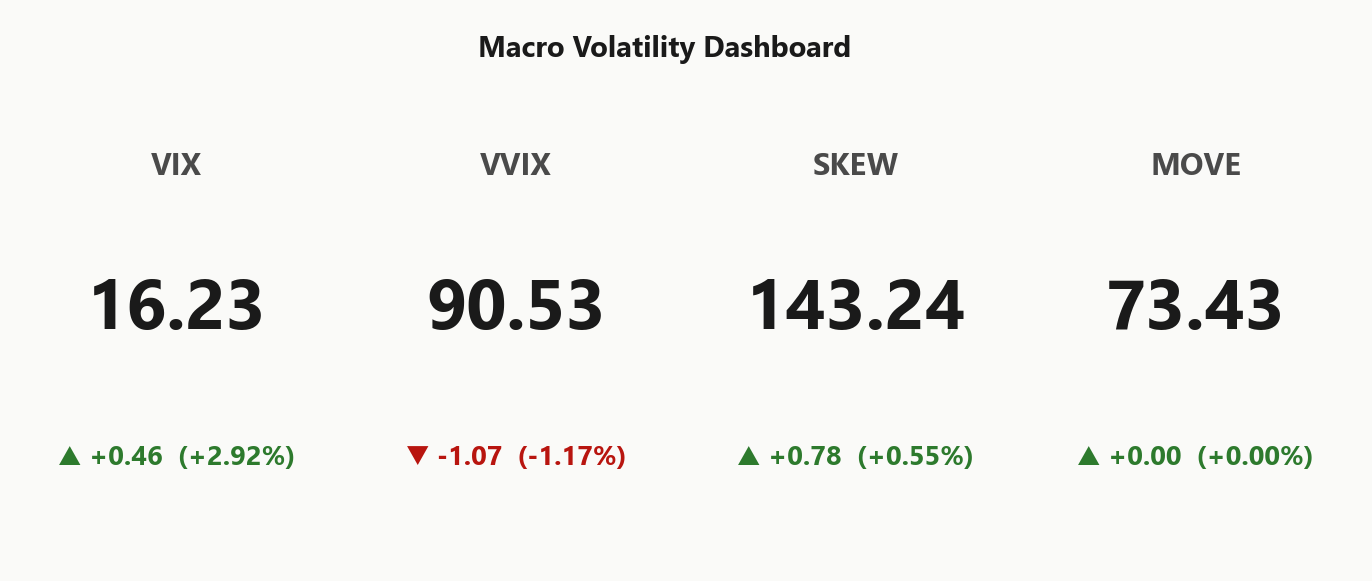

Tape sits in Elevated / Watchful territory with VIX anchored at 16.23 - premium-selling is viable but the regime demands tail-aware sizing. Transition odds skew toward mean-reversion: probability of slipping to a panic state within five sessions sits at 0.05, while the path lower to a low-vol regime over ten sessions runs 0.45. Iran headlines keep that panic tail non-zero, but the base case is decay, not escalation.

Half-life of the current state is 15 sessions - moderately sticky, not glued. Expect the regime to morph within two-to-three weeks; carry trades have runway but no permanence. Combined with aligned positive-gamma across SPY/QQQ/IWM and contango paying the front, the playbook is Iron Condor in the 30-45 DTE bucket - defined risk preferred over naked premium while the geopolitical bid under vol persists.

What it means for your trading

Elevated / watchful regime with mean-reversion probabilities dominating the transition matrix - sell premium with defined risk and harvest before the 15-session half-life expires.

Trading readVIX up modestly, VVIX actually down, MOVE flat, SKEW slightly elevated - no confirmation of stress across the dashboard. That's the textbook 'geopolitical noise, not regime shift' signature; trust the mean-reversion trade until at least two of these flip risk-off in lockstep.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve sits in Contango from 13.19 at the front through 16.23 spot, 19.49 at three months, and 22.13 at six - a Steep Contango shape that pays sellers to hold through the belly. Near-slope at 23.05% confirms the front is meaningfully suppressed versus the 3M anchor; despite the overnight Iran tape, VIX9D refuses to bid through spot VIX, so front-end stress is conspicuously absent.

The VIX-to-VIX3M gap is doing the structural work - it prices a real risk premium 1 - 3 months out without dragging the front along, which is exactly the shape that rewards defined-tenor short-vol carry. Forward 30→60 implied lands near 20.9304491113, the sweet-spot tenor where IV dominates expected realized and roll-down compounds the carry.

The kink to watch is the 9D-to-VIX hinge: a cross of 13.19 above 16.23 is the backwardation trigger and the cleanest regime-break signal on the board. Until then, the curve says stay short the belly, stay defined on the wings.

What it means for your trading

Steep contango with a suppressed front pays carry in the 30 - 45 DTE bucket and tags forward 30→60 near 20.9304491113 as the highest-EV tenor. Flip the trade only if VIX9D crosses 16.23 - that's the backwardation signal.

Trading readSteep contango from front to back = vol carry trade is live, and the market is not pricing imminent stress. The slope tells you sellers get paid for holding, but watch the 9D-to-spot kink - if VIX9D crosses above VIX, that's the early-warning backwardation flip.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM implied at 12.07% against HV20 9.57 leaves VRP at 2.5% - positive, but compressed. Options are moderately rich to recent realized, not a fat-pitch short-vol setup. With HV60 at 14.17 printing above the 20-day window, the tape is decelerating into the calmer regime rather than catching up to a hot one - supportive of premium sellers, but the cushion is thin enough that defined-risk wins over naked structures.

The cleanest edge sits in the 8-16 DTE bucket where IV-over-RV is least diluted by event premium and roll noise. Further out the term, contango carry does the heavy lifting; closer in, gamma risk dominates and the realized/implied gap narrows. Sellers should harvest where the spread is widest and the dealer-gamma cushion is still actively suppressing intraday range.

The watch: a VRP drift toward zero - driven either by realized re-accelerating on an Iran headline or implied bleeding lower into a quiet tape - kills the carry outright. HV20 turning higher is the first tell; VRP collapse is the exit.

What it means for your trading

VRP at 2.5% with HV20 9.57 below HV60 14.17 = premium-selling has edge, concentrated in the near-dated 8-16 DTE window. Exit the carry trade if VRP compresses toward zero.

Skew Convexity

Quarter-delta skew prints 3.75% with the smile ratio at 1.28% - left tail dominant, but a long way from crisis-steep. Put wing at 17.24% sits cleanly above ATM 14.62% while the call wing fades to 13.49% - an ordered downside bid with zero upside chase.

The asymmetry is the trade: put protection is paying up modestly, call premium is structurally cheap. Use call spreads, not naked calls, for upside expression - the flat right wing means outright calls give back too much extrinsic if spot drifts. Conversely, short put spreads remain the cleaner short-skew vehicle than naked short puts given the Iran tail still has a bid.

Trigger: if skew steepens further on escalation headlines and smile ratio extends, retire short put spreads in favor of fully defined-risk structures only. The current ordering is constructive; a parallel shift in the put wing is the regime-break tell.

What it means for your trading

Skew is firm but orderly - put wing bid at 17.24% vs flat call wing at 13.49% rewards defined-risk condors and call spreads over naked wings. Steepening past current smile ratio 1.28% is the signal to shift fully defined-risk.

Vol-of-Vol Structure

VVIX at 90.53 against VIX 16.23 prints a ratio of 5.58 - squarely in the Normal band. Options on vol are cheap, the surface is not pricing a bimodal jump, and the tape is shrugging off Middle East headlines rather than re-rating them. VVIX actually ticked -1.17% on the session - the second derivative is desensitizing, not flaring.

Translation for the book: Standard Size on premium-selling structures. The vol-of-vol gauge is the green light the iron condor thesis needs - no convexity tax embedded in short-vol carry here. The market is treating Iran as noise, and the VVIX print confirms it; if dealers expected a tail, options on VIX would not be this cheap.

That said, cheap insurance is still insurance. Long VIX calls at this VVIX print are reasonably priced - not free, but a fair hedge against the regime-break scenario where VIX9D crosses VIX. Carry the trade, but own the tail.

What it means for your trading

VVIX at 90.53 and ratio 5.58 green-light Standard Size on short-vol structures, with cheap VIX calls available as a reasonable tail hedge.

Dispersion Spread

Index-to-single-name vol spread is the cleanest setup on the board: SPY ATM IV prints 12.07% against QQQ at 19.81% and IWM at 21.11% - the single-name complex is carrying meaningfully fatter implieds than the index aggregate. With cross-asset regime Aligned and correlation suppressed, idiosyncratic risk is doing the work while index vol gets dampened by the cancellation. That's the textbook dispersion signature.

VRP confirms the geometry. SPY VRP at 2.5% is the cleanest premium - modest but uncluttered. QQQ VRP at 4.12% looks richer on the screen but the cushion is being paid for by name-level dispersion, not index repricing. IWM at 1.59% is the thinnest of the three - small-cap premium isn't compensating for the gamma risk.

Trade structure: short index vol, long single-name straddles - the dispersion spread pays directly. Sell SPY/SPX premium for size, leave IWM alone, and avoid shorting single-name vol where the carry looks rich but the realized is doing the lifting.

What it means for your trading

Single-name implieds at 19.81%/21.11% running well above SPY's 12.07% with QQQ VRP 4.12% richer than SPY's 2.5% - classic dispersion: short index vol, long single-name straddles, skip IWM where VRP 1.59% is too thin to justify the risk.

Liquidity & Microstructure

Spot 756.56 sits wedged between the put wall at 754.00 and the call wall at 757.00 - a tight book, dealers in the driver's seat. The gamma flip at 754.98 is the level: spot is a hair above, and a close below flips dealer hedging from suppressive to destabilizing.

The highest OI strike at 565 is parked in LEAP territory - irrelevant to today's tape. Live action sits at 754.00, which carries the deepest negative-gamma slug at -$6.22B - the magnet if SPY breaks the flip lower.

P/C OI at 2.389 reads as hedged-long: puts as insurance, not directional shorts. Liquidity is deep, walls are firm, but the cushion between spot and the flip is thin - respect 754.98 on close.

What it means for your trading

Spot pinned between 754.00 and 757.00 with the gamma flip 754.98 as the regime switch - hedged-long P/C OI at 2.389 backs the mean-reversion read until the flip breaks.

Trading readDealers are net long gamma above the flip with the biggest positive-gamma slug at the call wall - that's the magnet pulling rallies back. The 754.00 strike carries the deepest negative-gamma cluster, so any break below it accelerates downside as dealers flip from suppressing to amplifying moves.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX at -$37.22B sits deeply negative - a vol uptick mechanically forces dealer delta selling, the textbook accelerant if Iran headlines push VIX through 16.23. The cushion looks generous in positive-gamma terms, but vanna is the trap door: it doesn't open until vol moves, and then it opens fast.

Charm compounds the problem. Net CHEX at -$2.01B means time decay is pressing dealers to sell into the close rather than support - the regime is mean-reverting on price but quietly bleeding on the clock. Spot sits a hair under the Call Wall pivot at 757, only 0.0581579782 away, with current bias Neutral.

That distance is the tell: balance, not conviction. Cross through the pivot and dealer flow flips - short-vol structures need to respect the asymmetry, half-size into any VIX gap and keep the tail hedge on while VEX stays this negative.

What it means for your trading

Positive-gamma price stability masks a hostile vanna/charm setup - net VEX -$37.22B and net CHEX -$2.01B both lean against dealers, so any vol pop or close-bleed accelerates downside. Fragile equilibrium at the Call Wall pivot 757 - trade the carry, but keep the structure defined.

Cross-Asset Confirmation

Bond vol refuses to confirm the equity-stress tape: MOVE prints 73.43 and sits flat on the session, telling you rates desks are pricing geopolitical headlines as noise, not a credit event. When Iran escalates and MOVE doesn't budge, the cross-asset tell is unambiguous - there is no systemic transmission channel opening up, and the equity vol bid is a reflex, not a regime shift.

The index complex confirms the read. QQQ at 744.25 and IWM at 287.97 both hold above their flips alongside SPY, with cross-asset regime Aligned - no leadership crack, no small-cap canary singing. Fear & Greed reads 56 (Greed); enough cushion to sell premium, not frothy enough to fade.

Trade the noise, not the narrative: mean-reversion intact until MOVE expands and IWM breaks first. Watch small caps - that's where the credit-transmission story would print before SPY ever cracks.

What it means for your trading

Bonds, megacap, and small-cap all aligned with positive-gamma equity regime - Iran is a vol-of-vol blip, not a compounding credit shock, so stay short premium with defined risk and let IWM lead any genuine regime break.

Scenario EV

Highest-EV structure prints Iron Condor at score 33, optimal window 30-45 DTE - short strikes parked around 754.00 / 757.00. Carry math is clean: VIX term in Steep Contango from 13.19 through 22.13 pays sellers, positive-gamma regime (Positive Gamma) holds spot pinned between the walls, and VVIX at 90.53 reads Normal - no bimodal jump pricing in the vol surface.

Put spread sits second on the board at score 22 - the runner-up, not the trade. Reason the condor wins: skew is firm but not crisis-steep, call wing flat at 13.49%, and defined-risk wings beat naked strangles while Iran headlines remain a live tail. Sizing guidance is Standard Size - green light from VVIX, half it only if VVIX clears triple digits.

Pivot work runs through 757 (Call Wall), current bias Neutral. Backwardation flip - VIX9D crossing VIX - is the kill switch; flatten on that print.

What it means for your trading

Iron condor 30-45 DTE around 754.00/757.00 at Standard Size is the recommended structure (score 33 vs put spread 22); defined risk wins over naked premium while the Iran tail stays live.

Actionable Summary

Trade: Iron condor in the 30-45 DTE bucket, short strikes pinned at 754.00 / 757.00, standard size. Spot sits a hair under the call-wall pivot at 757 in an Elevated / Watchful regime - contango pays carry, positive gamma anchors the range, VVIX at 90.53 greenlights normal sizing.

Watch: the gamma flip at 754.98 is the line - a close below flips dealers into negative gamma and accelerant flow; cut shorts on the break. Avoid naked strangles into a live Iran tail, naked upside chase (call wing flat - use spreads), and single-name index hedges with dispersion this wide.

Hedge cheap with VIX calls or a put-spread tail while VVIX is asleep at 90.53. Trigger to flatten: VIX9D crossing above VIX (13.19 vs 16.23) - that backwardation flip is the regime break, exit short vol immediately.

What it means for your trading

Run the Iron Condor around the 757 pivot while spot holds above the 754.98 flip; flatten the moment VIX9D inverts through VIX or spot closes below the flip.

Iran hitting Kuwait and US strikes near Hormuz is the live oil/risk-off catalyst - explains overnight VIX uptick and is the headline volatility traders must track.

White House proposing fresh EU tariffs is the second escalation axis on top of Middle East - compounding macro tail that argues against naked short vol.

Stocks dipping on Iran escalation with oil bid is the textbook geopolitical correlation - confirms the regime is reactive, not structural, supporting mean-reversion bias.

Talks-at-stalemate framing means no near-term de-escalation pricing - keeps a floor under VIX and an asymmetric tail on the short-vol trade.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.98 against a spot of 756.56. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.07% with a volatility risk premium of 2.5%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.23. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime