Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY trades 754.33 with net GEX at -$13.06B - dealers are in Negative Gamma and the tape is unstable. The gamma flip sits at 754.98, call wall 757.00, put wall 754.00; spot is pinned within fractions of the flip, which is why every push is being faded both ways. Vanna at -$27.5B and charm at -$2B both lean negative, meaning a vol uptick or time decay sells dealer delta into the close. VIX prints 16.26 with VVIX 91.01 and the curve is Contango at 16.89%% near-slope - vol sellers paid, but VRP at 2.28% is modest in SPY. QQQ 742.38 and IWM 287.25 stay above their flips in Positive Gamma, so the divergence is the lead story - index complex isn't yet confirming SPY's fragility. Bottom line: trade the flip - above 754.98 fade to 757.00, below it expect amplification toward 754.00 then deeper put-OI clusters. Structure of choice: Iron Condor in the 30-45 bucket, sized Standard Size.

SPY is sitting right on the gamma flip at 754.98 with dealers in Negative Gamma, while QQQ and IWM hold positive-gamma cushions - a textbook intra-complex divergence (Qqq Heavier). VIX term structure prints Steep Contango with VVIX ratio Normal, so vol sellers retain the carry but the SPY flip is the swing factor. Bias is Neutral; reclaiming the flip restores the dampener, losing it hands the tape to trend.

Regime Assessment

Regime prints Elevated / Watchful with VIX anchored at 16.26 - elevated enough to demand respect, nowhere near the panic band. The transition matrix tells the story: probability of escalating to panic over the next five sessions is 0.05, while the path back to a low-vol state over ten sessions sits at 0.45. Tail risk is asymmetric to the downside in vol space, but not imminent.

Half-life of 15 sessions makes this regime moderately sticky - don't trade it as a one-day mean-revert. Position for persistence: the carry edge in Steep Contango survives, VVIX in Normal territory authorizes Standard Size, and the scenario engine's Iron Condor in the 30-45 bucket is built for exactly this shelf-life.

Kill switch: a VIX print breaching the next band or backwardation in the front-slope flips the matrix. Until then, plan for the regime to hold and harvest accordingly.

What it means for your trading

Regime is Elevated / Watchful with VIX at 16.26, half-life 15 sessions - sticky enough to trade the carry, not so stressed that sizing must be cut.

Trading readVIX up modestly, VVIX barely moved, MOVE flat, SKEW elevated - credit/rates calm, equity-only stress signature. Confirms the geopolitical-headline read over a structural shift.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

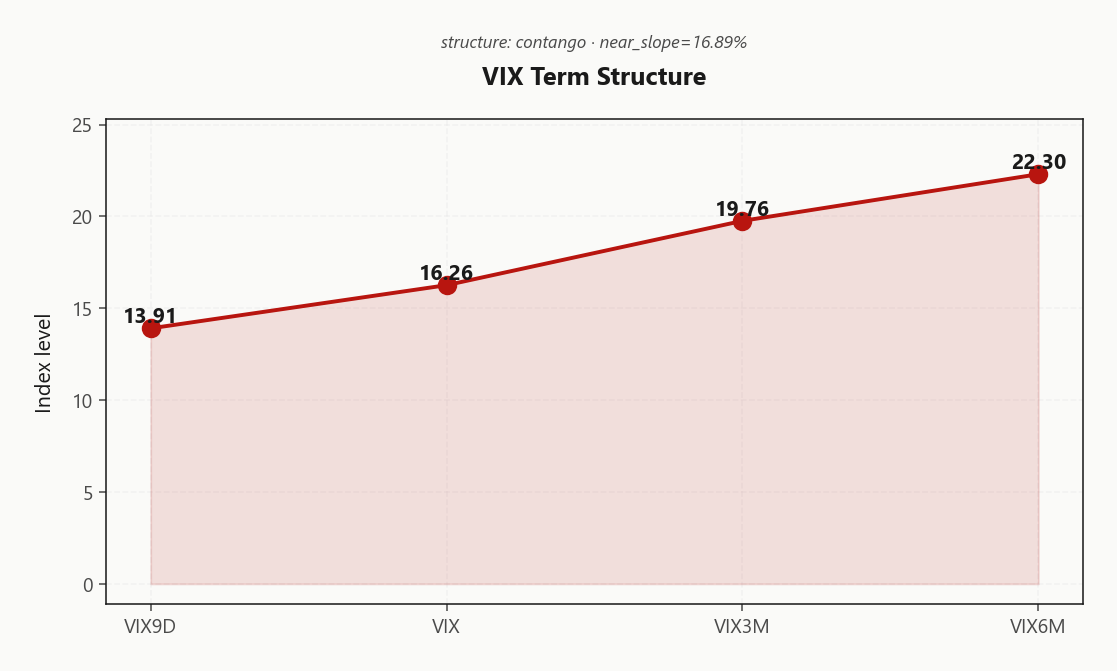

The curve is in Steep Contango - VIX9D at 13.91 sits well beneath VIX 16.26, with the near-slope printing 16.89%%. Front-end is suppressed, no event premium bid into the weekly. This is structural carry: spot vol is being paid relative to forwards, and the curve shape itself is the trade.

The back end keeps climbing - VIX3M 19.76, VIX6M 22.30 - so term carry is intact and the dated wing is where vol is being absorbed. Forward 30-to-60 prints 21.295365693 and forward 60-to-90 prints 24.5789015214, marking the dated bucket as the richest segment of the surface versus anything resembling near-term realized.

Steep contango - vol sellers favored: sell the front, hedge with dated wings. The cleanest pocket of edge is the 30-45 DTE bucket where forward vol is most divorced from spot tape - short the suppressed near-dated, finance dated-put protection against any backwardation flip.

What it means for your trading

Curve in Steep Contango with VIX9D under VIX and the back end rising - vol sellers retain carry, with the 30-45 DTE bucket the optimal harvest zone. Backwardation flip is the kill switch.

Trading readCurve in Contango with strong near-slope - vol carry trade is paid, market not pricing any near-term shock. Backwardation watch is the kill switch for short-vol books.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV prints 12.16% against HV20 at 9.88, leaving a 2.28% vol-point cushion for premium sellers - paid, but not a fat pitch. HV60 at 14.24 sits well above HV20, confirming realized is decelerating off the longer window; the tailwind for short-vol carry is intact, but the index itself isn't where the carry lives.

The richness sits one ticker over. QQQ ATM IV at 20.09% drives a VRP of 4.24% - materially wider than SPY and the cleanest IV-RV spread in the complex, more than enough to absorb the firmer tech skew. IWM, by contrast, is a non-starter: VRP at 1.17% is barely positive and will not compensate small-cap dispersion.

Trade construction follows the spread: rotate vol selling into QQQ, use SPY only as a directional or hedging vehicle around the flip, and skip IWM as a premium-harvest leg entirely. The carry is real - it just isn't in the ticker everyone is watching.

What it means for your trading

SPY VRP at 2.28% is paid but thin while QQQ runs a 4.24% cushion against ATM IV of 20.09% - the short-vol edge has rotated to QQQ, and IWM at 1.17% is uninvestable as a premium vehicle.

Skew Convexity

The 2.64% quarter-delta skew with a smile ratio of 1.21% tells a clean story: the left tail is bid in an ordered way, not a panic bid. Put quarter-delta IV at 15.4% trades over ATM at 14.09%, while call quarter-delta IV at 12.76% sits below ATM - a textbook distribution-tape signature with zero upside convexity demand.

Across the complex, QQQ skew prints 4.47% - tech wings are firmer than SPY's, consistent with single-stock dispersion concentrated in mega-cap names. IWM at 2.88% is the calmest read of the three; small-caps simply aren't paying for protection here. Wing demand is mega-cap-led, not broad.

Trade implication: put spreads beat outright puts - financing the long leg against the modestly bid wing is cheaper than chasing naked downside. On the upside, with call quarter-delta below ATM, sell the call wings - there is no premium to pay for a melt-up that the market isn't pricing.

What it means for your trading

Skew is ordered-steep, not panic-bid, with call convexity dead - structure protection as put spreads financed by short call wings, and prefer QQQ wings over SPY where skew is firmer.

Vol-of-Vol Structure

VVIX at 91.01 against VIX 16.26 prints a ratio of 5.60 - squarely in the Normal band. The vol-of-vol surface isn't pricing a bimodal tape; jump premium is absent, and the convex bid that usually accompanies regime-change anxiety simply isn't there.

That matters for execution. With VVIX in Normal territory, the structure book gets Standard Size - full risk allocations are appropriate, no need to half-size the way a print north of triple digits would demand. The carry trade in Steep Contango is clean, the iron condor scoring holds, and short-vol vehicles aren't fighting a convexity tax.

Tail watch is mechanical: any push of VVIX through the triple-digit threshold flips the structure recommendation and forces a sizing cut. Until then, treat the Normal regime as the green light it is - premium harvest, standard book.

What it means for your trading

VVIX at 91.01 and the ratio at 5.60 place vol-of-vol in Normal territory - no jump premium, full-size carry trades cleared, with the kill switch a VVIX break above triple digits.

Dispersion Spread

Index vol is mispriced against its components. SPY ATM IV prints 12.16% while QQQ runs 20.09% and IWM 20.95% - the index is trading at a deep discount to the basket it represents. That gap is the dispersion signature: correlation is being marked down even as single-name vol stays bid.

The wings tell the same story. Cross-strike dispersion is alive - OTM strikes carry premium against ATM across the complex, but the index ATM is the cheapest leg in the room. Buying SPY puts as a hedge against single-name risk is cheap insurance, but it does not compensate anyone short single-name vol; the correlation assumption embedded in index IV is too generous to underwrite naked straddle sales in QQQ or IWM constituents.

Preferred expression in this regime: short index vol against long single-name wings. Sell SPY/SPX premium where the carry is depressed, finance single-name wing protection where idiosyncratic risk remains bid. Avoid the inverse - short single-name straddles into long index hedges is the trade that breaks when correlation cracks.

What it means for your trading

SPY IV at 12.16% versus QQQ 20.09% and IWM 20.95% flags a classic dispersion setup: index hedges are cheap, single-name vol is rich, and the trade is short index vol financed against long single-name wings.

Liquidity & Microstructure

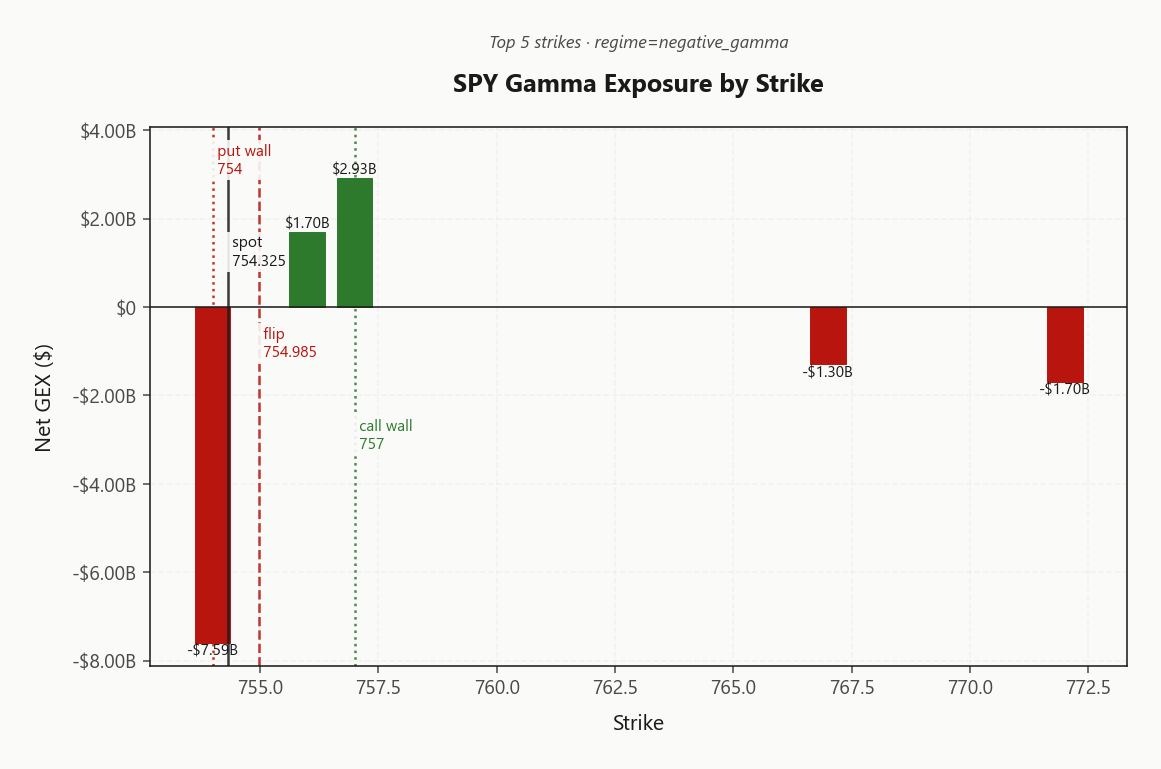

The book is concentrated and the geometry is binary: spot 754.33 sits directly on the gamma flip at 754.98, with the 754.00 strike alone carrying -$7.59B of negative gamma. That single line IS the level dealers are forced to defend - above it their hedging buys weakness and sells strength, below it the relationship inverts and every push compounds.

The structural OI cluster sits well below at 565 - pure macro hedge real estate, not today's trade. The live battle is between the put wall at 754.00 and the call wall at 757.00, a razor-thin corridor pinned at spot. The top strike's 228034 in put OI dwarfs the call side - defensive positioning already in place, not chasing.

Trade the flip, not the trend. Reclaim 754.98 and dealers re-supply stability into the close; lose it and the tape gets handed to amplification toward the put wall.

What it means for your trading

Spot 754.33 on the gamma flip 754.98 with the 754.00 strike carrying the entire negative-gamma load - the level decides whether the afternoon stabilizes or trends.

Trading readThe strike right at spot is the entire game today - dealers carry massive negative gamma there, which means every dollar move gets amplified above the flip and absorbed below. Trade the level, not the trend.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$27.5B and net CHEX -$2B - both deeply negative, a compounding hedging setup. Vanna is an accelerant: any uptick in vol forces dealers to sell delta into weakness, while charm drains long delta out of the book mechanically as the clock runs to 4pm. Two forces, one direction.

The swing factor is the Put Wall at 754, with spot a hair away at -0.0430848772. Current bias reads Neutral - a knife-edge. Reclaim the level and the negative-gamma hedging dampener re-engages on the upside; lose it and charm-driven supply meets vanna-driven supply in the same tape, classic afternoon sell-program geometry.

Trade the pivot, not the narrative: above 754, fade pushes toward 757.00; below, expect amplification down to 754.00. No middle ground while VEX and CHEX both lean this hard negative.

What it means for your trading

Vanna and charm are aligned negative - vol up and time forward both sell dealer delta, so the Put Wall at 754 is the single switch between stability and an afternoon sell program. Bias Neutral means the next dollar decides.

Cross-Asset Confirmation

Cross-asset tape refuses to confirm the SPY fragility story. MOVE prints 73.43 - credit and rates are calm, nowhere near the levels that would mark a genuine macro shock. Fear & Greed sits Neutral at 54, neither washed-out nor euphoric, so sentiment offers no contrarian fuel in either direction.

Inside the index complex, QQQ at 742.38 and IWM at 287.25 both hold above their gamma flips in positive-gamma regime - SPY is the lone outlier sitting on the knife-edge. Divergence direction reads Qqq Heavier, the textbook signature of localized positioning rather than systemic stress.

Read it as idiosyncratic SPY unwind, geopolitical-headline driven and mean-revertable - not a regime change. The first confirmation of escalation would be QQQ losing its flip; until then, treat SPY weakness as positioning to fade, not a trend to chase.

What it means for your trading

Cross-asset signals stay Qqq Heavier with MOVE at 73.43 and F&G Neutral - SPY's flip risk is localized, not systemic. Watch QQQ's flip as the trigger that converts positioning unwind into regime change.

Scenario EV

The scoring engine prefers Iron Condor at 42, with the 30-45 DTE bucket as the sweet spot. The structure wins on three coincident inputs: a Steep Contango term structure paying carry, VVIX in the Normal band with no jump premium, and a positive VRP backdrop - pure premium harvest, not a directional bet.

Put spreads score only 31 against the condor's 42, and the gap is structural: call skew at 12.76% trades below ATM 14.09% while the put smile ratio is only 1.21%. Directional skew simply does not pay. Express the trade in QQQ rather than SPY - QQQ VRP at 4.24% dwarfs SPY's 2.28%, and QQQ sits in Positive Gamma above its flip while SPY trades the knife-edge.

Sizing follows the vol-of-vol read: Standard Size. VVIX/VIX at 5.60 permits full allocation; no need to half-size as a triple-digit VVIX would demand. Stay out of the front week - the carry is too thin to compensate gamma risk.

What it means for your trading

Sell the Iron Condor in QQQ at 30-45 DTE, sized Standard Size - contango plus normal vol-of-vol plus positive VRP is the textbook premium-harvest setup, and QQQ's richer VRP makes it the cleaner vehicle than SPY.

Trade of the day: Iron Condor in QQQ at the 30-45 DTE bucket, where VRP at 4.24% dwarfs SPY's 2.28% and the structure scores 42 against put-spread 31. Watch level is SPY 754 - reclaim restores the dampener, lose it and charm sells dealer delta into the close with net CHEX at -$2B.

Avoid naked SPY puts with smile ratio only 1.21%, and skip front-week vol selling - VRP cushion too thin. Hedge with long dated SPY put wings financed by short call wings; call 12.76% trades under ATM 14.09%, so upside convexity is free to sell.

What it means for your trading

Regime is Elevated / Watchful at VIX 16.26 - play the carry in QQQ via Iron Condor, defend the SPY 754 pivot, and let the rest of the complex confirm before treating SPY's flip break as regime change rather than positioning.

Hezbollah-Israel rocket exchange directly tests the U.S.-mediated ceasefire and is the immediate driver of today's VIX tick-up and oil bid - geopolitical premium re-entering the curve but not yet bleeding into the front end.

A Trump claim that Iran agreed to no-nuclear is a binary headline catalyst - confirmation would crush oil and energy-premium in vol; reversal extends the geopolitical bid into the term structure.

EU energy-job warning ties the Iran conflict to growth-impact, which is the channel through which a geopolitical shock becomes a credit/macro shock - watch MOVE for confirmation.

Tungsten supply-shock framing extends the war-driven commodities theme beyond oil - industrials and defense single-names should see sustained vol bids regardless of the Iran headline.

US strikes near Hormuz raise the tail probability of a closure event - this is the single headline that could flip VIX curve into backwardation overnight, materially changing the iron condor scoring.

Fresh White House EU tariff proposals reintroduce the trade-policy overhang on top of geopolitics - when two macro stressors stack, single-asset hedges underperform; cross-asset hedging gets paid.

Generic stocks-down-oil-up tape risk-off note confirms the regime read - risk premia rising but not yet at panic; supports the elevated-but-not-stressed regime assessment.

Housing market sellers withdrawing at fastest pace since 2020 is the slow-burn domestic demand story - feeds into the Fed-easing path narrative that underpins SPY's long-term gamma support but isn't a same-day trade.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Neutral, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.98 against a spot of 754.33. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.16% with a volatility risk premium of 2.28%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.26. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime