Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY trades at 757.36 sitting essentially on its 757.50 gamma flip, net GEX of -$12.24B confirming a Negative Gamma regime where dealers amplify moves rather than dampen them. Key levels: call wall at 757.50 caps upside, put wall at 754.00 is the failure point - a break of either side hands dealers a forced-hedge feedback loop. QQQ tells the opposite story at 741.19 with net GEX of -$1.24B and spot above its 737.53 flip, so tech is the stabilizer while SPY is fragile. Dealer vanna (-$53.84B) and charm (-$1.73B) are both negatively skewed - any vol expansion sells delta, time decay pressures into close. VIX at 16.18 with 9d/3m/6m at 13.76/19.43/22.13 is Steep Contango - vol sellers carry but VVIX jumped to 91.60, flagging vol-of-vol risk that argues against full-size short premium. VRP read: Thin Premium, recommended structure is Iron Condor in the 30-45 DTE window. Bottom line: trade the SPY 754.00 - 757.50 range mean-reverting while above flip, but reduce size and skew puts on any break below 754.00 given dealers will sell into weakness.

SPY pinned at gamma flip with QQQ holding positive gamma - divergent dealer regimes amid Steep Contango

SPY trades within a hair of its 757.50 flip, leaving dealers short gamma and any directional break self-amplifying, while QQQ sits comfortably above its own flip in dealer-stabilized territory. VIX term structure remains in Steep Contango and VRP is Thin Premium, but VVIX firmed sharply - premium sellers are paid, yet vol-of-vol is whispering that the consensus carry trade is getting crowded.

Regime Assessment

Regime read: Elevated / Watchful with VIX anchored at 16.18 - elevated enough to pay sellers, nowhere near panic. The transition matrix backs the carry: probability of escalating to panic over the next five sessions sits at 0.05, while the move-to-low probability over ten sessions is 0.45. The base case is stay put, not break out.

Half-life of 15 sessions confirms the regime is sticky - sized positions can ride the cycle rather than chase reprice. The yellow signal is the discipline: short-vol exposure works, but full size does not. Half-size short premium, defined-risk structures, and respect the 757.4978931935 pivot. Carry trades still work here; reaching for them does not.

What it means for your trading

Regime is Elevated / Watchful at VIX 16.18 with a 15-session half-life and panic-transition probability of 0.05 - carry trades work at half size, not full size.

Trading readVIX calm, VVIX firming, SKEW elevated, MOVE flat - vol of vol diverging upward while the rest hold steady. That's the watch-list signal: vol-of-vol typically leads vol turns by sessions, not days.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

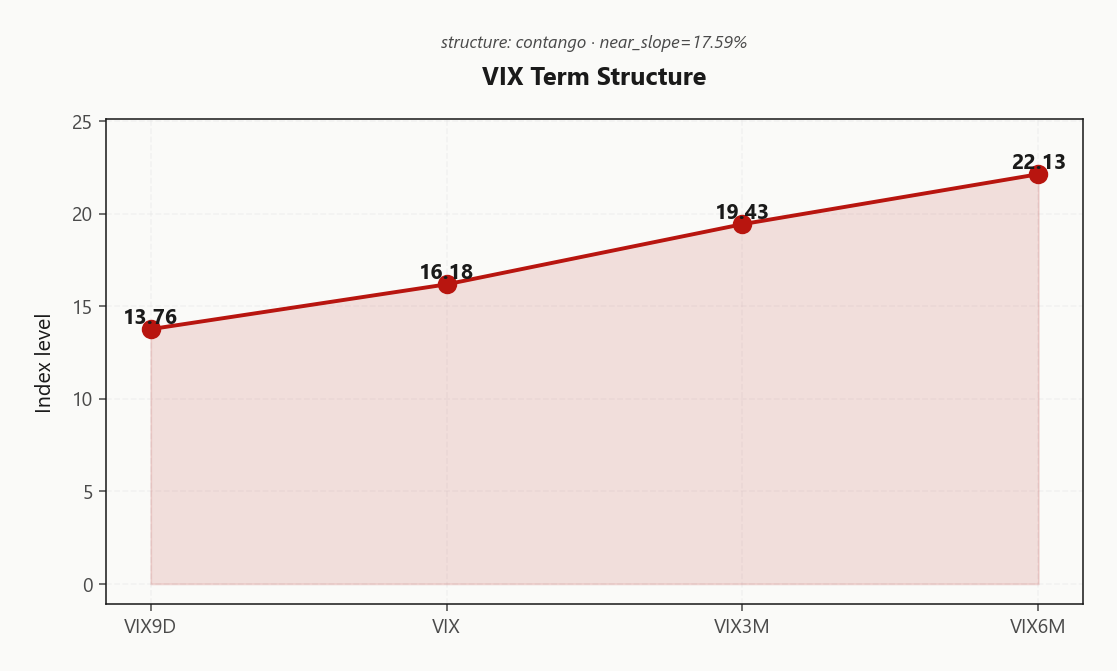

Term structure prints Steep contango - vol sellers favored with VIX9D at 13.76 sitting well under spot VIX at 16.18 - near-dated vol is underbid against the one-month, and the curve into 19.43 and 22.13 holds clean Contango. No event premium is being priced into the front; the back end is simply demanding term, not crisis insurance.

Forward 20.8660286111 versus spot VIX is the carry seam - sellers are paid to roll down the slope, and the 24.5346469304 forward confirms the priced-in escalation is orderly, not panicked. The steepest segment of the curve is the part that pays.

Best edge lives in the 30-45 DTE window where slope is richest and roll-down captures most aggressively. Steep Contango is a vol-seller's regime - carry the front, finance the wings off the back, and let the curve do the work.

What it means for your trading

Steep contango - vol sellers favored with VIX9D under VIX and a clean ramp into 22.13 defines a carry-friendly geometry; trade the roll-down in the 30-45 DTE window where the slope pays most.

Trading readSteep contango with VIX9D well below VIX3M - vol-sellers' carry curve. Slope of 17.59% per cent rewards rolling short front into long mid; no event premium pricing in the front month.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 11.5% trades comfortably above HV20 at 9.6 - the premium is real, and it's being paid in the body of the curve, not just the wings. VRP of 1.9% reads Thin Premium: enough carry to justify short-premium structures, not enough to justify reaching for size.

The deceleration tells the rest of the story. HV60 at 14.21 sits well above HV20 - realized vol is cooling, not coiling. Sellers earn the differential between elevated implied and decelerating realized, but the spread is normalized, not a gift. This is carry, not asymmetry.

Translate it to position: defined-risk short premium dominates naked structures here. With vol-of-vol firming in the background, give back a touch of theta to cap convexity - iron condors and put spreads over strangles. Size to the normalized carry, not the headline VRP print.

What it means for your trading

IV at 11.5% over HV20 at 9.6 with VRP reading Thin Premium supports short premium, but normalized carry - not gift levels - argues defined risk over naked structures.

Skew Convexity

Quarter-delta skew prints 2.34% with a smile ratio of 1.19% - puts paid over calls in ordered fashion, not tail-bid panic. Put quarter-delta IV at 14.52% versus ATM 13.24% defines the actual cost of asymmetry; the gap is real but carryable, not a hedge-flow stampede.

The call wing tells the more interesting story: 12.18% sits flat-to-inverted versus ATM - zero upside conviction is bid into the curve. No one is reaching for calls, which means a melt-up scenario gets repriced violently rather than gradually. Combined with a smile ratio above one, the structure is textbook orderly downside premium with hollowed-out upside wings.

Trade implication: verticals over outrights. Naked puts are bleeding carry against the steepened put wing, and naked calls collect almost nothing for the tail. Put spreads neutralize the skewed wing financing, call spreads exploit the inverted upside. In this regime, defined-risk structures dominate outright wings on every vol-adjusted metric that matters.

What it means for your trading

Skew is steep but ordered - puts richer than calls at 2.34% with smile ratio 1.19% reflecting hedge demand, not panic, while the flat call wing at 12.18% signals no upside chase. Vertical spreads dominate naked wings on a carry-adjusted basis.

Vol-of-Vol Structure

VVIX prints 91.60 against a VIX of 16.18, with the ratio sitting at 5.66 - squarely in the Normal band. The headline level is benign; the composition is not. VVIX expanded 6.44% on the session while spot VIX barely flinched - vol-of-vol is leading, and that divergence is historically the early tell that the consensus short-vol carry is getting crowded.

The mechanical read: rising VVIX with flat VIX flags binary-outcome pricing creeping into the wings - convexity is bid even as the body of the surface stays anchored. Sizing guidance reads Standard Size, consistent with the Normal band, but the path matters more than the level. Bias structures toward defined risk over naked premium; an Iron Condor in the 30-45 window captures roll-down without leaving wings exposed to a VVIX re-rate.

Hard line: VVIX through the triple-digit handle is the trigger to halve risk. Until then, carry the short-vol book at standard clip but treat every uptick in the ratio as a sizing signal, not noise.

What it means for your trading

VVIX firming at 91.60 against a calm VIX of 16.18 keeps the Normal regime intact and supports Standard Size, but the leading divergence biases execution toward defined-risk structures and a hard downsize trigger if VVIX breaks the triple-digit handle.

Dispersion Spread

Index vol is the quiet one in the room. SPY ATM IV at 11.5% sits well under QQQ at 19.14% and IWM at 20.08% - a clean tell that correlation is moderate and the heavy lifting is being done at the single-name layer, not at the index.

QQQ's premium over SPY is the tech-led dispersion footprint: mega-cap idiosyncratic risk is bid while index correlation stays subdued. IWM's lift is the other side of the same coin - small-cap stress that never surfaces in the broad index print. Two distinct fragility pockets, one calm headline number.

Trade implication is unambiguous. With dispersion this wide, index condors dominate single-name strangles on a vol-adjusted basis - you're selling the most suppressed leg of the surface while idiosyncratic noise compounds elsewhere. Avoid name-specific short premium while dispersion is expanding; the realized path in QQQ and IWM constituents will chew through carry that the SPY surface no longer pays you for.

What it means for your trading

SPY IV at 11.5% versus QQQ at 19.14% and IWM at 20.08% argues for index condors over single-name strangles - sell the suppressed index leg, let dispersion stay in the names.

Liquidity & Microstructure

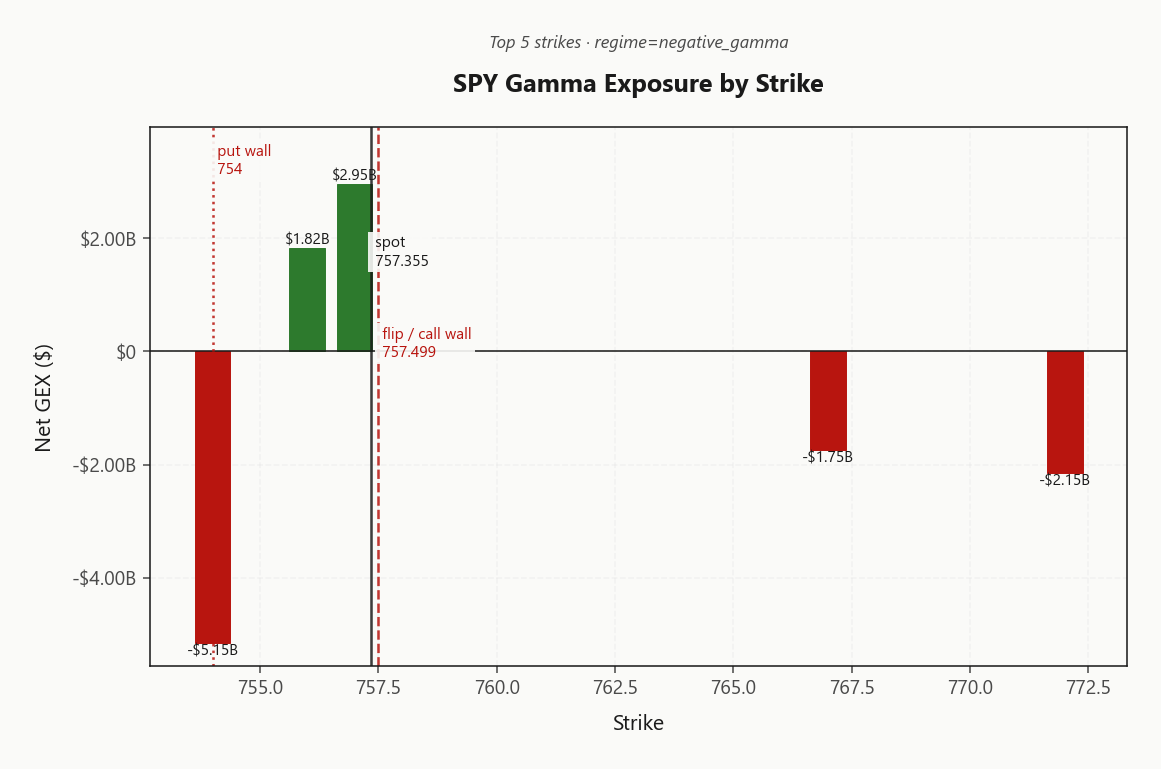

SPY at 757.36 is welded to the 757.50 gamma flip - spot and pivot are effectively the same number, which is the highest-reflexivity setup the tape offers. Above the line dealers stabilize; below it they amplify. Right now the book is balanced on the knife edge, and any decisive print picks the regime for the session.

The range is bracketed by a heavy put wall at 754.00 and a call wall at 757.50. Top-strike OI concentrates at 754.00 carrying net GEX of -$5.15B - the single deepest pool of forced dealer flow in the book, and the level that flips hedging direction when it goes. Highest-OI strike anchors at 565, well below spot, so the latent gravity is downward if the pivot fails.

Trade the 754.00 - 757.50 band mean-reverting while spot holds the flip. A clean break of 754.00 hands dealers a selling mandate into weakness; rallies into 757.50 get capped by supply.

What it means for your trading

Spot pinned on 757.50 with the put wall at 754.00 as the failure trigger - binary regime switch, not a gradient.

Trading readNegative gamma below the flip, modest positive cluster right around spot - dealers amplify any decisive move away from 757.50. Above the call wall they dampen rallies; below the put wall they accelerate selling. Trade the range until it breaks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks are pulling in one direction and it isn't the stabilizing one. Net VEX prints -$53.84B - deeply negative - meaning any uptick in implied vol forces dealers to sell delta, the textbook vanna accelerant. Stack net CHEX at -$1.73B on top and time decay adds a second seller into the close. Vol pop plus clock ticking equals double accelerant, no offsetting hedger in the book.

The charm pivot sits at 757.4978931935 - same level as the gamma flip, a clean single inflection. Current bias reads Destabilizing with signal Red: spot below pivot means dealer flow amplifies, above pivot it stabilizes. Treat this as binary - there is no gray zone between regimes.

What it means for your trading

With VEX at -$53.84B and CHEX at -$1.73B, dealers are a one-way accelerant in any vol expansion, and the 757.4978931935 pivot is the single level that flips the book from amplifying to stabilizing.

Cross-Asset Confirmation

Credit complex flashes the all-clear: MOVE at 73.33 sits unchanged, so the bond vol tape refuses to confirm any equity-side stress. No rates panic, no flight-to-quality bid - whatever is rattling SPY's gamma book is not being echoed in fixed income. That alone reframes today as an equity-isolated mean-reversion setup, not the opening leg of a systemic risk-off.

Within equity the dispersion does the talking. QQQ at 741.19 holds cleanly above its flip in dealer-stabilized territory, while IWM at 290.64 trades under its put wall in trend-amplification mode - classic intra-equity divergence with tech as the anchor and small caps as the pressure valve. Cross-asset tone reads Qqq Heavier, which keeps the index condor thesis intact.

Sentiment closes the loop: Fear & Greed scores 56 rating Greed - contrarian bias is to fade strength, not chase it. Pair greedy positioning with negative dealer gamma and you get an asymmetric fade-the-rip setup, but without the credit confirmation needed to press a directional short.

What it means for your trading

MOVE flat and Fear & Greed at Greed rule out credit-led panic and tilt toward fading strength rather than chasing weakness. QQQ above flip versus IWM under its put wall confirms intra-equity dispersion, not systemic shock - trade the index condor, skip the directional macro hedge.

Scenario EV

Scenario EV scores Iron Condor at 40 against the put spread's 28 - defined-risk wins because diverged dealer regimes plus a firming VVIX argue against naked premium. The 30-45 DTE window is the structural sweet spot: far enough out to dodge 0DTE pin reflexivity, close enough to harvest the steepest roll-down on a Steep Contango curve from 13.76 into 19.43.

Iron condor over strangle is the carry-vs-tail decision. Skew sits at 2.34% with smile ratio 1.19% - puts are paid but not panic-bid, so wing definition costs little relative to the disaster protection it buys. Anchor the body inside the 754.00 - 757.50 dealer corridor and let the Unknown VRP work.

Put spread at 28 remains the directional alternative if spot loses 754.00 and the Destabilizing charm regime activates. Size half while VVIX runs at 91.60.

What it means for your trading

Trade Iron Condor structures in the 30-45 DTE window, anchored inside the 754.00 - 757.50 corridor; rotate to put spreads if spot breaks 754.00.

Actionable Summary

Bottom line: structure Iron Condor in the 30-45 DTE window as the primary expression. The 757.4978931935 charm pivot is the binary trigger - above it dealer flow stabilizes, below it the book amplifies into a negative-gamma cascade with vanna (-$53.84B) and charm (-$1.73B) compounding the slide.

Regime reads Elevated / Watchful with VIX at 16.18 and term structure in Steep Contango - carry trades work, but VVIX firming to 91.60 argues for half-size, not full deployment. Avoid naked strangles, single-name short premium, and any full-size short-vol expression while vol-of-vol leads vol higher.

Watch level: SPY 754.00 put wall - a clean break flips dealer hedging from absorbing to selling, and the Positive Gamma cushion in tech will not be enough to offset a small-cap-led flush given IWM already sits below its own put wall.

What it means for your trading

Trade Iron Condor in 30-45 DTE around the 757.4978931935 pivot at half-size; a break of 754.00 hands dealers a forced-sell loop and ends the carry regime.

Iran deal-to-halt-war signal is the dominant geopolitical lever today - peace progress collapses oil and crude vol, deflating the inflation-fear bid that has supported gold and weighed on duration.

Rubio testimony on the Iran war re-injects headline risk during the trading session - congressional scrutiny can swing the diplomatic narrative either way intraday.

Trump halting Israeli strikes on Beirut tightens the de-escalation narrative - risk premium being unwound across oil, defense, and safe havens simultaneously.

AI-frenzy-stokes-inflation framing matters because it cuts against rate-cut optimism - keeps the back end of the curve nervous and supports the steep VIX contango we're seeing.

Oil down on Iran reviewing the US agreement is the single cleanest macro signal today - lower oil cascades through inflation expectations, terminal rate pricing, and equity risk premia.

Wall Street higher on tech and US-Iran peace hopes establishes the prevailing risk-on baseline that today's session is testing - the QQQ leadership versus SPY/IWM fragility fits this exactly.

South Korea inflation hitting a two-year high with a possible rate hike is a reminder that global tightening risk is not fully retired - a quiet contrarian to the US carry-trade complacency.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 757.50 against a spot of 757.36. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.5% with a volatility risk premium of 1.9%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.18. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime