Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY at 759.32 pinned just under the 760.00 call wall, net GEX of -$10.89B keeps dealers long gamma and moves dampened. Gamma flip sits at 754.98 - spot is barely above it, so cushion is thin and a break below flips us into acceleration mode. Put wall anchors at 754.00 with the heaviest negative-gamma strike at 754.00 - that's the trapdoor. Dealer vanna at -$62.2B is meaningfully short, so a VIX pop crushes dealer delta and accelerates downside; charm at -$1.74B adds late-day sell pressure. VIX at 15.98 with VIX9D/VIX3M in Contango and VVIX at 91.09 - vol-of-vol benign, term carry rich, VRP positive at 1.6%. IWM in Negative Gamma below its flip is the divergence flag - small caps amplify moves. Bottom line: sell premium in 30-45 DTE iron condors anchored 754.00/760.00, half-size if IWM breaks 291.00 or VIX reclaims 17.

SPY trades just below its 760.00 call wall with dealers long gamma - moves get absorbed, not extended. VIX term structure remains in Contango while VVIX sits at 91.09, framing a benign vol-of-vol regime that favors premium harvest. IWM diverges in Negative Gamma territory - the small-cap tape is where stress would surface first.

Regime Assessment

Regime sits at Elevated / Watchful with VIX at 15.98 - neither panic nor low-vol bliss, but the middle of the distribution where carry trades work and tail hedges stay on. The transition matrix is the tell: probability of escalating to panic over the next five sessions is only 0.05, while the decay path down to a low-vol regime over ten sessions runs at 0.45 - roughly even-money in either direction from here.

The half-life of 15 sessions is the load-bearing number. This is a sticky regime, not a transient one - position for persistence, not for a quick break. Cross-asset confirms: SPY and QQQ are Aligned in positive gamma, with IWM's Negative Gamma divergence the sole fragility flag worth tracking.

Trade the persistence: standard-size premium harvest in the recommended 30-45 window, anchored on structural walls. Watch the gamma flip at 754.98 and IWM's flip at 291.00 as the early-warning levels that would force a regime re-rating.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - sticky enough to fund the carry trade, with panic probability at 0.05 over five sessions keeping standard sizing intact.

Trading readVIX low, VVIX benign, MOVE subdued, SKEW elevated - three say calm, SKEW says tails are bid; the divergence is the structural fingerprint of a 'sell vol, but keep tail hedges' regime.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

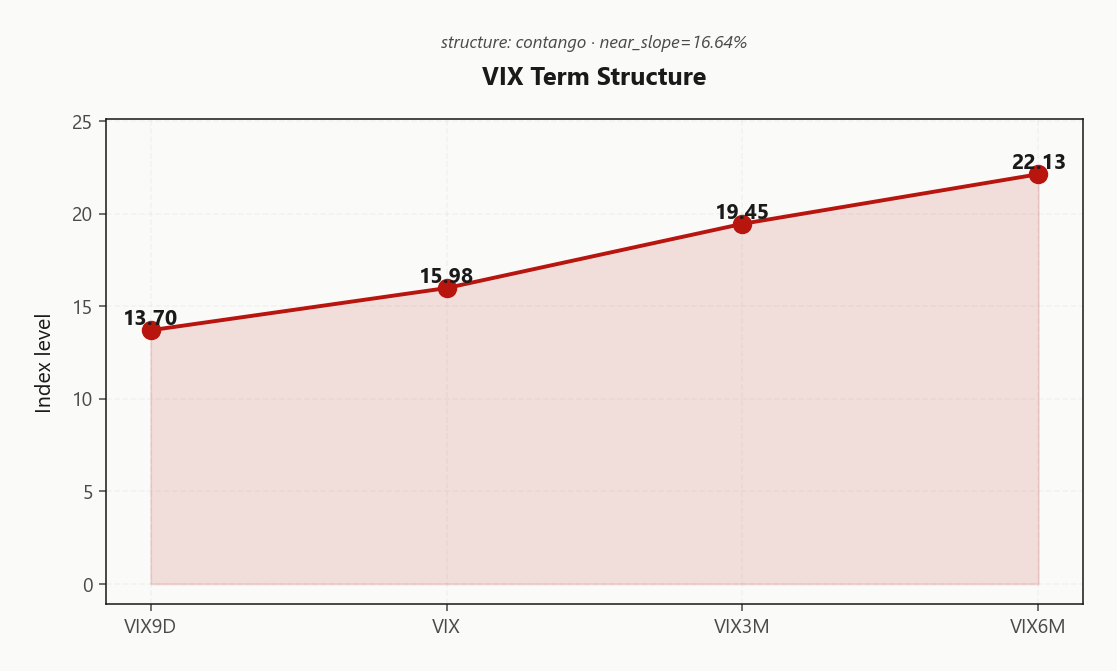

The curve is screaming carry. 13.70 on VIX9D against spot VIX at 15.98 says zero near-term stress is priced, while VIX3M at 19.45 and VIX6M at 22.13 trace a textbook Contango ramp. Near slope of 16.64% is the engine - calendars long the front, short the belly, and 30-45 DTE iron condors capture the fattest roll.

One caveat: this shape reverts violently when it reverts. Harvest the carry, but don't sell wings naked - keep a back-end tail hedge financed by the front-end premium sale.

What it means for your trading

Steep Contango with VIX9D at 13.70 well under spot VIX makes 30-45 DTE the carry sweet spot, but the forward 60-to-90 at 24.5187948317 says don't sell the back-end wings - finance them as tail hedges instead.

Trading readFront-end VIX9D well under spot VIX with the curve rising into 3M and 6M - the carry trade is on, but the steepness itself is a warning that any spot-vol pop has room to invert the curve violently.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 11.09% prints above 20-day realized of 9.49, leaving VRP at 1.6% - positive, but the cushion is thin. Sellers still get paid to underwrite the tape, just not generously. The structural read is that options remain richer than what stock actually delivered, which keeps the premium-harvest bid intact through the front of the curve.

The tell is HV60 at 14.19 running well above HV20 - recent realized has compressed, not exploded. Vol sellers are riding a calming tape where the long-window memory still carries the prior shock, but the short window is doing the heavy lifting on the carry. That gap is the engine of today's edge, and also its fragility: a single accelerating session flips RV5 above HV20 and the VRP margin evaporates before the print refreshes.

Translation for sizing: lean into defined-risk premium sale - 30-45 DTE iron condors over naked strangles. The VRP is positive enough to underwrite the structure, thin enough that an undefined short gamma payout doesn't compensate for the asymmetric tail.

What it means for your trading

Positive VRP with ATM IV at 11.09% over HV20 at 9.49 keeps premium sellers paid, but the margin is thin enough that defined-risk iron condors are the right vehicle - not naked strangles.

Skew Convexity

The wings are doing the talking. Put quarter-delta IV at 13.1% sits well above ATM at 11.83%, while call quarter-delta prints 10.79% - flat-to-inverted versus the body. The 2.31% skew differential is ordered hedging demand, not panic; nobody is paying up for upside.

Smile ratio at 1.21% clears the structural threshold - the left-tail premium is sticky, not a transient bid. The market has priced a ceiling and a bid for downside insurance simultaneously, which is exactly the convexity signature of a complacent tape buying cheap protection rather than chasing.

Trade implication: do not buy naked puts here - the wing is too rich. Put debit spreads dominate, financing the closer-to-money long leg by shorting the structurally bid 13.1% wing. On the call side, the flat-to-inverted profile offers no edge to sell - wrap the credit inside an iron condor anchored at 754.00/760.00 rather than naked.

What it means for your trading

Steep put skew with smile ratio of 1.21% and flat call wing means downside hedges are structurally bid while upside conviction is absent - favor put debit spreads over naked puts and harvest the wings via defined-risk condors.

Vol-of-Vol Structure

VVIX prints 91.09 against VIX at 15.98, putting the ratio at 5.70 - squarely in Normal territory. Sub-hundred VVIX means no jump premium is being bid into the vol-of-vol surface; the market is pricing a smooth drift in either direction, not a binary gap. With the ratio comfortably under six, the expectation is mean-reversion in vol rather than discontinuous repricing.

That combination is the green-light for Standard Size on premium-harvest structures - no need to half-size into the iron condor book despite IWM sitting in Negative Gamma. The vol-of-vol channel says any pop gets absorbed before it cascades.

The tripwire: VVIX punching through the low triple-digits is the first signal dealers are paying up for tail. Until then, the regime stays benign and the carry trade runs.

What it means for your trading

Benign vol-of-vol at 91.09 with a 5.70 VVIX/VIX ratio green-lights Standard Size on premium sales; the early-warning shift is a VVIX break above triple-digits.

Dispersion Spread

Dispersion is alive and well: 18.89% ATM in QQQ sits nearly double 11.09% in SPY, with 19.43% in IWM rounding out the spread. Index netting is doing its job - the mega-cap idiosyncratic risk concentrated in tech names is getting diluted at the SPY level, leaving index premium suppressed relative to the constituents driving it.

The trade is mechanical: sell the index, own the single names. SPY/SPX become the vol-selling vehicle of choice this regime - the basket premium is the cheapest leg to short while the dispersion engine still pays the wings. Avoid short strangles on NVDA, MSFT, AAPL ahead of any name-specific catalysts; that's where the IV is actually earned, not given away. With cross-asset tone Aligned and QQQ holding its Positive Gamma footing, the asymmetry favors index-vol shorts financed by leaving the single-name premium untouched.

What it means for your trading

QQQ ATM at 18.89% versus SPY at 11.09% is the dispersion tell - short index vol via SPY/SPX iron condors, but keep hands off naked single-name premium where the idiosyncratic catalysts actually live.

Liquidity & Microstructure

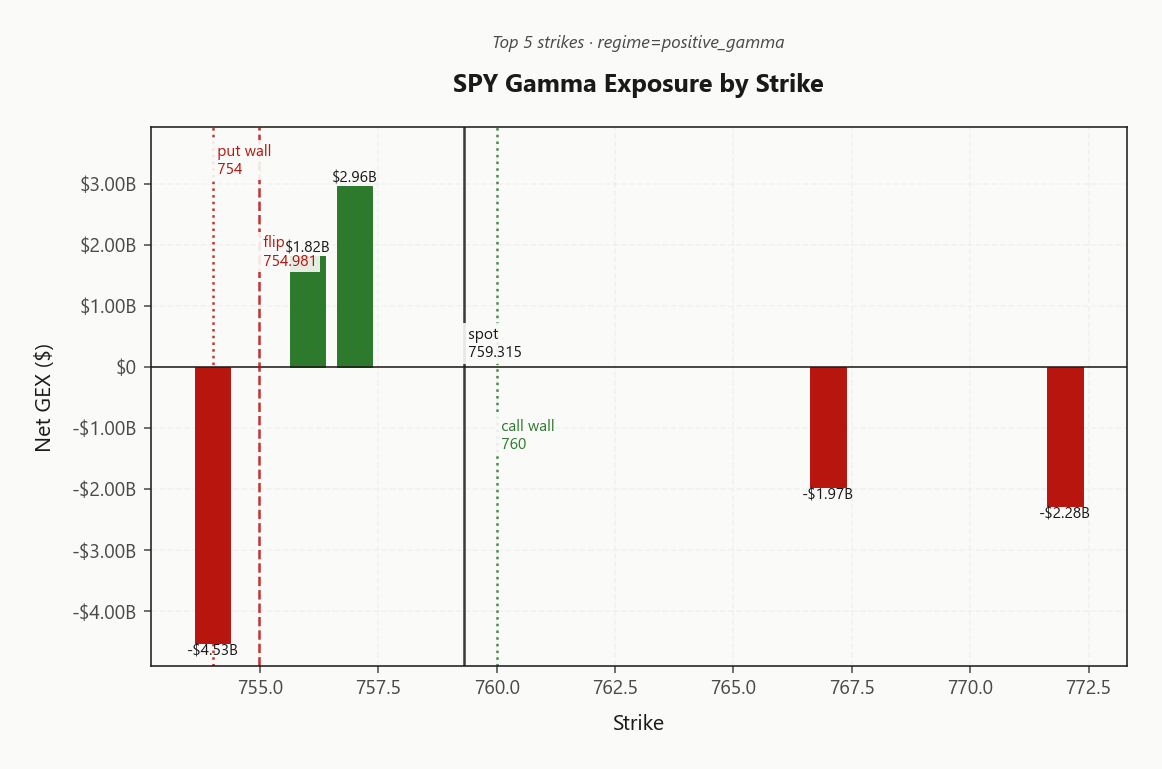

Open interest clusters tightly across the 754.00 - 760.00 corridor with the gamma flip parked at 754.98 - essentially co-located with spot at 759.32. The cushion is paper-thin: dealers are nominally Positive Gamma, but the buffer between here and acceleration mode is measured in basis points, not handles.

Directly below sits the trapdoor - 754.00 carries -$4.53B of concentrated negative gamma, the single heaviest amplifier on the board. Lose the flip and that strike pulls flow into a self-reinforcing leg lower; expected daily range expands meaningfully the moment dealer hedging crosses from suppressive to additive.

Overhead, the 760.00 wall caps the upside path - dealer short-call inventory grinds rallies into pin behavior rather than breakout, and the heaviest OI block at 565 anchors the structural book. The flip is the trade-decision line: above it, fade extensions and harvest premium; below it, stand aside and let the amplifiers run.

What it means for your trading

The 754.98 flip is the binary line for today's tape - above it dealer flow absorbs and pins toward 760.00; below it the 754.00 negative-gamma cluster forces hedging into the move and range expands.

Trading readDealers are long gamma right at spot but the negative-gamma cluster just below the flip is the trapdoor - moves get absorbed inside the put-wall to call-wall band, but a break below 754.98 hands flow to the amplifiers.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna sits deeply negative at -$62.2B - the hedging engine is loaded against the tape. Any uptick in 15.98 mechanically forces dealers to sell delta, so a vol pop doesn't just reprice options, it manufactures supply into spot. Charm at -$1.74B compounds the problem on a different clock: Time decay pushing dealers to sell - pressure into close, a steady late-session bleed independent of whether vol moves at all.

The 760.00 call wall is the single pivot that matters. Above it, dealer flow flips supportive and the vanna/charm load becomes a non-event; below, Vol up = dealers sell delta - downside amplified if vol spikes and the charm drip run unopposed into the close. Current bias reads Neutral with spot pressed against the Call Wall at 760 - a coin-flip setup where the asymmetry sits firmly on the downside if vol breaks higher.

Scenario that matters: a 15.98 spike compounds the negative vanna with the heaviest negative-gamma strike at 754.00 - that's the cascade trigger, not a slow bleed.

What it means for your trading

Dampening is real above 760.00; below it, negative vanna and charm turn dealer flow into an accelerant rather than a brake.

Cross-Asset Confirmation

Cross-asset signal reads Aligned at the index level - SPY and QQQ both sit in Positive Gamma with QQQ printing 744.96, telling the same dampened story from mega-cap down to broad beta. MOVE at 73.33 stays subdued and Fear & Greed reads Greed at 57, so there is no credit stress and no fear premium being paid - this is an equity-only calm, not a macro shock.

The break in the chorus is IWM at 290.77, which sits in Negative Gamma below its flip at 291.00 - small caps are the lone amplifier in an otherwise absorbing tape. That is where the cycle-sensitive break would surface first, and the Iran headline tape isn't pricing into vol because the market is discounting geopolitical stalemate as noise.

Trade the calm, watch the canary: harvest premium in SPY/QQQ while IWM's flip is the cross-asset tripwire - lose it and the divergence becomes the lead story.

What it means for your trading

Index-level regimes are Aligned with MOVE at 73.33 and sentiment in Greed, confirming an equity-only calm; IWM's negative-gamma posture below 291.00 is the single fragility flag worth watching.

Scenario EV

The scoreboard hands the trade to the Iron Condor, posting a best score of 38 against a put-spread alternative that doesn't clear the bar. With VRP still positive at 1.6% and VVIX benign at 91.09, the vol-of-vol green light supports standard sizing - no need to half-clip into a regime that isn't pricing a jump.

Optimal tenor sits 30-45, where the contango roll from 13.70 up through 19.45 is steepest and the carry is fattest. Anchor the wings at the structural walls - short put at 754.00, short call at 760.00 - and let the OI magnets do the bookending work for you.

Avoid naked strangles: call skew is flat-to-inverted so there's no edge selling the upside wing outright, while put skew at 2.31% with smile ratio 1.21% means the left tail is structurally rich - defined-risk wins. Half-size if spot loses 754.98 or IWM breaks 291.00.

What it means for your trading

Sell 30-45 iron condors anchored 754.00/760.00 while VRP and VVIX cooperate; the structure scores 38 versus the put-spread alternative and the wings are your magnets, not your problem.

Actionable Summary

Trade the regime, not the headline. SPY sits in Positive Gamma with spot holding above the flip at 754.98, VRP positive at 1.6%, and VVIX benign at 91.09 - the algorithmic call is Iron Condor in the 30-45 DTE window, wings anchored at the 754.00 put wall and 760.00 call wall. Term structure in Contango pays you to carry; standard sizing is approved.

For directional downside, use put debit spreads - the 2.31% put skew makes naked puts a tax, not a trade. Avoid short strangles on single-name mega-caps; dispersion is alive and idiosyncratic IV dwarfs index ATM. Sell the index, not the names.

Tripwires. SPY losing 754.98 flips dealer flow from absorptive to amplifying - half-size or stand down. IWM in Negative Gamma below its flip at 291.00 is the macro canary; a break there is the cross-asset stress flag well before SPY confirms. Regime read: Elevated / Watchful - sticky, not bliss.

JOLTS surging to a 2-year high reframes the macro: tight labor undermines aggressive cut expectations and pressures the long end - supportive of MOVE staying contained but caps equity upside.

HPE guidance hike echoes Dell's setup - AI-infrastructure capex theme keeps mega-cap tech bid and is a fundamental tailwind under the positive-gamma SPY/QQQ regime.

Reuters Morning Bid framing 'equity supply shock' matters for regime - if absorbed by dealer-positive gamma, supply gets dampened; if it breaks the flip, it accelerates.

AI capex fueling inflation thesis is the single biggest threat to the VIX contango trade - re-acceleration would steepen far-end IV and break the carry.

Nvidia 'supply constrained' commentary keeps the single-name AI bid alive - dispersion stays elevated, reinforcing sell-index-vol-not-single-name positioning.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.98 against a spot of 759.32. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.09% with a volatility risk premium of 1.6%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.98. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime