Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

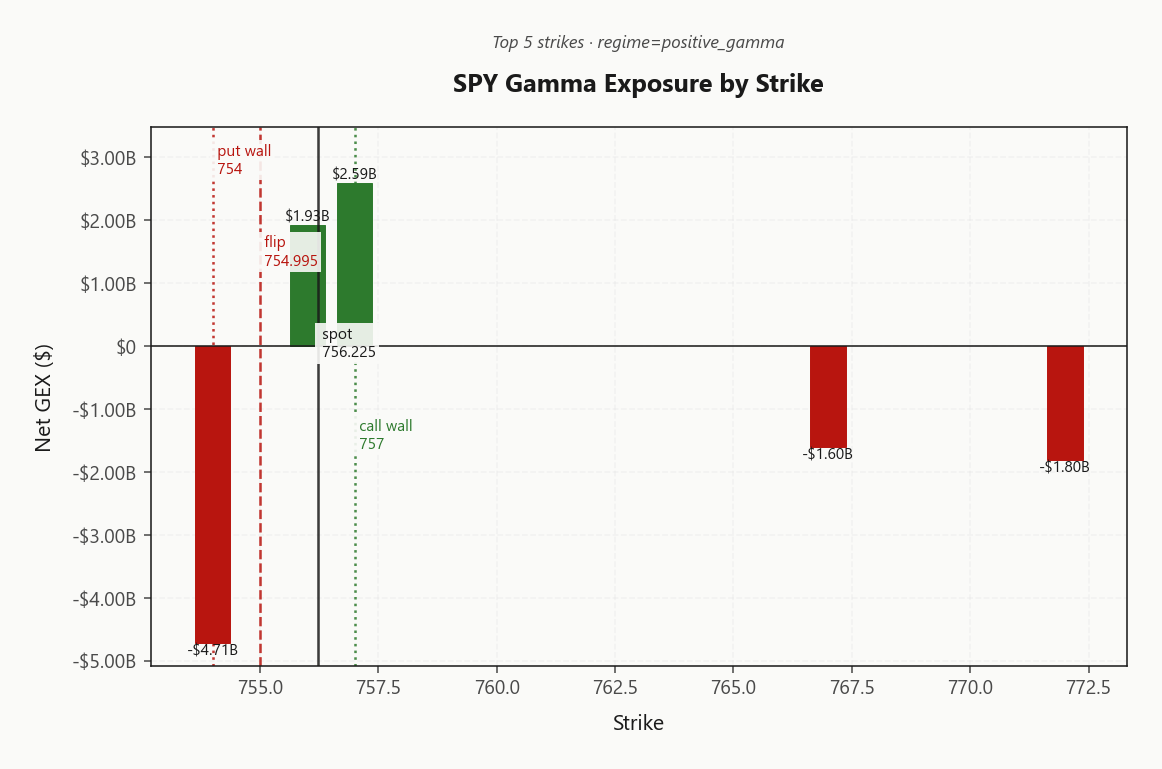

SPY trading at 756.23 with dealers long gamma at -$12.04B - a Positive Gamma regime that dampens moves and rewards mean-reversion fades. Key levels: gamma flip at 755.00 sits just below spot (cushion is thin at 0.1024827267%), with the call wall at 757.00 acting as magnetic resistance and put wall at 754.00 as the floor before flow flips hostile. Net VEX at -$44.86B means a vol spike forces dealers to sell delta - the downside accelerant - while charm at -$1.37B pressures dealers to sell into the close. VIX at 16.20 with term structure in Contango (VIX9D 12.59 → VIX3M 18.66) is textbook vol-seller carry, and VVIX at 86.06 confirms low jump risk. VRP is active at 1.87% vol points, but the 144.18 SKEW reading says the tail is still being bid. IWM diverges with net GEX at -$28.5M below its flip at 289.02 - small caps remain the fragile cousin. Bottom line: structure Iron Condors in the 30-45 DTE window between 754.00 and 757.00, size standard per Standard Size, and trim aggressively if spot loses 755.00.

Positive gamma index complex with IWM lagging; VIX contango invites vol selling but skew warns tail bid

Index complex opens with dealers long gamma in SPY and QQQ at -$12.04B and -$2.12B, anchoring spot near 755.00 where mean-reversion dominates. IWM diverges into negative gamma below its flip at 289.02, flagging small-cap fragility while VIX term structure remains in Contango with VIX at 16.20. The trade is sell premium into the SPY call wall at 757.00, but the 144.18 SKEW print warns the tail is still bid.

Regime Assessment

The tape is in Elevated / Watchful mode with VIX at 16.20 - workable for carry, not benign enough to ignore. The Elevated state is sticky: half-life prints 15 sessions, meaning the contango harvest trade lives for weeks, not days, before the regime naturally rotates.

Transition math favors the seller. The 10-session probability of dropping into the low-vol bucket sits at 0.45 - the dominant drift is down, not up. The 5-session path to panic is only 0.05, but that tail is headline-deliverable: Middle East escalation lands and the half-life collapses overnight.

Posture accordingly. Run the Iron Condor in the 30-45 window, size standard per Standard Size, and keep one cheap tail hedge on. The carry is real; complacency about the path to panic is the trap.

What it means for your trading

Elevated / Watchful regime with VIX at 16.20 and a 15-session half-life favors persistent premium-selling, but the 0.05 five-session panic probability keeps tail hedges non-negotiable.

Trading readVIX up, SKEW up, VVIX flat, MOVE flat - equity vol and tail risk lifting in isolation while bond vol stays calm = isolated equity event, not credit shock. Divergence to watch is MOVE following VIX.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

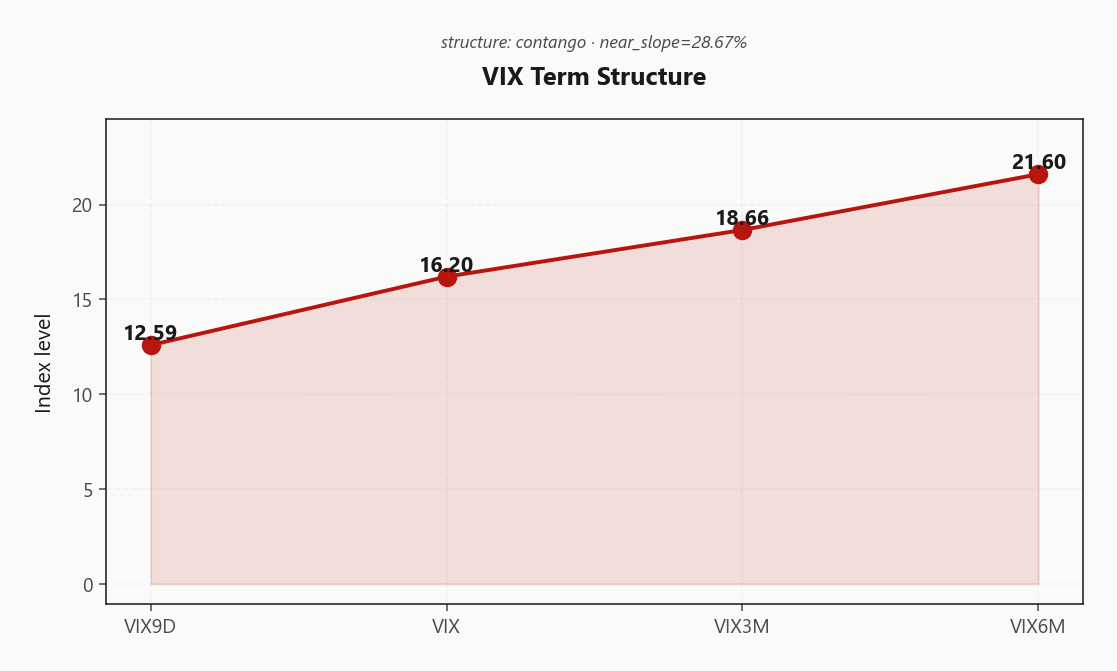

Forward Vol Geometry

The VIX curve is in textbook Steep Contango: VIX9D at 12.59 trades at a clean discount to spot VIX at 16.20, while the belly holds at 18.66 and the long end at 21.60. The front-end discount tells you the tape is not pricing a near-term event, while the term premium past the belly says hedgers are still willing to pay up for the tail beyond a month. That is the carry trade configuration in its purest form.

Near slope at 28.67%% confirms the regime as Steep Contango and the structure as Contango. The edge sits in the belly: sell premium in the 30-45 DTE window where contango is feeding theta but you are not yet paying the long-end term premium.

Avoid buying short-dated vol absent a hard catalyst - the front-end discount is precisely what punishes long-gamma carry. The risk to the trade is binary: any headline that lifts spot VIX through the front of the curve collapses the discount and the carry inverts overnight.

What it means for your trading

Curve in Steep Contango with the front-end discount to spot VIX confirming no event premium - sell 30-45 DTE belly, avoid short-dated longs.

Trading readSteep contango with VIX9D well below VIX and VIX6M printing the term premium - vol-seller carry trade is fully there, but the >2-point spot/front-month spread leaves no buffer if a single headline lifts spot VIX.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM implied at 11.67% sits cleanly above realized HV20 at 9.8, leaving 1.87% vol points of premium on the table - the textbook VRP harvest backdrop where options are paying for movement that has not been delivered. Premium-sellers collect first.

The caveat lives in the longer window: HV60 prints 14.54, materially elevated against HV20, meaning recent realized has decelerated from a noisier two-month tape. That deceleration is the coiled-spring risk - short premium pays until realized re-converges higher, so size against HV60, not HV20, and keep the wings tight.

Across the complex, QQQ VRP runs richer at 3.21% vol points - tech is the better carry trade today as dispersion keeps single-name vol bid while index IV gets diluted. IWM VRP is slim at 0.42% and not worth shorting given the small-cap sits in negative_gamma; the thin premium is correctly priced for the fragility.

What it means for your trading

Index VRP is active and harvestable with QQQ offering the richer carry at 3.21% vs SPY's 1.87%; size against HV60 at 14.54 rather than HV20 since the recent deceleration leaves room for realized to re-converge higher.

Skew Convexity

The put wing is paying up in an orderly way. Put quarter-delta IV at 15.08% sits cleanly above ATM at 13.47% and well clear of the call quarter-delta at 12.39% - a clean asymmetry that reads as measured tail demand, not crash hedging.

Quarter-delta skew at 2.69% with smile ratio 1.22% confirms the left wing is bid in an ordered, premium-paying manner - institutional protection, not panic. The CBOE SKEW print at 144.18 ticked 3.34% on the session as Middle East headlines lifted convexity demand without dragging VVIX off its 86.06 floor.

Trade implication: the wing is too rich to short outright. Express downside protection through put spreads to finance the bid wing; sellers of premium should avoid naked short puts and rotate to put spreads or iron condors that monetize skew steepness rather than fight it.

What it means for your trading

Skew is steep and ordered: put quarter-delta 15.08% versus call quarter-delta 12.39% with SKEW at 144.18 flags measured tail demand. Sell put spreads, not naked puts.

Vol-of-Vol Structure

Vol-of-vol is Low: VVIX prints 86.06 against VIX at 16.20, with the ratio at 5.31 sitting cleanly inside the normal band. No binary outcome is being priced into the convexity of vol itself - the jump premium that screens before a real dislocation is absent.

That reads as a green light for Standard Size on the short-premium book. This is not a half-size environment; the carry trade in Steep Contango can be worn at full clip, and the Iron Condor in the 30-45 window does not warrant haircuts on size.

The asymmetry: any single headline that drags VVIX through the jump-risk threshold flips the calculus instantly - convexity reprices before spot vol does. Keep one cheap tail hedge on, and treat a VVIX break as the trigger to cut size, not a reason to be there now.

What it means for your trading

VVIX at 86.06 and the ratio at 5.31 green-light Standard Size - wear the carry at full clip, but a VVIX break-out is the size-cut trigger.

Dispersion Spread

The dispersion gap is the cleanest carry in the complex today: SPY ATM IV at 11.67% sits well under QQQ ATM IV at 19.19%, with IWM ATM IV the highest of the three at 20.12%. AI-led narrow leadership is keeping single-name vol bid while the index gets diluted by the broader basket - the textbook setup where index implieds underprice the realized dispersion that mega-cap idio is delivering.

Trade the structure, not the symbol. Index iron condors in SPY harvest the muted index vol between 754.00 and 757.00, while single-name premium stays rich and compresses through dispersion. QQQ at 19.19% is the better carry of the two index vehicles given the 3.21% VRP backdrop, and IWM's 20.12% print correctly prices the negative-gamma fragility below its flip at 289.02 - do not short that vol.

Bottom line: sell the index, leave the single-names alone, and let dispersion do the work.

What it means for your trading

Index IV at 11.67% trades a clean discount to QQQ at 19.19% and IWM at 20.12% - sell index condors, skip single-name shorts, and let dispersion compress the gap.

Liquidity & Microstructure

The strike map is doing the heavy lifting here: spot at 756.23 sits a sliver above the gamma flip at 755.00, with the put wall stacked directly underneath at 754.00 carrying -$4.71B of net GEX. That is the floor dealers are paid to defend - and the level where flow flips hostile if it gives way.

Overhead, the call wall at 757.00 is the magnetic ceiling for the session. Expect dealer supply to thicken into any push toward it; fade strength there rather than chase. Between the walls, hedging is mechanical and symmetric - the mean-reversion corridor is wide open for premium harvest.

Ignore the headline OI print at 565 - that is long-dated structural positioning, not session-relevant tape. The actionable book sits in the 754.00 - 757.00 band, and the cushion below spot is thin at 0.1024827267%.

What it means for your trading

Dealers are positioned to defend 754.00 and cap into 757.00 - trade the corridor, but respect that loss of 755.00 flips the regime.

Trading readMassive negative-gamma cluster at the put wall with positive-gamma walls above spot - dealers will buy weakness into 754.00 and sell strength into 757.00, classic mean-reversion zone today.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna prints deeply negative at -$44.86B - a vol-up shock mechanically forces dealers to sell delta into weakness, the textbook downside accelerant that turns a benign tape into an air-pocket if VVIX lifts off 86.06. Long gamma alone is not the full story; the bundle reads supportive in calm, hostile in spasm.

Charm sits at -$1.37B, a steady-state pressure that pushes dealers to lighten delta into the bell - the systematic late-session drift that fades any uncontested afternoon rally. The pivot is 757 (Call Wall), with current read Neutral; cushion to the flip is thin at 0.1024827267%.

Trade: fade rallies into 757.00, keep a cheap tail hedge live for the VEX accelerant, and trim aggressively if spot loses 755.00.

What it means for your trading

Long gamma stabilizes the tape but negative vanna at -$44.86B arms the downside - fade strength into 757, defend below 755.00.

Cross-Asset Confirmation

The cross-asset tape is Aligned and that is the tell: MOVE at 70.22 sits quiet while equity vol and skew lift on weekend Middle East headlines. Bond vol is not confirming. This is an isolated equity narrative being priced through options, not a credit shock bleeding across asset classes.

QQQ at 738.81 and SPY hold the Positive Gamma bid together while IWM at 288.24 drags in Negative Gamma - large-cap leads, small-cap is the fragile cousin. Fear & Greed reads 60 (Greed), supportive but not stretched - there is no contrarian short signal from sentiment yet.

Trade the isolation: stay short index premium while bonds confirm calm. The regime flips the moment MOVE tracks higher with VIX - that cross-asset confirmation reprices the book from contained-equity-vol to credit-shock-pricing, and the carry trade dies first. Watch MOVE as the leading indicator, not VIX.

What it means for your trading

Equity vol and tail premium are lifting in isolation while MOVE at 70.22 stays calm - carry trade is live, but the regime breaks if bond vol joins the move.

Scenario EV

The scorecard prints Iron Condor at 32 - the cleanest expression of a positive-gamma index complex stapled to a VIX curve in Contango. Long dealer gamma at -$12.04B caps range expansion between the put wall at 754.00 and call wall at 757.00, while the front-end discount from VIX9D 12.59 into VIX3M 18.66 bleeds theta directly into the seller.

The 30-45 DTE window is the carry sweet spot - far enough out to harvest meaningful decay, close enough to dodge longer-dated term premium and event drift. Put spread alternative scores 21 - viable for directional books but inferior carry for a range-bound regime. VRP backdrop reads Unknown; trust the structure score over the bucket label.

Sizing stays standard per VVIX at 86.06 - Low jump regime, no half-size adjustment warranted. Trim if SPY loses 755.00.

Trade: put on the Iron Condor in SPY between 754.00 and 757.00, 30-45 DTE - positive gamma at -$12.04B caps range while Contango term structure (VIX9D 12.59 → VIX3M 18.66) feeds the theta. QQQ carries the richer VRP at 3.21% - sequence the condor there first.

Avoid: naked short puts - skew at 2.69% and SKEW at 144.18 make the wing too rich to short outright; use put spreads. Skip IWM long-vol - small caps remain in negative gamma at -$28.5M, sitting below the flip at 289.02, so flow amplifies rather than dampens.

Watch: the SPY gamma flip at 755.00 - losing it pivots dealer flow from supportive to accelerating, especially with net VEX at -$44.86B. VVIX at 86.06 - a break higher invalidates Standard Size sizing. Regime reads Elevated / Watchful: sticky, but headline tail risk persists - keep one cheap hedge on.

What it means for your trading

Sell the Iron Condor in SPY/QQQ between 754.00 and 757.00 for 30-45 DTE, fade IWM long-vol given negative gamma below 289.02, and trim aggressively if spot loses the 755.00 flip while VVIX threatens to break out of its Low jump regime.

SpaceX/OpenAI/Anthropic IPO narrative reinforces the AI-led-leadership concentration risk highlighted in the dotcom comparison news.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 755.00 against a spot of 756.23. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.67% with a volatility risk premium of 1.87%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.20. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime