Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY closed at 758.66 with dealers in Positive Gamma and net GEX at -$11.46B - moves dampen, mean reversion wins until breached. Key levels: call wall at 760.00 (spot sitting right beneath it), gamma flip at 754.99 (0.1772874363% cushion - thin), put wall at 754.00. Dealer flow: net DEX positive at $10.79B, but VEX deeply negative at -$56.77B - a vol spike turns dealers into delta sellers and amplifies any breakdown. Charm pressure tilts dealers to sell into the bell - typical end-of-session drift. Vol read: VIX at 16.00 climbing 4.44%%, VVIX expanding to 90.99, term structure in steep contango with 16.7%% near slope - vol carry rich, sellers paid handsomely. IWM is the tell: dealers short gamma below flip at 289.09, trend follows lower if small caps lose 275.00. Bottom line: sell premium in SPY/QQQ via Iron Condor in the 30-45 bucket, but size half on any IWM breakdown that drags index correlation higher.

Positive gamma cushion across SPY/QQQ holds while IWM slips below flip - divergence is the story

SPY and QQQ closed the session firmly in positive gamma with spot riding just under the call wall at 760.00, while IWM tipped into negative gamma below its flip at 289.09. VIX term structure remains steep contango with Steep contango - vol sellers favored, but VVIX ticked higher to 90.99 - the tape is calm on the surface and quietly paying up for vol-of-vol. Bottom line: index complex is in a mean-reversion regime favoring premium sellers, but small-cap fragility is the asymmetric risk no one is hedging.

Regime Assessment

Tape sits in the Elevated / Watchful bucket with VIX at 16.00 - north of the structural low band, well shy of stress. Yellow signal, not red. The mean-reversion half-life of 15 sessions tells you this is a sticky regime: don't expect it to resolve in a week, and don't trade as if it will.

Transition math reinforces the posture. Five-session panic probability prints at 0.05 - negligible, no tail bid required in size. But ten-session decompression odds run 0.45 - materially probable, and the asymmetric path of least resistance is down the vol surface, not up. Sellers of front-end premium get paid to wait.

Position for the grind. Iron condors and calendar carry harvest the regime; chasing breakouts or paying up for tail convexity fights it. The watch trigger is VVIX expansion through the 90.99 handle, not VIX itself - that's the signal the sticky regime is breaking, not the spot tape.

What it means for your trading

Elevated / Watchful with half-life of 15 sessions - position for grind, decompression odds at 0.45 favor premium sellers over tail buyers.

Trading readVIX firmer, VVIX expanding faster than VIX, SKEW elevated, MOVE asleep - equity vol-of-vol is being quietly bid while rates stay calm, a divergence that often precedes a regime shift.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

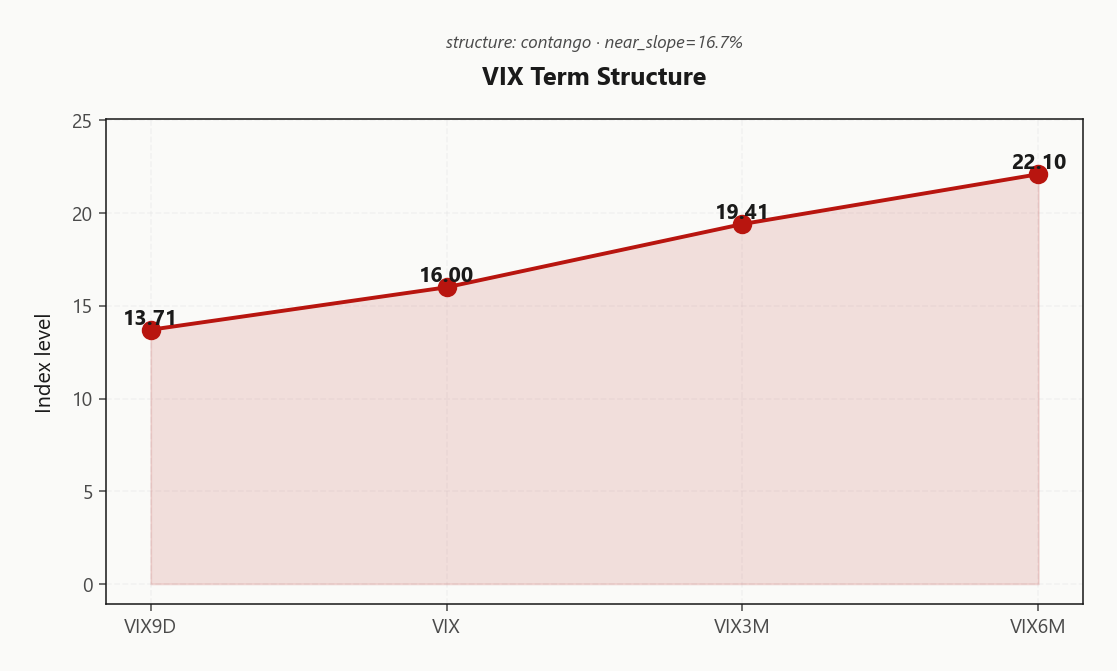

Forward Vol Geometry

The term structure is in Steep Contango - VIX9D at 13.71 sits well beneath spot VIX at 16.00, with VIX3M extending to 19.41. Front end is relaxed, the back end keeps climbing - Steep contango - vol sellers favored. Structural carry is paying and there is no event premium concentrated in any single tenor; this is clean contango, not a fear-shaped curve.

The forward 30-to-60 prints 20.9074663697, marking the sweet spot where roll-down is fattest without crowding into back-end illiquidity. That window dominates the EV map for premium sellers - far enough from the front-week gamma whip near 754.99, short enough to harvest the slope before vega risk dilates.

Calendar long-back, short-front is the cleaner expression than naked vol selling: you bank the contango without sitting outright short convexity while VVIX at 90.99 quietly bids. Default structure for the section: Iron Condor in the 30-45 bucket, financed by the slope rather than fighting it.

What it means for your trading

Steep contango with the front end relaxed at 13.71 and the long end stretched to 19.41 pays sellers to carry - the 30-to-60 forward at 20.9074663697 is where the cleanest roll lives. Favor calendar long-back/short-front over outright vol shorts.

Trading readContango with VIX9D well below VIX and the long end stretching to 22.10 - vol sellers paid handsomely to carry the front end, no stress priced into any window.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The index complex is trading rich to realized, and the spread is where the trade lives. SPY HV20 sits at 9.75 against an ATM IV of 11.21%, leaving the variance risk premium at 1.46% - moderate, payable, but not the fat pitch.

The fat pitch is QQQ. VRP runs 2.76% against an ATM of 18.69% - the widest spread in the complex and the highest premium-per-unit-of-risk on offer. IWM is the opposite tell: VRP collapses to 0.22%, effectively fairly priced, leaving nothing to harvest on the short-vol side and confirming the small-cap fragility the gamma map already flagged.

Realized is not accelerating, so there is no urgency to chase IV higher into the bell. On a risk-adjusted basis the order is clear: short QQQ vol > short SPY vol >> short IWM vol. Concentrate condor risk in tech, leave small-cap premium alone - own downside there instead.

What it means for your trading

VRP is alive in SPY at 1.46% and fattest in QQQ at 2.76%, while IWM's 0.22% spread offers no edge - concentrate short-vol structures in QQQ, avoid IWM premium selling.

Skew Convexity

Quarter-delta put skew runs 1.68% on SPY with smile ratio at 1.17% - downside vol bid, upside wing flat. Puts mark 11.33% against an ATM print of 10.18% while calls trade at 9.65%. The convexity bid is broad: every index shows smile ratio above parity, no one is paying up for the right tail.

QQQ skew is the steepest of the complex at 3.35% - tech downside the most expensive insurance in the book - while IWM holds skew at 1.9% even sitting in Negative Gamma, meaning the chain isn't fully discounting the fragility below the flip at 289.09. Either skew is cheap there, or small-cap protection is the under-owned trade.

Trade the steepness, don't pay the wing. Put spreads dominate naked puts at these levels - finance the long leg by selling the deeper strike, harvest the smile rather than paying it. Short call wings into a flat upside surface stays the cleanest financing trade.

What it means for your trading

Put skew elevated, calls flat - the surface prices downside protection and ignores upside, so put spreads beat naked puts and IWM skew at 1.9% looks underpriced for a tape already in negative gamma.

Vol-of-Vol Structure

VVIX prints 90.99 against VIX at 16.00, putting the ratio at 5.69 - squarely Normal on the regime map. On the surface, nothing to write home about: the dial says Standard Size and the tape closed green.

The tell is in the second derivative. VVIX expanded by 5.73% while VIX barely moved - that is convexity being bid into a quiet print, not a coincidence. Somebody is paying up for jump risk while the headline gauge naps, and that asymmetry tends to lead, not lag.

Trade the regime as written - Normal means full clip on iron condors and short premium in the index complex - but set the trip wire now. VVIX through 100 is the size-down line: halve premium-short exposure, and treat any VVIX expansion that outruns VIX as the first crack in the dampening trade.

What it means for your trading

Vol-of-vol screens Normal at a 5.69 ratio so size stays standard, but today's VVIX bid on a green tape is the quiet warning - convexity is being accumulated while VIX sleeps.

Dispersion Spread

Index vol screens cheap against single-name vol - that's the dispersion tell. SPY ATM IV at 11.21% sits well inside QQQ's 18.69%, and the mega-cap movers - MSFT, AAPL, AMZN, TSLA, GOOGL - are clearing single-name premium that runs visibly fatter than the index complex carrying them. Cross-strike dispersion at 80.3 is moderate, not screaming, but the signal is consistent: correlation discount is being paid.

The implication is mechanical. Sell the index, leave the names. SPX/SPY iron condors in the 30-45 bucket harvest the moderate VRP without paying up for single-stock idiosyncratic risk that's commanding its own bid. Naked short-vol on TSLA or the mega-caps is the wrong side of dispersion here - that's where the premium actually lives.

What it means for your trading

With SPY ATM at 11.21% versus QQQ at 18.69% and single-name vol running materially richer, the dispersion lean is unambiguous: short index premium via Iron Condor, do not short single-stock vol into it.

Liquidity & Microstructure

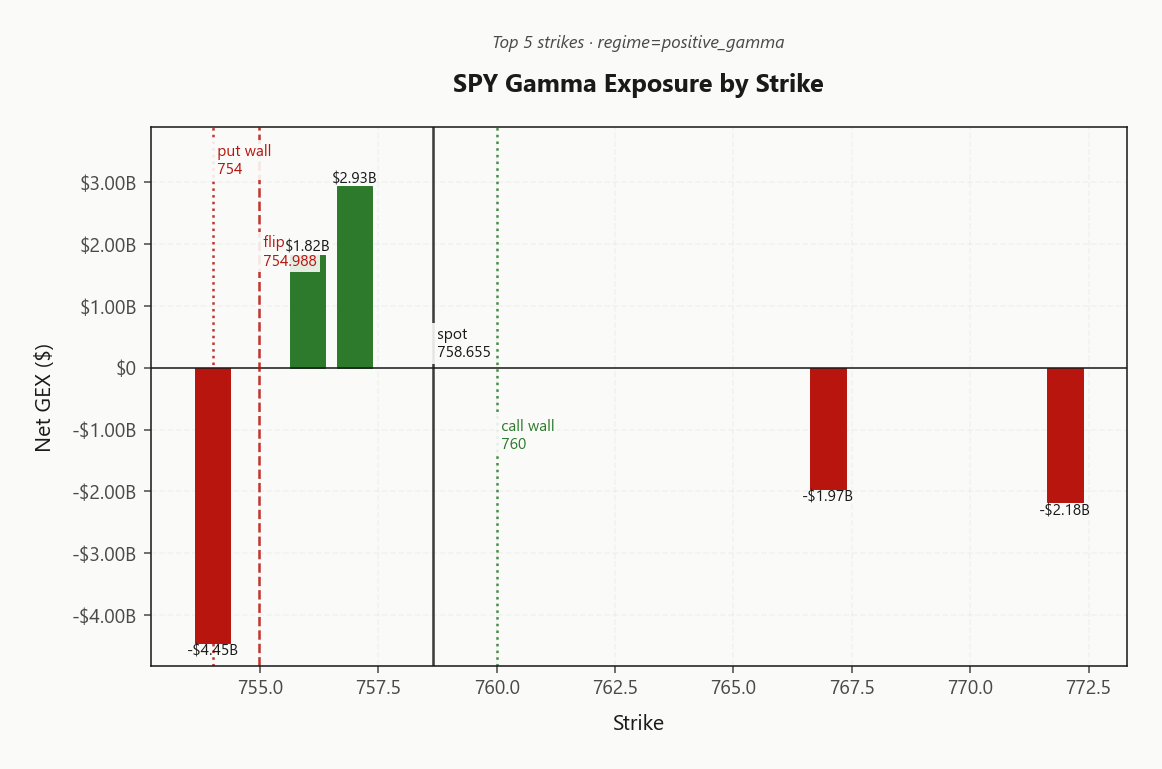

Ignore the headline open interest figure - the highest-OI strike at 565 is legacy structural positioning, not where today's tape is being fought. The live battlefield is 754.00, carrying -$4.45B of net gamma and effectively defining the flip at 754.99. That cluster is THE level for this session - dealer hedging behavior inverts on each tick across it.

Above the flip, mechanical dampening reasserts and rallies decay into the call wall at 760.00, where Positive Gamma exhausts and supply meets every probe. Below it, dealers turn sellers into weakness and slippage compounds. The put wall at 754.00 sits as the reversal pivot on downside flow - close beneath it and the entire dampening engine runs in reverse overnight.

Trade the corridor between 754.00 and 760.00; the legacy OI strike is a distraction, the flip at 754.99 is the line that matters.

What it means for your trading

Today's microstructure is defined by the 754.00 gamma cluster, not the headline OI strike at 565 - flow inverts at the flip 754.99, with rally exhaustion at 760.00 and the downside reversal pivot at 754.00.

Trading readGamma stacks heavily near the call wall and the cluster around 754.99 - dealers dampen rallies into the wall but the flip is so close that one bad session inverts the whole picture. Trade the range, respect the edges.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Strip the gamma cushion away and the second-order book is hostile. Net VEX sits at -$56.77B - a vol shock flips dealers into mechanical delta sellers, with vanna as the accelerant rather than the brake. Charm at -$1.73B layers a steady late-tape drift on top: dealers shed length into the bell whether spot cooperates or not.

The pivot is 760, structurally the Call Wall and the line where today's regime narrative either holds or inverts overnight. Current bias reads Neutral - knife's edge, not conviction. Hold above and supportive dealer buying keeps the dampening engine intact; lose it and the VEX/CHEX combo compounds into a one-way pressure trade as vanna unwinds and charm stops paying you to fade.

Translation for the book: the positive-gamma comfort is conditional. Sell premium with one eye on the pivot, finance convexity hedges with the call wing while skew lets you, and respect that the same vanna that pins you today does the selling for you tomorrow.

What it means for your trading

Dealers are long gamma but short vanna and charm - the cushion holds above 760 and inverts below it, with VEX at -$56.77B ready to convert any vol spike into forced delta supply.

Cross-Asset Confirmation

Cross-asset tape is Aligned on the surface but quietly fractured underneath. MOVE sits benign at 70.22 - rates vol is asleep, no credit contagion bleeding into equity hedges - while Fear & Greed prints 59 (Greed), confirming positioning is extended and the marginal dollar is already long risk.

The real story is the index split. QQQ at 742.32 holds Positive Gamma with dealers cushioning every dip, mega-cap gamma absorbing the tape. IWM at 288.93 sits below its flip at 289.09 in Negative Gamma - small-cap dealers are now short gamma, forced to sell weakness and chase strength. That's the asymmetric leg no one is paying for.

Bottom line: large-cap pin holds while rates and credit stay quiet, but the foundation is the IWM put wall at 275.00. Lose it, correlation snaps higher, and the SPY/QQQ dampening trade unwinds in a single session.

What it means for your trading

MOVE at 70.22 and F&G Greed confirm a calm, risk-on backdrop, but QQQ positive gamma versus IWM below flip is the fragile divergence - own IWM downside, sell large-cap premium.

Scenario EV

The scorecard prints Iron Condor as the structure of choice at 30, comfortably ahead of the put spread at 17 - moderate edge, not a screaming setup, but the cleanest expression of the regime. VRP is Unknown on the scorecard yet the surrounding tape - QQQ VRP at 2.76%, SPY at 1.46%, VIX term in Steep Contango - pays the seller to wait.

Sweet spot sits in the 30-45 DTE bucket: long enough to harvest the full carry across 20.9074663697 forward vol, short enough to roll cleanly past the next macro print. Bracket the SPY structure between the 760.00 call wall and the 754.00 put wall; VVIX at 90.99 sits in the Normal band, so deploy Standard Size.

Pair with a long VIX call hedge if VVIX breaches triple digits, and stay clear of front-week 0DTE - gamma whips around the 754.99 flip and the 0.1772874363% cushion is too thin to underwrite weekly tape risk.

What it means for your trading

The book pays you to sell defined-risk vol in the belly of the curve via Iron Condor structures in the 30-45 window - standard size while VVIX stays orderly, halve it the moment the flip at 754.99 gives way.

Actionable Summary

DO: sell premium in SPY and QQQ via Iron Condor structures in the 30-45 DTE bucket, bracketing the call wall at 760.00 against the put wall at 754.00. Own IWM put spreads outright - dealers are short gamma below the flip at 289.09, and that tape risk is going unhedged across the complex.

AVOID: naked short VIX calls with VVIX expanding to 90.99 on a green tape - vol-of-vol is being quietly bid. Skip chasing SPY 0DTE upside through 760.00; dealer dampening kicks in hard against the wall and the payoff thins fast.

WATCH: the charm pivot at 760 - a close below flips the regime overnight and inverts the mean-reversion engine. If VVIX clears the triple-digit threshold, halve all premium-short risk. Regime read: Elevated / Watchful - yellow, sticky, position for grind not breakout.

What it means for your trading

Sell SPY/QQQ Iron Condor in the 30-45 window bracketed by 754.00 and 760.00, hedge the IWM tail, and treat a close below 760 or a VVIX breakout as the kill switch.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.99 against a spot of 758.66. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.21% with a volatility risk premium of 1.46%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.00. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime