Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

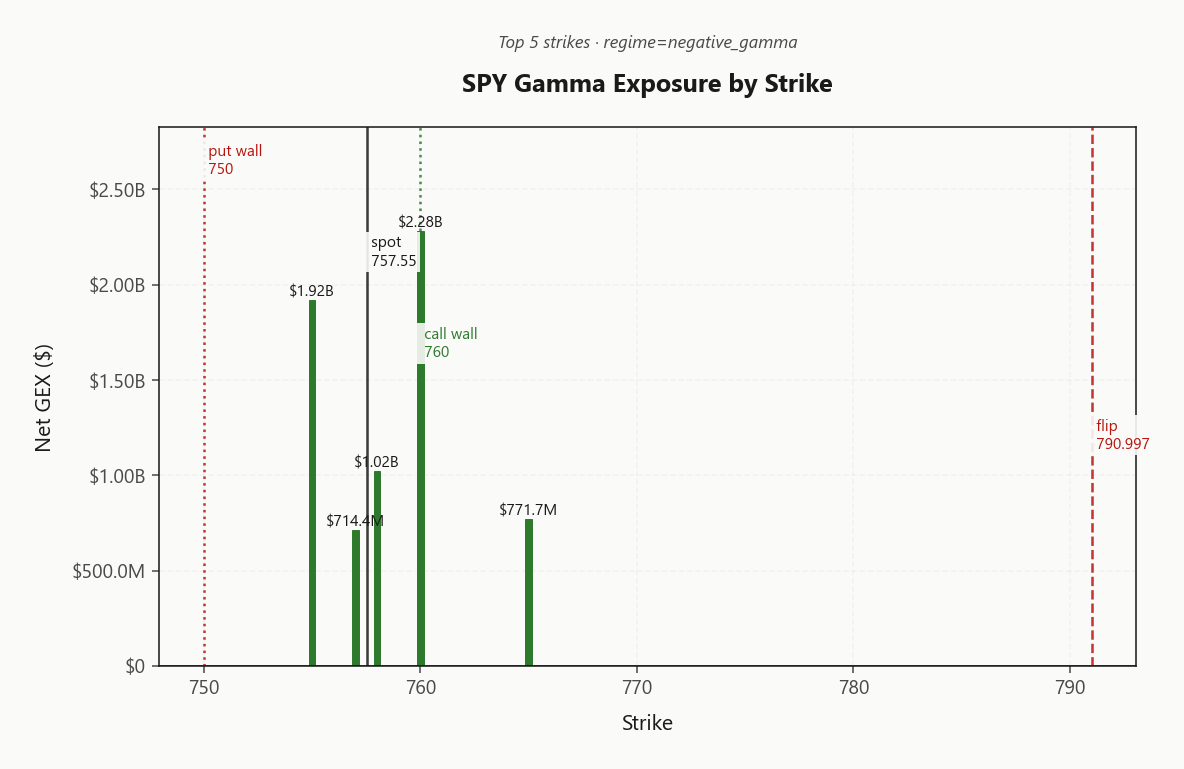

SPY at 757.55 sits below its gamma flip at 791.00 - dealers short gamma, moves amplified, while net GEX still prints $8.26B from concentrated upside walls. Call wall 760.00 caps rallies; put wall 750.00 is the support to defend; gamma flip overhead means a push back above 791.00 flips dealer flow supportive. QQQ (Positive Gamma, spot above flip 660.98) and IWM (Positive Gamma) diverge from SPY - tech and small caps are the cushioned tape, SPY is the fragile one. Vol read: VIX 15.70, VIX9D 12.98, VIX3M 19.11 - steep contango (20.96%% slope), VVIX 86.03 subdued, VRP 1.64% active. Vanna (-$296.93B) is the accelerant if VIX pops - short-vol carry is paid but needs a stop. Bottom line: sell premium in 30-45 DTE iron condors around SPY's 750.00/760.00 walls, fade strength into the flip from below, and treat a QQQ break of 660.98 as the kill switch on the carry trade.

SPY in negative gamma below flip while QQQ/IWM hold positive - divergence is today's tell

SPY trades 757.55 under its gamma flip at 791.00, putting dealers in amplification mode while QQQ and IWM still sit above their flips in positive gamma. Vol term structure is steep contango (Steep contango - vol sellers favored) and VVIX/VIX ratio prints Low - carry environment intact. The cross-asset regime split, not the absolute VIX print, is the story to trade.

Regime Assessment

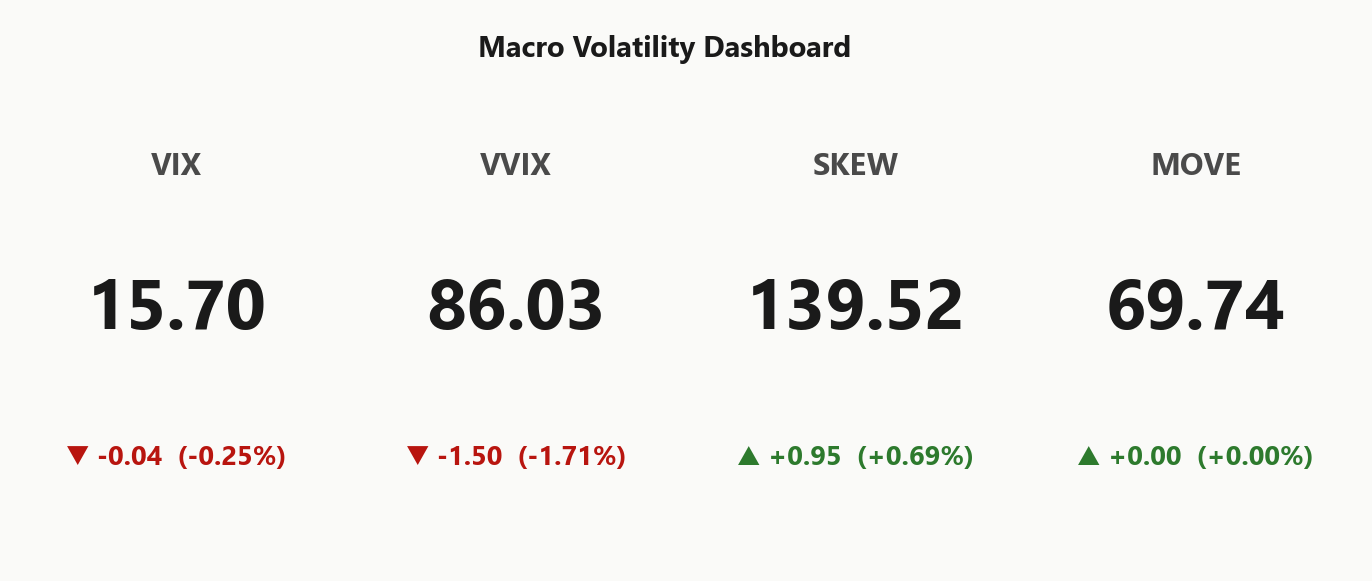

The tape sits in Elevated / Watchful - VIX at 15.70 is north of the dormant band but well shy of stress. Transition math is the story: probability of a panic break in five sessions reads 0.05, while the path back to a low-vol regime over ten sessions sits at 0.45. Neither side has the votes - the modal outcome is stays here.

Half-life prints 15 sessions, which is the operative number. Regimes this sticky reward fading the edges, not chasing the breakouts - vol mean-reverts to itself before it mean-reverts to the next regime. SPY's local Negative Gamma posture below 791.00 is the fragility inside an otherwise stable structure, not a regime change in waiting.

Trade the regime you have: sell premium, size standard per Standard Size, and let the half-life do the work. The kill switch is a VVIX lift with VIX flat - that's how Elevated becomes Panic, and it isn't printing yet.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life and panic odds of 0.05 - fade the edges, don't fight the band.

Trading readVIX subdued, VVIX subdued, MOVE flat, SKEW elevated - four sleepy needles and one whisper. The SKEW divergence is the only watch-out: tail demand without VIX confirmation usually resolves with VIX catching up, not SKEW falling.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

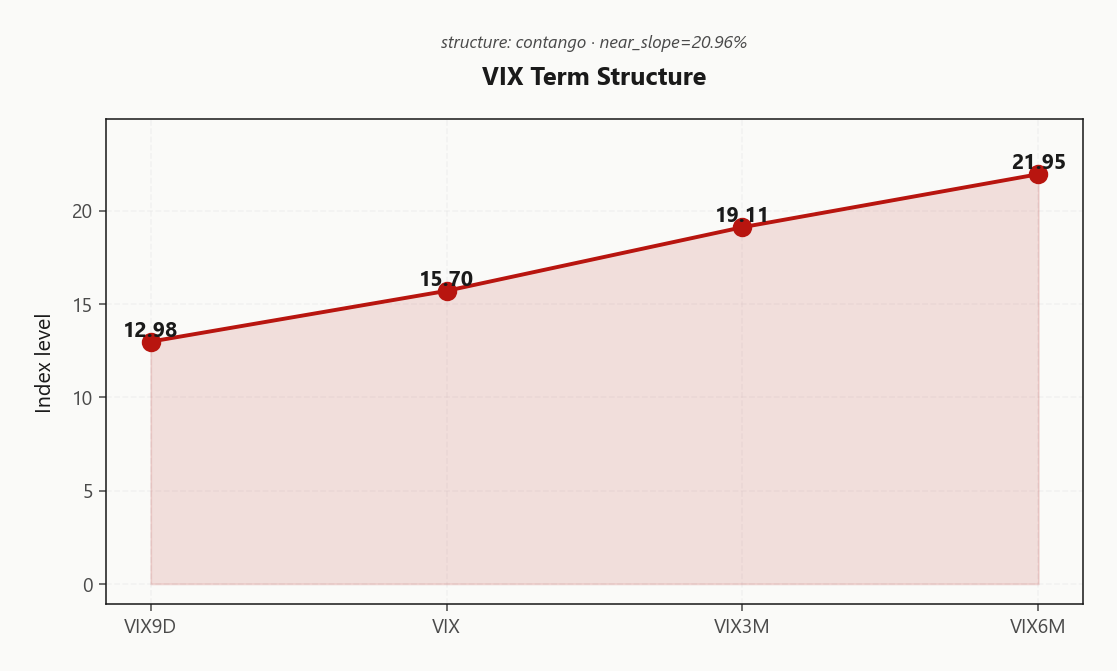

The VIX curve prints Contango with VIX9D at 12.98 sitting under spot VIX at 15.70 - realized hasn't bled into front-week implieds, and the near slope at 20.96%% is textbook structural. VIX3M ramps to 19.11 and VIX6M to 21.95, with the 30-60 forward at 20.6044449088 and 60-90 forward at 24.4624794328 - a clean ramp with no event hump, meaning the curve isn't pricing a near-dated catalyst.

Regime label reads Steep contango - vol sellers favored. The carry trade is paid, and the structural tailwind sits with the front-end seller. Best edge prints in the 30-45 DTE window where forward vol is cheapest versus the back-month bid - sell the front, respect the back-of-curve ramp.

Watch one number: a VIX9D cross above spot VIX flips the contango to backwardation and is the kill switch on the structural carry. From 12.98 versus 15.70, that line is not close today.

What it means for your trading

Steep contango with VIX9D well under spot and a clean back-curve ramp leaves the structural sell-vol carry intact - fade the front, anchor in 30-45 DTE, and treat a VIX9D reclaim above 15.70 as the regime-flip trigger.

Trading readContango with a steep near slope - sellers are paid up front, and the back-of-curve ramp prices longer-dated unease without immediate catalyst. Classic carry-trade setup with a back-month tail bid.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Implieds are bid over recent realized across the complex - SPY ATM IV prints 11.4% against HV20 of 9.76, leaving the index VRP at 1.64% and the structural seller paid. The carry isn't uniform: QQQ carries the widest gap at 2.99%, while IWM compresses to 0.53% as realized closes on implied. That fan-out is the trade - same regime, different edge per venue.

HV60 sitting above HV20 at 14.61 says realized has been decelerating, not accelerating into the print. Term-structure of realized vol cooling into a still-rich implied surface is the textbook setup for premium harvest; the curve isn't pricing a near catalyst and the spot tape isn't delivering one. Vrp_active across the board, widest in QQQ, thinnest in IWM.

Action: anchor short-vol structures on QQQ where the carry is fattest, treat SPY as the size-balancer, and keep IWM out of the short-premium book - the gap doesn't pay for the gamma.

What it means for your trading

Vol sellers are paid over recent realized across the index complex, but the edge is concentrated in QQQ where VRP at 2.99% prints widest; IWM's thin 0.53% is the venue to skip.

Skew Convexity

Quarter-delta put skew prints 1.62% on SPY with smile ratio 1.19% - left tail still bid even with VIX anchored at 15.70. Put quarter-delta IV at 9.95% sits well above ATM 9.18%, while call quarter-delta prints 8.33% - below ATM. No upside conviction is priced; the smile is a one-sided hedge, not a two-way bet.

QQQ tail runs steeper at 2.04% - tech beta loaded with downside protection demand. IWM smile ratio at 1.09% is the flattest of the complex, making small-cap convexity the cheapest left-tail expression on the board. Smile ratios above unity across the board confirm ordered hedging - flow is structured, not panicked.

Trade implication: at this skew geometry, put spreads dominate naked puts - you're paying for protection that's already richly bid, so finance the long leg by selling further-out tail. Naked short puts collect thin premium against a skew that punishes mark-to-market on any vol pop.

What it means for your trading

Quarter-delta put skew at 1.62% with call quarter-delta below ATM signals ordered downside hedging without upside conviction - favor put spreads over naked puts, and lean on IWM at smile ratio 1.09% for the cheapest tail convexity in the complex.

Vol-of-Vol Structure

VVIX prints 86.03 against VIX at 15.70, ratio 5.48 - Low. The market isn't pricing a bimodal regime; no jump-risk premium is baked into the vol-of-vol layer, and the carry trade isn't being charged a convexity tax to stay in the seat.

Sizing reads Standard Size - no half-rack discount, no fractional book. Run the iron condor at full clip, because the second-order surface is telling you the regime is anchored, not coiled. That's a different message than VIX alone: VIX can sit subdued because realized is quiet; VVIX subdued means the distribution of VIX itself is well-behaved.

The watch is the leading-indicator break. A VVIX lift through triple digits with VIX still pinned at 15.70 is the early shift - vol-of-vol moves first, VIX confirms second, and the carry is already bleeding by the time the spot tape notices. Until that print arrives, the Low regime says size up, not down.

What it means for your trading

Vol-of-vol at Low with VVIX/VIX ratio 5.48 sanctions Standard Size on the short-vol book. Watch VVIX through triple digits with VIX still anchored at 15.70 - that's the carry-trade exit bell.

Dispersion Spread

Index-level vol screens benign - SPY ATM IV prints 11.4% and IWM at 19.95% - but QQQ runs richer at 19%, and that gap is the dispersion fingerprint. Tech beta is loaded into the index implied while broad-market realized stays anchored; the single-stock layer is doing the work the index isn't pricing.

That asymmetry has a trade implication: idiosyncratic risk lives at the constituent level, not the wrapper. Selling single-name strangles forfeits the correlation cushion that makes index premium-selling robust - when one mega-cap blows out, the index absorbs it, the single name does not. With cross-asset tone Unknown and the QQQ/SPY regime split flagging Qqq Heavier, the diversification benefit accrues to the index seller, not the name picker.

Play it through SPY/SPX iron condors and let QQQ-anchored structures harvest the richer wing premium. Skip single-name short vol - the dispersion isn't paying you enough to carry the jump risk.

What it means for your trading

Index IV at 11.4% understates the cross-sectional risk priced into 19%; sell vol at the index layer where correlation does the hedging for you.

Liquidity & Microstructure

SPY's open interest stacks heavy at the upside walls with the active gamma concentration at 760.00 printing $2.28B of net GEX - that's the live hedging node. The headline 550 top-OI strike is historical residue, not active flow; ignore it for today's tape.

Spot at 757.55 trades beneath the gamma flip at 791.00, putting dealers in Negative Gamma - every dip gets sold harder, every rally meets fade flow into the 760.00 call wall. 750.00 is the bid to defend; reclaim of the flip overhead is the single mechanic that turns dealer flow from amplifying to dampening.

Microstructure caveat: 55.5% of net GEX sits in 0DTE - intraday amplifies, the close pins hard. Size around the magnet, not the day's range, and treat any push back above 791.00 as the regime flip rather than noise.

What it means for your trading

Active wall at 760.00 caps; 791.00 is the binary level - below it dealers amplify, above it they dampen. Fade rallies into the call wall, defend the put wall, and let 0DTE concentration dictate intraday sizing.

Trading readUpside walls stack thick above spot - the 760.00 cap is real but spot is still below the flip, so dealers amplify dips until reclaim. Fade strength into the wall, don't chase breakouts beneath the flip.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The single level that resolves the setup is the charm pivot at 760 (Call Wall). Current bias reads Neutral - neither side owns the flow, which is exactly the condition where vanna and charm dominate price action over fundamental positioning. Below the gamma flip at 791.00, both Greeks lean against dealers; reclaim it and the vector flips supportive in a single tick.

Trade the asymmetry: a VIX pop here is doubly costly because vanna sells into it while charm bleeds the bid. A push back through 791.00 is the green light to lift hedges.

What it means for your trading

Vanna at -$296.93B and charm at -$12.5M are both accelerants pointed down while spot sits beneath 791.00 - the pivot at 760 is the only level that flips the flow vector.

Cross-Asset Confirmation

Cross-asset tape confirms the sell-vol regime even as SPY carries the local fragility. MOVE prints 69.74 - rates vol quiet, no credit signature bleeding into equity hedges. Fear & Greed sits at Greed (60) - constructive sentiment with room before it becomes a contrarian fade. The Iran-framework headline complex is pushing oil lower and equities higher; read it as geopolitical mean-reversion, not a compounding shock.

Breadth holds where it counts: QQQ 739.84 above its flip at 660.98, IWM 290.56 above its own - two of three core indices sit in positive gamma while SPY slips below 791.00. Tech and small-cap are absorbing the risk-on flow; SPY alone is short-gamma. With cross-asset tone Unknown and the macro dashboard quiet, the carry trade still has its tailwind - but QQQ's flip is the kill switch.

What it means for your trading

No macro shock signature - MOVE flat, sentiment in greed, breadth holding above flips in QQQ and IWM. SPY's short-gamma is local, not systemic; sell-vol regime stays intact until QQQ breaks 660.98.

Scenario EV

The EV grid lands on Iron Condor as the cleanest expression - score 49 versus put spread at 37. VRP is active, vol-of-vol prints Low, and sizing guidance reads Standard Size. The regime supports range, not directional skew expression - strangles give back the wings you're being paid to sell, and put spreads concede the upside premium that's still rich at 11.4% versus 9.76 realized.

Optimal window sits 30-45 DTE - far enough out that gamma decay isn't punitive, close enough that the steep contango (20.96% slope) bleeds in your favor. Anchor wings on SPY 750.00/760.00, or shift the venue to QQQ where VRP at 2.99% beats SPY's 1.64% - same structure, fewer crumbs.

Kill switches are explicit: VVIX lifting through triple digits with VIX still anchored, or QQQ breaking 660.98. Either trips the carry trade.

What it means for your trading

Iron condor is the recommended structure at score 49, anchored 30-45 DTE with wings at SPY 750.00/760.00 or QQQ-loaded for the richer VRP.

Actionable Summary

Bottom line: sell premium in 30-45 DTEIron Condors anchored on QQQ where VRP runs widest at 2.99% versus SPY's 1.64%. Use SPY's 750.00/760.00 walls as guideposts and treat 760 as the single number that decides whether dealer flow stays amplifying or flips supportive.

Do: fade SPY strength into 760.00, defend the 750.00 put wall, size standard given VVIX/VIX prints Low. Avoid: naked short puts while spot sits below the gamma flip at 791.00, and skip single-name short vol - dispersion isn't paying for the crumbs. Watch: a VVIX lift with VIX anchored near 15.70 as the early carry-trade exit, and a QQQ break of 660.98 as the regime-change tell that kills the trade outright.

What it means for your trading

Regime reads Elevated / Watchful with cross-asset tone Qqq Heavier - sell vol where it's paid, anchor on QQQ, and let 760 dictate when to fold.

ECB research flagging 'doubly scar' consumer impact from the Iran war injects a slow-burn macro overhang - relevant for the vol-term backend even with front-month contango.

Oil tumbling on US-Iran deal hopes is the single biggest reason VIX9D is suppressed below spot VIX today - it's the catalyst behind the steep contango.

A US-Iran framework deal narrowing in is the central catalyst priced into front-week vol; any breakdown reprices VIX9D first and flips the carry trade.

Largest annual core inflation print in three years is the sleeper macro story underneath the geopolitical optimism - it's the reason VIX3M and VIX6M ramp higher despite spot calm.

Fresh sanctions on Iran's oil sales sits in tension with deal-framework headlines - the policy two-step is exactly what keeps event premium in the back of the curve.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 791.00 against a spot of 757.55. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.4% with a volatility risk premium of 1.64%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.70. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime