Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

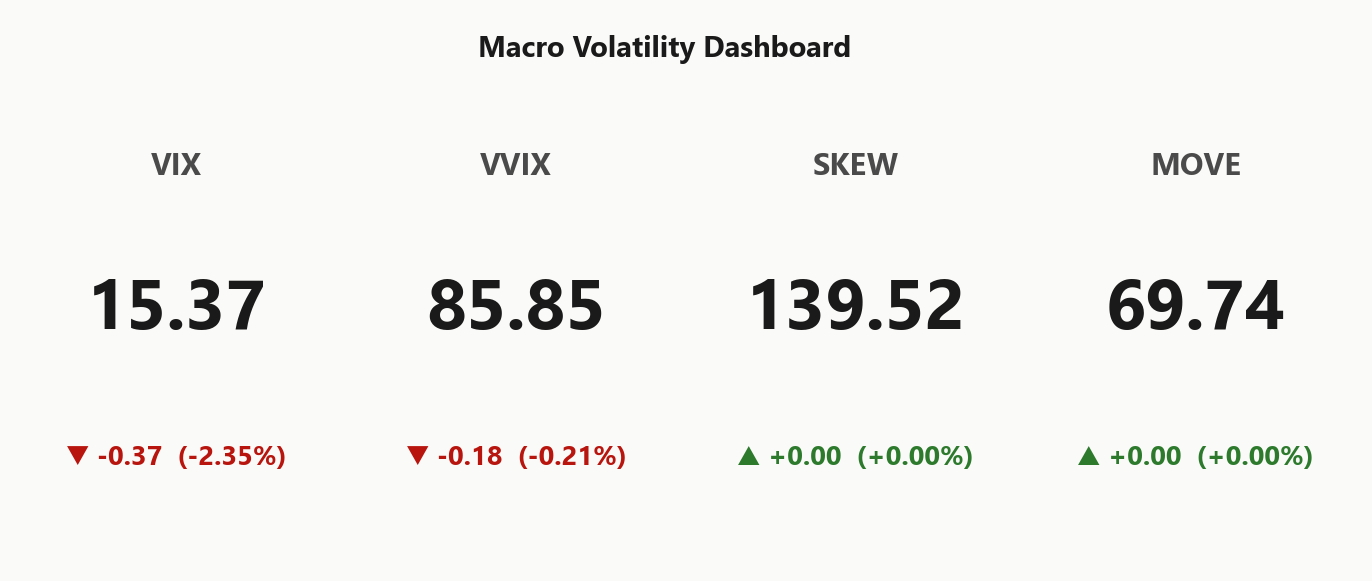

Regime tags Elevated / Watchful with VIX anchored at 15.37 - neither low-vol complacency nor stress, but the watchful middle where premium harvesters get paid without underwriting a binary. The transition matrix is the tell: panic-state probability over five sessions sits at 0.05 while the drift back to low-vol over ten sessions runs 0.45 - the path of least resistance is decay, not dislocation.

Half-life of 15 sessions makes this sticky. Persistence at this VIX level, with cross-asset tape reading Aligned and forward curve in Steep Contango, gives the short-vol carry trade meaningful runway before the regime tips. Steep contango pays the roll; the regime stays put long enough to harvest it.

Action: lean into Iron Condor in the 30-45 window - half-life exceeds tenor, panic odds are remote, and the slow grind toward low-vol is your tailwind. Hedge convexity stays cheap-but-deferred; only re-rate if VIX breaks higher with VVIX confirming.

What it means for your trading

Regime is Elevated / Watchful and sticky - half-life of 15 sessions with panic odds at 0.05 means short-vol carry has time to work before the tape forces a re-rate.

Trading readVIX bleeding, VVIX bleeding, MOVE quiet, SKEW at 139.52 - all four confirming each other in suppressive mode, no divergence signaling a regime shift.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

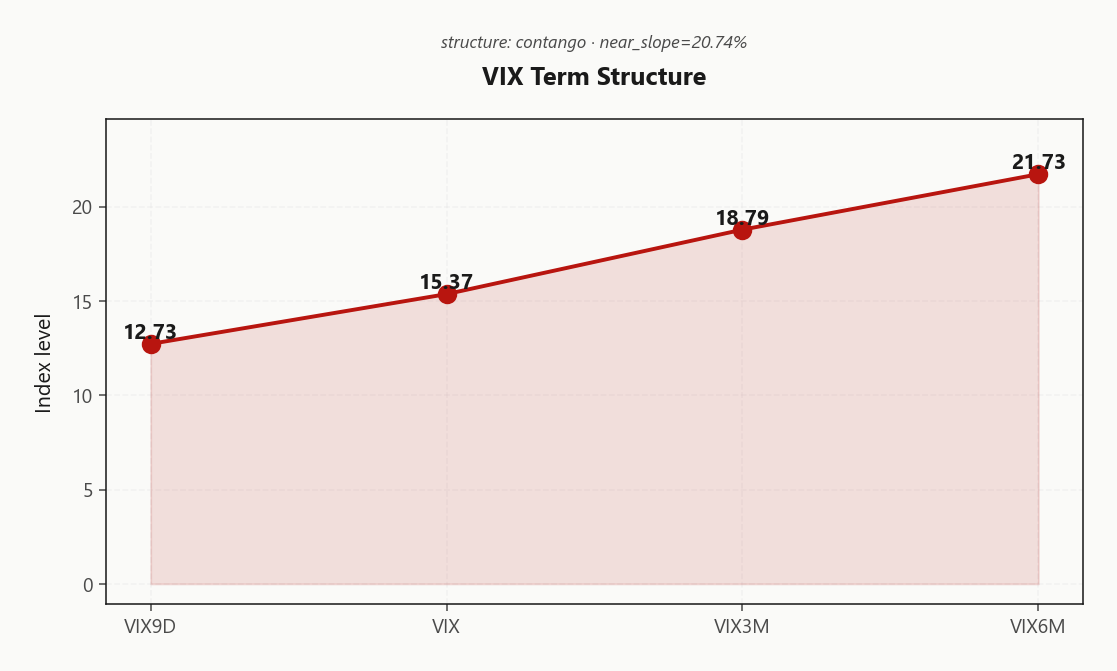

The forward curve is doing the heavy lifting here. VIX9D at 12.73 sits well below spot VIX at 15.37, with VIX3M anchoring at 18.79 and VIX6M further out at 21.73 - a Steep Contango structure that pays sellers to roll down the curve. Near slope at 20.74% confirms the Steep contango - vol sellers favored read: no event premium is being aggressively bid into the back end, just clean carry.

The geometry points to a specific tenor. Forward 30-to-60 implied at 20.284913113 against the back-end at 24.317107147 flags the 30-45 DTE pocket as the sweet spot - far enough out to harvest the slope, short enough to avoid the back-month vega kink. This is where Iron Condor structures earn their keep.

What it means for your trading

With term structure in Steep Contango and front contango healthy at 20.74%, the carry edge lives squarely in the 30-45 DTE window - sell premium where the curve flattens, not where it kinks.

Trading readSteep contango from VIX9D 12.73 to VIX3M 18.79 pays the vol-carry roll - no stress priced beyond the immediate window.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 11.06% sits above HV20 at 9.75, leaving SPY VRP at 1.31% - positive, ordered, and exactly the kind of premium harvesters get paid to collect into a calm tape. Spread assessment reads Thin Premium, which keeps the bar honest: options are richer than realized, but not so rich that the trade is crowded.

The decay structure reinforces it. RV5 at 4.17 well beneath RV20 confirms realized has been bleeding lower into the implied print - vol sellers compound as the tape stays mechanical and the call wall pins. With HV60 still riding above the near window, sellers are paid against a vol stack that has structurally decayed rather than against a base that is rebuilding.

Cross-complex, QQQ VRP at 2.29% prints richer than SPY - tech premium remains the deepest payout per unit of risk. IWM VRP at -0.34% is the laggard: small-cap sellers are under-compensated and the cushion is thinner. Concentrate condor risk on SPY and QQQ; skip IWM premium until the spread re-widens.

What it means for your trading

SPY VRP at 1.31% with ATM IV at 11.06% against decaying realized confirms premium sellers are paid - concentrate the harvest on SPY and QQQ where the spread is deepest, fade IWM where compensation thins.

Skew Convexity

The quarter-delta skew prints at 1.43% with the put wing IV at 9.24% sitting above the call wing at 7.81% - downside is still paying up relative to upside, but the bid is ordered, not panicked. ATM reference at 8.26% frames the put wing as bid-but-contained, while the call wing trades through ATM - a flat-to-inverted call skew that confirms no upside chase is being priced.

Smile ratio at 1.18% reads balanced, not stressed - consistent with the Positive Gamma backdrop and the Low jump-risk read off VVIX. Translation for the book: the wings are not cheap enough to hoard naked puts, but they are rich enough to finance defined-risk downside. Put spreads and call spreads dominate naked wings here - sell the call-side into the 757.00 cap, fund put-spread protection with the still-bid put wing rather than chasing the tail outright.

What it means for your trading

Quarter-delta skew at 1.43% and smile ratio of 1.18% mark an ordered, not stressed, convexity surface - favor spread structures over naked wings, with the call side sold into 757.00 and put protection bought as spreads rather than outright.

Vol-of-Vol Structure

VVIX prints 85.85 against VIX at 15.37, with the ratio compressing to 5.59 - squarely in the Low jump-risk bucket. VVIX is bleeding in lockstep with spot vol at -0.21%, which tells you the options-on-options complex is not hoarding convexity into the close. No bimodal outcome is being priced.

That matters for sizing. When vol-of-vol stays anchored, the tail on your short premium does not fatten asymmetrically overnight - Standard Size sizing is appropriate, no haircut required for a latent VVIX squeeze. The dog that is not barking here is the wing bid: if VVIX were leading VIX higher, you would defer the Iron Condor and pay up for skew. It is not.

Bottom line: collect carry, lean into 30-45 DTE structures, and let the suppressive VVIX print do the work of validating the short-vol thesis. Only re-rate sizing if the ratio reflexively expands back toward jump territory.

What it means for your trading

Vol-of-vol at Low with the VVIX/VIX ratio at 5.59 greenlights Standard Size on premium-selling structures - no regime-shift premium being bid into the options-on-options complex.

Dispersion Spread

Index vol is doing the heavy lifting on the suppression side: SPY ATM IV at 11.06% reads compressed against the single-name complex, with QQQ ATM IV at 18.3% sitting noticeably richer - the tech premium is where the dispersion edge actually lives. Cross-strike dispersion at 85.52 against cross-expiry at 3.49 confirms a moderate, ordered regime - strikes are dispersed but the term surface is tight, classic mid-cycle geometry.

The trade construction follows the geometry: sell the index, leave the names alone. With cross-asset Aligned and the complex uniformly in Positive Gamma, single-name shocks won't transmit cleanly into index hedges - long-index/short-name dispersion is uncompensated here. Concentrate premium harvest in SPY and QQQ where the spread between implied and ordered realized is widest; skip the granular leg.

What it means for your trading

Index IV compressed and dispersion moderate - sell index premium via Iron Condor structures rather than chase single-name vol, with QQQ at 18.3% carrying the richest leg.

Liquidity & Microstructure

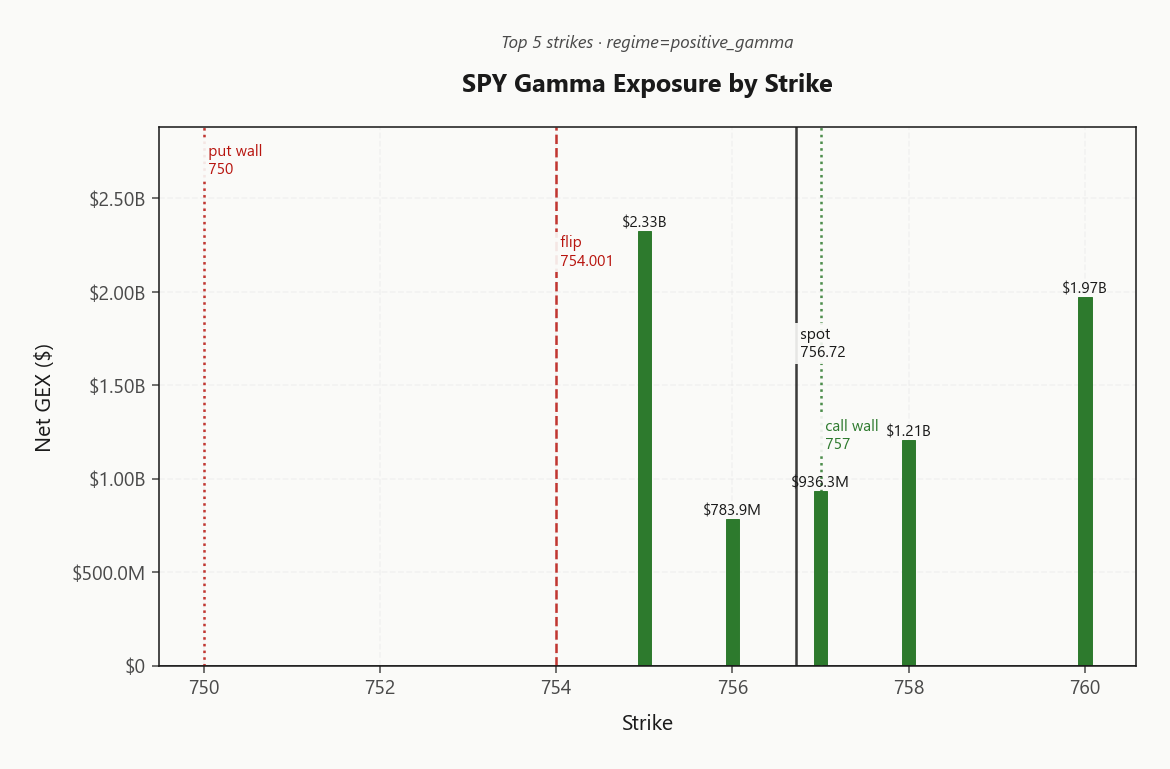

The strike map tells the story: highest OI parks at 550, a legacy anchor well below spot and no longer an active magnet. The live battleground sits at 755.00, where net GEX of $2.33B concentrates dealer long-gamma into a hard supply shelf.

With spot above the gamma flip at 754.00, dealer hedging flow runs with dips and against rips - the mechanical bid that has defined the tape. The call wall at 757.00 is THE level: every grind-higher attempt walks into dealer supply, and proximity is uncomfortably tight. The put wall at 750.00 backstops the session floor, framing a narrow, dealer-enforced corridor.

Trade the channel - fade strength into 757.00, accumulate into 750.00, and only abandon the mean-reversion playbook on a clean break of 754.00 on volume.

What it means for your trading

Dealer book is structurally supportive above 754.00 but capped by the 757.00 supply shelf - corridor trade, not a breakout setup.

Trading readHeavy positive gamma stacked at 755.00 and above into the call wall means dealers absorb supply on rallies - fade pushes into 757.00, expect mechanical bid below 750.00.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer vanna sits negative at -$291.48B - the cushion is conditional, not free. A vol spike from here forces dealers short delta, which would accelerate any downside print rather than dampen it. That is the asymmetry to respect: the positive-gamma anchor holds the tape calm, but the vanna axis is loaded to amplify, not absorb, the first real IV pop.

Trade the asymmetry: lean short premium while spot pins to the wall, but pre-stage downside wings - a tag through 757 on rising IV would invert dealer flow from suppressive to accelerative within a single session. Watch 754.00 as the regime-break trigger.

What it means for your trading

Vanna is the trap door: -$291.48B means any vol spike flips dealers into delta-selling, and with spot hugging the charm pivot at 757 only 0.0370017972 away, the cushion is thin enough to demand wings rather than naked premium.

Cross-Asset Confirmation

Bond vol is the tell: MOVE sits at 69.74, well inside any credit-stress threshold and entirely consistent with the equity complex's Positive Gamma posture. With Greed sentiment registering 60, positioning is leaning long without tipping into the euphoric zone that historically precedes vol expansion - exactly the tape where dealer suppression compounds.

Cross-asset confirmation is Aligned: SPY anchors against its walls while QQQ at 738.45 and IWM at 290.08 both hold positive_gamma regimes with spot above their respective flips. No index is leading the others into stress; the small-cap canary is quiet. Iran-framework headlines are trading as mean-revert noise rather than a credit-compounding catalyst - the bond market is not validating any tail bid.

Bottom line: every cross-asset channel is aligned with the short-vol thesis. Press iron condor structures; only reassess if MOVE pops or IWM cracks its flip first.

What it means for your trading

Bond vol calm at 69.74, sentiment at Greed, and aligned positive-gamma regimes across SPY/QQQ/IWM confirm a suppressive cross-asset backdrop with no credit signal contradicting the short-vol setup.

Scenario EV

Synthesis points to Iron Condor as the top-scoring structure at 54, beating the put spread at 40. The optimal tenor sits in 30-45 DTE - far enough out to harvest the forward curve where it flattens, close enough to capture the bleed from Contango term structure with VIX9D at 12.73 versus VIX3M at 18.79.

Why condors over naked strangles: VRP at 1.31% is constructive but not extreme, and the call wall at 757.00 caps any breakout - defined-risk wings are the right expression. Anchor the body between the put wall at 750.00 and the call wall, with VVIX at 85.85 flagging Low jump risk and Standard Size sizing appropriate.

VRP assessment Unknown - lean on the structural edge from Steep Contango and dealer suppression rather than chasing premium. Flip the thesis only on a gamma flip breach at 754.00.

What it means for your trading

Sell the Iron Condor in 30-45 DTE - best-scoring structure at 54, with defined wings respecting the 757.00 cap and 750.00 floor.

Actionable Summary

Trade structure: Iron Condor in the 30-45 DTE pocket, body anchored between the 750.00 put wall and 757.00 call wall. Sell calls into the 757.00 cap where dealer supply dampens breakout attempts, and accumulate longs near 750.00 where mechanical bid kicks in. VRP at 1.31% with VVIX at 85.85 signals Low jump risk - Standard Size is appropriate.

Avoid naked premium as VVIX bleeds and skip long gamma in the Elevated / Watchful regime - half-life of 15 sessions confirms persistence. Watch 757 for the dealer-bias flip; spot sits within 0.0370017972 of that Call Wall. Only flip bearish if spot breaches 754.00 on volume - below the flip, dealer flow becomes accelerant, not cushion.

What it means for your trading

Sell Iron Condor wings in 30-45 DTE around the wall corridor; the Elevated / Watchful regime rewards premium collection but the 757 pivot and 754.00 flip are the non-negotiable kill levels.

US-Iran framework progress is the single biggest macro tape catalyst today - a deal compresses oil-shock tail risk and reinforces the suppressive vol regime; collapse re-prices MOVE and SPY skew within hours.

Global bond vol whipsaw in May from Iran headlines is the reason MOVE was elevated earlier this month - current calm in MOVE is the credit signal that the worst tail has been priced out.

ECB research flagging compounding euro-zone consumer damage from the conflict is a reminder that a deal failure transmits via European credit before US equities - watch EU spreads as the early-warning channel.

Oil tumbling on ceasefire optimism while equities gain confirms the macro alignment supporting today's positive-gamma calm - directly underpins the short-vol thesis.

Reuters morning bid framing the day as another 'Iran deal moment' captures the binary headline-risk structure - explains why VRP is positive but VVIX is muted (event known, timing unknown).

Costco's lukewarm-but-OK print is a consumer-health read for the index; absent margin shock, it removes one near-term catalyst that could have rattled the gamma cushion.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.00 against a spot of 756.72. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.06% with a volatility risk premium of 1.31%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.37. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime