Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

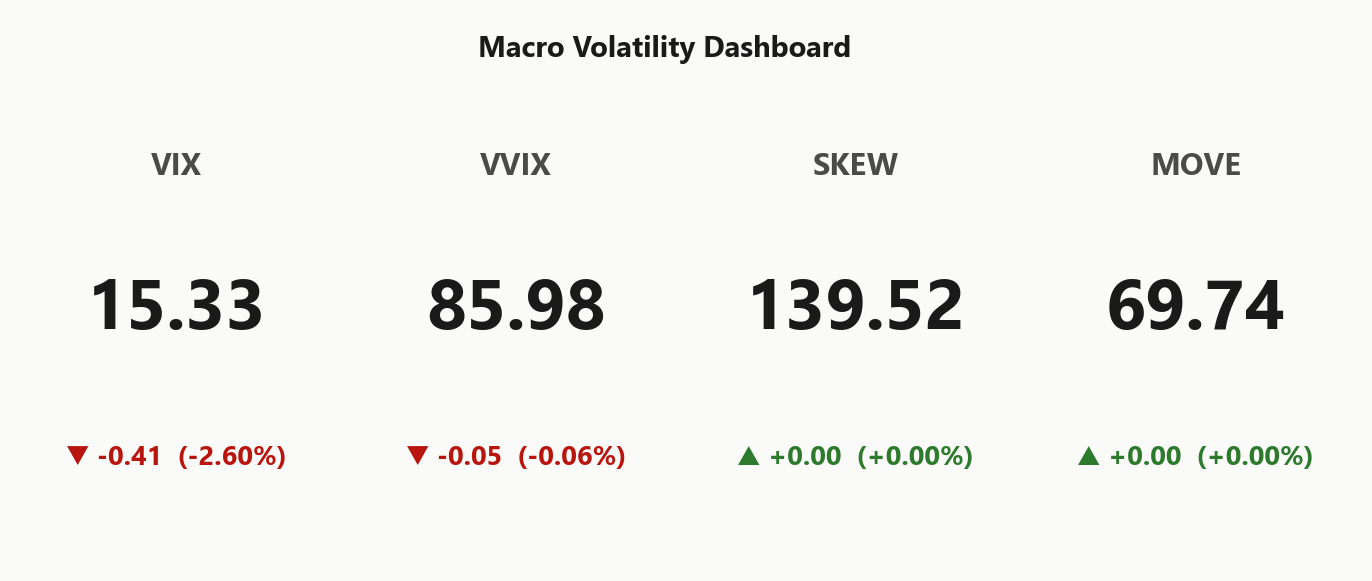

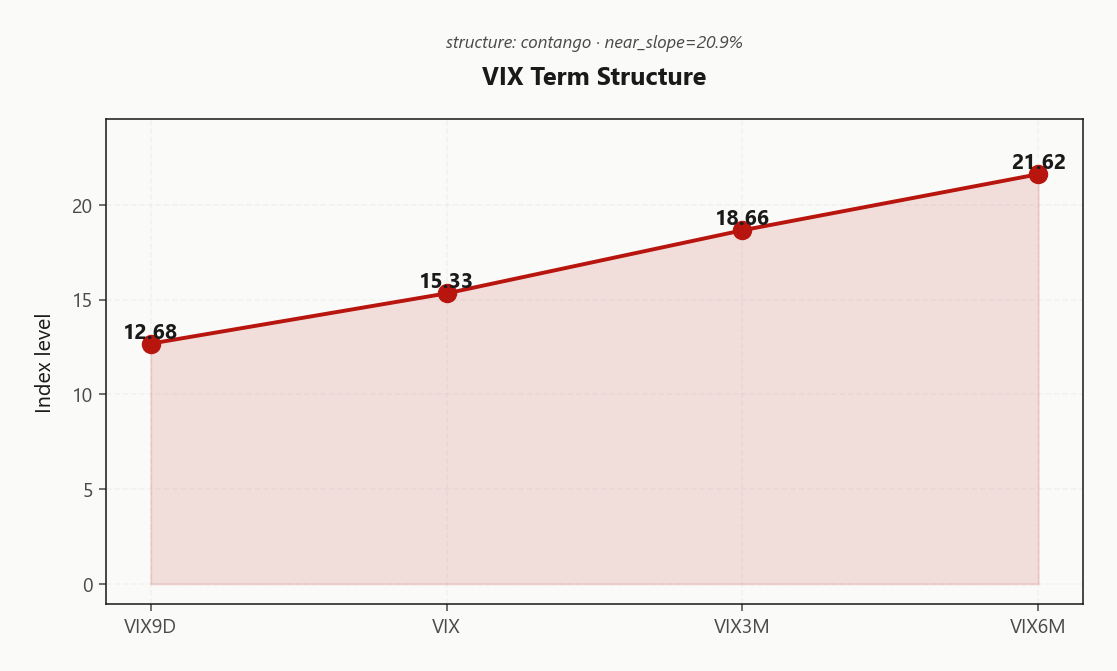

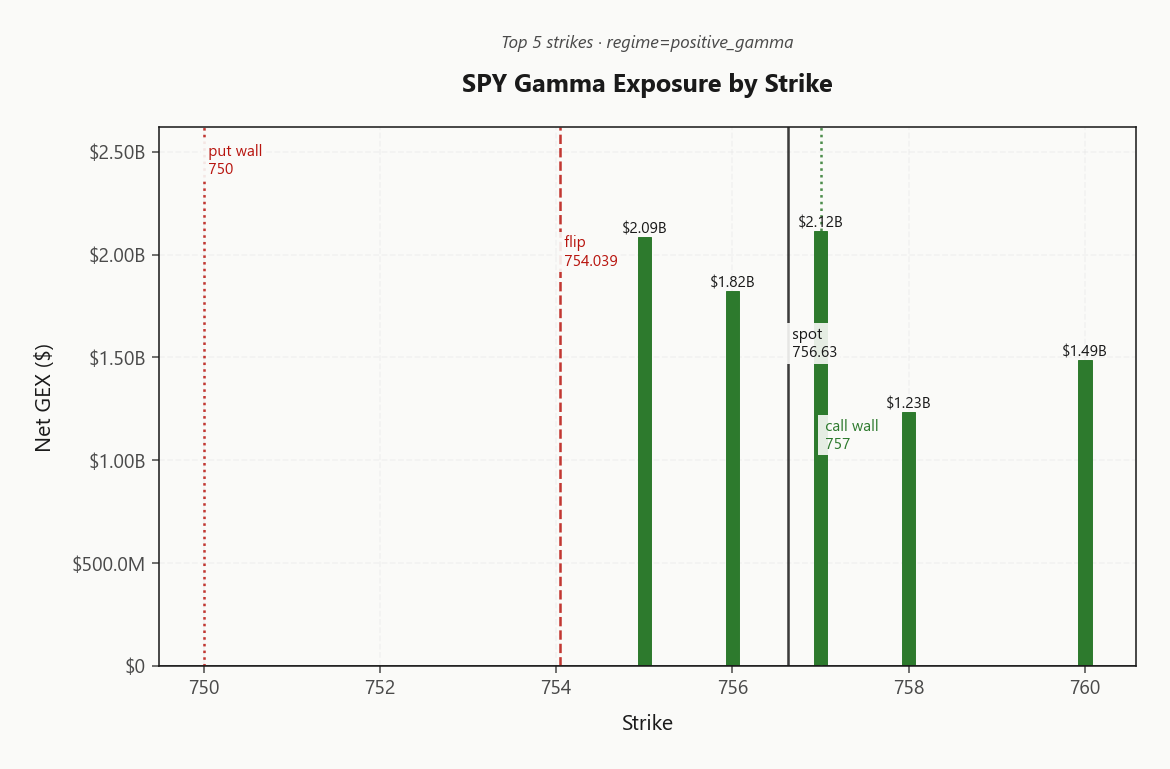

SPY closed at 756.63 in deep positive gamma with net GEX of $9.69B - dealers long gamma, mean-reversion dominates. Call wall sits at 757.00 (spot pinned within a stone's throw), put wall at 750.00, gamma flip at 754.04 - current spot sits roughly 0.0489010481% from the pivot, leaving a healthy cushion before flow flips amplifying. Dealer vanna at -$283.39B is meaningfully negative, meaning a VIX spike would force dealers to dump delta - the asymmetric risk in this regime. Charm at -$1.37B is mildly negative, modest decay-driven selling pressure into close. VIX at 15.33 (--2.6%%) with the curve in steep contango (Steep contango - vol sellers favored) and VVIX at 85.98 = vol sellers' paradise, no premium being paid for vol-of-vol. VRP at 0.49% is active but not extreme, with 0DTE gamma at 63.8%% of total. Bottom line: structured short premium - iron condors centered around 756.63 in 30-45 DTE is the highest-EV trade; fade strength into 757.00, buy weakness above 754.04, and avoid naked short vol given the negative vanna asymmetry.

Positive gamma across index complex with steep VIX contango - vol sellers favored, mean-reversion regime intact

SPY closed at 756.63 pressed against the call wall at 757.00, with dealers deeply long gamma and spot sitting comfortably above the 754.04 flip. VIX term structure remains in steep contango (20.9%% near slope) and VVIX at 85.98 signals no jump risk being priced. The setup rewards systematic vol harvesting in 30-45 DTE iron condors, with the 757 call wall as the upside magnet and 750.00 as the downside backstop.

Regime Assessment

Volatility sits in the Elevated / Watchful bucket with VIX anchored at 15.33 - not crisis, but not the sleepy floor either. The transition matrix puts the probability of escalating to panic over the next week at 0.05 while the odds of drifting back to a low-vol regime over two weeks sit near 0.45 - a near coin-flip for the carry to extend. Half-life of 15 sessions tells you the regime is sticky: the base case is more of the same, not a reversion in either direction.

Signal color reads Yellow - actionable but conditional. The Steep contango - vol sellers favored curve and VVIX at 85.98 validate the carry, yet net VEX at -$283.39B means a VIX repricing forces dealers to dump delta into the move. Harvest the slope, size to the Standard Size guidance, and keep a tail bid against 754.04 - the watchful posture is earned, not optional.

What it means for your trading

Regime is Elevated / Watchful with a sticky 15-session half-life - base case is the carry extends, but the 0.05 tail probability over five sessions is why this prints yellow, not green.

Trading readVIX, VVIX, SKEW, and MOVE are all in confirming-calm mode - no divergence between equity vol, vol-of-vol, tail skew, or rates vol. That's broadly bullish for short premium but tightens the wake-up call if any one starts to misbehave.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve is in Contango with a near slope of 20.9% - VIX9D at 12.68 against VIX at 15.33, then climbing through VIX3M at 18.66 to VIX6M at 21.62. That stack is paying forward vol sellers a real carry, and the absence of any front-end kink confirms no event premium is bid in the front month.

The forward 30-60 prints at 20.1193675348, materially above front spot - calendars and diagonals capture the slope cleanly, with the short leg rolling down a green-shaded curve while the back leg sits as a structurally cheap tail hedge. Regime label reads Steep contango - vol sellers favored; the configuration structurally favors systematic premium harvest in the near tenor, financed by owning back-dated convexity.

What it means for your trading

Curve geometry is unambiguous: Steep Contango from VIX9D through VIX6M means sell front, own back. The carry trade is live until the front end kinks - that is the single signal to monitor.

Trading readFront month 18.66 vs spot 15.33 = 21.72%% basis - vol carry trade is wide open, short front-month/long spot is the carry play.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 10.24% prints above HV20 at 9.75, leaving a modest but constructive VRP of 0.49%. Options are not screamingly rich, but they pay a positive carry - enough for systematic harvesters to keep collecting, not enough to warrant maximum sizing.

The structural tell is in the longer window: HV60 at 14.61 sits well above HV20 at 9.75, confirming realized vol has been decelerating into the close. With RV trending lower and no catalyst on the immediate tape, IV should follow - the path of least resistance favors continued mean-reversion and short-dated premium decay.

Trade implication: premium-to-realized still pays, but sized to the modesty of the spread. Stay disciplined on notional - VRP at 0.49% is active, not extreme, and the catalyst-free tape is what's keeping it that way.

What it means for your trading

VRP at 0.49% with decelerating HV20 versus HV60 keeps the short-premium carry trade live, but the modest spread argues for measured sizing rather than aggressive deployment.

Skew Convexity

The 1.58% quarter-delta skew prints ordered but unmistakably put-heavy: downside 8.68% sits well above the ATM 7.51%, while the call wing fades to 7.1%. Smile ratio at 1.22% codes the surface as skew_steep - a modest left-tail premium being paid, not a panic bid.

The flat call wing is the actionable read: no one is reaching for upside convexity, which reinforces the fade-strength logic against the 757.00 dealer cap. Combined with the muted 85.98 VVIX and Steep contango - vol sellers favored, there is no upside-chase to lean into and no jump-risk bid to fight.

At this skew geometry, naked puts overpay for the wing - debit put spreads through the 750.00 backstop monetize the steepness without paying full carry, and the short-call leg of a condor harvests the flat call wing cleanly.

What it means for your trading

Skew is ordered-steep on the put side at 1.58% with a flat call wing - fade rallies into 757.00 and finance downside via spreads, not outright puts.

Vol-of-Vol Structure

VVIX at 85.98 sits firmly in the low regime against VIX 15.33 - the tape is pricing zero jump risk and no binary hedging bid is showing up in the wings. The VVIX/VIX ratio at 5.61 confirms a calm vol-of-vol backdrop: dealers are not paying convexity premium, and the second-derivative tail is asleep.

Sizing follows the read - Standard Size is appropriate, full notional acceptable on systematic short-premium structures. The asymmetric risk remains net VEX at -$283.39B, so the trade is conditional on VVIX staying suppressed; any uptick in vol-of-vol typically leads VIX itself by a session, making it the cleanest early-warning gauge on the board.

Watch the VVIX print before the VIX print - that is the trigger to cut size, not the spot tape.

What it means for your trading

Vol-of-vol at 85.98 with VVIX/VIX at 5.61 greenlights Standard Size on short-premium books; treat any VVIX uptick as the lead signal to de-risk before VIX confirms.

Dispersion Spread

Index vol is trading cheap to its constituents: SPY ATM IV at 10.24% sits well below QQQ at 17.57% and IWM at 17.74%. That spread is the dispersion tell - correlation is moderate, not collapsing, so single-name risk premium isn't getting absorbed into the index print. Broad hedges aren't compensating for idiosyncratic tape.

The harvest hierarchy follows directly. QQQ VRP at 1.56% screens richer than SPY's 0.49% - that's the cleanest premium target in the complex. IWM VRP at -1.72% prints negative: realized is outrunning implied, and short vol there is a coin flip dressed as carry. Avoid small-cap premium sales.

Bottom line: express short vol at the index level, not through single-name dispersion. QQQ condors carry the best edge, SPY structures pin against the dealer walls, and small caps stay off the menu until that VRP turns positive.

What it means for your trading

Index ATM IV sits below QQQ and IWM with moderate correlation - favor index-level vol selling, with QQQ at 1.56% the richest harvest and IWM's negative VRP a no-go zone for short premium.

Liquidity & Microstructure

The book's center of gravity sits at 757.00, where $2.12B in net GEX acts as today's gravitational magnet. Legacy OI still anchors at 550, but that's stale tape - the active battle is fought inside the 750.00 to 757.00 corridor, a tight pinball zone where dealers will pin the close.

Spot sits above the 754.04 flip, putting dealer flow squarely in Positive Gamma: rallies supported into dips, capped firmly into the 757.00 ceiling where hedging supply intensifies. The 750.00 put wall provides the symmetric backstop - dealer buying defends that floor mechanically.

The pivot to respect is 757: lose it and the supportive bid inverts to amplification, with the same flow that's currently dampening flips chasing the move down. Fade strength into the wall, lean long above the flip, and treat any close beneath 754.04 as a regime change, not noise.

What it means for your trading

Dealers are long gamma with spot pinned inside the 750.00 - 757.00 corridor and 757.00 the magnet; the regime holds while spot stays above 754.04, inverts below.

Trading readMassive call-side gamma concentrated at 757.00 and the 757.00 cluster acts as a hard magnet today - dealers dampen any push higher and provide bid support down to 754.04. Below that flip, the same flow reverses and amplifies - that's the line traders are watching.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer net VEX at -$283.39B is the buried fault line under an otherwise placid tape. The exposure is deeply negative, meaning a VIX uptick mechanically forces the street to dump delta into weakness - the classic vanna accelerant that turns a benign vol pop into a directional cascade. Vanna read: Vol up = dealers sell delta - downside amplified if vol spikes. Until vol stays pinned, the cushion holds; the moment VVIX twitches, the asymmetry bites.

Charm is the quieter story. Net CHEX at -$1.37B sits modestly negative - measured decay-driven supply bleeding into the bell rather than a structural drag. Read: Time decay pushing dealers to sell - pressure into close. Enough to lean rallies, not enough to override the gamma magnet.

The pivot is surgical: 757 (Call Wall), with spot sitting 0.0489010481 away and bias tagged Neutral. Above, supportive flow persists and mean-reversion compounds; cross below and the same dealer book flips hostile - gamma amplifies, vanna accelerates, charm stops helping. One level, one regime switch.

What it means for your trading

Trade the regime, respect the asymmetry: harvest premium while spot holds above 757, but size for the vanna trapdoor - -$283.39B means naked short vol pays you pennies to assume catastrophic convexity if VIX breaks higher.

Cross-Asset Confirmation

Cross-asset tape confirms the equity vol read with no dissent. MOVE at 69.74 sits benign - rates vol is not flagging credit or duration stress, removing the most common transmission channel for an equity vol shock. Fear & Greed prints 61 (Greed), a modest bullish lean that earns a contrarian yellow flag but stops well short of the euphoric extremes that historically mark fade zones.

QQQ at 738.27 and IWM at 290.35 both sit in positive gamma alongside SPY - the regime read across the index complex is Aligned. No divergence between large-cap, tech, and small-cap dealer positioning means no asymmetric break risk to arbitrage and no early-warning crack telegraphing a regime flip. This is isolated equity calm reinforced by quiet rates vol, not the macro-shock setup where one asset class leads the others into stress.

What it means for your trading

Cross-asset confirmation is clean: MOVE at 69.74 and Aligned positive-gamma regimes across SPY/QQQ/IWM validate the short-vol thesis with no fragility leaking from rates or small caps. Fear & Greed at 61 is the only mild yellow flag - bullish enough to watch, not stretched enough to fade.

Scenario EV

The optimization stack lands on Iron Condor as the highest-EV expression, scoring 43 versus a put spread at 30 - neutral premium outranks directional because VRP carries but doesn't scream, and the dealer wall corridor between 750.00 and 757.00 hands you natural width without forcing the trade.

Target window is 30-45 DTE - far enough to harvest theta cleanly, short enough to recycle before charm pressure compounds, and well clear of the front-end gamma minefield. Wings sit at the dealer extremes: short the 757.00 call where dealer selling caps strength, short the 750.00 put where dealer buying defends weakness. Size to Standard Size - VVIX at 85.98 validates full notional.

The asymmetric risk is negative vanna at -$283.39B - defined-risk wings are non-negotiable here, naked strangles trade the carry for tail exposure you don't get paid for. Pivot to monitor: 757.

What it means for your trading

Iron condor at 30-45 DTE wings the dealer walls - short 757.00 call, short 750.00 put - sized Standard Size per the 85.98 VVIX read. Defined-risk only; negative vanna at -$283.39B makes naked premium the wrong vehicle.

Actionable Summary

Trade: deploy Iron Condor in 30-45 DTE - short call at 757.00, short put at 750.00. The dealer walls do the structural work; positive gamma keeps the corridor sticky and VRP at 0.49% pays the carry. VVIX at 85.98 green-lights Standard Size.

Watch: the charm pivot at 757 (Call Wall) is the regime line - a close below flips dealer flow from dampening to amplifying. Avoid naked short strangles: net VEX at -$283.39B is the asymmetric tail, a VIX pop forces dealer delta dumps against you. Also fade, don't chase, any push through 757.00 - dealer selling caps strength.

Hedge: cheap puts at 754.04 are a near-free tail given Elevated / Watchful conditioning and low vol-of-vol - optional, but the cost of insurance has rarely been this thin.

What it means for your trading

Highest-EV expression is a 30-45 DTE Iron Condor pinned to the 750.00/757.00 dealer corridor, sized standard given low VVIX. The trade is structurally short vanna - hedge or de-size if spot tests 757.

Iran deal headline risk is the lone wildcard in an otherwise sleepy vol regime - a breakdown reopens crude tail risk and could spike VIX out of contango fast.

Trump Friday meeting on Iran deal = binary event risk against a low-VVIX backdrop; consider cheap weekly puts as tail given how cheap optionality is right now.

ECB flagging Iran war as 'doubly scarring' to euro zone consumers = early signal that any deal breakdown leaks into rates and credit, not just equity vol.

AI capex / token economics framing matters because it reframes mega-cap earnings risk - relevant for NVDA, MSFT, META gamma positioning if the narrative cracks.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 754.04 against a spot of 756.63. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 10.24% with a volatility risk premium of 0.49%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.33. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime