Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

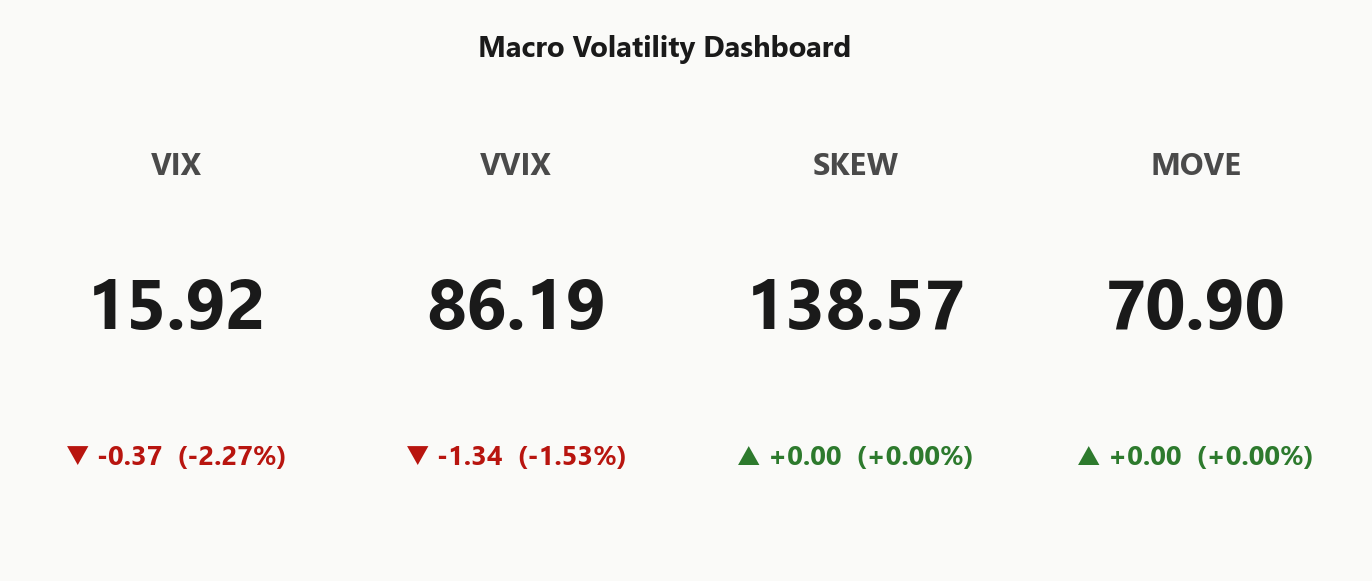

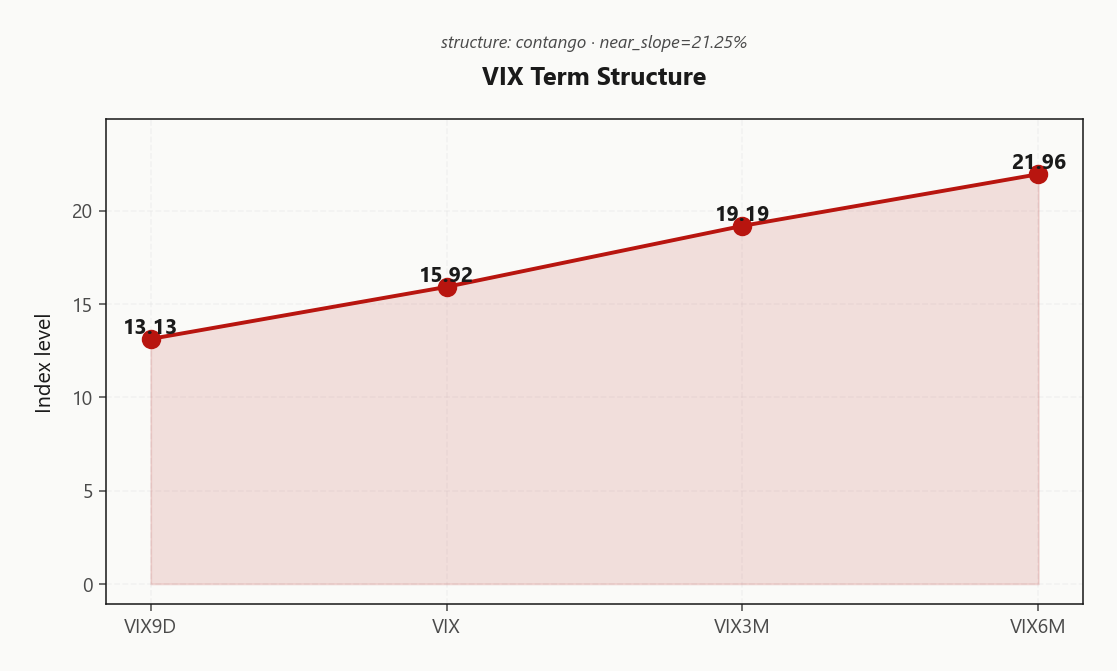

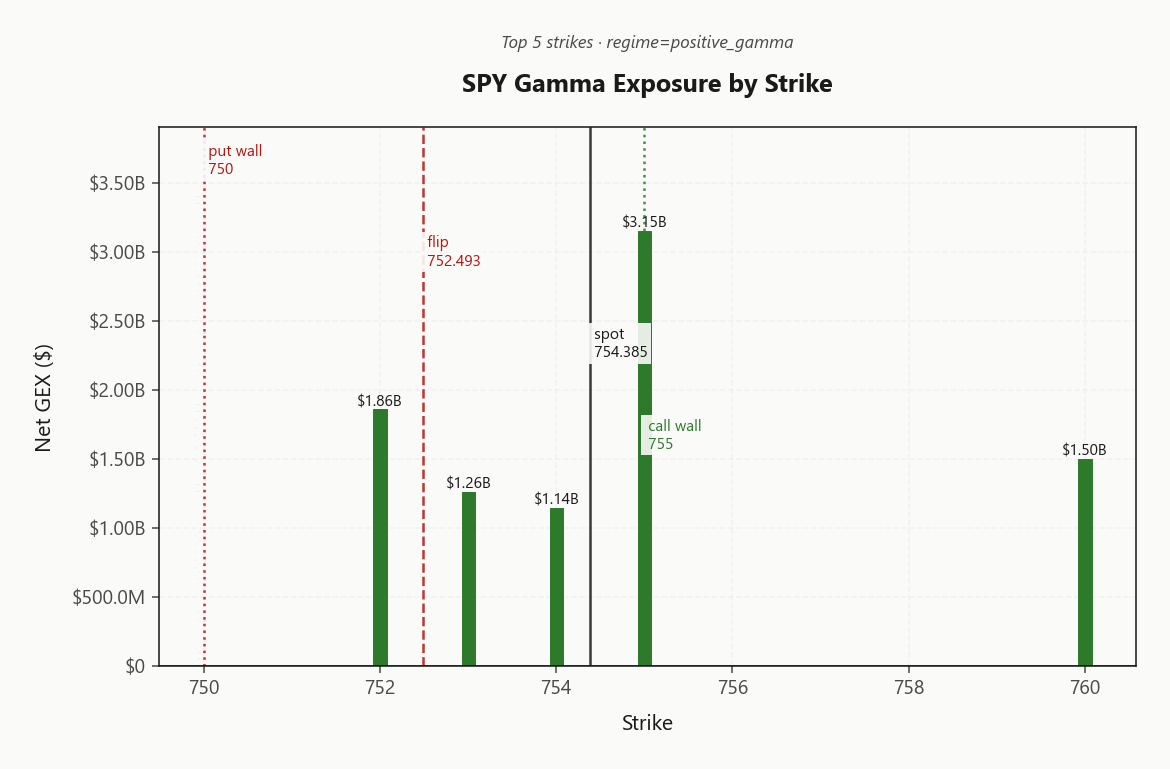

SPY at 754.39 sits firmly above the gamma flip at 752.49 with net GEX at $11.84B - a deep positive-gamma cushion that dampens intraday moves. Call wall at 755.00 caps upside, put wall at 750.00 backstops dips; the 755.00 strike concentrates dealer gamma and acts as the magnet into close. Dealers carry net DEX of $149.71B and net VEX of -$274.81B - meaning a vol spike forces delta selling (vanna accelerant lurking under the surface), while charm flow is mildly net seller into expiry. VIX at 15.92 with a steep contango term structure (13.13 / 15.92 / 19.19) - front-end vol is being paid down aggressively, VRP at 1.02% keeps premium sellers paid. VVIX at 86.19 is benign, sizing guidance is Standard Size. Zero-DTE accounts for 31.7% of total SPY gamma - meaningful, but not extreme. Bottom line: fade strength into 755.00, lean iron condors in the 30-45 DTE window, keep tail hedges live since VIX label is Elevated / Watchful not benign.

Positive gamma across index complex with Steep Contango term structure - mean-reversion regime intact

SPY trades at 754.39 with dealers long gamma and the gamma flip below at 752.49, framing a mean-reversion tape pinned beneath the call wall at 755.00. Steep VIX contango (Steep contango - vol sellers favored) and subdued VVIX at 86.19 green-light premium harvest, but elevated VIX label (Elevated / Watchful) warns the cushion is thinner than headline gamma suggests. Cross-asset signals align with no SPY/QQQ divergence - the day's risk is single-name idiosyncratic, not index-level.

Regime Assessment

Regime classification reads Elevated / Watchful with VIX at 15.92 - the dissonance with the index complex sitting in Positive Gamma is the trade's central tension. Positive dealer gamma is doing the heavy lifting on intraday tape, but the absolute vol level keeps the regime tagged watchful rather than benign; the cushion exists, the all-clear does not.

Persistence is the structural feature. Half-life prints 15 sessions, anchoring the elevated/watchful classification through the next couple of weeks barring an external catalyst. Transition probability to panic over a five-session horizon sits at 0.05 - low, not zero - while drift to a low-vol regime over ten sessions runs 0.45, the more probable migration path.

Read-through: the carry trade has multi-week runway. Premium harvest, calendars, and condors in the 30-45 DTE window remain the structurally favored book, but tail hedges stay live - watchful means the regime can re-rate faster than the gamma cushion suggests if VIX expands off its base.

What it means for your trading

Regime is Elevated and sticky at 15-session half-life - carry trade has runway, but the Elevated / Watchful tag demands tail hedges remain in place.

Trading readVIX low, VVIX benign, SKEW elevated, MOVE quiet - three of four point to calm, SKEW alone whispers tail demand. No confirming cross-asset stress, but tail hedges remain cheap insurance.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward 30-to-60 implied prints 20.6315522925 against forward 60-to-90 at 24.4177619777 - the slope from 19.19 into 21.96 is where the carry lives, and it pays sellers to sit. Forward vol cleanly north of spot VIX means the curve is not pricing near-term stress; it is pricing the option to be wrong later, cheaply.

Operationally, calendars selling front-month against 30-45 DTE capture both roll-down and slope, and the same window anchors the recommended Iron Condor at score 52. Regime Steep Contango - front of the curve is the cheapest seat.

What it means for your trading

Steep contango from 13.13 through 21.96 green-lights structural vol carry, with the 30-45 DTE pocket optimal for premium harvest via calendars or the recommended Iron Condor.

Trading readSteep contango end-to-end - vol-carry trade has runway. Market is not pricing imminent stress; calendar and condor sellers paid to wait.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The realized-vol structure hands sellers a clean edge. SPY ATM IV at 11.1% prints materially rich to HV20 at 10.08, with VRP at 1.02% - options are being paid a premium the tape is not delivering. The HV20-below-HV60 configuration (10.08 vs 14.64) confirms realized is decelerating, not catching down to a prior spike - a structural tailwind for premium harvest rather than a base effect.

QQQ runs richer on the same axis with VRP at 2.27% - wider than SPY and the sharper book to be short. The cross-index spread argues a Nasdaq-tilted vol-selling sleeve over an index-neutral one, with SPY held as the residual leg. Posture: short vol within regime sizing, with QQQ carrying the heavier weight.

What it means for your trading

IV pays a clean premium over decelerating realized across the index complex, with QQQ VRP at 2.27% outpacing SPY at 1.02% - lean short vol, tilt Nasdaq.

Skew Convexity

Quarter-delta put skew prints 1.44% with the smile ratio at 1.13% - wings are paying, but the left tail is ordered, not panic-bid. Put quarter-delta IV runs at 12.88% against an ATM print of 11.7%, while call quarter-delta sits at 11.44% - flat to ATM, signaling zero upside convexity bid. Classic carry-regime skew: hedgers paying for downside, no one chasing calls.

The slope geometry argues for spread protection over naked tails. With put wings bid but smile ratio shy of a convex blowout, put spreads finance cleanly against the steeper inside-the-money leg - the skew is paying you to give back the deep tail. QQQ skew runs steeper than SPY, consistent with mega-cap idiosyncratic risk concentration; the Nasdaq book carries the sharper tail premium and the better short-skew expression.

Bottom line: skew steepness yellow, not red. Sell index call wings into the ATM-flat call skew, monetize put-spread structures rather than naked downside, and lean QQQ over SPY for any explicit skew-flattener expression.

What it means for your trading

Quarter-delta skew at 1.44% with smile ratio 1.13% is ordered hedge demand, not crisis bid - favor put spreads over naked puts and lean QQQ for the sharper skew expression.

Vol-of-Vol Structure

VVIX prints 86.19 against VIX at 15.92 - a Low vol-of-vol read that sits comfortably below the jump-risk threshold the desk watches for bimodal pricing. No convex stress in the second-moment surface; the market is not paying up for a vol-of-vol spike, which means the front-end carry trade isn't carrying hidden gap risk.

The 5.41 VVIX/VIX ratio screens optically elevated, but that's a denominator artifact - a depressed VIX inflates the ratio without signaling jump demand. Read the absolute VVIX level, not the quotient: dealers are not bidding vega convexity, and skew of vol is flat enough that calendar and condor structures don't need a tail premium baked in.

Sizing follows the signal: Standard Size. No haircut on premium-seller structures, conviction trades take full risk units, and the iron condor book at the 30-45 DTE window runs without a vol-of-vol overlay. Tail hedges stay live on regime grounds - Elevated / Watchful - not because VVIX is flashing.

What it means for your trading

Vol-of-vol is benign at 86.19 - green light for Standard Size on premium-harvest structures, with the elevated VVIX/VIX ratio at 5.41 a denominator illusion rather than a jump-risk warning.

Dispersion Spread

Index vol is the cheap seat. SPY ATM IV at 11.1% sits markedly below the single-name complex - QQQ alone prints 18.35%, and the cross-strike IV dispersion at 72.15 confirms the spread is wide enough to monetize. Correlation regime reads Moderate: index moves are being dampened by offsetting single-name flows, exactly the configuration where dispersion books earn carry.

QQQ VRP runs richer than SPY VRP - mega-cap concentration is the lever. The cleanest posture is short index vol against opportunistic long single-name gamma, with the top-mover stack (AAPL, TSLA, META) the natural pool for idiosyncratic vol expansion. Cross-asset tape is Aligned, so today's risk is single-name, not index-level - directly favorable to the spread.

What it means for your trading

Sell index vol via SPY/QQQ structures, stay long select single-name gamma in the mega-cap movers - the dispersion spread is paying with regime tagged Moderate and cross-asset signals Aligned.

Liquidity & Microstructure

The gamma map is dominated by a massive OI cluster at the 755.00 call wall, with the top strike at 755.00 carrying $3.15B of dealer gamma - the magnet into the close. Spot sits just above the gamma flip at 752.49, so dealer hedging is supportive on dips but the buffer is thin, not deep. Highest OI at 700 sets the longer-term anchor, but today's tape is governed by the top-three strike cluster that warehouses the bulk of dealer GEX.

Operationally: call wall 755.00 caps upside and rewards fades; put wall 750.00 backstops dips and anchors condor short legs. Cross-asset regime is Aligned - no index-level lead divergence to override the microstructure read.

The trade-killer is a clean break of 752.49. Below the flip, the regime inverts from dealer-stabilizer to dealer-amplifier and intraday realized expands meaningfully. Watch it as a hard line, not a soft level.

What it means for your trading

Deep positive-gamma cushion with the 755.00 strike as the dominant magnet - mean-reversion tape between 750.00 and 755.00 until 752.49 breaks.

Trading readMassive dealer-long gamma stacked at the call wall - spot pinned beneath it means dealers buy dips and sell rips, supporting mean reversion until spot pierces the gamma flip below.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Beneath the headline positive-gamma cushion, the second-order book tells a sharper story. Net VEX at -$274.81B is deeply negative - a coiled vanna accelerant that flips dealers into delta sellers the moment IV expands. Today's calm is conditional: gamma anchors spot while vol stays bid down, but any uptick in implied forces mechanical supply into the tape, and the cushion thins faster than the GEX number suggests.

Charm prints modestly negative at -$471.1M, biasing dealer flow to the sell side as time decays into expiry - mild close pressure, not a cliff. The directional switch sits at the charm pivot of 755, coincident with the Call Wall. A clean break above unlocks vanna-and-charm-driven upside acceleration as dealers chase; failure there bleeds the tape lower on charm drift toward the flip at 752.49.

Current bias reads Neutral - trade the range, not the breakout, until the pivot resolves.

What it means for your trading

Vanna is the lurking risk, not gamma: a vol pop forces dealer delta supply at -$274.81B sensitivity. Watch 755 - that's the level that decides whether charm becomes a tailwind or a drag into the close.

Cross-Asset Confirmation

Cross-asset tape confirms the index-level read: MOVE at 70.90 sits in benign territory, ruling out a rates-vol shock as the marginal driver. QQQ at 735.64 and IWM at 292.24 both hold Positive Gamma alongside SPY - no lead-lag divergence, no small-cap crack telegraphing risk-off. VIX itself sits in Negative Gamma, the textbook complement that keeps vol sellers in the driver's seat.

Fear & Greed prints Greed at 61 - a contrarian yellow flag against chasing strength, but well short of the extreme greed band that historically precedes sharp reversals. Regime divergence reads Aligned; the index complex moves as one block.

Operationally: this is a single-asset equity carry tape. The day's tail risk is single-name idiosyncratic - watch the AAPL/NVDA gamma migration - not a cross-asset contagion vector. Premium harvest stays on; tail hedges remain the cheap insurance, not the trade.

What it means for your trading

Cross-asset signals confirm a coherent positive-gamma index block with no rates or credit stress contaminating the equity carry trade. Fade strength into the call wall and keep the iron condor book on; the F&G Greed reading is a sizing nudge, not a regime warning.

Scenario EV

The regime stack scores Iron Condor at 52 versus a put spread alternative at 38 - a clean win, not a coin flip. Positive gamma cushioning spot above 752.49, steep contango from 13.13 through 21.96, and a benign VVIX print at 86.19 form the textbook condor backdrop: mean-reverting tape, decaying front vol, no jump premium to fight.

The 30-45 DTE window is where theta-to-gamma geometry inflects in the seller's favor - short enough to harvest the steepest part of the term slope, long enough to dodge the 0DTE whip. Anchor the wings at 755.00 and 750.00; dealer flow does the fence-building for you. VRP at 1.02% pays the carry; QQQ at 2.27% pays sharper if you want the second leg.

Sizing is Standard Size - no VVIX haircut required, but the regime label remains Elevated / Watchful, so keep tail hedges live and respect the charm pivot at 755.

What it means for your trading

Iron condor in the 30-45 DTE window is the structurally favored trade - score 52 with walls at 755.00 and 750.00 providing natural fences. Standard size, tails live, watch the flip at 752.49.

Actionable Summary

Primary trade: iron condor SPY in the 30-45 DTE window, strikes anchored at the 755.00 call wall and 750.00 put wall. Positive gamma cushion plus Steep contango - vol sellers favored and benign VVIX at 86.19 make this the textbook premium-harvest setup - Iron Condor scored 52 versus put spread alternatives.

Fade rallies into 755.00 - dealers pinned long gamma at that strike sell rips mechanically, and the charm pivot at 755 is the directional switch. Hold the call wall, drift sideways; break above it, vanna and charm flip from headwind to accelerant.

Do not get cute with naked tails. Regime label is Elevated / Watchful, not benign - VIX at 15.92 keeps the cushion thinner than headline gamma suggests. Size Standard Size. Watch the gamma flip at 752.49 - a print below flips the tape from dampener to amplifier.

What it means for your trading

Sell defined-risk premium in the 30-45 window framed by 755.00 / 750.00, fade into the call wall, and treat a break of 752.49 as the line that voids the trade.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 752.49 against a spot of 754.39. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.1% with a volatility risk premium of 1.02%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.92. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime