Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

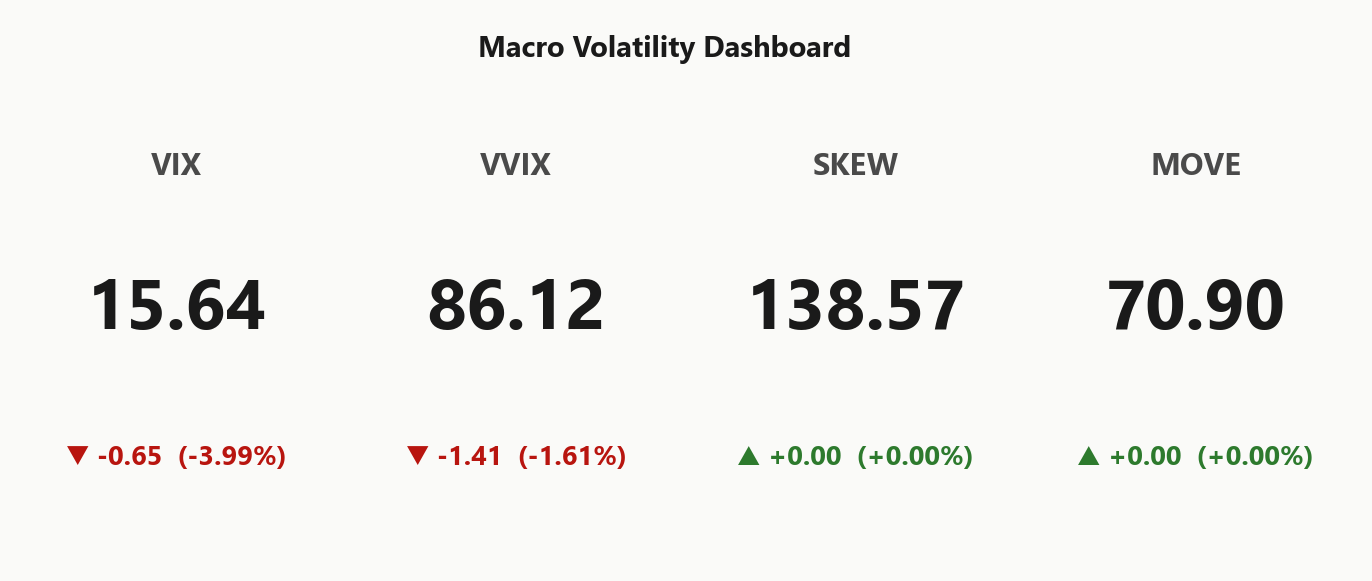

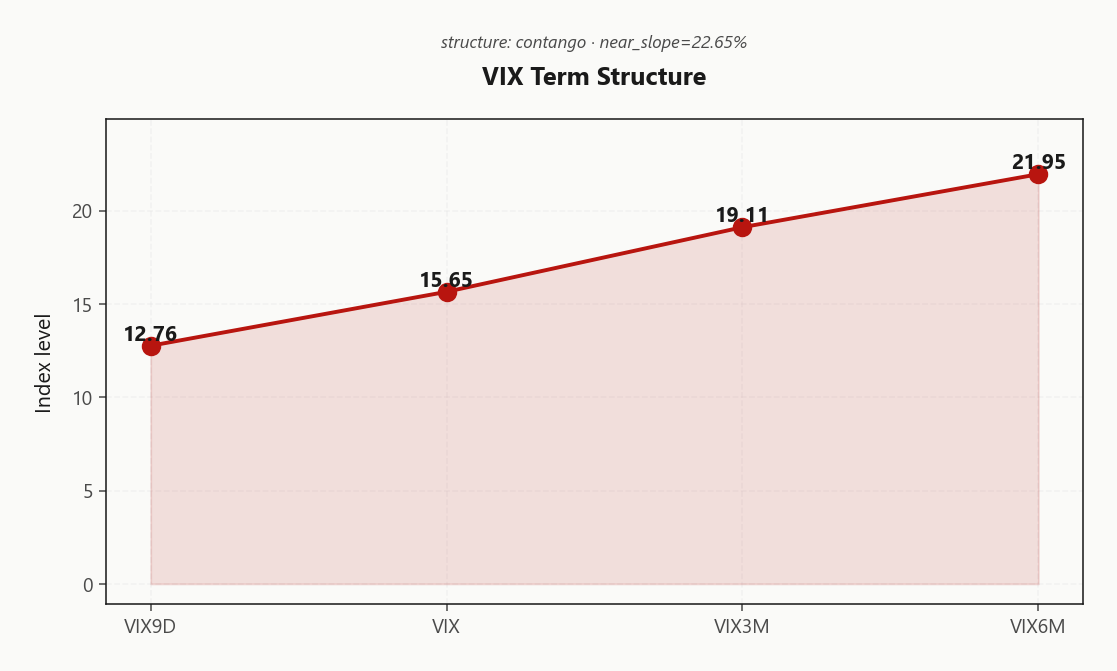

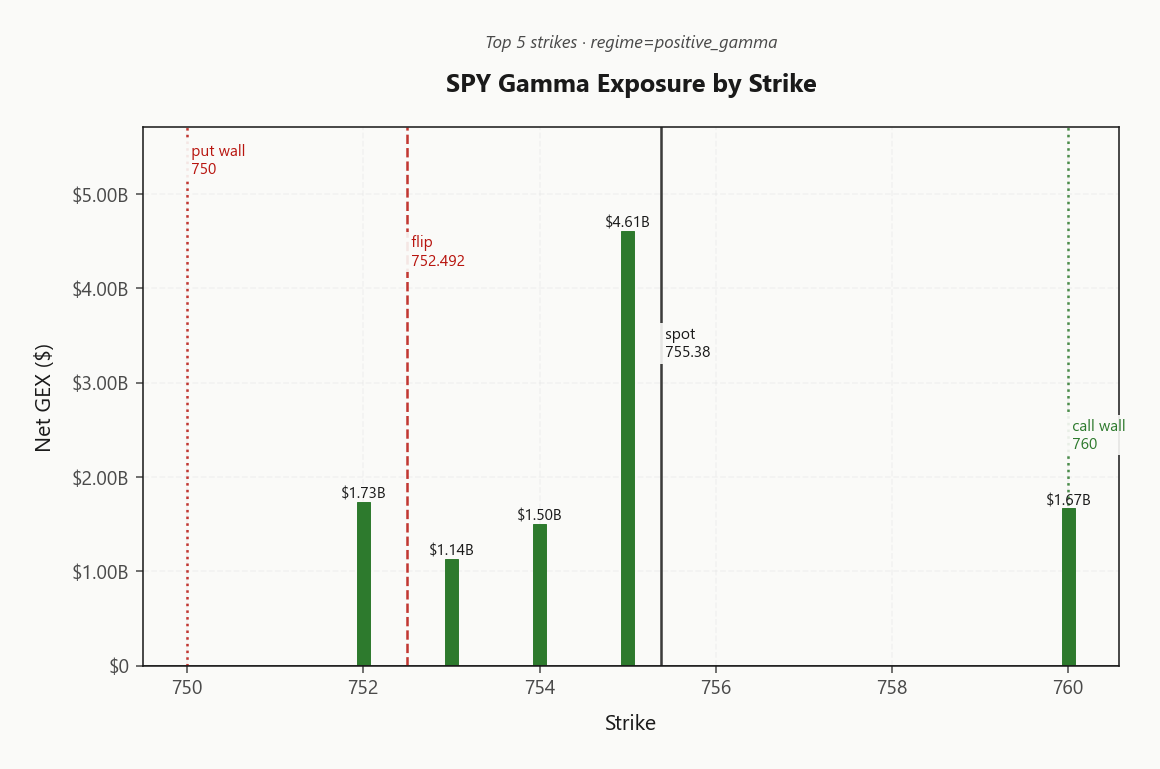

SPY closed at 755.38 in a deep positive gamma regime with net GEX of $14.41B - dealers are long gamma and dampening every move. Key levels: call wall 760.00 above, put wall 750.00, gamma flip 752.49 - spot is -0.3822652435 above flip, a meaningful cushion. Dealer vanna at -$278.43B means a vol spike pushes them to sell delta (downside accelerant), but with VIX at 15.64 and bleeding lower the vanna risk is dormant. Charm at -$1.37B is mildly negative - slow delta sell into close, not panic. Vol read: VIX9D 12.76 → VIX 15.65 → VIX3M 19.11 is textbook steep contango (22.65%% slope), VRP 1.39% vol points rich. VVIX at 86.12 confirms no jump-risk premium being paid. Bottom line: Iron Condor in the 30-45 window is the scored-best structure - sell the wings, respect 760.00 and 750.00 as the box.

Positive gamma across index complex with steep VIX contango - vol sellers favored, mean reversion wins

Index complex closes in synchronized positive gamma with SPY 755.38 sitting comfortably above the 752.49 flip. VIX at 15.64 compressing into a steep contango while VVIX stays subdued at 86.12 - dealer suppression mechanics fully engaged. Vol sellers carry the edge, but skew remains paid on the put side, so naked short premium needs structure.

Regime Assessment

The composite regime reads Elevated / Watchful with VIX anchored at 15.64 - not the all-clear, but a long way from stress. Transition mathematics favor the carry side: probability of escalating to panic over the next five sessions sits at 0.05, while the path to a lower-vol state over ten sessions runs materially richer at 0.45. Asymmetric drift is downward in vol, not upward.

Half-life of 15 sessions defines the window - multi-week, not multi-day, but not a permanent fixture either. The complex confirms: SPY, QQQ, and IWM all post Aligned positive gamma with VIX term structure in Steep Contango, and vol-of-vol sizing reads Standard Size.

Implication: stagger expiries across the 30-45 belly rather than lump premium in a single tenor - ride the half-life, don't bet it. Lean into Iron Condor while the watchful label holds, but keep a roll plan ready once the to-low path resolves.

What it means for your trading

Regime label is Elevated / Watchful with a low 0.05 panic probability and a richer 0.45 path to lower vol - short-vol carry has runway, but stagger tenors across the 30-45 window rather than concentrating in one expiry.

Trading readVIX down, VVIX down, MOVE flat, SKEW steady - all four confirming each other in a benign vol regime; divergence between them would be the warning, and there isn't one.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The vol curve prints Contango from front to back: VIX9D at 12.76 sits well under spot VIX at 15.65, with VIX3M extending to 19.11 and VIX6M anchoring the back at 21.95. Near-slope of 22.65% across the front leaves no room to argue the tape is pricing imminent event risk - the regime reads Steep Contango, the classifier flags Steep contango - vol sellers favored, and that is the signature of a market funding short vol, not defending it.

The structural carry lives in the back half of the curve. With forward 30-to-60 implied at 20.6234550937, the term spread between VIX3M and VIX6M finances itself in the 30-90 DTE window - calendars long the back are paid by the front roll-down, and convexity is cheapest to short in the front belly where VIX9D-to-VIX gap is widest. That is where the edge concentrates: front-belly short premium harvests the steepest roll while leaving the back of the curve as the natural hedge.

No backwardation print means no need to defend short books or pull risk. The carry trade is open; size to the regime, not against it.

What it means for your trading

Steep Contango with VIX9D at 12.76 under spot VIX at 15.65 validates the vol-seller regime - front belly is the highest-edge short, back of the curve provides the natural offset, no defensive posture required while contango holds.

Trading readTextbook contango 22.65%% near-slope - vol carry trade is open for business; backwardation would be the warning sign and it's nowhere on screen.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 11.48% sits modestly above HV20 of 10.09, leaving 1.39% vol points of carry on the table - paid, but not begging. HV60 at 14.65 remains elevated versus the cooled twenty-day print, telling us recent tape compression hasn't fully bled into implieds yet. That's the active edge: options are still pricing memory of a hotter regime while spot grinds in a dampened corridor.

The twenty-day VRP at 1.39 with percentile rank 23 reads as sustainable carry rather than euphoric premium - rich enough to harvest, not stretched enough to fade. With the gamma flip cushion holding and VVIX subdued at 86.12, the 30-45 DTE window is where theta dominance meets the steepest IV decay - the structural sweet spot for short-vol carry.

What it means for your trading

IV-RV gap is paid and stable: ATM at 11.48% over HV20 at 10.09 with VRP percentile 23 makes 30-45 DTE the cleanest window to monetize the carry.

Skew Convexity

The smile is doing the talking: 12.21% on the put quarter-delta sits above 12.56% at the money, while the call quarter-delta prints 11.33% - downside hedges are being paid, upside is being given away. The skew measure at 0.88% with a smile ratio of 1.08% reads as ordered steepening, not the convex panic curl you get when the tape is hunting a stop.

That asymmetry is the trade. With a smile ratio above unity, a symmetric short straddle gives up the put richness for free. Construct the condor with wider put wings inside the 750.00 floor and tighter calls outside the 760.00 magnet - let the call spread finance the puts rather than paying the steep skew naked. Above the 752.49 hinge, dealer suppression keeps the put bid honest without letting it run away.

What it means for your trading

Put skew bid, call skew flat, smile ratio above one - the carry is in the wings, but only if you respect the asymmetry by building the condor put-spread-wider rather than selling premium symmetrically into a one-sided smile.

Vol-of-Vol Structure

VVIX prints 86.12 against spot VIX at 15.64 - a ratio of 5.51 that sits squarely in the standard band, nowhere near the panic zone where vol-of-vol bids signal bimodal jump pricing. The tape is not paying for gap risk, it is paying for carry.

With derived vol-of-vol flagged Low, there is no premium being demanded for tail convexity - a clean vol-seller environment where the second moment of vol is itself suppressed. Combined with steep contango and an aligned cross-asset regime (Aligned), the jump-risk channel that normally forces defensive trim is dormant.

Sizing guidance reads Standard Size - full book weight on premium-selling structures, not the half-size defensive posture that a bid VVIX would mandate. The VVIX cushion is the green light to deploy the iron condor at standard notional rather than scaling down for phantom convexity risk.

What it means for your trading

VVIX at 86.12 with a VVIX/VIX ratio of 5.51 confirms no jump premium is being paid - deploy short-vol structures at Standard Size, not a defensive trim.

Dispersion Spread

Index vol sits cheap to the single-name complex - SPY ATM IV at 11.48% prints well under the cross-strike dispersion read of 75.54, the structural tell that correlation suppression is doing the heavy lifting. Cross-expiry dispersion at 3.32 confirms the term surface is orderly while single names carry the convexity premium. Index hedges stay cheap precisely because the constituents aren't moving together.

Trade expression follows the geometry: short SPY vol where the carry is paid against a suppressed correlation tape, not single-name premium where you collect richer theta but underwrite earnings-gap and idiosyncratic-headline risk that won't smooth into the index. Pair the short index leg with selective single-name put ownership - the names mapping into today's mega-cap GEX shift cluster, where dealer flow is Aligned across the complex but a single gap rewrites the dispersion math.

Net: harvest the index/single-name spread through SPY structures and reserve premium-spend for downside optionality in the dispersion sources, not the index itself.

What it means for your trading

Index IV at 11.48% versus cross-strike dispersion of 75.54 keeps the dispersion carry alive - sell SPY vol, own single-name tail.

Liquidity & Microstructure

The strike map is doing the heavy lifting today: 755.00 carries the heaviest net gamma in the book at $4.61B, sitting effectively on top of spot and acting as the magnetic center for dealer rebalancing flow. The corridor between the 750.00 put wall and the 760.00 call wall is the tradeable box - fade strength into the upper rail, fade weakness into the lower, and let the pin do the work.

Note the 700 highest-OI strike sits well beneath spot - legacy positioning, not a fresh directional bet, so don't read it as a magnet. The active gravity is the top-gamma cluster, not the stale OI peak. Above the 752.49 flip, dealer flow buys dips and sells rips; that mechanic stays intact while spot holds the cushion.

The flip is the single hinge. Break it and suppression flips to acceleration - until then, the book is structurally short volatility on your behalf.

What it means for your trading

Top gamma strike at 755.00 is the active pin; trade the 750.00 - 760.00 box and treat 752.49 as the regime line.

Trading readDealers are long gamma straight through the 750.00 - 760.00 corridor - fade strength into the wall, fade weakness into the floor, and avoid chasing breakouts until spot decisively breaches 752.49.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer vanna sits deeply negative at -$278.43B - the textbook downside accelerant lying dormant under a bleeding VIX. The mechanic: Vol up = dealers sell delta - downside amplified if vol spikes. While vol grinds lower the book stabilizes; a sharp VIX pop reverses dealers from suppressors to forced sellers into weakness. This is the asymmetric hostage on an otherwise constructive tape.

Charm reads -$1.37B - modestly negative, an orderly time-decay drag rather than panic delta-shedding. Expect a slow lean lower into the bell, not a flush. The single hinge level is the gamma flip at 752.4924448034: above it dealers stabilize, below it they amplify. Spot currently carries a -0.3822652435 cushion, leaving the bias Supportive.

Trade the regime, respect the trapdoor: gamma cushions today, but vanna defines the break risk if VVIX wakes up.

What it means for your trading

Vanna at -$278.43B is the dormant accelerant - supportive while spot holds its -0.3822652435 cushion above the 752.4924448034 flip, but a vol spike flips dealer flow from stabilizer to seller. Charm at -$1.37B signals orderly close-of-day drift, not stress.

Cross-Asset Confirmation

The cross-asset tape is Aligned and uneventful - exactly the backdrop short vol wants. MOVE at 70.90 sits flat and unloved, meaning rates vol is not bidding for a macro tape bomb; without a rates impulse, the equity vol surface has no external accelerant to repricing.

QQQ closes at 736.18 and IWM at 292.21, both anchored in Positive Gamma alongside SPY - mega-cap and small-cap dealer books pulling in the same suppressive direction. No idiosyncratic index stress, no dispersion blow-out fighting the index pin. VIX in its native Negative Gamma posture is normal furniture for the vol product, not a warning.

Sentiment reads Greed at 60 - leaning with the regime rather than fading it, which is the one yellow flag worth tracking; greed is fuel, and contrarian risk compounds the longer it persists. For today the confirmation is clean: complex Aligned, vol-carry green-lit.

What it means for your trading

Equity-vol-carry day, not a credit or rates shock - Aligned index regimes with MOVE at 70.90 clear the path for premium selling. Greed at 60 is the lone watch-item: ride the carry, but keep tail hedges cheap while sentiment is this committed.

Scenario EV

The scoring engine ranks Iron Condor as the dominant structure at 44, well clear of the put spread at 31. Positive VRP at 1.39%, VVIX bedded down at 86.12, and a Steep Contango term structure stack the theta-vega-vanna math cleanly in favor of premium sellers.

Park the structure inside the 30-45 DTE window - the carry sweet spot where front-belly convexity is cheapest to short and time decay outruns the residual vanna exposure. Anchor the short wings outside 750.00 and 760.00, lean the call side wider to monetize the asymmetric skew, and run standard book weight - VVIX at Low does not warrant defensive trim.

Avoid directional put spreads chasing a downside the regime is actively fading, and skip naked strangles where the vanna pocket below 752.49 remains the asymmetric break risk.

What it means for your trading

Iron condor at 44 is the scored-best expression of positive VRP, subdued VVIX, and Steep Contango term structure - deploy in the 30-45 window with wings outside the 750.00 - 760.00 box.

Actionable Summary

The book scores Iron Condor in the 30-45 DTE window as the cleanest expression of today's regime - short wings outside the 760.00 call wall and 750.00 put wall, sized standard book weight while VVIX holds at 86.12. The Elevated / Watchful tape with positive VRP and steep contango funds the structure; the wings respect dealer gravity rather than fighting it.

The single hinge is 752.4924448034 - break below the flip and dealer flow inverts from suppressive to accelerant, so manage the trade against that level, not against ticks. AVOID directional put spreads paying up for steep skew to fade a regime that is intact, and AVOID short single-name vol where dispersion still compounds gap risk. Express the carry through the index, keep the structure on, and let theta work into the 15-session half-life window.

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 752.49 against a spot of 755.38. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.48% with a volatility risk premium of 1.39%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 15.64. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime