Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

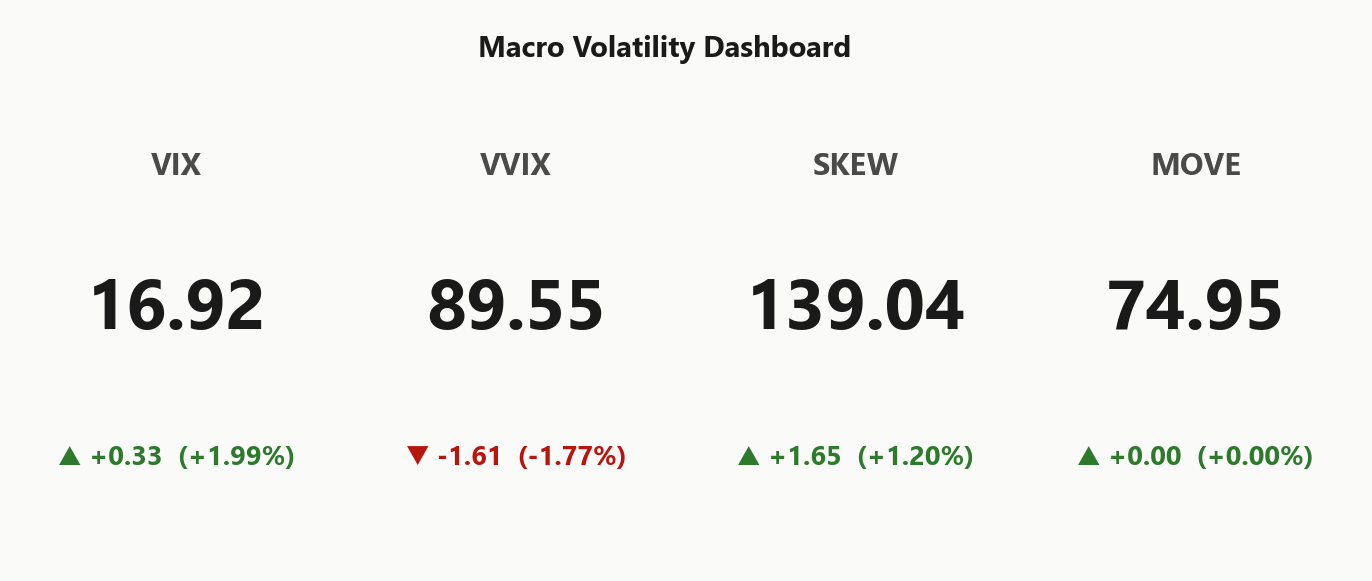

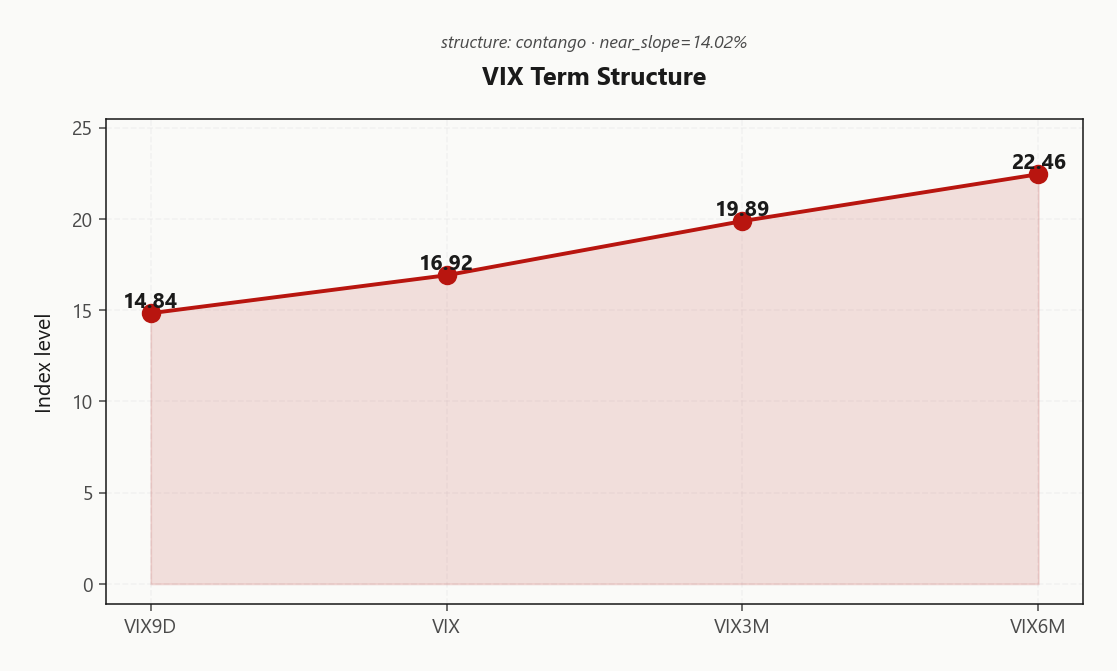

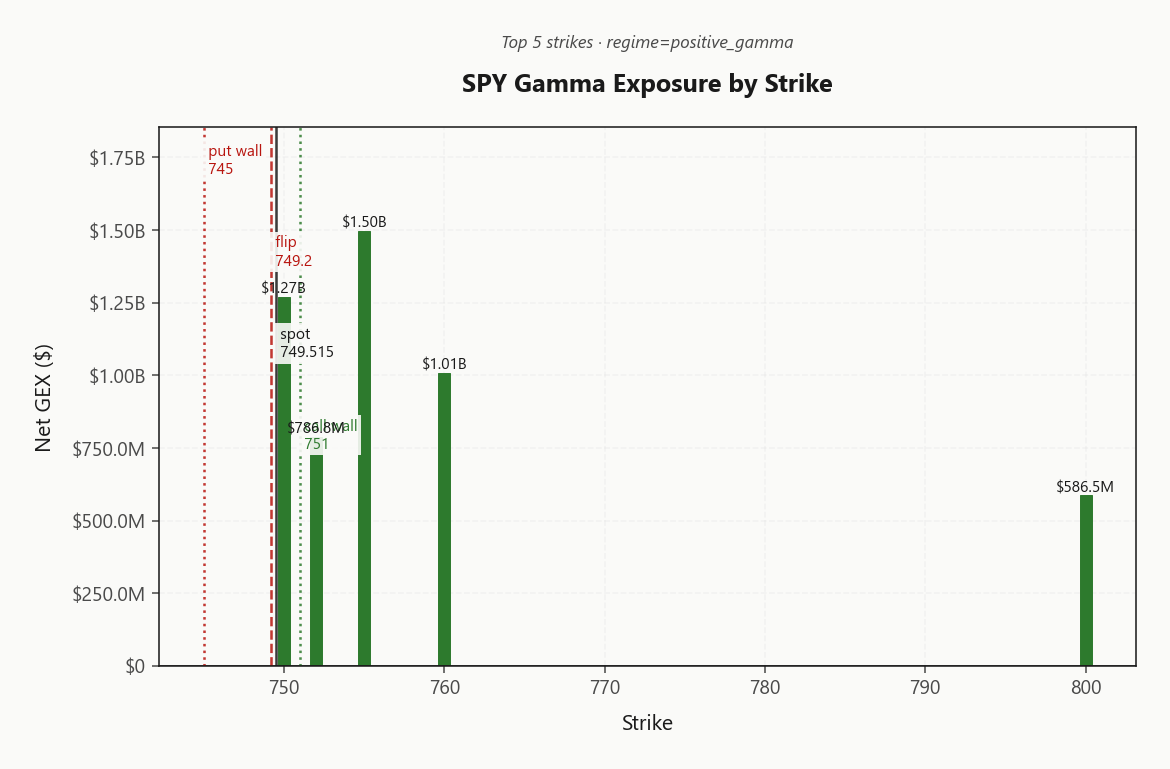

SPY at 749.52 sitting fractionally above the gamma flip at 749.20, net GEX $4.04B - dealers long gamma, mean-reversion regime intact but the cushion is thin. Call wall 751.00 caps the tape, put wall 745.00 is the bid; expect chop between those rails barring a headline. QQQ has broken: spot 728.01 is below flip 760.86, net GEX $1.12B flipped negative and 0DTE GEX is meaningfully short (-34.4%% of total) - that's the divergence story today. Vanna across the complex is large and negative (-$232.63B), so a VIX pop accelerates dealer selling - watch 16.92. Term structure in steep contango (14.84/16.92/19.89), VVIX low at 89.55, VRP positive at 2.52% - vol sellers are paid but tails are cheap. Bottom line: sell premium in SPY iron condors at 30-45 DTE around the flip, avoid naked QQQ short vol while it's below flip, keep cheap VIX call wings on for Hormuz/Iran tape risk.

Positive gamma cushion intact on SPY/IWM, QQQ slips below flip - divergence is the story

SPY sits a hair above 749.20 with dealers long gamma, but QQQ has dropped through its flip at 760.86 and gone net short - the index complex is no longer aligned. Steep VIX contango (Steep Contango) and a tame VVIX (89.55) keep the carry trade alive, but the QQQ break is the lead tell. Iron condors fit the VRP/vol-of-vol mix; tail hedges stay cheap to add given Mideast headline risk.

Regime Assessment

Tape sits in Elevated / Watchful - VIX at 16.92 parks the complex in the high-teens elevated band, neither panic nor low-vol complacency. The regime is sticky: a half-life of 15 sessions means today's posture is roughly tomorrow's posture absent a shock, so don't fade the label intraday.

The transition math favors mean-reversion lower over a melt-up in vol - P(low in 10) prints 0.45 against P(panic in 5) of just 0.05. That's the carry case for staying short premium, sized standard not stretched.

What earns the watchful qualifier rather than a clean green light: QQQ has already broken to Negative Gamma while SPY clings to Positive Gamma a hair above 749.20, and Hormuz headline tape can re-rate VIX 16.92 in a single print. Trade the regime, hedge the tail.

What it means for your trading

Elevated but sticky - base case is mean-revert lower in vol with 0.45 probability over 10 sessions versus 0.05 for a panic break, justifying short-premium carry held at standard size with cheap tail wings on for headline risk.

Trading readVIX up modestly, VVIX down, SKEW up, MOVE flat - that's a textbook 'orderly hedge bid, no jump fear' picture. SKEW rising while VVIX drops is mild divergence worth watching but not actionable yet.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

Term structure is stacked clean: 14.84 front, 16.92 spot, 19.89 three-month - textbook Contango with near-slope at 14.02% confirming the Steep Contango read. No event premium is being demanded in the front; the curve says vol sellers' carry is structurally rich, not stress-priced.

The juice sits in the belly: forward 30-to-60 IV at 21.2196830796 is cheap to the back-month 22.46, where the roll-down is steepest. That's the pocket - 30-45 DTE - and it's where the model lands on Iron Condor at a score of 58.

Caveat the front. VIX9D well under VIX means the very-near tenor is already compressed, so weekly shorts are picking up nickels with Hormuz headlines live. Carry is alive, sizing standard per Standard Size, but the front can re-rate in one tape - own the belly, leave the weeklies alone.

What it means for your trading

Steep contango with a clean 14.84/16.92/19.89 stack pays sellers in the 30-45 DTE belly; don't oversize the front while Mideast headline risk is live.

Trading readClean steep contango - vol sellers' carry is structurally there, market is not pricing event risk into front-month. But VIX9D under VIX means the very-near tenor is already cheap, so don't oversize 0-7 DTE shorts.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.68% sits cleanly above HV20 of 10.16 - vol sellers are being paid a real, measurable premium over what the tape has actually delivered. VRP prints 2.52%, comfortably positive and tradable rather than residual. This isn't a stale-IV mirage; it's honest carry.

HV60 at 14.79 sits above HV20 - realized is cooling, not heating. That's the cleanest tell for short-vol structures: the recent path is calmer than the medium-term print, so the IV cushion is widening as the realized leg compresses underneath it. Vol-of-vol is Low and regime is Positive Gamma, so the cushion isn't fragile.

Premium is real but not extreme - favor defined-risk structures over naked short vol. Iron condor scores 58 at 30-45 DTE; that's the lane. Naked strangles overpay for the carry given how close spot sits to the flip.

What it means for your trading

Vol sellers are paid honest premium here: IV at 12.68% versus HV20 at 10.16 with VRP of 2.52%, and HV60 above HV20 confirms realized is cooling. Sell defined-risk premium at 30-45 DTE - don't go naked.

Skew Convexity

Quarter-delta put IV prints 16.27% against an ATM of 14.84% and a quarter-delta call at 14.09% - the left tail is bid, the right side is asleep. Skew at 2.18% with a smile ratio of 1.16% reads as ordered hedging, not a panic bid; the curve is steep but the wings aren't blowing out.

Call skew flat tells you nobody is paying up for upside convexity - there's no chase premium embedded, no melt-up being underwritten. That's consistent with the Positive Gamma cushion holding spot near the flip while QQQ leaks: hedgers are buying downside, not lottery tickets.

Trade implication: with the put wing this rich versus ATM, naked puts overpay for the protection they deliver. Put spreads - financing the long leg by selling further-out strikes where the smile is still elevated - extract the skew rather than fund it. Stay away from naked short downside; the 1.16% smile means assignment math gets ugly fast if the tape cracks the flip.

What it means for your trading

Steep put skew with flat calls says hedgers are paying for orderly downside cover, not chasing tails - structure your downside via spreads to harvest the 2.18% skew rather than overpaying for naked puts.

Vol-of-Vol Structure

Vol-of-vol is asleep. VVIX at 89.55 prints cleanly below the hundred stress line, and the VVIX/VIX ratio at 5.29 sits well inside its benign band — the options-on-options market is not pricing a bimodal jump regime, just a slow grind in spot-vol. That distinction matters: when VVIX runs hot you discount short-vol structures because the gamma of your gamma blows up on a tape shock; here, it doesn't.

Translation to the book: Standard Size on premium-selling structures — this is not a half-size environment, and the model agrees. The carry trade is intact, dealer-of-dealers convexity is muted, and the iron condor scorecard isn't being penalized by a jumpy second moment.

Caveat — this cuts both ways. VVIX at 89.55 against VIX at 16.92 means tail wings are cheap to layer, not expensive to hold. With Hormuz headlines live, the asymmetry favors stacking long VIX call wings against your short-vol book; a single tape shock re-rates this complex fast, and the hedge is on sale.

What it means for your trading

Vol-of-vol regime is Low — size short-vol normally, but the cheapness of VIX upside wings at 89.55 VVIX means tail insurance is a free option you should be writing into the book, not skipping.

Dispersion Spread

Index VRP is positive but moderate - SPY ATM IV at 12.68% sits well inside QQQ's 20.6% and IWM's 22.02%, with SPY VRP at 2.52% screening cleaner than IWM's 1.3%. The index complex is the place to harvest premium; the headline tape in AAPL, TSLA, and NVDA tells you single-name dispersion is running hotter than the index print suggests.

That gap is the trade. Sell Iron Condor structures at the index level where the VRP is honest and the gamma cushion is doing real work above 749.20. Avoid naked single-name shorts - an idiosyncratic blowup in a megacap won't be cushioned by an index hedge in a Spy Heavier tape, and QQQ's slip below 760.86 means correlation breaks the wrong way when you need it.

Hedge tails with cheap convexity, don't short it.

What it means for your trading

Sell index premium where VRP is clean at 2.52%; avoid naked single-name short vol with dispersion elevated and QQQ already through 760.86.

Liquidity & Microstructure

Open interest is stacked tight around the tape: the top GEX strike at 755.00 carries $1.5B of net gamma, and the flip at 749.20 sits effectively on spot 749.52. Dealers are pinned with the call wall 751.00 capping strength and the put wall 745.00 catching weakness - rails are narrow and well-defined.

Longer-cycle gravity still anchors at 700, the heaviest aggregate OI print and the magnet beneath this week's microstructure. With the flip glued to spot, every tick is a referendum on regime: hold above and the positive_gamma mean-revert engine keeps grinding; lose it and dealer hedging pivots pro-cyclical, lining up with the negative-gamma posture QQQ is already showing.

Bottom line - this is a pinning tape between tight rails. Fade extensions into 751.00, lean on 745.00 as the bid, and treat 749.20 as the single regime trigger barring a Hormuz headline.

What it means for your trading

Microstructure is a pinning setup: call wall 751.00 caps, put wall 745.00 bids, and the flip at 749.20 is the regime trigger sitting on spot 749.52.

Trading readDense positive gamma clusters above spot through the call wall create a soft ceiling - fade strength into those rails. Below the flip the GEX inverts fast, so a break of 749.20 switches the tape from mean-revert to trend-follow.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna is the tell. SPY net VEX prints -$232.63B - large and negative - meaning any pop in 16.92 mechanically forces dealer delta sales rather than cushions them. Charm at -$4.9M layers on a mild bleed into the close. The gamma flip itself, 749.1997788686, is the only level that matters: above it vanna is a buffer, below it the same vector becomes an accelerant.

For now bias reads Supportive - spot sits a hair north of the pivot, dealers in Positive Gamma, mean-reversion mechanics intact. QQQ has already lost that argument: spot below flip 760.86, regime Negative Gamma, vanna there is hostile not protective. The complex is split - Spy Heavier - and a single VIX impulse routes through QQQ first, SPY second.

Treat the flip as a binary trigger: a clean break and SPY inherits QQQ's vanna problem in real time.

What it means for your trading

Vanna across the complex is large and negative, so a tick higher in 16.92 forces dealer selling rather than cushions it; the gamma flip at 749.1997788686 is the binary line where vanna stops being a buffer and starts being an accelerant.

Cross-Asset Confirmation

Cross-asset tape is doing the heavy lifting the equity book can't: MOVE at 74.95 is asleep, rates vol is not corroborating any equity stress, and Fear & Greed prints 61 (Greed) - sentiment is supportive, not stretched. Credit and rates calm under an equity wobble is the signature of an isolated event, not a systemic one.

Inside the complex, the split is the story: SPY and IWM hold positive-gamma posture while QQQ has slipped through its flip, and the divergence reads Spy Heavier. QQQ at 728.01 is the fragile leg; IWM at 289.79 is quietly confirming the benign-macro read. This is a tech-led tremor, not a broad de-risking - until MOVE wakes up or F&G rolls, treat the QQQ break as contained.

Wild card sits offshore: Hormuz headlines can re-rate MOVE and crude in a single tape, and cheap VIX call wings remain the right insurance against a benign backdrop that flips on a wire.

What it means for your trading

Rates vol asleep at 74.95 plus Greed sentiment confirms today's QQQ break is an isolated tech wobble, not a credit-led risk-off - keep cheap VIX wings on for Mideast tape risk.

Scenario EV

The model lands on Iron Condor at score 58 - positive VRP at 2.52%, low vol-of-vol with VVIX 89.55, steep contango (Steep Contango), and SPY still in positive_gamma above the flip at 749.20. That's the clean lane: sell defined-risk premium in the 30-45 DTE pocket where the term-structure slope pays best and 0DTE pin risk doesn't dominate.

Strangles get penalized by assignment risk with spot pressed against the flip; calendars need flatter vol than this curve offers. Put-spread sits behind at 46 - the regime-break backup if SPY loses 749.20 and follows QQQ into negative gamma. VVIX read says Standard Size; no half-size discount, but keep cheap VIX call wings on top given Hormuz headline risk.

Structure the wings around the charm pivot at 749.1997788686, lean the short call into the 751.00 ceiling and the short put toward 745.00. Avoid running the same book in QQQ while it sits below 760.86.

What it means for your trading

Iron condor wins at 58 in the 30-45 DTE pocket; put-spread at 46 is the fallback if SPY breaks 749.20.

Fade strength into the 751.00 call wall; lean on the 745.00 bid. Avoid naked QQQ premium below 760.86 - vanna there amplifies, not absorbs. Keep cheap VIX call wings on against Hormuz headline tape; tail insurance is rarely priced this thin with 74.95 MOVE asleep.

Pivot watch: 749.20. A clean break drops SPY into QQQ's trend regime and the iron condor thesis dies - flatten short vol and let the VIX wings work. Regime stays Elevated / Watchful until proven otherwise.

What it means for your trading

Sell SPY Iron Condor around 749.1997788686, avoid naked QQQ short vol below 760.86, and hold cheap VIX call wings as Mideast insurance. 749.20 is the regime line - a break flips SPY into the same negative-gamma tape QQQ is already trading.

Crude down hard on a reported Iran framework deal restoring Hormuz traffic - direct relief for the energy/inflation channel and a tailwind for risk if it holds.

UK energy bills jumping 13% on Iran war impact - a reminder the macro cost is already in the system even if a deal lands; sticky for European risk and bonds.

ECB warning Iran fallout is amplifying European financial vulnerabilities - keep an eye on EU credit/banks if the deal slips; tail-risk channel is live.

Megacap milestone - SK Hynix and Micron joining the $1T club signals the AI bid is still institutional, not retail froth, even as QQQ chops.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 749.20 against a spot of 749.52. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.68% with a volatility risk premium of 2.52%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.92. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime