Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Positive gamma cushion in SPY/IWM, QQQ short-gamma fragile - divergence is today's lead story

SPY anchored at 749.27 with dealers long gamma - the mean-reversion magnet is live. QQQ trades below its flip at 729.04 in negative-gamma territory, where any vol uptick gets amplified. VIX term structure in Contango keeps vol sellers paid, but Spy Heavier divergence demands selective hedging.

The transition matrix tells the trade: P(panic) over the next five sessions sits at 0.05 - effectively dismissed - while P(grind back to low) over ten sessions runs 0.45, the dominant path. With a half-life of 15 sessions, this regime is sticky: it neither demands panic hedges nor rewards the assumption of an imminent collapse to calm.

Implication: standard sizing, full book, and harvest the VRP that the elevated label keeps bid. Watch the SPY gamma flip at 749.2749588421 as the regime-change tell - a clean break flips the matrix faster than the VIX print will signal.

What it means for your trading

Regime classified Elevated / Watchful with sticky 15-session half-life: panic probability negligible at 0.05, mean-reversion to low at 0.45 - size standard, harvest VRP, watch the flip for regime change.

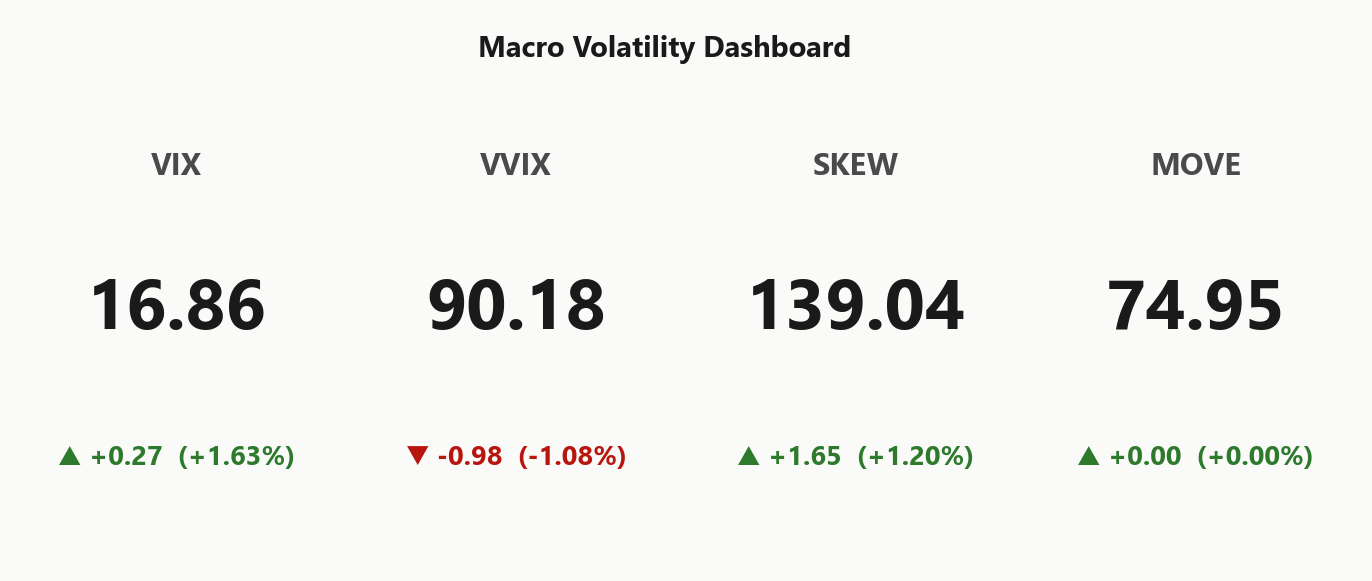

Trading readVIX up slightly, VVIX down, SKEW up, MOVE flat - the cross-confirmation says 'equity-tail bid, rates-tail calm.' This is geopolitical risk pricing, not credit/funding stress, and that distinction defines hedge selection.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

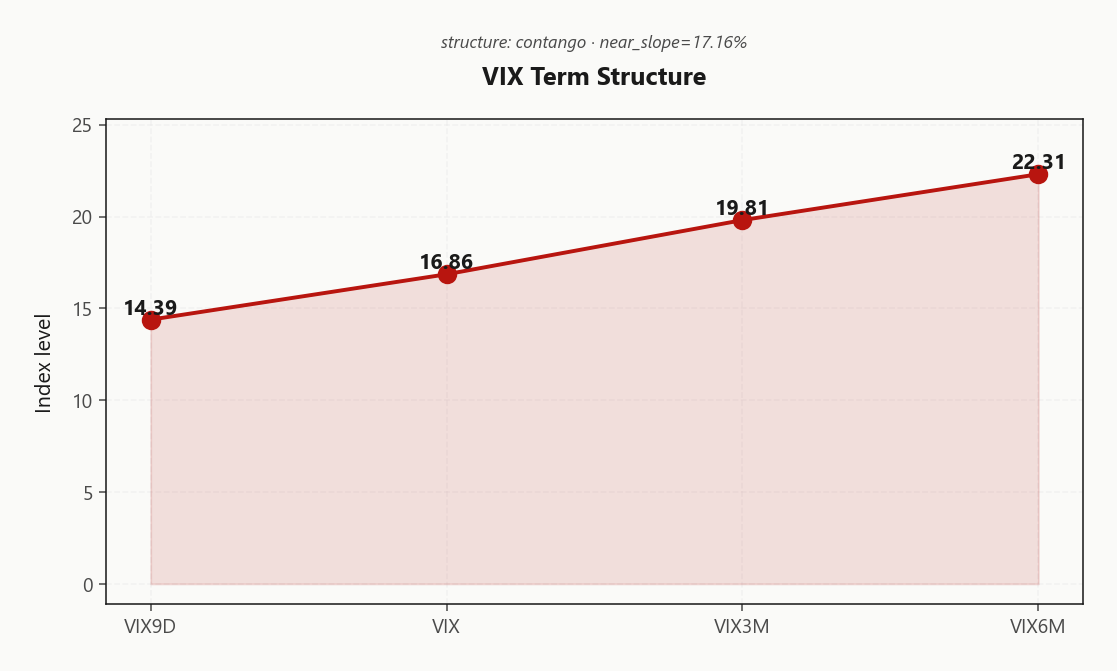

The VIX complex prints a textbook upward-sloping curve: VIX9D at 14.39 sits beneath spot VIX at 16.86, with VIX3M at 19.81 and VIX6M at 22.31 stacking above - a Contango structure pricing carry, not stress. The front-end discount says the tape expects calm into the next handful of sessions; the back-end premium says term sellers still want paying for what they can't see.

Near-slope of 17.16%% confirms Steep contango - vol sellers favored - short-vol carry is positive and roll-down is monetizable. The implied forward 30-60 vol at 21.1311227813 is the cleanest expression of the curve's edge: high enough to harvest, low enough that calendars and condors aren't selling tail for pennies.

Operationally, the belly of the curve in the 30-45 DTE window is where slope monetization compounds without front-end pin risk. Sell vol where forward implieds are richest, fund tail cover with the back-month premium, and respect that Steep Contango regimes invert hard when they break.

What it means for your trading

Steep Contango from 14.39 through 22.31 keeps short-vol carry paid; the 30-45 DTE belly at forward 21.1311227813 is the highest-EV slice to monetize the slope.

Trading readSteep contango with VIX9D well under spot VIX = the market is pricing zero event risk in the next 9 sessions but term premium beyond. Carry is alive but skinny - don't oversize the front.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.06% trades meaningfully rich to HV20 at 10.15, leaving a 1.91% point variance risk premium that pays sellers to stay engaged. The asymmetry is the trade: HV60 at 14.79 sits above spot IV, meaning the tape is already discounting the recent vol burst rather than pricing it forward - short-vol carry is live, not catching a falling knife.

Cross-index dispersion sharpens the call. QQQ VRP at 3.22% is the fattest pocket in the complex - that is where the harvest pays best, premium per unit of realized risk. IWM VRP at 0.35% is barely positive, options priced near fair to realized, which makes small-cap protection the cheapest hedge on the board.

Trade construction follows the spread: monetize QQQ richness through defined-risk premium sales, run SPY as the workhorse condor venue, and finance the book with IWM puts where vol is on sale. The VRP is paying - collect it where it is fattest, hedge where it is cheapest.

What it means for your trading

Vol sellers are paid across SPY and QQQ with QQQ the richest harvest; IWM VRP barely exists, making small-cap puts the cheapest tail hedge to pair against the short-vol book.

Skew Convexity

Quarter-delta put skew is bid across the complex even with VIX subdued - SPY prints 1.62% with a smile ratio of 1.13%, left tail elevated while the call wing trades flat. Put 25d IV at 14.06% sits well above ATM 12.95% and the call 25d at 12.44% - no one is chasing upside, everyone is paying for the downside.

QQQ confirms the broad-tape bid with skew at 2.28%, materially steeper than SPY and consistent with the Negative Gamma regime sitting below its flip. The SKEW index at 139.04 grinds higher into a quiet VIX print - classic tail-demand divergence and the tell that hedgers, not directional buyers, are setting the wing.

Trade implication: with puts rich and calls flat, naked downside is a giveaway. Debit put spreads in SPY and outright put structures in QQQ monetize the smile asymmetry; sell the flat call wing to finance, and lean into Iron Condor in the 30-45 DTE pocket where the skew premium is most harvestable.

What it means for your trading

Steep put skew with smile ratio above parity and SKEW index at 139.04 says downside vol is paying up against a flat call wing - spread protection beats naked puts, and selling the upside wing finances the structure.

Vol-of-Vol Structure

VVIX at 90.18 against spot VIX at 16.86 prints a ratio of 5.35 - squarely Normal. No jump premium is being demanded, no bimodal distribution baked into the wings. The vol-of-vol curve is telling you the tape is not pricing a surprise.

Sizing read comes back Standard Size - full book engaged, no need to defang the gross. With VVIX subdued relative to spot vol, optionality on optionality is on sale: if you are buying tails or layering long-vol convexity, back-month VIX calls and gamma-rich calendars are the cleanest expressions while the cost-of-carry on the wing is this thin.

Cross-checks line up - Contango forward-vol geometry and Spy Heavier cross-asset tone mean cheap vol-of-vol confirms the Iron Condor thesis. No fat-tail to fight, just curve carry to harvest. Sell vol with conviction, own convexity selectively.

What it means for your trading

VVIX/VIX at 5.35 sits in the Normal pocket - no jump risk being priced, sizing stays Standard Size. Cheap vol-of-vol means tail-buyers get optionality on optionality at fair, while short-vol carry remains the higher-EV trade.

Dispersion Spread

Index vol is sitting tame while single-name tape runs hot - SPY ATM IV at 12.06% against QQQ at 19.36% tells you correlation has bled out from under the hood. The QQQ-SPY IV wedge is the dispersion print: mega-cap idio is doing the work, the index basket is dampening it. That's a sell-the-index, leave-the-names tape.

IWM ATM IV at 20.99% rounds out the picture - small-cap idio is bid, but with VRP barely positive there it's the cheapest single-name hedge venue in the complex. Layer that against QQQ's richer VRP at 3.22% and the trade builds itself.

Action: harvest index vol - iron condor in SPY 30-45 DTE - and route any tail hedge into single-name puts, not SPY puts. The basket won't catch the idio shock; the names will.

What it means for your trading

Wide IV gap between QQQ at 19.36% and SPY at 12.06% flags low correlation and live dispersion - sell index vol, own single-name puts as the cheap idio hedge.

Liquidity & Microstructure

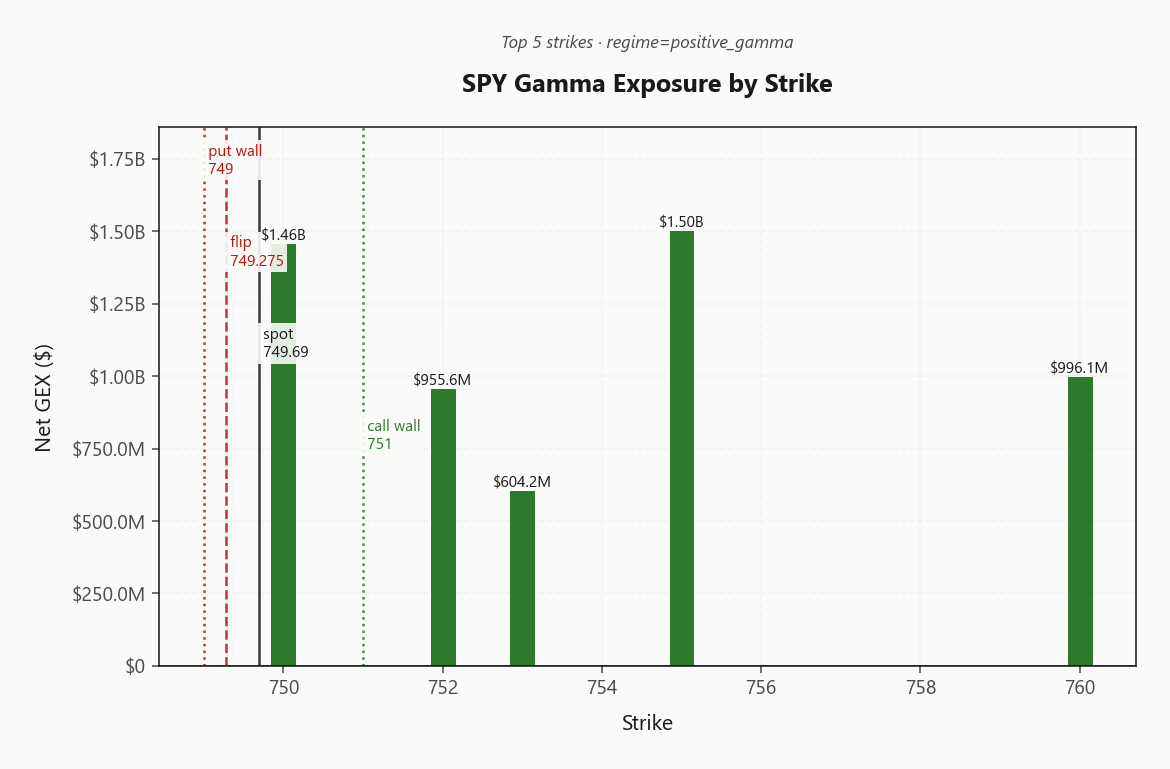

The book pins on a single line: 749.27 sits fractionally beneath spot at 749.69, a knife-edge that decides whether dealer flow dampens or amplifies. Hold above and the long-gamma cushion does its work - vol sold into rips, bought into dips - with the top strike at 755.00 acting as a magnet, carrying $1.5B of net gex anchoring the tape.

The rails are tight: call wall at 751.00 caps grind-up extensions while the put wall at 749.00 backstops shallow dips. The structural OI cluster down at 700 is the long-dated hedge anchor - not in play intraday, but defining the term-structure pocket dealers carry. Trade the rails; do not chase a breakout.

Lose the flip and the same chart inverts - dealer buying becomes dealer selling, mean-reversion becomes trend, and the cushion evaporates in a single print.

What it means for your trading

749.27 is THE level - above it, fade strength into 751.00 and lean on 755.00 as the magnet; below it, flow flips ugly and the long-gamma trade is dead.

Trading readMassive call-side gamma cluster at the top SPY strike with the flip directly under spot - dealers will dampen any move into the wall but flow flips fast if spot loses the flip line. Trade the rails, don't chase the breakout.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$233.8B - deeply negative, which makes vanna the hostile greek today: any meaningful VIX pop forces dealers to sell delta into weakness, the textbook accelerant pattern. The cushion holds while vol stays bid-but-orderly; lose that and the same book that's dampening moves becomes the engine behind them.

Charm is the gentler counterweight. Net CHEX at -$4.5M reads mildly negative, biasing a supportive grind into the bell so long as spot stays north of the pivot. The pivot itself is the gamma flip at 749.2749588421, with current bias Supportive - but distance to pivot is -0.0553617039, a knife-edge where the entire flow regime flips on a single tick.

Trade it accordingly: harvest OTM call decay while charm pays you, but keep the flip as a hard line. Above it, mean-reversion into 751.00; below it, vanna takes the wheel and the same book turns predatory.

What it means for your trading

Dealers sit long gamma but short vanna - supportive bias holds above the flip at 749.2749588421, but a VIX spike weaponizes the book. Treat the pivot as the regime line, not a level.

Cross-Asset Confirmation

Cross-asset tape reads geopolitical, not systemic. MOVE pinned at 74.95 says rates-vol is asleep - no funding stress, no credit contagion, no balance-sheet pricing under the surface. Fear & Greed at 61 prints Greed, which confirms the read: this is Iran-headline tape, not de-risking tape.

The lead story is the index regime split. SPY at 749.69 sits long-gamma above its flip while QQQ at 728.18 trades short-gamma below - Spy Heavier divergence with SPY carrying the cushion and Nasdaq carrying the fragility. IWM at 290.77 holds positive-gamma alongside SPY, and small-cap participation rules out broad de-grossing.

Trade the divergence directly: harvest vol where dealers dampen (SPY/IWM), buy protection where flow amplifies (QQQ). Same hedge, opposite sign across the complex.

What it means for your trading

MOVE flat at 74.95 and Fear & Greed reading Greed rule out systemic stress - the actionable story is the SPY/QQQ Spy Heavier split, with IWM at 290.77 confirming risk-on breadth.

Scenario EV

Scenario engine flags Iron Condor as the highest-EV structure with a composite score of 56, decisively beating the put-spread alternative at 43. The setup is textbook: VRP rich with SPY ATM IV at 12.06% sitting well above HV20 at 10.15, vol-of-vol calm with VVIX/VIX ratio reading Normal, and a deep dealer gamma cushion anchoring the tape above the flip at 749.27.

Optimal DTE band is 30-45 - the front belly where contango slope is most monetizable without absorbing short-dated pin risk. Sell the upper wing into the call wall at 751.00, anchor the lower wing above the put wall at 749.00. VRP assessment reads Unknown, and sizing guidance from the vol-of-vol bundle is Standard Size - full book, no haircut.

What it means for your trading

Iron condor wins the scoring race at 56 vs put-spread 43; deploy in the 30-45 DTE pocket at Standard Size to monetize curve carry while gamma cushions the tape.

Actionable Summary

Trade the divergence. SPY sits in a Positive Gamma regime with spot pinned above the gamma flip at 749.2749588421, bias Supportive - the mean-reversion magnet is live and dealers absorb both sides. QQQ is the fragile cousin, trading below its flip at 729.04 in Negative Gamma territory where any vol pop gets amplified into trend.

Structure of the day:Iron Condor in SPY across the 30-45 DTE belly, selling premium into the 751.00 call wall with the put wall at 749.00 as the lower rail. VRP rich at 1.91%, VVIX/VIX ratio Normal - sizing per Standard Size.

Avoid chasing QQQ longs while spot trades below 729.04; short-gamma amplifies the chase. Hedge cheap via IWM puts - VRP at 0.35% is the thinnest in the complex. Regime read: Elevated / Watchful - full book, watch the flip for the regime flip.

What it means for your trading

Sell SPY Iron Condor into 751.00 while spot holds the 749.2749588421 flip; fund QQQ short-gamma hedges with IWM puts where VRP at 0.35% is cheapest in the complex.

Draft Iran-US deal reopening Hormuz is the biggest oil-vol catalyst this week - if confirmed, removes a key tail risk that's been propping single-name energy vol.

Crude down ~6% on Hormuz reopening news directly compresses inflation-vol pricing and feeds the contango VIX structure - confirms why front-vol is being sold.

ECB warning on European financial vulnerabilities is the contrarian flag - Europe-specific tail risk if Iran deal slips, watch EWG/EZU vol if it escalates.

UK energy bill 13% jump is the canary that even with a deal, second-order inflation pass-through is in motion - keeps central-bank vol bid in the back half of the curve.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.01 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 749.27 against a spot of 749.69. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.06% with a volatility risk premium of 1.91%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.86. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime