Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

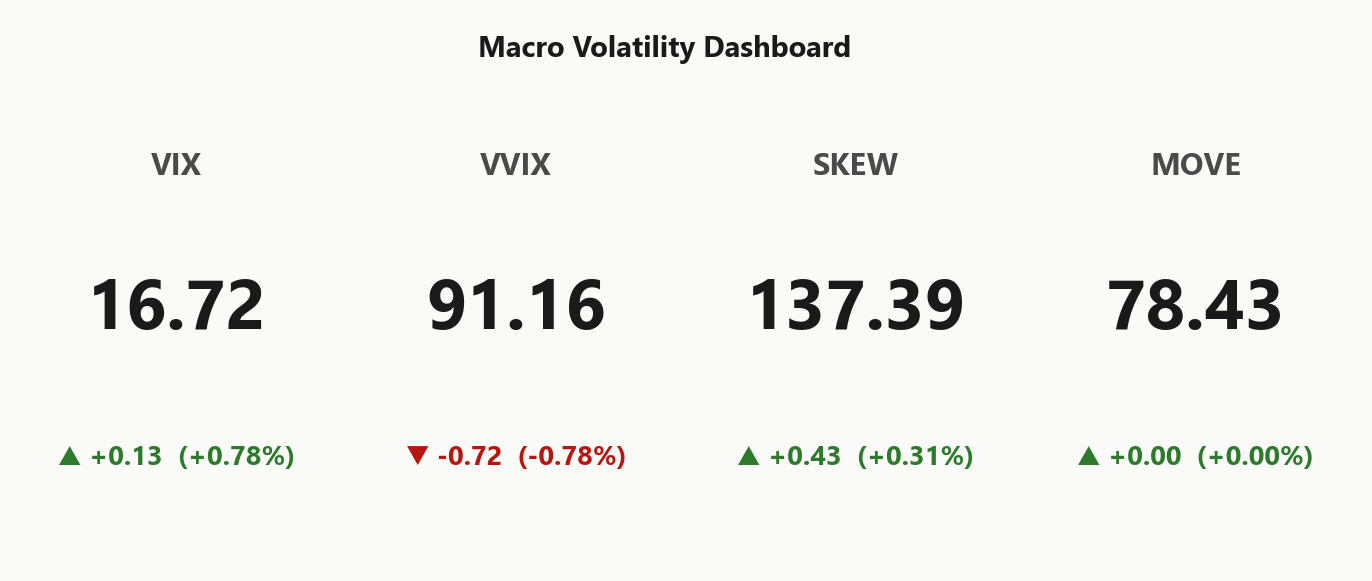

SPY at 750.69 sits fractionally below its gamma flip at 752.93, with net GEX -$3.87B placing dealers in short-gamma territory - moves get amplified, not dampened. Call wall 751.00 is right above spot acting as a ceiling, put wall 745.00 is the air-pocket trigger. QQQ and IWM both hold positive gamma above their flips, so this is an SPY-specific fragility - divergence direction Qqq Heavier. VIX at 16.72 with VIX9D at 14.07 and VIX3M at 20.03 keeps term structure in Contango, VVIX at 91.16 is benign - vol sellers' carry is intact. VRP at 1.92% vol points is active but not extreme, and skew_25d at 2.14% shows ordered downside bid, not panic. Bottom line: reclaim of 752.93 flips dealer flow supportive and clears the path to mean-reversion trades; failure here and 745.00 becomes the next stop with accelerating dealer sell-flow.

SPY short gamma below 752.93 while QQQ/IWM hold positive - fragile mean-reversion

SPY sits a hair below its gamma flip at 752.93 with dealers net short gamma, while QQQ and IWM remain comfortably in positive-gamma territory - a classic single-index fragility setup. VIX term structure is in steep contango with VVIX at 91.16 signaling no jump-risk premium, so vol sellers are paid but the SPY/QQQ regime split is the day's tell. Iron condor edge exists in the 30-45 window, but size must respect that any SPY breach below 745.00 flips the entire complex hostile.

Regime Assessment

Regime tape reads Elevated / Watchful with VIX anchored at 16.72 - elevated enough to pay carry, nowhere near panic. Half-life of 15 sessions stamps this as sticky, not transitional; the Markov drift is sideways, not breaking.

Transition math is the tell: probability of escalation to panic over five sessions sits at 0.05, while decay to low-vol over ten clocks 0.45 - asymmetric in favor of melt, not crack. Tail hedges remain optional, structural VIX upside convexity is a luxury position, not a requirement.

Trade the persistence: short premium and iron condors carry their edge as long as the regime holds. Reassess only if VIX clears the twenty handle or QQQ surrenders its flip - that is the signal the Elevated tag flips character and the playbook changes.

What it means for your trading

Regime is Elevated / Watchful and sticky at a 15-session half-life - decay to calm is more likely than escalation, so trade today's tape as the central case.

Trading readVIX elevated, VVIX benign, SKEW elevated, MOVE contained - the equity tail is priced but the rate-credit complex isn't confirming. Divergence between SKEW and MOVE is the standout - equities pricing risk that rates don't see.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

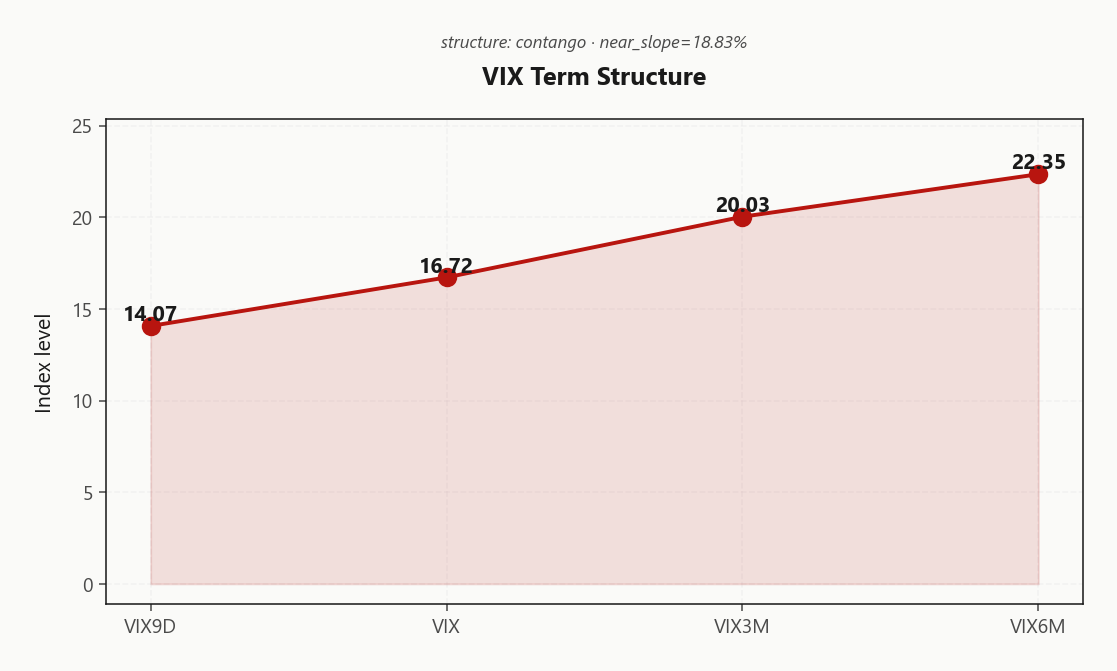

Forward Vol Geometry

The VIX curve prints Contango in textbook order - 14.07 front, 16.72 spot, 20.03 three-month, 22.35 six - no event hump, no kink, just clean upward slope. Near-slope at 18.83%% pays the vol seller cleanly, but back-end sitting structurally elevated above realized says the curve is pricing carry, not crisis. Regime reads Steep Contango.

The forward 30→60 implied at 21.4947005097 against 60→90 at 24.4508507009 embeds modest mean-reversion higher - the curve doesn't believe today's front-end calm persists into the back. That's the tell: short the belly, not the wings. The 30-45 window is where slope steepness translates to theta without buying tomorrow's tape.

Calendar diagonals over outright short premium - sell the belly, own the back-month convexity that the curve already says is mispriced. Beyond ninety days the slope flattens and the carry thins; don't reach.

What it means for your trading

Curve in Steep Contango with near-slope at 18.83%% - the 30-45 belly is the carry sweet spot, calendar diagonals beat naked short premium given the structurally elevated back end.

Trading readSteep contango from VIX9D through VIX6M tells you the curve trader is paid to be short front-month vol - no event premium priced, calendar carry intact, but the steepness itself is a warning that any spot drop steepens it further.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.33% sits comfortably above HV20 at 10.41, putting VRP at 1.92% vol points - a real premium, not a rounding error. Options are pricing meaningfully richer than short-window realized, and the carry is live for sellers who respect the regime.

HV60 at 14.78 sits above HV20, telling you recent realized has decelerated versus the prior quarter - not accelerated. That asymmetry matters: premium sellers are paid against a cooling tape, not chasing a heating one. Classic carry regime, but the easy money was last month.

Cross-asset, the dispersion is the tell. QQQ VRP at 2.57% runs wider than SPY - tech-vol remains the cleanest structural carry. IWM VRP at 0.11% is razor-thin, effectively zero margin for small-cap premium sellers. The hierarchy is clear: deploy condors in QQQ first, SPY second, and treat IWM short-premium as a margin-of-safety trap until the spread widens.

What it means for your trading

VRP is active in SPY at 1.92% vol points with HV60 above HV20 confirming a cooling-realized backdrop, but the cleanest carry sits in QQQ at 2.57% while IWM at 0.11% offers no margin and should be avoided for short-premium structures.

Skew Convexity

The quarter-delta skew at 2.14% with smile ratio 1.16% tells the cleanest story in the surface: downside is bid, but it's a structural bid, not a panic steepening. Put wing prints 15.33% against ATM 13.93% - paying up in an orderly cadence consistent with hedge demand, not tail grab.

The more revealing tell sits on the call side. Call wing at 13.19% trades below ATM - flat-to-inverted upside skew, which prices zero melt-up conviction in the chain. Combined with the steep put slope, the surface is asymmetric in the textbook sense: downside paid, upside abandoned. Put spreads dominate naked puts here - you're financing tail at a wing the market refuses to bid, and the carry is real.

Cross-asset, QQQ skew at 2.86% runs materially steeper than SPY - tech panic premium is the more expensive insurance, and the dispersion read says single-name vol is doing the work the index won't price.

What it means for your trading

Skew is steep but ordered - structural hedging, not left-tail panic, with call skew inverted at 13.19% versus ATM 13.93%. Favor put spreads over naked puts and route panic-protection budget toward QQQ where skew at 2.86% is doing the actual pricing work.

Vol-of-Vol Structure

VVIX at 91.16 sits squarely in Normal territory against VIX at 16.72 - the ratio prints 5.45, which is to say the market is not paying for vol-of-vol convexity. No binary-outcome pricing, no embedded jump-risk premium, no scramble for upside VIX wings. That's the green light for Standard Size on premium-selling structures rather than the defensive half-size posture a stressed VVIX would force.

The asymmetry to lean on: with vol-of-vol asleep, deep OTM VIX calls and structural upside-vol convexity are cheap on a relative basis. This is the regime where you finance carry with one hand and add tail convexity with the other - not because the tail is imminent, but because you're being given the optionality at fair-to-discounted prices while the rest of the chain is calm.

Watch the same VVIX print as the abort signal. A break above 91.16 coincident with a VIX expansion is the binary-pricing tell - that's when the convexity bid arrives, the ratio re-rates, and standard sizing becomes a liability. Until then, the carry trade has the wind.

What it means for your trading

Vol-of-vol benign at VVIX 91.16 with ratio 5.45 sanctions Standard Size on short-premium while leaving structural VIX upside convexity attractively priced. Cut size if VVIX breaks higher on a vol spike.

Dispersion Spread

Index ATM IV at 12.33% sits materially below QQQ at 18.96% and IWM at 21.02% - dispersion is alive. Correlation is suppressed, single-name vol is doing the work, and the index aggregate is cheap precisely because the components aren't moving together. Cross-strike dispersion at 76.84 confirms the smile is doing the lifting, not the headline ATM.

Trade implication is directional: SPY/SPX is the premium-selling vehicle, not single names. Index IV gives you carry without paying the idiosyncratic vol tax embedded in QQQ and IWM strips. The inverse also holds - anyone long single-name gamma cannot hedge cheaply with index puts; the basis works against you when correlation re-couples.

The cleanest structural expression is tech dispersion: short QQQ vol against long baskets of constituent vol captures the 18.96% vs SPY 12.33% gap with a defined correlation kicker. IWM at 21.02% is a trap for short-premium - small-cap dispersion is wider but the VRP cushion isn't there to underwrite the structure.

What it means for your trading

Suppressed index correlation makes SPY at 12.33% the right premium-sale vehicle versus QQQ 18.96% and IWM 21.02%; tech dispersion (short QQQ vol, long constituents) is the cleanest structural trade today.

Liquidity & Microstructure

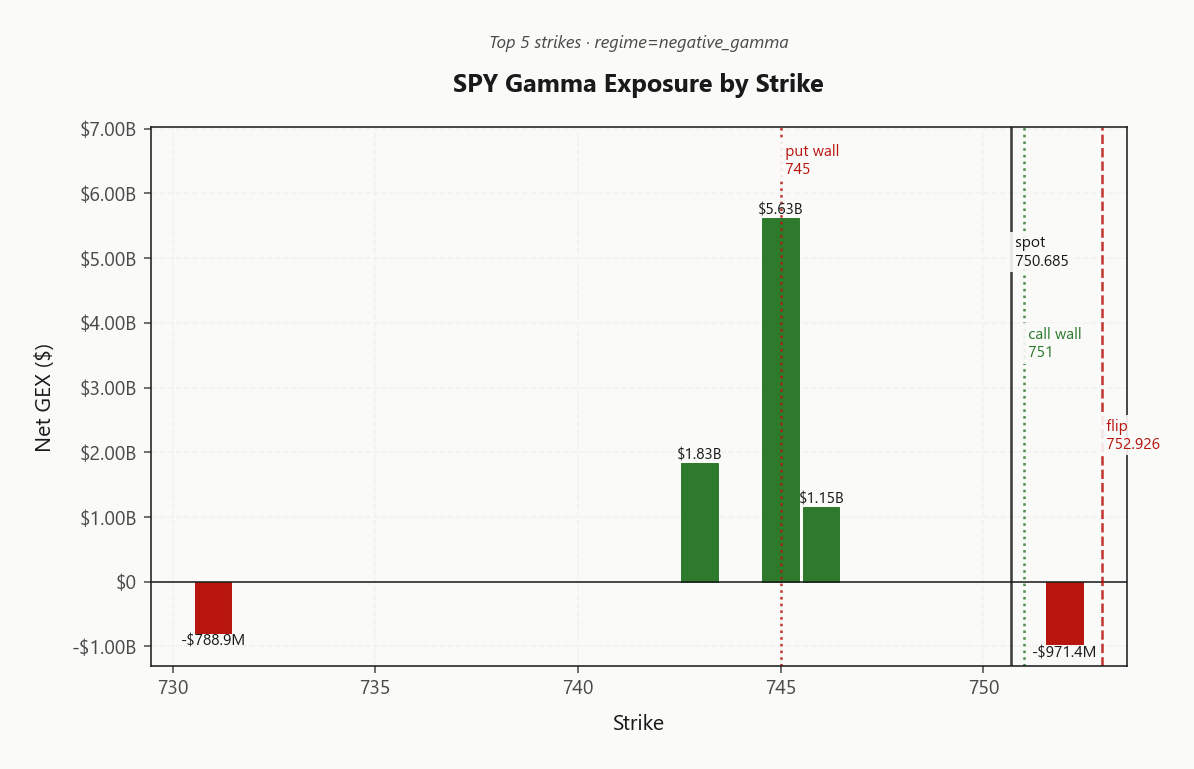

SPY trades at 750.69, a hair below the gamma flip at 752.93 - the single level that defines the session. Above it dealers buy dips and the tape dampens; below it they sell rallies and moves get amplified. Open interest gravity sits well above spot at 765, meaning if buyers reclaim the flip, the magnetic pull is higher, not lower.

The call wall at 751.00 caps near-term upside and sits effectively at spot - dealers are pressed right against it. Below, the put wall at 745.00 is the air-pocket trigger; the top GEX strike at 745.00 carries a positive-gamma cushion of $5.63B that should catch a first probe lower.

Trade it as a binary: reclaim of 752.93 flips dealer flow supportive and clears the path toward the 765 OI gravity. Failure here and a clean break of 745.00 opens accelerating sell-flow with no structural cushion until the next strike cluster.

What it means for your trading

The gamma flip at 752.93 is the binary pivot - reclaim turns dealer flow supportive toward the 765 OI cluster, while loss of 745.00 opens an air pocket with accelerating sell-flow.

Trading readHeavy positive GEX concentrated below at the 745.00 cluster while 751.00 caps just above spot means dealers dampen rallies up to the call wall and provide air below it - the gamma flip 752.93 is the only level that matters today.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$58.03B - deeply negative and the cleanest tell on the tape. Any uptick in vol forces dealers to sell delta, which means a VIX expansion from here is self-reinforcing on the downside, not absorbed. Vol up = dealers sell delta - downside amplified if vol spikes - there is no offsetting bid waiting in the vanna book.

Charm compounds the problem. Net CHEX at -$1.42B means dated puts bleed theta straight into dealer sell-flow as the session ages - Time decay pushing dealers to sell - pressure into close. The pressure isn't theoretical; it builds mechanically into the close, peaking when intraday liquidity thins.

The flow inflection sits at 751 (Call Wall). Current bias reads Neutral - neither side owns the dealer hedge yet. Reclaim and vanna/charm flip supportive; lose it and both greeks pull the same direction, hostile, into the bell.

What it means for your trading

Vanna and charm are aligned hostile below 751 - vol-up sells delta, time decay sells delta, and the pivot is the only thing standing between Neutral flow and a one-way close.

Cross-Asset Confirmation

MOVE at 78.43 stays contained - no rate-credit stress is leaking into equity vol, which is why SPY's gamma fragility reads as positioning, not macro shock. Fear & Greed at 59 registers Greed, sentiment crowded long against an elevated VIX - the textbook contrarian setup where consensus gets caught offside on any reflexive flush.

QQQ at 726.70 and IWM at 289.25 both hold above their flips while SPY sits below its own at 752.93 - divergence direction reads Qqq Heavier, meaning the fragility is SPY-isolated and mean-revertible, not a complex-wide breakdown. Iran headlines are noise: gold giving back peace-hope premium and European equities absorbing locally confirms geopolitics is mean-reverting, not credit-shocking.

Net read: cross-asset tape is aligned, not confirming a regime change. Watch MOVE for the real tell - a break higher there is the only signal that turns SPY's isolated fragility into a contagion trade.

What it means for your trading

Cross-asset confirmation says SPY's short-gamma posture is an isolated positioning fragility, not a macro shock - MOVE at 78.43 contained and QQQ/IWM holding their flips. Greed at 59 flags contrarian risk if SPY fails its flip, but the absence of rate-vol contagion keeps mean-reversion the central case.

Scenario EV

Scenario EV ranks Iron Condor highest at 42, with the put-spread alternative trailing at 30. The stack is coherent: VRP active at 1.92% vol points pays the wings, VVIX at 91.16 keeps vol-of-vol benign, and the term curve in Contango means the slope itself bleeds in your favor.

Place the structure in the 30-45 DTE belly - far enough out to capture the curve's steepest segment, close enough in to avoid the charm-cliff and the 0DTE gamma whip around the flip at 752.93. Short call wing anchored outside 751.00, short put wing outside 745.00 - the existing dealer book defines the rails for you.

Size standard, not defensive: VVIX in normal zone means no jump-risk discount needs paying. The put-spread at 30 is the substitute structure if SPY fails to reclaim flip - ordered skew at 2.14%, not panic, keeps it second-best, not first.

What it means for your trading

Iron condor in the 30-45 window with wings outside 751.00 and 745.00 - standard size given benign VVIX. Put-spread is the fallback if 752.93 fails to reclaim.

Actionable Summary

BLUF: SPY pinned at the flip while QQQ and IWM hold positive gamma - an Elevated / Watchful regime that pays carry but punishes complacency. The trade is Iron Condor in the 30-45 window, wings outside 751.00 and 745.00. 752.93 is the only level that matters: reclaim flips dealer flow supportive and validates the short-premium thesis; failure here turns dealers into accelerants and puts 745.00 in play as the air-pocket trigger.

Avoid the 0DTE chase in either direction - SPY's 0DTE book is short-gamma biased and built for whipsaw, not trend. With VVIX at 91.16, VIX upside convexity is structurally cheap; pair the condor with a small dated VIX call overlay rather than tightening the wings. Reassess if VIX clears 16.72's next handle or QQQ loses its flip - at that point the cross-asset divergence (Qqq Heavier) resolves the wrong way and the regime changes character.

What it means for your trading

Trade Iron Condor around 752.93 with wings outside 751.00/745.00; cheap VVIX at 91.16 makes tail convexity the right hedge, not wider strikes.

UK gilts retreating from multi-decade highs eases global duration stress - supportive backdrop for risk and for the contained MOVE reading driving today's benign cross-asset tone.

AI optimism overpowering Middle East risk in the open is exactly what the data confirms - MOVE flat, F&G greedy, geopolitics priced as noise not credit-event.

ECB hawkish 'hike anyway' line from Schnabel is the real macro signal today - it props euro rates, drains dollar liquidity at the margin, and matters more for vol than any Iran headline.

Rubio's Strait of Hormuz line is the one geopolitical trigger that could break the MOVE-contained narrative - energy and shipping vol are the cleanest expression if it escalates.

Gold giving back on receding peace hopes confirms this is a mean-reverting geopolitical trade, not a credit-shock - exactly why MOVE stays calm and SPY's fragility is positioning, not macro.

European equities lower on Iran headlines while US futures lean higher signals risk is locally absorbed, not contagious - supports the cross-asset 'isolated SPY fragility' read.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 752.93 against a spot of 750.69. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.33% with a volatility risk premium of 1.92%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.72. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime