Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

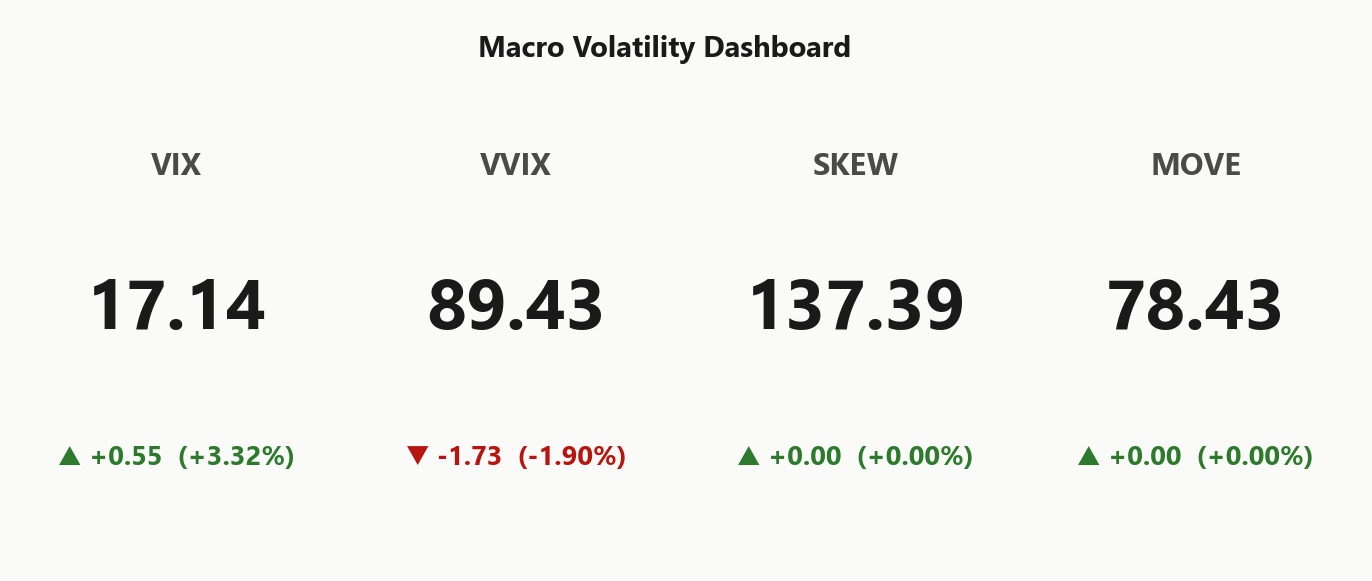

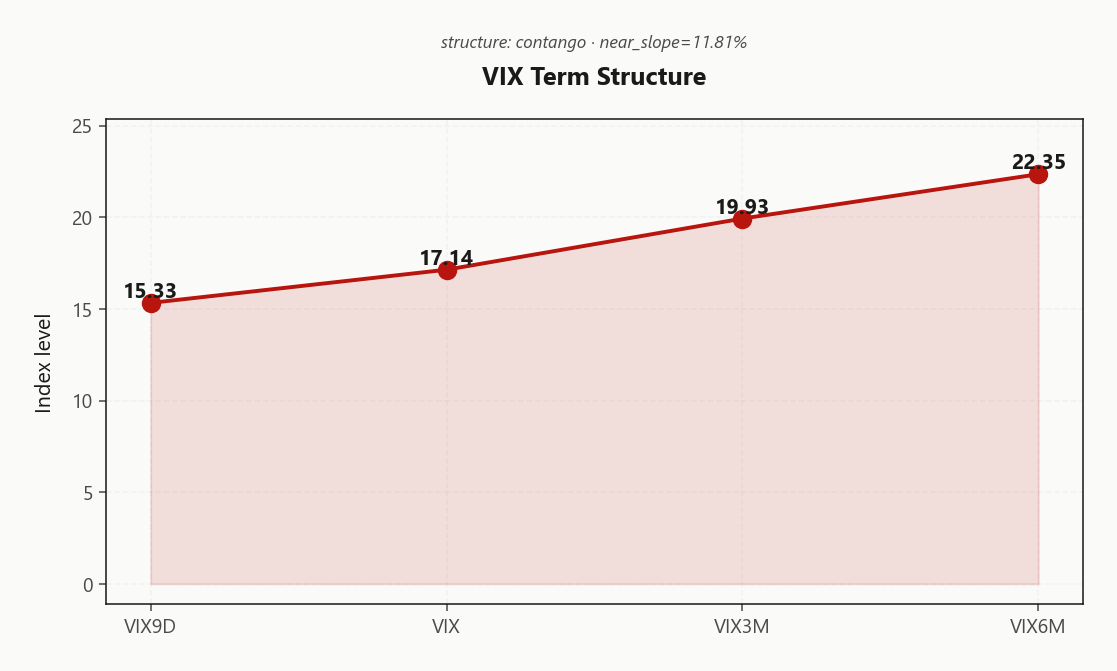

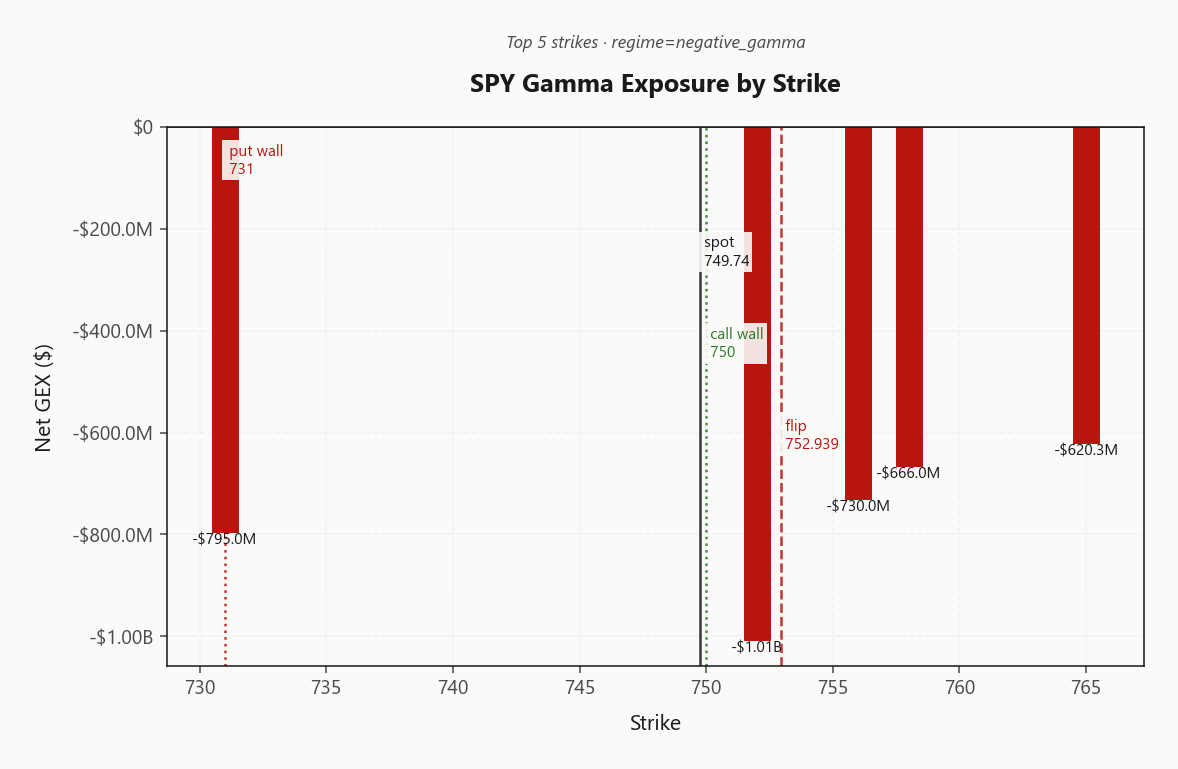

SPY at 749.74 sits just below the gamma flip at 752.94 with dealers carrying net GEX of -$16.05B - squarely in negative gamma. Call wall stacked at 750.00, put wall at 731.00, max pain up at 761.00, and the heaviest OI lives at 765 - spot is pinned right under resistance. Dealer vanna of -$45.74B and charm of -$2.4M are both hostile: a vol spike forces additional delta-selling, and time decay nudges hedgers to lean lower into the bell. VIX at 17.14 with the term curve in Contango (15.33 → 19.93) keeps structural carry alive, and VVIX at 89.43 confirms no jump-risk panic. Cross-asset is aligned - QQQ at 728.13 and IWM at 289.91 share the negative-gamma label but with green forward-vol geometry. VRP is 2% vol points over 20d realized - modest but real. Bottom line: Iron Condor on 30-45 DTE is the cleanest expression - fade strength into 750.00, defend below 752.94, and size standard given Standard Size.

Negative gamma across index complex with VIX in contango - amplified moves, but vol sellers structurally favored

SPY at 749.74 is wedged against its call wall while dealers sit in negative gamma - moves get amplified intraday but the Steep Contango term structure and subdued Low VVIX say vol sellers still own the carry. The split signal - short-gamma microstructure inside a contango macro - is THE story: trend-following bursts above the flip, mean-reversion bias once price reclaims 752.94. Trade the regime, not the headlines.

Regime Assessment

Current state: Elevated / Watchful with VIX anchored at 17.14. The transition matrix is the tell - probability of escalating to panic over the next handful of sessions sits at 0.05, while the drift back to a low-vol regime over ten sessions runs 0.45. Asymmetric, and the asymmetry favors mean-reversion lower, not escalation higher.

The half-life of 15 sessions is the operative number. This is a sticky state - not transient, not a coiled spring. Don't trade for a near-term resolution; the regime tells you it wants to sit. Panic requires an exogenous shock the system isn't currently pricing - 89.43 VVIX and 78.43 MOVE both confirm no underlying jump-risk bid.

Trade implication: position for persistence, not transition. The base case is grind, with drift back toward low-vol the higher-probability path. Carry-collecting structures over 30-45 DTE clear the regime's expected lifetime - let the half-life work for you, and don't pay for tails the matrix says aren't coming.

What it means for your trading

Regime is Elevated / Watchful and sticky - half-life of 15 sessions, panic probability negligible, drift-lower the dominant path. Sell time against persistence; don't bet on a fast resolution either way.

Trading readVIX up modestly, VVIX down, SKEW unchanged, MOVE subdued - confirming each other in a 'controlled elevated' read. No divergence flashing regime-shift; this is genuine consolidation, not the calm before.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The vol curve sits in Steep Contango: VIX9D at 15.33 sits well below cash VIX at 17.14, which itself trails the three-month at 19.93. No event premium in the front, no stress bid leaking into the back. Structure is Contango with a near-slope of 11.81% - clean carry geometry, vol sellers' market.

Forward front-leg vol prints 21.1876744831 stepping up to 24.5324295576 on the back. The curve is pricing gradual normalization, not a regime break - the back end expects elevation, the front does not. That is structural carry, the kind that compounds for short-vol books, not the stress contango that whips into backwardation on a single tape.

Best edge lives in the 30-45 DTE bucket where roll-down compounds hardest. The caveat: front-end carry is rich precisely because dealers sit short gamma at spot. Harvest the term-structure premium, but respect the gamma flip at 752.94 - vol-of-spot can blow through carry assumptions on any session that breaks the line with conviction.

What it means for your trading

Steep contango with VIX9D anchored under cash and forward slopes pricing gradual normalization keeps vol sellers structurally favored. The 30-45 DTE window is the sweet spot for roll-down compounding, but front-end carry comes packaged with short-gamma microstructure - respect the flip at 752.94.

Trading readNear-slope of 11.81%% in Contango - the curve is carrying without pricing event stress. Vol carry trade is live; the curve itself becomes a warning signal if it inverts.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.35% prints above HV20 of 10.35 but sits well under HV60 of 14.77 - options are modestly rich to recent tape, not historically extreme. The VRP of 2% is positive but compressed, which is the entire trade-design constraint: there is carry, but not enough to cover sloppy execution or oversized exposure.

The HV60 > HV20 geometry says realized has decelerated into the present - the longer lookback still carries the memory of a hotter tape, while the recent twenty sessions have already cooled. That mean-reversion in realized is exactly what compresses VRP from generous to merely active, and it argues against pressing naked short vol into an environment where the cushion has already been harvested.

Cleaner expression: defined-risk spread structures over naked premium sales. Iron condors and put-spread verticals monetize the 2% edge without exposing the book to a single asymmetric tail event. Size standard, not aggressive - the carry is real but the margin for error is thin.

What it means for your trading

VRP of 2% is positive but compressed with HV20 cooler than HV60, so the realized-vol cushion is real but thin - deploy spread structures, not naked premium, and let sizing reflect the modest edge.

Skew Convexity

Quarter-delta skew prints 2.07% with the smile ratio at 1.16% - elevated, ordered, and decidedly not panicked. Put quarter-delta IV of 14.88% sits a measured step above ATM at 13.58%, with calls bid down to 12.81%. Downside demand is structural, not desperate - the tail isn't screaming, the hedge book is just doing its job.

At this convexity the math favors put spreads over naked OTM puts: you're paying a premium for downside that's already priced in, so finance the long leg by selling the steeper wing. The skew curve is doing the work for you - extracting the embedded richness beats paying it. Symmetrically, upside calls screen cheap against the skew premium; for tape that's pinned under 750.00 with dealers short gamma, the convexity-relative value sits squarely on the call side.

Net: orderly skew + aligned cross-asset regime (Aligned) keeps this a vertical-spread tape, not a tail-hedge scramble. Trade the wings as spreads; let someone else overpay for the crash bid that isn't coming.

What it means for your trading

Quarter-delta skew at 2.07% is elevated but ordered - put spreads dominate naked puts on convexity-adjusted carry, and call quarter-delta at 12.81% screens as the cleanest value buy against the skew premium.

Vol-of-Vol Structure

VVIX at 89.43 against VIX 17.14 prints a ratio of 5.22 - squarely in the Low vol-of-vol regime. The tape is not pricing bimodal jump risk: no fat tail bid into VIX calls, no convexity premium hunting a shock. This is the quiet ceiling under which short-vol structures actually clear.

Sizing guidance reads Standard Size - operators get the green light to deploy full-notional vol-selling structures without the half-clip discipline that an extreme VVIX print would force. The negative-gamma microstructure in SPY argues for spread geometry, but the vol-of-vol backdrop itself is permissive, not punitive.

The trigger to flip the playbook is mechanical: VVIX through the century mark. That's the first regime-shift tell - convexity bid returns, jump risk gets re-priced, and the standard-size license gets pulled. Until then, carry is alive and the structural seller owns the curve.

What it means for your trading

VVIX at 89.43 confirms the Low vol-of-vol regime - full-size short-vol structures cleared, with VVIX through 100 as the mechanical kill-switch.

Dispersion Spread

Index vol screens cheap to constituents: SPY ATM at 12.35% versus QQQ at 19.17% and IWM at 21.25%. The spread is moderate but directionally clear - single names are carrying the idiosyncratic premium while the index aggregate gets the diversification discount. Correlation assumptions baked into SPY surface are too generous given the megacap concentration driving the tape.

Idiosyncratic risk is stacked in the growth complex - the AI-megacap cohort owns the realized-vol contribution while SPY surface socializes it away. That asymmetry is the trade: monetize SPY/SPX vol where the carry is clean against 2% VRP, and avoid short single-name premium against the same theme - you'd be selling the rich leg of the dispersion at the wrong sign.

For desks with the infrastructure, the cross-name dispersion play is live: long constituent vol, short index vol harvests the structural mispricing without taking a directional view on the 752.94 flip. For everyone else, the actionable read is simpler - stay in SPY for the Iron Condor on 30-45 DTE and keep single names out of the short-vol book.

What it means for your trading

Index vol at 12.35% underprices constituent risk relative to QQQ's 19.17% and IWM's 21.25% - monetize SPY premium, leave single-name short vol alone against the AI-megacap theme.

Liquidity & Microstructure

SPY is wedged between the gamma flip at 752.94 and the call wall at 750.00, with the heaviest open interest stacked overhead at 765. The dominant GEX cluster sits at 752.00 carrying -$1.01B - a concentrated short-gamma pocket right where price wants to trade.

Sub-flip mechanics are unambiguous: dealer hedging amplifies directional moves rather than dampening them, so intraday bursts run further than positive-gamma intuition suggests. Reclaim of 752.94 flips the tape back toward mean-reversion; failure leaves trend-following flow in control with the 731.00 put wall as the structural circuit-breaker beneath.

Trade the levels, not the chop. Fade strength into 750.00, respect 752.94 as the regime line, and treat 731.00 as the defensive backstop where dealer flow finally resists.

What it means for your trading

Spot pinned between 752.94 and 750.00 with dealers short gamma - moves amplify until the flip is reclaimed, with 731.00 the downside circuit-breaker.

Trading readHeavy negative GEX stacked below spot with the dealer-short concentration at the 750.00 call wall - moves get amplified in both directions until spot reclaims the gamma flip. Trade the levels, not the chop.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks are uniformly hostile. Net vanna sits at -$45.74B and net charm at -$2.4M - both negative, both reinforcing the same direction. A vol spike doesn't stabilize the book; it accelerates dealer delta-selling, wiring a vol-up/spot-down feedback loop straight into the tape. This is the opposite of the cushioned, mean-reverting behavior longs assume from muscle memory.

Charm compounds the problem into the bell. As theta burns, hedgers lean lower mechanically - late-session drift carries a structural selling bias rather than the gamma-pinning longs are conditioned to expect. The Call Wall at 750 is the dealer-flow inflection: above it, charm/vanna pressure releases; below it, the feedback loop owns the close. Current bias reads Neutral, which is permission to trade levels, not narrative.

Operationally: do not fade vol spikes assuming dealer absorption, and do not size into the last hour expecting stabilization. Trade the 750 flip as the regime line - that is where the dealer-flow vector changes sign.

What it means for your trading

Vanna and charm are both pulling dealers the same way - vol-up forces selling, time-decay forces selling - so the 750 pivot is the only level that matters for whether the feedback loop accelerates or releases into the close.

Cross-Asset Confirmation

MOVE at 78.43 stays subdued - credit and rates vol are not amplifying the equity short-gamma profile. That's the single most important cross-asset tell: whatever fragility lives in the index complex is microstructural, not macro-transmitted. Fear & Greed prints 60 (Greed) - constructive sentiment without the euphoria that typically front-runs reversals.

QQQ at 728.13 and IWM at 289.91 both carry the same negative-gamma label as SPY, and the regime read is Aligned. Uniform fragility is paradoxically the cleaner setup - no single index is leading a break, which materially compresses tail-event probability. When SPY, QQQ, and IWM disagree, you trade the divergence; when they align, you trade the regime.

Geopolitical headlines remain noise, not signal. With MOVE compliant and cross-asset Aligned, the Hormuz/ECB tape is headline risk - pricedown-able through spreads - not regime risk demanding gross reduction.

What it means for your trading

Cross-asset is aligned and benign: subdued 78.43 MOVE and Aligned index regimes confirm an equity-microstructure story, not a macro shock. Trade the short-gamma microstructure with standard sizing - the tail isn't being priced anywhere else.

Scenario EV

The scenario engine lands on Iron Condor with a score of 42 on 30-45 DTE - the cleanest expression when Steep Contango term structure, Low VVIX at 89.43, and a modest VRP of 2% all line up. Range-bound premium harvesting beats taking a side on the gamma-flip war at 752.94.

Put-spread directional fallback scores 30 - usable if you must lean, but the carry/risk geometry favors the two-sided structure. Avoid naked strangles: short-gamma microstructure below the flip means dealer flow amplifies, not dampens, and an unhedged tail in this regime is the trade that ends the month.

Center the condor above spot, lean the call wing into 750.00, set the put wing with cushion above 731.00, and size standard given Standard Size. Defend if SPY breaches 752.94 with VVIX expanding.

What it means for your trading

Iron condor on 30-45 DTE is the highest-EV expression at score 42; the 30-scored put spread is the directional backup, while naked strangles get vetoed by the short-gamma tape.

Actionable Summary

Trade the regime, not the headlines. With SPY at 749.74 wedged beneath the gamma flip at 752.94 and dealers carrying -$16.05B net GEX, the cleanest expression is a Iron Condor on 30-45 DTE, anchored above the 750 charm pivot. Forward vol geometry is Steep Contango and VVIX sits Low at 89.43 - carry is intact, sizing is Standard Size.

Defend if SPY breaches 752.94 lower with VVIX confirming through triple digits - that is the regime-shift tell, not the headline. The 750.00 call wall is the upside cap; the 731.00 put wall is the downside circuit-breaker. Regime label is Elevated / Watchful with a half-life of 15 sessions - sticky, not transient. Patience pays.

Avoid naked strangles into hostile vanna and charm, single-name short premium against the AI/megacap theme, and any length-extension into vol given negative-gamma microstructure. Cross-asset is Aligned: this is an equity-microstructure story, not a macro shock.

What it means for your trading

Deploy Iron Condor on 30-45 DTE around the 750 pivot; defend below 752.94 with VVIX confirming. Regime is Elevated / Watchful and sticky - avoid naked vol and AI-complex single-name short premium.

AI optimism overriding geopolitical risk is the macro permission slip for the current vol-seller regime - confirms why MOVE stays subdued despite Middle East headlines.

ECB tightening commentary directly affects USD/rate vol transmission into US equity vol - a hawkish ECB into a hawkish Fed sets up cross-asset vol divergence trades.

UK gilt yields backing off multi-decade highs takes a tail off global rates vol - supportive for MOVE staying low and for risk-asset carry trades broadly.

ECB hike conviction even with Iran peace deal removes the dovish off-ramp markets were partially pricing - bond vol implication and EUR cross flows worth monitoring.

Strait of Hormuz commentary keeps oil-vol tail alive - relevant for energy single-name vol and as the one genuine geopolitical tail still in the system.

Dollar steady despite faltering Iran peace hopes is the cleanest tell that the headline-risk channel is closed for now - FX vol confirms equity vol's complacency.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 752.94 against a spot of 749.74. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.35% with a volatility risk premium of 2%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.14. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime