Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

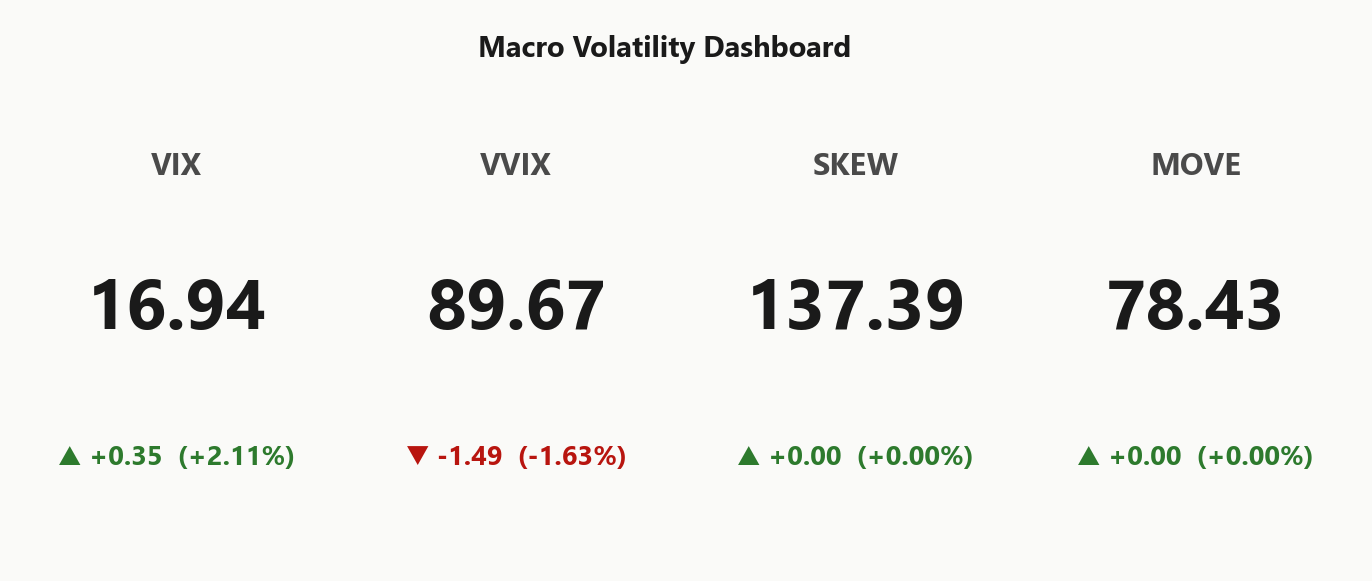

SPY closed at 750.18 in a negative-gamma regime with net GEX at -$15.69B - dealers short gamma means intraday moves get amplified rather than mean-reverted. Key levels: call wall at 751.00, put wall at 731.00, gamma flip at 752.95 - spot sits below the flip, so dealer hedging amplifies directional moves. Dealer positioning is hostile on the downside: net vanna at -$48.54B means a vol pop forces dealers to sell delta, and net charm at -$406.7M adds late-day pressure into close. Vol read: VIX at 16.94 with VIX9D at 14.69 and VIX3M at 19.87 = Contango, with VVIX at 89.67 signaling vol-of-vol is quiet. VRP of 1.94% vol points sits above HV20 at 10.41 - IV is rich to realized, structural carry is there. Regime assessment: Elevated / Watchful with half-life of 15 sessions and only 0.05 probability of moving to panic in 5 sessions. Bottom line: harvest the contango via Iron Condor in the 30-45 DTE window, but cut size if spot breaks below the put wall at 731.00 - that's where the vanna accelerant kicks in.

Negative gamma across complex with VIX at 16.94 in steep contango - fragile but carry-favorable

SPY closed at 750.18 with dealers short gamma across the index complex - net GEX at -$15.69B means moves get amplified, not dampened. The VIX term structure is in Contango with VIX at 16.94 and VIX3M at 19.87, so vol sellers still get paid carry while VVIX at 89.67 stays subdued. The tension: contango says sell vol, but short-gamma positioning says size down and respect levels.

Regime Assessment

Regime reads Elevated / Watchful with VIX at 16.94 parked in the watchful band - not panic, not complacency, but the zone where dealer hedging asymmetries start to matter more than carry math. The cross-asset tape is Aligned: SPY, QQQ and IWM are all sitting in negative_gamma, so no index hedges the others and correlation risk is the dominant exposure.

Transition odds are the tell. Probability of escalating to panic over the next five sessions sits at 0.05 - low, but non-zero given short-gamma positioning below the flip. Probability of de-escalating to a low-vol regime over ten sessions runs 0.45, and the regime half-life of 15 sessions confirms this state is sticky. Don't fade it on the first VIX uptick; the base rate says we stay here.

Signal color is Yellow - harvest the contango, respect the pivot, size for the regime you're in rather than the one you want.

What it means for your trading

Regime is Elevated / Watchful with VIX at 16.94 and a 15-session half-life - sticky, carry-favorable, but not a green light to press.

Trading readVIX modestly up, VVIX down, SKEW unchanged, MOVE flat - these aren't confirming each other. The divergence between VIX rising and VVIX falling says vol-of-vol isn't worried, even as headline VIX drifts up.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

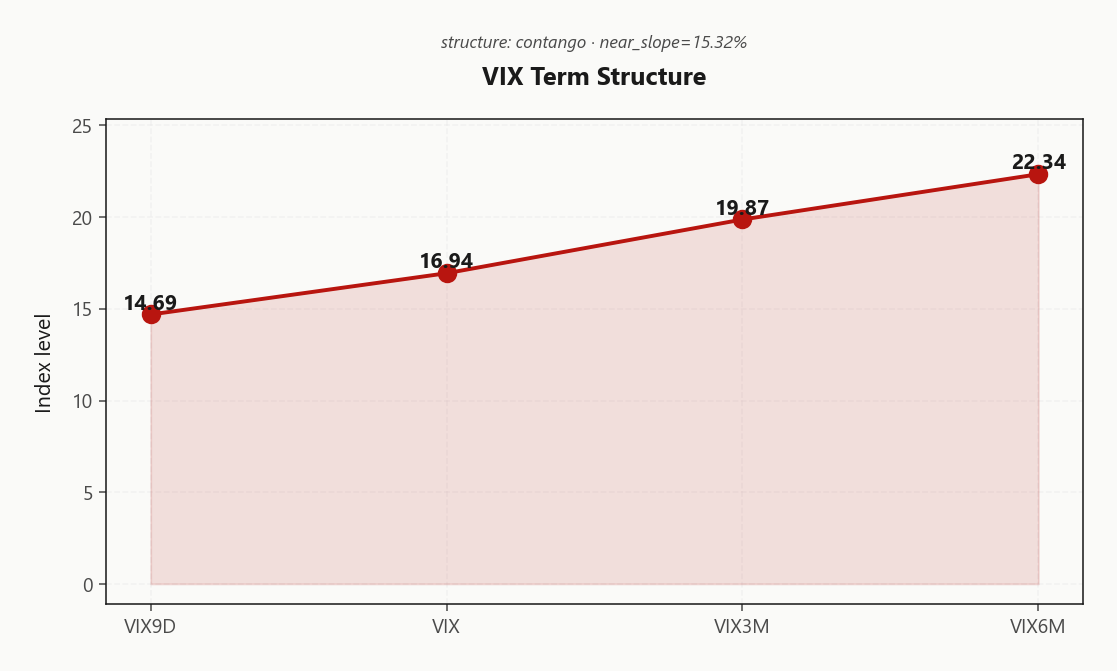

Forward Vol Geometry

The VIX complex prints a textbook upward stack: VIX9D at 14.69 sits cleanly under spot VIX at 16.94, with VIX3M at 19.87 and VIX6M extending to 22.34. Near slope of 15.32% ratifies the Contango read and the Steep Contango regime tag - no near-term event premium is being demanded, the curve is paying systematic sellers to be patient.

The interesting tell is in the forwards. Implied 21.1835679242 on the 30→60 leg is where the carry-to-realized edge is cleanest, while the 24.5628642467 kink into the back end says distant uncertainty is being marked up - tails are bid even as the near calendar prices benign. That asymmetry is the trade: harvest the belly, leave the wings alone.

Operationally, Steep contango - vol sellers favored - front-leg selling into back-leg ownership captures the roll while it stays this shape. The lead warning is slope inversion: if VIX9D crosses above VIX, the contango trade dies before the print does. Until then, the regime is yours to rent.

What it means for your trading

Curve geometry favors systematic vol sellers in the Steep Contango regime, with the 30→60 forward at 21.1835679242 marking the cleanest harvest window. Watch VIX9D versus VIX as the single tripwire - inversion ends the trade.

Trading readSteep upward slope from VIX9D to VIX6M = no near-term event premium and rolling carry available for VIX futures sellers. As long as VIX9D stays below VIX, the contango trade keeps paying.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.35% prints meaningfully above HV20 at 10.41, with VRP at 1.94% vol points confirming options are paid rich to actual tape movement. The carry trade is structurally live - this is the textbook setup where systematic vol sellers earn the premium, provided sizing respects the short-gamma backdrop.

HV60 at 14.78 sitting above HV20 tells the deceleration story: realized has been cooling from a prior regime, and the market hasn't fully repriced. That asymmetry between trailing realized and forward implied is exactly where the edge lives - IV is anchored to a regime that the tape has already left.

Skew at 1.8% shows a moderate put bid, not panic. Smile ratio at 1.16% says the wings are paying up while the body sits cleaner - a profile that favors defined-risk structures over naked vol selling. Section reads Vrp Active; harvest the carry, but let the wings be your friend, not your trade.

What it means for your trading

VRP at 1.94% with IV at 12.35% over HV20 at 10.41 is the structural case for short-vol - size controlled, wings owned.

Skew Convexity

The wing structure is textbook ordered: 13.33% on the quarter-delta put prices above ATM at 12.2%, which itself prices above the quarter-delta call at 11.53%. No inversion, no kink - just clean downside skew with steepness measured at 1.8% vol points. The smile ratio at 1.16% confirms what the levels imply: this is structural hedging demand, not panic bid.

Read the wings independently. The put side is paying enough to make naked short premium uncomfortable, especially with dealers already short gamma below the flip. The call wing, by contrast, is flat-to-suppressed - there is no upside conviction premium being paid, which removes the case for ratio structures leaning long-call. The asymmetry tilts the trade construction toward defined-risk spreads where the long wing finances the short, rather than naked legs that pick up the full skew tax.

Section signal reads Skew Steep - the wing bid is real but ordered, the regime is Negative Gamma, and the path of least resistance is to harvest the skew via spreads, not sell it outright.

What it means for your trading

Ordered downside skew with the put wing at 13.33% over ATM 12.2% and a smile ratio of 1.16% argues for spread structures over naked short puts - the wing bid is hedging demand, not capitulation, and defined-risk captures the skew without paying the convexity tax.

Vol-of-Vol Structure

VVIX at 89.67 sits on the calm side of the distribution, with the tape printing a -1.63%% session move - vol-of-vol is cooling, not coiling. The VVIX/VIX ratio at 5.29 reads Low, which is the market's way of saying it isn't pricing a binary outcome into the front of the curve. No fat tail bid, no convexity scramble - just an orderly vol surface that lets premium sellers operate without paying up for jump insurance.

With VIX itself at 16.94 and the term structure in Contango, the carry case is intact and the vol-of-vol read removes the usual size constraint. Signal color prints Green, and sizing guidance lands on Standard Size for short-vol structures - meaning the desk can run normal clips on iron condors and put-spread sales rather than scaling down for a bimodal regime that isn't there. The watch is for VVIX/VIX expanding back toward the upper band; until then, the vol-of-vol greenlight stands.

What it means for your trading

VVIX/VIX at 5.29 in the Low band supports Standard Size for short-vol books - no jump premium being paid, so size short vol like the regime is benign even while spot respects the gamma flip.

Dispersion Spread

The index complex is fanned out: SPY ATM IV at 12.35% sits well inside QQQ at 19.85% and IWM at 21.63%. That spread is the tell - single-name vol is doing the heavy lifting in the high-beta sleeves while SPY rides the correlation dampener. Dispersion is wide, idiosyncratic risk is being repriced name-by-name, and the broad index is the cleaner expression of the carry trade rather than the basket of underliers.

SPY VRP at 1.94% vol points is where the risk-adjusted edge lives - paid for index optionality with correlation working for the seller, not against. Contrast IWM VRP at 0.34%: razor-thin, with realized doing most of the work the premium ought to cover. Russell vol selling is not a trade here; the implied isn't compensating for the realized churn underneath. Section signal reads Moderate.

Operationally: harvest the index VRP, skip the single-name and small-cap legs. The dispersion picture says the basket is calmer than its parts - which is exactly when index vol-selling outperforms component vol-selling on a Sharpe basis.

What it means for your trading

Wide SPY-vs-QQQ-vs-IWM IV spread with SPY VRP at 1.94% flags index as the preferred vol-sell vehicle; IWM VRP at 0.34% is too thin to underwrite, so concentrate the carry in SPY and leave Russell alone.

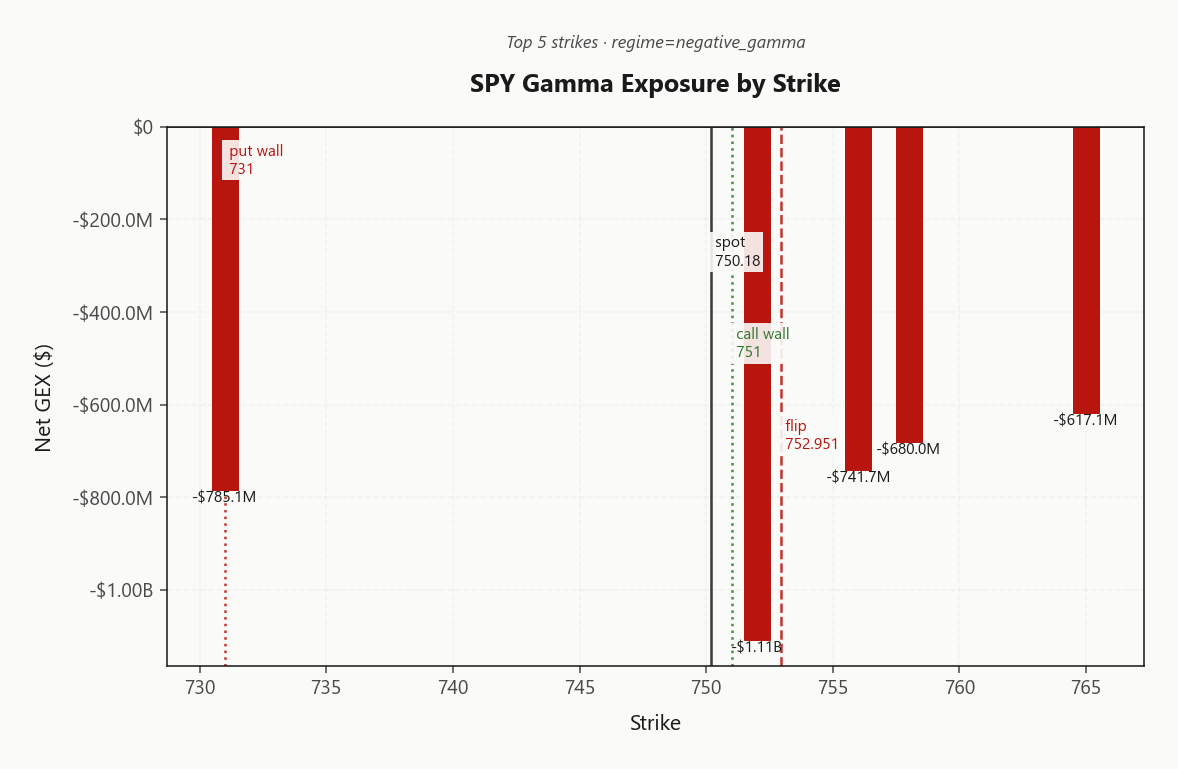

Liquidity & Microstructure

The strike map is unambiguous: the highest OI strike at 765 sits as the magnet above spot, while the gamma flip at 752.95 hovers just above the call wall at 751.00. With spot below the flip and the regime stamped Negative Gamma, dealer hedging is procyclical in both directions - rips chase, dips accelerate.

The top strike at 752.00 anchors the book with -$1.11B of net GEX, reinforcing the call wall as the immediate upside cap. Downside, the put wall at 731.00 is the first level where dealer flow flips supportive - break it, and the vanna accelerant at -$48.54B kicks the slope steeper.

Trade the band, not the breakout: respect the flip at 752.95 as the regime hinge, and treat the OI magnet at 765 as a destination only if dealers get squeezed long-gamma through the wall.

What it means for your trading

Spot below the flip at 752.95 with heavy OI overhead at 765 means dealer hedging amplifies, not dampens - the put wall at 731.00 is the line where the vanna accelerant engages.

Trading readNegative GEX clusters around current spot mean dealers are forced sellers on dips and forced buyers on rips - moves amplify rather than mean-revert. The call wall at 751.00 is the first ceiling; the put wall at 731.00 is the first floor where flow flips supportive.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks are stacked against the tape. Net vanna at -$48.54B is deeply negative - any uptick in implied forces desks to sell delta into weakness, mechanically amplifying any downside impulse. Net charm at -$406.7M compounds the bias, with time decay biasing dealer flow short into every session close.

The pivot that matters is 751 - a Call Wall sitting 0.1093070996 from spot, with current bias reading Neutral. Above it, charm flow stabilizes; below it, vanna becomes the accelerant. The gamma flip at 752.95 remains the regime switch - spot trades beneath it, which is why hedging is procyclical rather than dampening.

Vanna at -$48.54B and charm at -$406.7M point the same way - a vol pop or a late-day drift below 751 turns dealers into forced sellers. Respect the pivot; the gamma flip at 752.95 is where flow inverts.

Cross-Asset Confirmation

Cross-asset tape is Aligned, not diverged - and that's the tell. MOVE sits flat at 78.43 while VIX drifts higher; the bond market is refusing to ratify equity stress, which historically caps the depth of any vol pop driven purely by index hedging flow.

QQQ at 729.72 and IWM at 290.62 both trade below their respective gamma flips in the same negative_gamma regime as SPY - no index offers a hedge against the others, so correlation risk dominates and dispersion trades lose their cushion. Fear & Greed at 61 reads Greed: sentiment hasn't capitulated, which removes the contrarian bid that would normally cap downside vol.

Net: aligned short-gamma posture across the complex with rates calm and sentiment still constructive - fragile, but not the geometry of a panic. Vol sellers keep the carry; size to the weakest link, not the headline.

What it means for your trading

Cross-asset tone reads Aligned with MOVE flat at 78.43 and F&G at Greed - equity short-gamma is the lone stress vector, not a rates-or-credit-led unwind. Trade the carry, but respect that QQQ and IWM offer no diversification today.

Scenario EV

Scoring lands on Iron Condor at 35, comfortably ahead of the put spread alternative at 23. The structure earns it: ATM IV at 12.35% prints rich to HV20 at 10.41, the VRP carry is live, and the wings cap the negative-gamma tail that naked vol selling would leave open. VRP assessment reads Unknown, but the index dispersion versus QQQ at 19.85% and IWM at 21.63% confirms SPY is the clean harvest vehicle.

Deploy in the 30-45 DTE window - long enough to monetize theta and the forward 30→60 implied at 21.1835679242, short enough to sidestep event drift baked into the Contango curve. Wings belong beyond the call wall at 751.00 and the put wall at 731.00, giving the structure room outside the dealer-flow inflection zones. Size normal - VVIX at 89.67 and a VVIX/VIX ratio of 5.29 support Standard Size, with no bimodal jump being priced.

What it means for your trading

The Iron Condor at 35 is the cleanest expression of rich IV plus contango carry, deployed in 30-45 DTE with wings outside 751.00 and 731.00. Standard sizing applies while the VVIX/VIX ratio sits at 5.29 - cut risk fast if that ratio re-rates higher.

Actionable Summary

Trade: harvest the contango via Iron Condor in the 30-45 DTE window, with wings beyond the call wall at 751.00 and the put wall at 731.00. The regime reads Elevated / Watchful with a half-life of 15 sessions - sticky enough to underwrite carry, fragile enough to demand discipline.

Watch: the charm pivot at 751 (Call Wall, current bias Neutral) is the line where dealer flow flips. Avoid: naked short puts under 731.00 - net vanna at -$48.54B turns a vol pop into forced dealer delta supply. Skip IWM single-leg vol selling outright; VRP at 0.34% is too thin to compensate.

Size:Standard Size - VVIX/VIX ratio at 5.29 says vol-of-vol is quiet and short-premium can run standard book weight.

What it means for your trading

Sell index VRP via Iron Condor in 30-45 DTE, sized standard against the 751 pivot, and stand down on naked downside under 731.00 where the vanna accelerant kicks in.

Middle East airline cancellations resurface geopolitical tail risk and crude/transports sensitivity right as VIX ticks up - explains the persistent skew bid even in contango.

ECB signaling a near-certain rate hike resets the global rates path - explains why MOVE has held firm and why long-dated SPY IV stays bid on the curve.

Iran-war-driven hit to German economic recovery surveys is the quiet macro datapoint that should keep European equity hedges bid into Europe's session.

ECB hawkishness persisting even with an Iran peace deal means the global rate cushion isn't coming - keeps the long-dated VIX curve elevated.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 752.95 against a spot of 750.18. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.35% with a volatility risk premium of 1.94%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.94. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime