Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

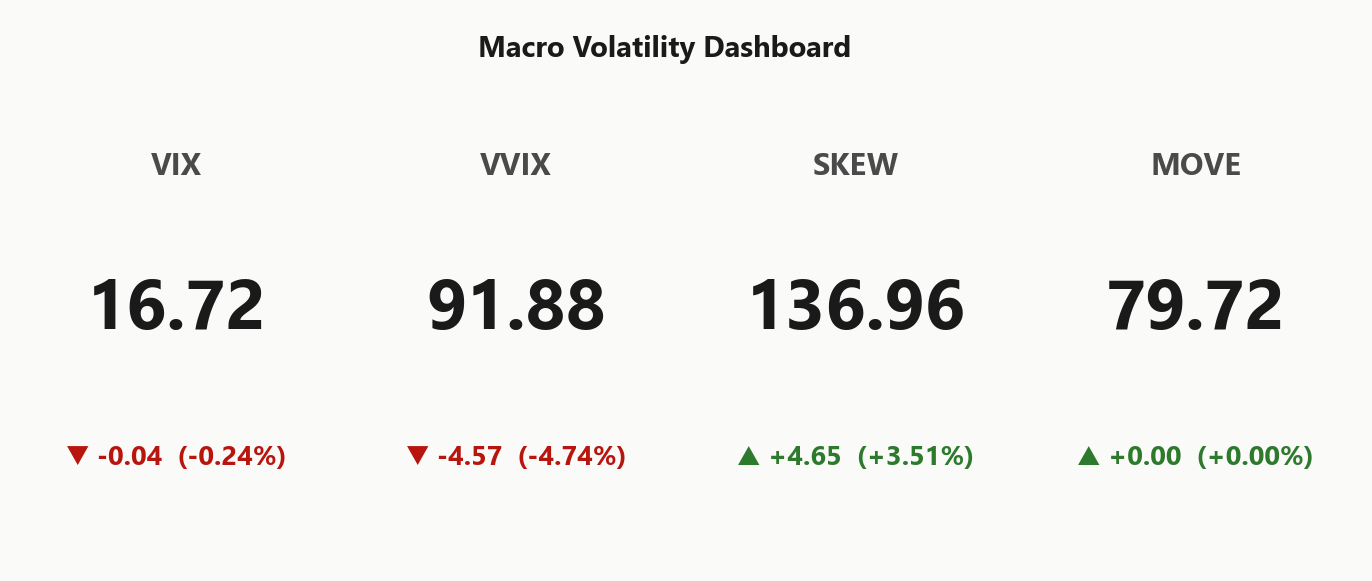

SPY trades at 747.41 in a Positive Gamma regime with net GEX of $10.59B - dealers are long gamma and dampening intraday range. Call wall sits at 750.00 and put wall at 730.00, with the gamma flip at 735.96 - spot is 0.3472013166% from the Call Wall pivot, leaving a deep cushion before flow flips hostile. Net vanna -$277.63B and charm -$371M read mildly negative - a vol spike would push dealers to sell delta, but with VVIX at 91.88 the vol-of-vol channel is quiet. VIX prints 16.72 with VIX9D 14.08 under VIX3M 20.00 - Steep contango - vol sellers favored, structural carry is live. VRP runs 2.32% vol points rich to 20-day realized, confirming options are well bid versus actual movement. QQQ aligned with SPY, IWM net GEX -$151.4M is the one soft node beneath the complex. Bottom line: fade strength into 750.00, lean on iron condors in the 30-45 DTE pocket, and keep tail protection cheap while VVIX is asleep.

SPY at 747.41 sits comfortably above the gamma flip with dealers long gamma - moves get dampened and walls hold. VIX term structure is in steep contango (Steep contango - vol sellers favored) while VVIX prints normal, so vol sellers are paid carry without paying up for jump risk. IWM net GEX skews slightly negative beneath the index complex, the one fragile node worth watching if breadth deteriorates.

Regime Assessment

Regime reads Elevated / Watchful with VIX anchored at 16.72 - not the low-vol carry paradise, not panic, but the watchful middle where carry still pays and tails still matter. Cross-asset complex sits Aligned in positive gamma, SPY above flip at 735.96, VIX curve in Steep contango - vol sellers favored - the structural backdrop confirms the regime label rather than fighting it.

Half-life clocks 15 sessions, which means this state is sticky - multi-day persistence is the base case, not a fade-fast tape. Transition probabilities tell the asymmetry: 0.05 chance of jumping to panic over the next week - low but non-zero, which is exactly why cheap tail protection stays on even with VVIX at 91.88. Meanwhile 0.45 probability of relaxing to low-vol over ten sessions is the meaningful drift - odds favor the regime softening into calmer carry rather than breaking hostile.

Trade the persistence, hedge the tail.

What it means for your trading

Regime is Elevated / Watchful at VIX 16.72 with a 15-session half-life - size carry trades to the persistence, keep cheap tails on for the 0.05 jump-risk residual.

Trading readVIX easing, VVIX easing harder, SKEW elevated, MOVE flat - confirming alignment, not divergence. The only watch item is SKEW - tail demand persists even as headline vol drops.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

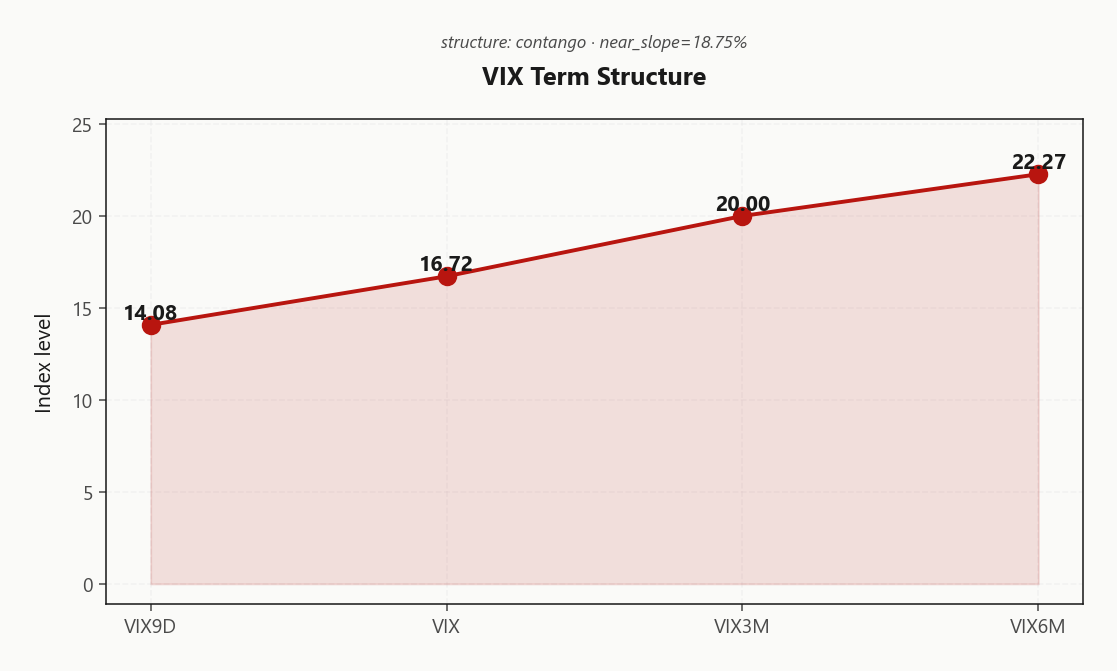

The VIX curve prints textbook Contango from front to back - VIX9D at 14.08 sits well under spot VIX at 16.72, with VIX3M ramping to 20.00. No event premium is being built into the front end; the belly is where forward vol prices richest, and that is where sellers are paid to wait.

Front-month futures carry a basis of 19.62% over spot at 20.00 - clean roll-down for systematic shorts. The Steep contango - vol sellers favored regime concentrates the harvest in the 30 - 60 DTE pocket, where calendar shorts and condor wings clip the steepest decay without paying up for jump risk further out the curve.

Structural Steep Contango of this shape historically persists ten to fifteen sessions absent a shock - half-life favors leaning into the trade rather than fading it. Lean short vol in the belly, locate wings around the 30 - 45 DTE zone, and let the curve do the work.

Trading readVIX9D under VIX under VIX3M under VIX6M - steep contango pays the seller in the belly. Curve says no near-term event premium priced; carry trade is live.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV prints 12.7% against 20-day realized at 10.38 - the gap is the harvest, and at 2.32% vol points the VRP is active but not extreme. This is sustainable carry, not a blow-off setup that mean-reverts against the seller in a session.

The tell is the term structure of realized itself: HV60 at 14.82 sits well above HV20 at 10.38, meaning recent tape has decelerated versus the trailing two months. Short-vol structures are being paid the regime-normalization premium - implied is anchored to a hotter recent past while spot delivers calmer prints.

QQQ widens the lens: VRP runs 2.74% vol points, materially richer than SPY's 2.32%. Tech complex offers more harvest per dollar of risk - locate condor wings in QQQ for premium, SPY for liquidity, and let the cross-index spread do the work.

What it means for your trading

VRP at 2.32% vol points with HV60 above HV20 confirms vol sellers are being paid on regime normalization, not catching a falling knife - and QQQ's richer 2.74% spread is where the cleanest harvest sits.

Skew Convexity

The quarter-delta skew prints 2.28% vol points with puts at 11.87% bid versus ATM 10.82%, while calls trade through at 9.59%. This is systematic protection demand, not panic - the down-wing is paid up in an orderly bid, the up-wing trades at a discount to the body. No melt-up convexity being chased here, no crash hedge being torched either.

Smile ratio at 1.24% clears the wings-rich threshold, meaning convexity is priced at a premium to the body on both tails. The implication is structural: favor put spreads over naked puts for downside expression - you are short the rich wing as part of the package rather than paying up for it. Naked premium on the put side bleeds against the smile.

The mirror trade: with call-side skew discounted and no upside conviction priced, vanilla calls are the cheap directional vehicle if a desk actually wants long delta. Sell the bid wing in spreads, buy the discounted wing outright - the smile geometry pays you to express the view that way rather than the other.

What it means for your trading

Skew at 2.28% with smile ratio 1.24% reads as ordered hedging - express downside via put spreads to harvest the rich wing, and use outright calls for any upside conviction since the call-side trades cheap to ATM.

Vol-of-Vol Structure

VVIX prints 91.88, easing -4.74%% on the session - the vol-of-vol channel is quiet, not asleep. The VVIX/VIX ratio at 5.50 sits squarely in the normal band, meaning the options-on-VIX market is not building a jump-risk premium beneath the headline tape. That is the missing piece the carry trade needed: steep contango pays you, and vol-of-vol isn't quietly repricing the convexity bill behind your back.

Sizing guidance therefore reads Standard Size - no half-sizing tax on short-vol structures, no defensive haircut on the iron condor book. The Normal vol-of-vol regime is the green light that pairs with the Steep Contango term structure, and absent that pairing the contango carry would be a trap.

The single tripwire: VVIX through 110. Above that level the carry regime fractures, the bimodal jump bid returns, and the negative-vanna book in SPY becomes the accelerant. Until then, deploy full size into the 30-45 DTE pocket and stop apologizing for the trade.

What it means for your trading

Vol-of-vol Normal at ratio 5.50 validates Standard Size on short-vol structures - the contango carry is not being secretly taxed by jump-risk premium.

Dispersion Spread

Cross-strike and cross-expiry dispersion sits modest while index VRP runs active - index ATM IV at 12.7% reads reasonable against the single-stock complex, with cross-strike dispersion at 77.89 and cross-expiry at 2.83. The lens favors selling index vol over single-stock vol - the term and skew surface offer cleaner harvest than chasing single-name strangles into an idiosyncratic tape.

The constraint is correlation: mega-IPO chatter and post-earnings residual flow in AAPL, NVDA, and MSFT raise dispersion risk in individual names where index-level VRP doesn't pay you to absorb the headline. Don't fight that with SPY structures - let condors in 30-45 DTE harvest the index premium and leave single-name event windows alone. Cross-asset tone Aligned across SPY/QQQ/IWM confirms the index-vol-selling thesis without single-name overlay.

What it means for your trading

Sell index vol via condors in the 30-45 DTE pocket where dispersion is modest and VRP active - avoid single-name strangle structures where mega-IPO and chip-cycle headlines distort the idiosyncratic surface.

Liquidity & Microstructure

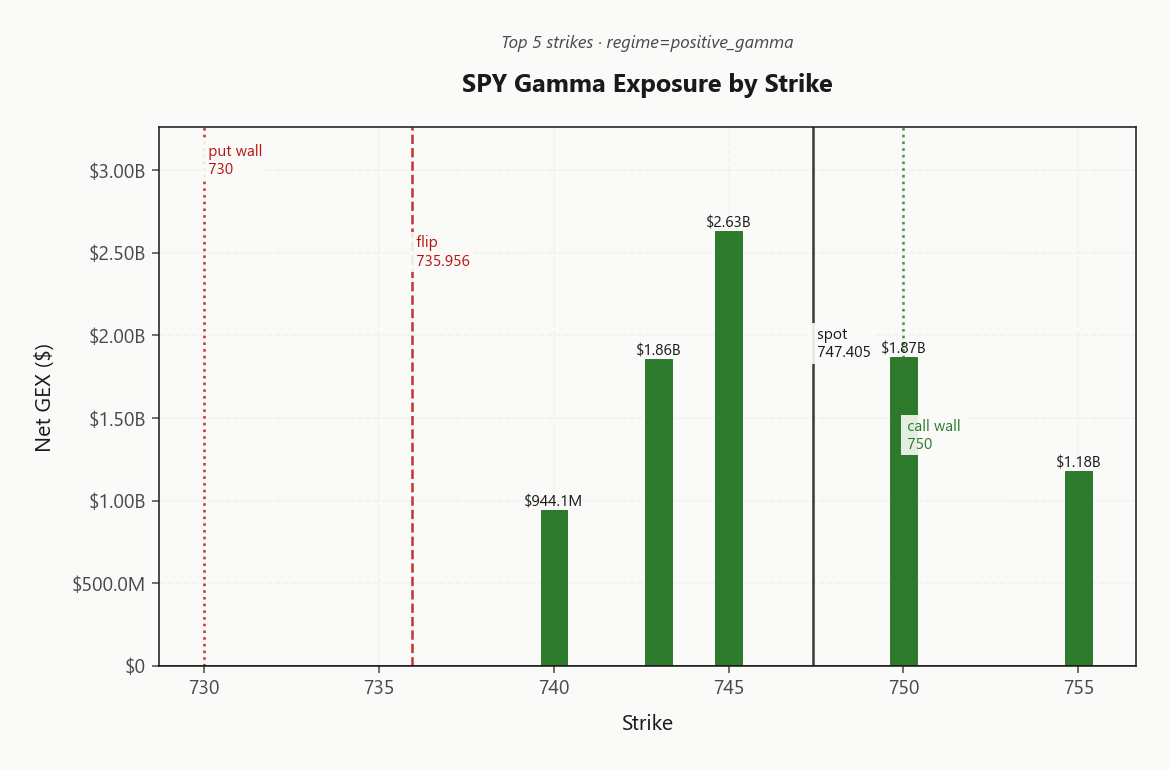

SPY's gamma book is stacked tight in the 745.00 - 750.00 corridor, with the highest-OI strike anchored at 700 and the top GEX node carrying $2.63B of dealer gamma. That concentration above spot is what's compressing intraday range - dealers are forced sellers into strength and forced buyers into weakness inside the 730.00/750.00 band.

The gamma flip sits at 735.96, a long way beneath the print - that's the demarcation between today's dealer-buying-support regime and the dealer-selling-amplification tape that lives below it. Until spot threatens that level, mean reversion is the default and walls hold. 0DTE accounts for 39.8% of total gamma - meaningful pin pressure into the close, but not dominant enough to override structural positioning.

Trade implication: fade strength into 750.00, lean on the cushion above flip, and treat any break of 735.96 as the regime tell rather than noise.

What it means for your trading

Dense OI in the 745.00 - 750.00 corridor pins the tape while the flip at 735.96 leaves a deep buffer - mean reversion owns the day until that level is threatened.

Trading readGamma stacks heavily on the call side above spot in the 700 - 750.00 corridor - dealers dampen rallies into the wall and the flip is a long way down, so mean-reversion plays own the day until spot tags 750.00.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna prints -$277.63B and net charm -$371M - both negative, both quiet for now. The asymmetry to flag: a vol spike from here forces dealers to sell delta, turning any IV jolt into a downside accelerant rather than a damped move. Keep cheap OTM puts on; the body of the smile says they aren't expensive relative to the wing demand that would re-rate fast.

Charm bleed tilts the late-tape distribution lower if no upside catalyst materializes - dealers shed long delta into the close mechanically. The single pivot is the Call Wall at 750: above it dealers cap rallies, below it they buy dips. Current bias reads Neutral with spot 0.3472013166 away - close enough to matter, far enough that the regime hasn't flipped.

IWM net vanna and net chex pull opposite to SPY - small-cap is the release valve and the fragility node. If breadth cracks, it shows there first.

What it means for your trading

Regime is calm but loaded with a vol-up-equity-down accelerant via negative vanna; trade the Call Wall at 750 as the line between dealer support and dealer sell pressure, and keep tail protection on while it's cheap.

Cross-Asset Confirmation

Cross-asset tape confirms the equity-positioning read rather than a credit or macro stress one. MOVE sits at 79.72 - rates vol contained, not bleeding into equity - while Fear & Greed prints 58 (Greed), supportive without tipping into euphoria that would invite a contrarian fade.

The index complex is Aligned: QQQ at 719.58 and IWM at 284.35 both trade above their respective flips, mirroring SPY's Positive Gamma posture. No divergence story to lead with - the carry regime is reinforced across the board, with IWM's softer GEX node the only fragility to keep on the radar if breadth deteriorates.

The distinction matters: credit shocks compound, positioning shocks mean-revert. Today's tape is the latter. Lean into the iron condor thesis, keep tail protection cheap, and watch IWM - not SPY - for the first crack.

What it means for your trading

Cross-asset tone reads Unknown with MOVE contained and sentiment supportive but not euphoric - an equity-positioning regime that pays carry, not a macro-stress regime that demands defense.

Scenario EV

The structure board scores Iron Condor at 58, clearing the put spread alternative by a meaningful margin. Active VRP at 2.32%, VVIX parked at 91.88, and a Steep contango - vol sellers favored term structure assemble the textbook condor setup - sellers are paid carry without paying up for jump risk, and the Standard Size read greenlights full-size deployment rather than half-clip caution.

Sweet spot sits in the 30-45 DTE pocket, where contango roll-down prints steepest and 0DTE gamma noise stays out of the trade. Anchor short legs at 750.00 on the upside and 730.00 on the downside - the OI architecture already does the pinning work - with longs placed outside to cap the tail.

Pass on the alternatives: short strangles pair uncapped wings with negative vanna at -$277.63B, the wrong asymmetry into a vol-up tape; calendars need a term-structure dislocation the curve isn't offering. Defend the thesis below 735.96.

What it means for your trading

Iron condor scores 58 as the cleanest expression of active VRP plus quiet vol-of-vol - short the 30-45 DTE wings at 750.00/730.00, full size, and walk away from strangles where negative vanna punishes uncapped tails.

Actionable Summary

Bottom line: deploy Iron Condor in the 30-45 DTE pocket, short legs anchored at 750.00 and 730.00. Fade strength into the call wall; defend below the flip at 735.96. Keep cheap OTM put protection on - net vanna at -$277.63B means a vol spike forces dealers to sell delta into the move, and that's the asymmetric tail you don't want naked.

The pivot at 750 is the regime-break line - spot sits 0.3472013166% away with bias Neutral. Regime reads Elevated / Watchful with a 15-session half-life, so the carry trade should persist multiple sessions absent a shock.

Avoid: naked short strangles in IWM - net GEX -$151.4M offers no dealer cushion below. Skip short calendars; the term structure is already Steep Contango, no event premium left to harvest. Watch: VVIX through 91.88 and any SPY break below 735.96 as the two early warnings the regime is rolling.

What it means for your trading

Deploy Iron Condor between 730.00 and 750.00 in the 30-45 DTE window, keep cheap tail protection on, and treat a break of 735.96 or VVIX expansion as the regime-rolling tell.

Mega-IPO wave (SpaceX, OpenAI) at record valuations is the classic late-cycle signal - institutional positioning will pre-hedge before the floats, watch for stealth put bids in QQQ even with VVIX asleep.

NVDA earnings beat is the single largest input to mega-cap gamma rebuild in today's data - confirms why AAPL/NVDA/MSFT dominate the mover board and why SPY call wall sits where it does.

IEA warning of oil 'red zone' by July re-introduces a tail risk that the current contango regime is NOT pricing - keep cheap macro tail protection on even as VRP says sell vol.

Billionaire family offices doubling down on semis during Iran-war pressure is the positioning tell - confirms the mega-cap tech gamma stabilization visible in today's mover data.

Flash PMI holding steady reinforces the 'no recession scare' read that underpins steep contango and the carry regime - bullish for the iron condor thesis through next refresh.

Cramer's 'tech leadership has changed' frame matters because it explains why mover GEX is concentrated in semis/AI infrastructure rather than software - relevant to dispersion trade selection.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 735.96 against a spot of 747.41. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.7% with a volatility risk premium of 2.32%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.72. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime