Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

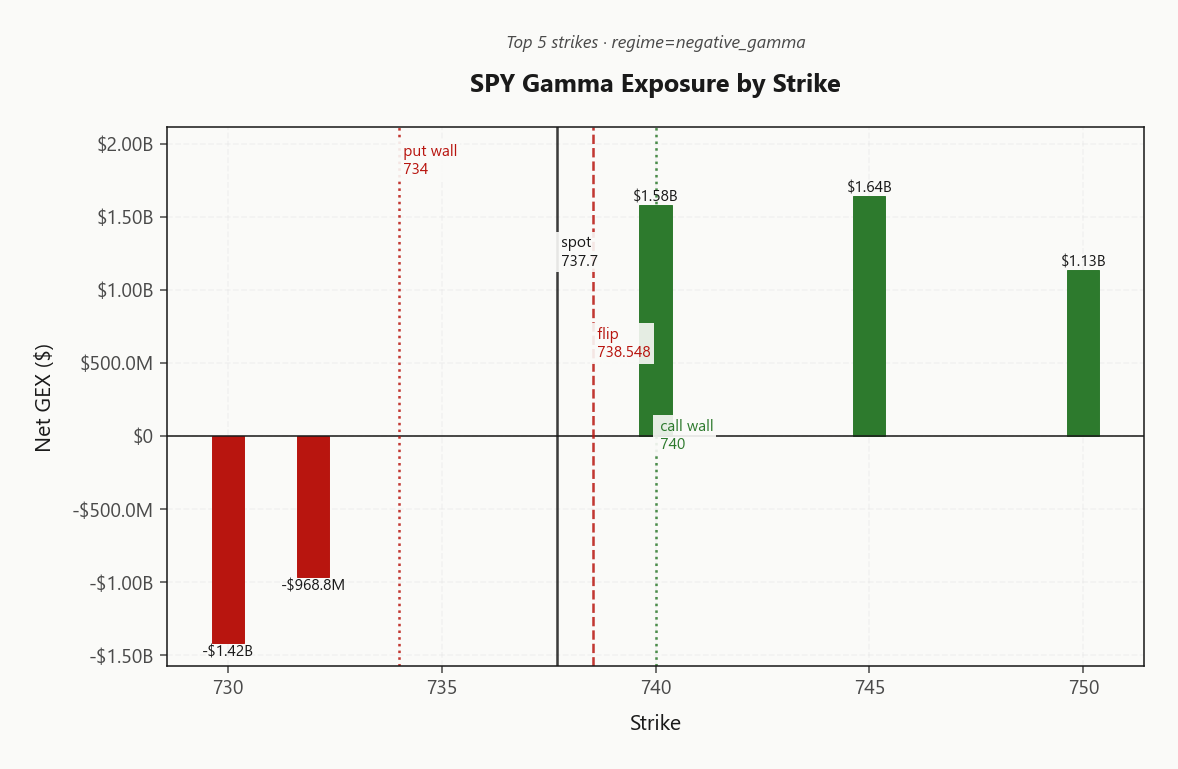

SPY at 737.70 sits fractionally below the gamma flip at 738.55, putting dealers in negative-gamma territory with net GEX at -$2.88B - moves get amplified, not dampened. Call wall stacks at 740.00, put wall at 734.00, and the heaviest OI cluster sits at 700 - a magnet well below spot. Dealer vanna at -$213.81B and charm at -$890.3M both lean destabilizing: vol up means dealers sell delta, time decay pushes them to sell into close. VIX at 17.72 with the term structure in steep contango (15.14 → 22.81) keeps the carry trade alive, and VRP at 2.95% confirms options remain rich to recent realized. QQQ diverges with positive gamma above its flip at 599.78 - tech is stable, broad index is fragile. Bottom line: fade strength toward 740.00, respect 738.55 as the pivot, and harvest premium with iron condors in the 30-45 DTE window.

SPY pinned just below gamma flip at 738.55 - destabilizing bias with QQQ diverging long-gamma

SPY sits a hair below the gamma flip at 738.55 in negative-gamma territory while QQQ holds positive gamma above its flip - a textbook intra-complex divergence that biases the tape toward chop with downside acceleration risk. VIX term structure in steep contango and VVIX at 96.45 leaves vol sellers paid, with the iron condor scoring best across structures. The trade: harvest VRP in the 30-45 DTE bucket, respect the charm pivot, and size standard until VVIX flags otherwise.

Regime Assessment

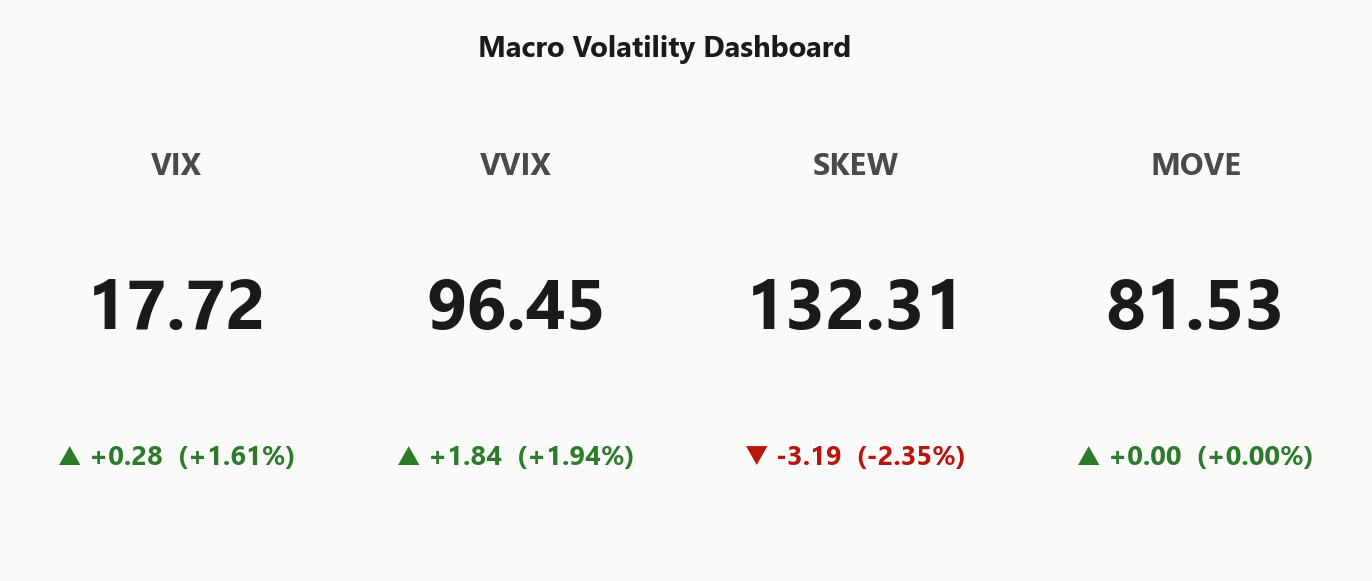

Regime reads Elevated / Watchful with VIX anchored at 17.72 - elevated enough to keep premium sellers paid, not stressed enough to chase tail bids. The current state classifies as Elevated: sticky vol with no panic confirmation from the cross-asset tape.

Transition probabilities are the tell. Move-to-panic over five sessions sits at 0.05 while move-to-low across ten sessions runs 0.45 - the distribution leans toward compression, not breakout. Half-life of 15 sessions means this is not a fast mean-reverter; the carry trade has runway, and rolling short-vol structures forward gets paid through multiple cycles before the regime decays.

Bottom line: this is a harvest tape, not a hedge tape. Standard sizing approved, iron condor in the belly favored, and only a clean break of the VIX regime - not an intraday spike - flips the playbook.

What it means for your trading

Regime is Elevated / Watchful at VIX 17.72 with a 15-session half-life - sticky, slow-decaying, and structurally favorable for premium harvest until the transition probabilities shift.

Trading readVIX, VVIX, and SKEW all sit in normal-elevated range while MOVE at 81.53 stays subdued - equity vol elevated without credit/rate confirmation. Classic isolated-equity setup, not a macro shock; mean reversion is the higher-probability path.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

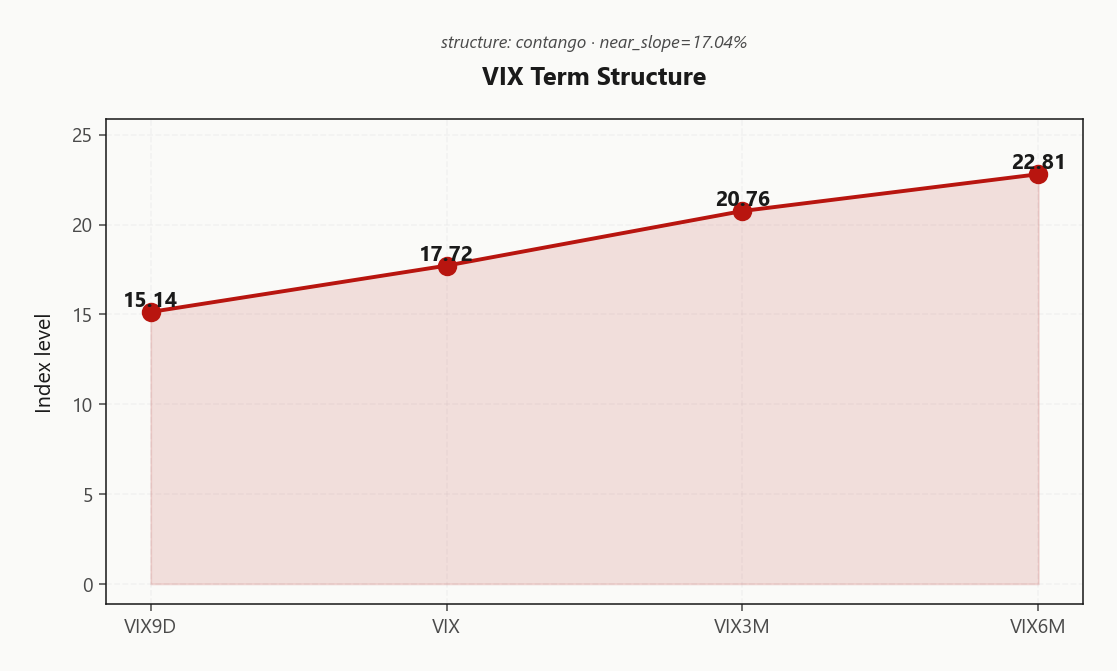

Term structure prints clean Contango with VIX9D at 15.14 well under spot VIX at 17.72 - front-end suppression is doing the heavy lifting and no event premium is being paid into the near calendar. VIX3M at 20.76 extending to VIX6M at 22.81 keeps the carry curve intact through the back, locking in Steep contango - vol sellers favored as the operative regime.

Near-term slope at 17.04%% pays vol sellers in the belly, with forward 30→60 implied at 22.1239056227 rolling to 24.6903746428 at 60→90 - the slope is steepest exactly where the harvest window sits. Calendar structure favors selling the front against the belly; outright premium sales cluster best in the 30-45 DTE bucket where roll-down does the work.

What it means for your trading

Steep contango with Steep Contango regime confirms the structural vol-selling carry - front suppressed, back elevated, belly pays. Concentrate short premium in the 30-45 window and watch for backwardation as the carry-break tell.

Trading readContango with near-slope at 17.04%% gives vol sellers a tailwind - the curve is paying you to roll short vol forward. Watch for backwardation as the early warning: that's when the carry trade breaks.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 13.72% sits comfortably above HV20 at 10.77, with VRP at 2.95% stamping a clean premium-to-realized cushion. The IV-RV spread reads Moderate Premium - options are pricing more vol than the tape is delivering, and the short-premium harvest case is open for business.

The realized term tells the deeper story: HV20 below HV60 (10.77 vs 14.9) means the recent tape is decelerating against its own longer window. RV is fading while IV stays sticky - that's the textbook setup where carry expands, not compresses. RV5 at 13.26 against RV20 at 10.77 seals the read.

Net: options remain rich to deliverable vol, harvest favored, lean into the belly where slope pays the most.

What it means for your trading

VRP at 2.95% with realized decelerating below HV60 keeps short-premium structures paid - sell vol into the steep-contango curve, respect the gamma flip as the regime switch.

Skew Convexity

The quarter-delta skew is doing its job in an ordered way: put-25d IV prints at 20.24% against a call wing at 18.85%, with ATM anchored at 18.4% - squarely below the put bid. Skew-25d at 1.39% says downside protection is being accumulated methodically, not chased; this is institutional hedging, not retail panic.

Smile ratio at 1.07% keeps the wings asymmetric - the put side carries a real premium while the call wing sits flat, signaling no upside conviction being paid for. That asymmetry is the trade: naked downside is expensive, naked upside is cheap, and the structure rewards spreading the put wing rather than buying it outright.

Operationally: put spreads finance better than long puts here, call ratios get attractive against the flat upper wing, and any tail hedge should be expressed as a spread rather than a single leg. With dealers destabilizing below the flip, paying full freight for the put wing is the wrong way to harvest the skew.

What it means for your trading

Skew at 1.39% with smile ratio 1.07% reflects orderly downside accumulation, not panic - favor put spreads over naked puts, and lean into call ratios where the upper wing offers no convexity premium.

Vol-of-Vol Structure

VVIX prints 96.45 against VIX at 17.72 - squarely in Normal territory with the ratio at 5.44. No bimodal jump premium is being paid here; the tail bid that defines a half-size regime simply isn't on the tape.

That matters for sizing. Vol-of-vol sitting normal while VRP stays active means the carry trade is structurally intact - sellers of premium aren't getting paid to flinch. Sizing guidance reads Standard Size: deploy full notional on iron condors in the 30-45 DTE window without the haircut a stressed VVIX would demand.

The caveat is the charm-pivot bias at Destabilizing - vol-of-vol normal doesn't neutralize the destabilizing dealer profile below the flip. Harvest the carry, but watch VVIX as the canary: any lift toward the elevated band is the first signal to cut size before the contango breaks.

What it means for your trading

VVIX at 96.45 keeps the VVIX/VIX ratio at 5.44 in Normal range - Standard Size approved, vol-selling carry intact with no tail-bid frenzy to fade.

Dispersion Spread

Index ATM IV at 13.72% sits inside QQQ at 20.25% and well inside IWM at 20.79% - the cross-strike dispersion read at 80.71 confirms single-stock vol is carrying a real premium over the index. Small-cap risk is priced widest, with IWM ATM at 20.79% reflecting the broader negative-gamma fragility outside mega-cap leadership.

The dispersion trade - long single-name vol, short index - is paid on paper, but the cleaner harvest for VRP-focused books is still SPY/SPX over single-name. Cross-expiry dispersion at 2.61 says the term-curve premium is modest; the edge sits in the strike axis, where index suppression from passive flow keeps SPY ATM cheap relative to constituents.

Bottom line: harvesters who want to avoid idiosyncratic earnings and headline risk get more reliable carry selling 13.72% than chasing the dispersion leg. Reserve single-name vol shorts for names with cleared catalysts; everywhere else, the SPY iron condor in the 30-45 window is the dominant expression.

What it means for your trading

Dispersion is paid with single-stock vol rich to SPY at 13.72% and IWM widest at 20.79%, but the cleanest VRP harvest remains SPY/SPX over single-name.

Liquidity & Microstructure

The book is unambiguous: heaviest OI stacks at 700, a magnet sitting well below spot, while the gamma flip at 738.55 hovers a hair above the current print. That leaves SPY pinned in the destabilizing zone - dealer hedging amplifies, not dampens, every tick until the flip clears.

Walls frame the playable range: call wall at 740.00 caps strength, put wall at 734.00 is the gravity well on weakness. The largest single-strike net GEX print sits at 745.00 with $1.64B of positive dealer gamma - the level rallies have to chew through before the regime flips supportive.

Trade the range, don't fade the breakout: above 738.55 dealer flow dampens, below it amplifies. Wing iron condors outside the walls and respect the flip as the binary pivot.

What it means for your trading

Spot trapped below the flip at 738.55 with OI gravity at 700 means dealer flow is pro-cyclical until SPY clears the inflection - fade strength into 740.00, respect 734.00 as the cushion.

Trading readSpot sitting fractionally below the gamma flip at 738.55 with negative net GEX means dealers amplify every move down and chase rallies - the call wall 740.00 is the magnet on strength, put wall 734.00 is the gravity well on weakness. Trade the range, don't fade the breakout.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order greeks line up against the tape. Net VEX at -$213.81B means any vol spike pushes dealer delta more short - a reflexive sell loop that accelerates downside rather than damps it. Net CHEX at -$890.3M reinforces the bleed: charm decay forces hedgers to lean into the offer as the session ages, so closes skew heavy absent a flip-clearing rally.

Trade the level, not the narrative. Until SPY reclaims 738.55, treat strength as fade material into 740.00 and avoid naked downside chases - the pro-cyclical hedging flow is doing that work for you. Clear the flip and the entire complexion of dealer flow inverts.

What it means for your trading

Net VEX at -$213.81B and CHEX at -$890.3M both lean destabilizing with bias tagged Destabilizing - 738.5482998005 is the binary level that flips dealer flow from hostile to supportive.

Cross-Asset Confirmation

The cross-asset tape refuses to confirm the equity-microstructure fragility. MOVE at 81.53 sits subdued - bond vol is calm, credit isn't flinching, and the rate complex is offering zero corroboration that SPY's flip-zone wobble is anything more than a positioning artifact. This is an isolated dealer-book story, not a macro shock in the making.

Risk appetite leans the other way: Fear & Greed prints 60 at Greed, and QQQ at 708.89 holds comfortably above its flip in positive-gamma territory. Tech leadership is absorbing the risk while broad-index dealer flow turns hostile - the textbook Qqq Heavier divergence with QQQ carrying the heavier long-gamma book.

IWM at 277.99 mirrors SPY's negative-gamma profile, so the fragility is real on the small-cap and broad index legs - but with bond vol quiet and sentiment greedy, the higher-probability path is chop and mean-reversion, not a macro-driven cascade. Pair long QQQ against short SPY vol while the divergence holds; that's where the cross-asset edge lives.

What it means for your trading

MOVE at 81.53 and Fear & Greed at Greed refuse to confirm SPY's flip-zone fragility - this is isolated equity microstructure, not a macro shock, with QQQ's long-gamma stability the dominant cross-asset tell.

Scenario EV

Edge of the morning is Iron Condor, scoring 37 against put-spread alternatives - the trifecta of active VRP at 2.95%, VVIX holding Normal at 96.45, and term structure in Contango from 15.14 to 22.81 is exactly the carry setup condors are built for.

Optimal window sits at 30-45 DTE - far enough out to harvest the steepest belly slope, short enough to clear the destabilizing 0DTE charm bleed flagged by net CHEX at -$890.3M. Place wings outside the call wall at 740.00 and the put wall at 734.00; let the structural magnets do the defending. Sizing is Standard Size - no half-clip needed with vol-of-vol benign.

The catch: spot under the flip at 738.55 with bias Destabilizing means entries respect the pivot - fade strength into the call wall, don't chase weakness through the put wall. QQQ long-gamma above 599.78 is the bid keeping the complex intact.

What it means for your trading

Iron condor at 37 is the cleanest VRP harvest in the 30-45 DTE window, with wings parked beyond the 740.00/734.00 rails. Standard sizing per Standard Size - the charm pivot at 738.5482998005 is the only level that flips the trade thesis.

Actionable Summary

Bottom line: harvest VRP with Iron Condor structures in the 30-45 DTE window, fade strength toward the call wall at 740.00, and treat 738.5482998005 as the directional pivot. With SPY printing 737.70 just below the flip and net GEX at -$2.88B, dealer flow amplifies rather than dampens - clearing the pivot flips the regime.

Place wings outside 740.00 on top and 734.00 below; size standard per Standard Size with VVIX at 96.45 and term structure Contango. Avoid chasing breakouts below the flip and half-size strangles - vanna at -$213.81B and charm at -$890.3M punish naked downside until SPY reclaims the pivot.

QQQ holding positive_gamma above its flip at 599.78 is the standing bid - express directional conviction as a SPY-vs-QQQ pair rather than outright. Regime tag: Elevated / Watchful.

What it means for your trading

Sell premium via Iron Condor in the 30-45 bucket, fade into 740.00, and pivot on 738.5482998005; pair-trade SPY-vs-QQQ for directional exposure while the intra-complex divergence holds.

Nvidia's blowout print is the morning's gamma-reset catalyst - index heavyweight delivering an AI-infra beat re-anchors the QQQ long-gamma read and explains the cross-asset divergence.

IEA flagging an oil 'red zone' by July with Hormuz still partially closed keeps a geopolitical risk-premium bid under crude - relevant for the energy sector and as a slow-burn tail risk priced into the back-end of the VIX curve.

Billionaire family offices doubling down on semis and energy during the Iran war confirms the smart-money positioning behind the AI-infra leadership Cramer flagged - supports QQQ's long-gamma stickiness.

Cramer's call that semis and AI-infra have replaced software as tech leadership is the structural backdrop for QQQ holding positive gamma while broad SPY sits negative - sector rotation, not broad risk-on.

Trump's 'may have to hit Iran harder' headline is the kind of binary geopolitical tape-bomb that justifies the VVIX bid and the persistent put-skew premium - keep tail hedges on a leash, not naked.

BoE's Bailey signaling time to gauge Iran-war impact is the policy template - central banks are in wait-and-see, which extends the VIX contango carry trade by a few weeks at minimum.

'Trump blinks as bond market bares its teeth' - credit/rate discipline is back as a constraint on the administration, which keeps MOVE subdued and prevents the equity vol spike from getting macro confirmation.

India T-bill yield surge on rate-hike expectations is an EM stress data point - worth watching as a leading indicator if MOVE starts to lift and the contango carry breaks down.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 738.55 against a spot of 737.70. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.72% with a volatility risk premium of 2.95%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.72. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime