Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

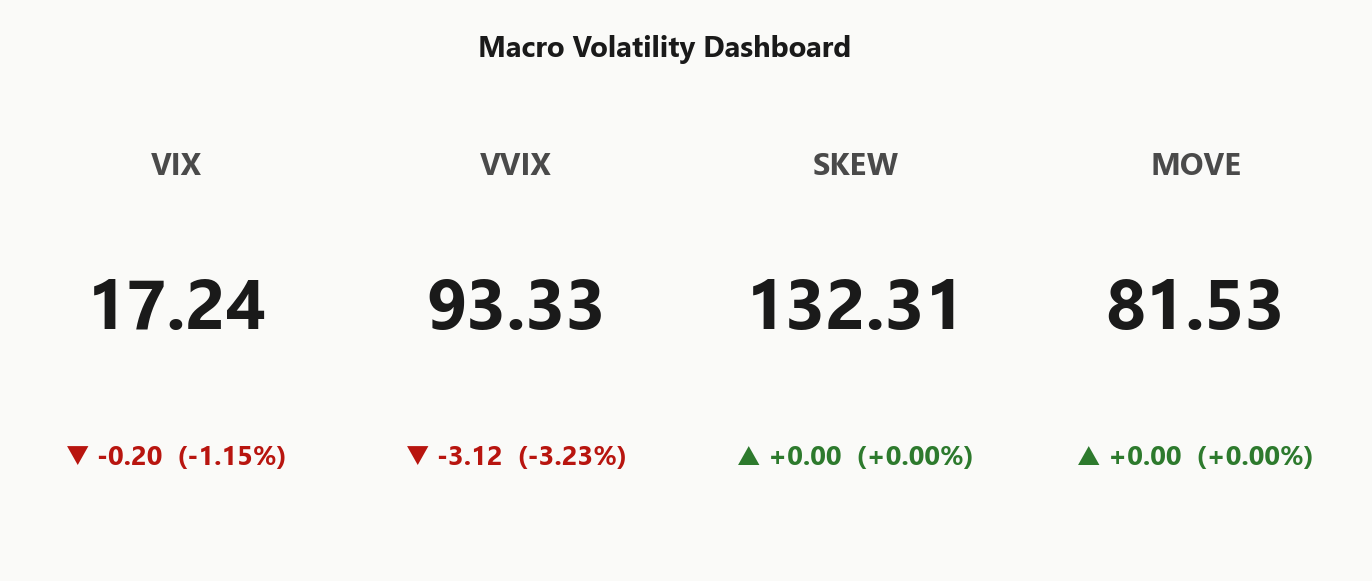

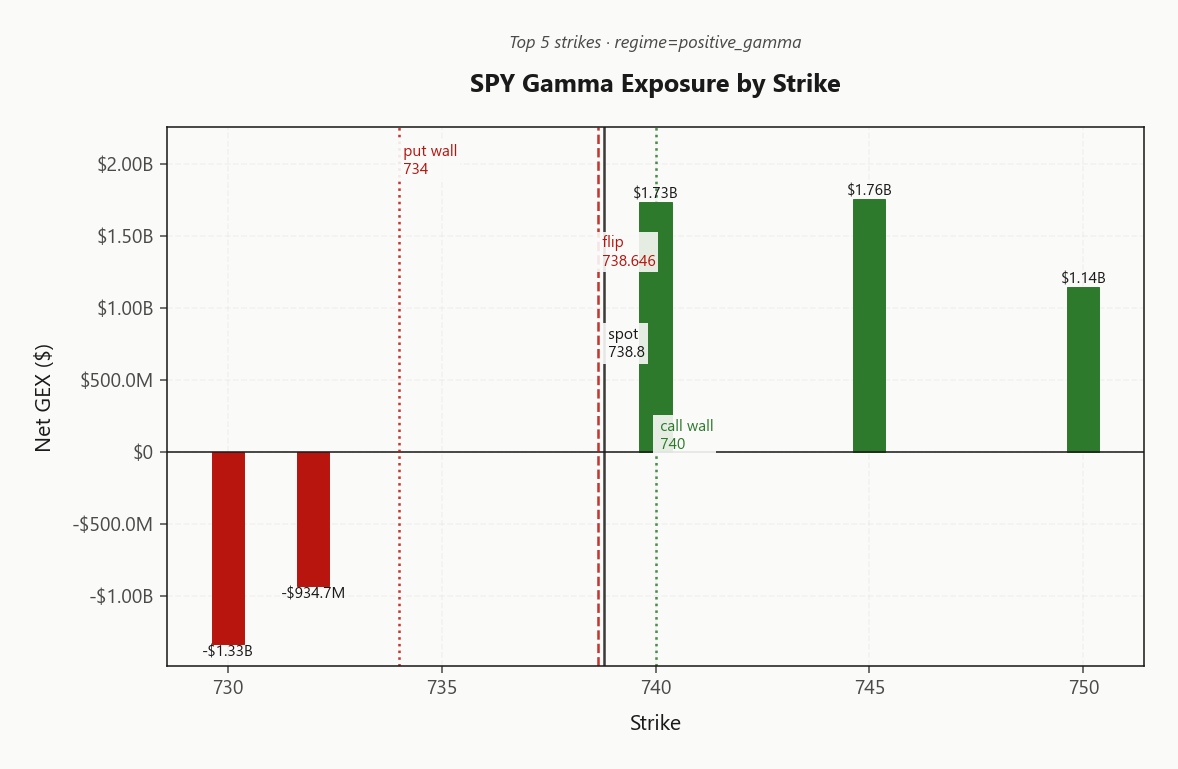

SPY trades at 738.80, sitting essentially on the gamma flip at 738.65 with regime Positive Gamma and net GEX of -$1.51B - dealers are barely long gamma, so a small downside push tips them short. Call wall at 740.00, put wall at 734.00, max pain at 720.00 - that gives you a tight 734.00 - 740.00 fade box for the session. Dealer vanna at -$223.65B is negative - a vol spike sells delta, accelerant on the downside - but charm at -$889.6M stays modest into the close. VIX at 17.24 with term structure Contango (VIX9D 14.69, 3M 20.47) and VVIX/VIX ratio 5.41 confirms benign vol-of-vol - VRP at 2.22% is harvestable. IWM at 280.16 sits below its flip 282.50 in Negative Gamma with negative VRP -0.55% - small-caps the fragile leg if breadth wobbles. Bottom line: sell premium via Iron Condor structures in SPY/QQQ 30-45DTE inside the walls; avoid naked IWM short vol - use defined-risk if you must play it.

Index complex in positive gamma with VIX in Steep Contango; IWM the lone fragile leg below flip

SPY trades right at the gamma flip 738.65 with dealers long gamma into walls at 740.00/734.00, while QQQ holds positive-gamma cushion above its flip. IWM is the divergent fragile leg - short-gamma below its flip with negative VRP - flagging small-cap idiosyncratic risk under an otherwise suppressive vol regime. VIX at 17.24 in steep contango with normal VVIX/VIX endorses size-on premium harvest with disciplined wings.

Regime Assessment

The regime classifier prints Elevated / Watchful with VIX anchoring at 17.24 - squarely in the Elevated band. This is the working middle: neither the compressed low-vol complacency that demands oversized harvest nor the dislocated panic state that mandates flat books. Signal color Yellow is the operator's instruction - engage the tape, but keep sizing one notch below maximum.

Transition math endorses leaning on the regime. Probability of escalating to panic over the next five sessions sits at 0.05 - low enough that short-vol structures aren't fighting the distribution. Probability of decaying to low over ten sessions runs 0.45, so the path to easier conditions is live but not imminent. Half-life of 15 sessions gives a workable trading horizon - long enough to underwrite 30-45DTE structures without betting against mean-reversion.

Operate the book: harvest VRP, keep wings disciplined, don't add gross on rallies. Defensive sizing is the price of staying paid through this band.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life and only 0.05 tail probability of escalation - sticky enough to lean on, but signal color Yellow mandates defensive sizing rather than full harvest.

Trading readVIX, VVIX, SKEW and MOVE all benign and confirming each other - no divergence to flag, regime is stable; the contradiction will come from IWM not the macro complex.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

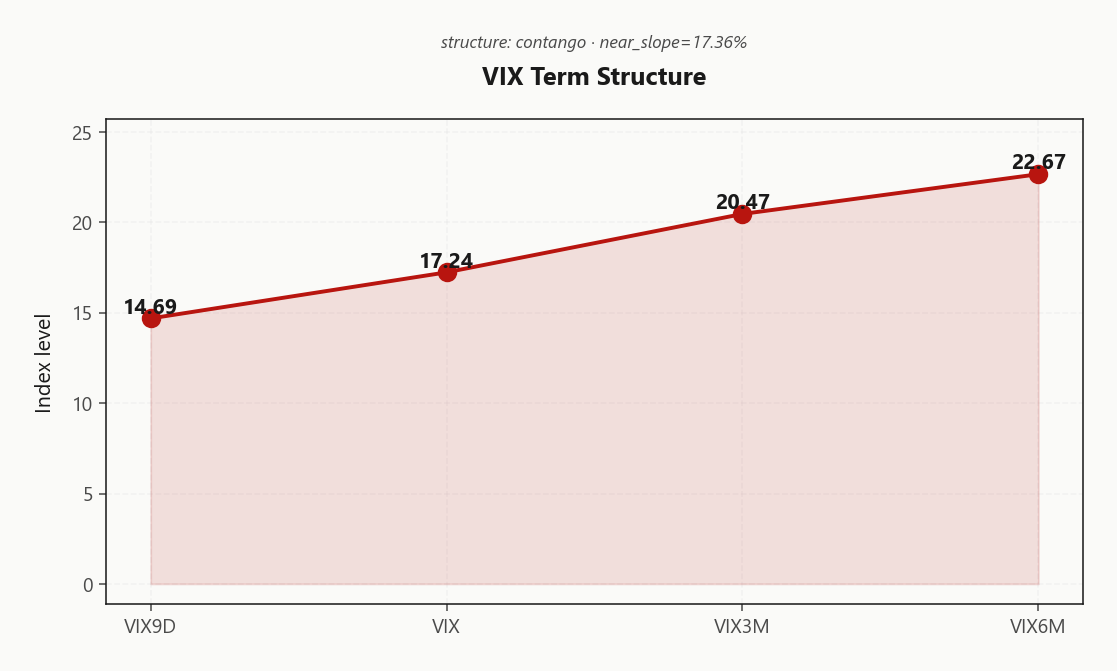

The term structure is in Contango from front to back - 14.69 below spot 17.24 below 20.47 below 22.67. That is the market explicitly refusing to pay any near-term event premium, and the near-slope at 17.36% is the cleanest carry signal we have printed this week. Steep contango - vol sellers favored.

The Steep Contango regime endorses structural short-vol carry, but the front leg at 14.69 is also the cheapest piece of the curve - selling it naked is asymmetric the wrong way. Express the carry through Iron Condor or calendar spreads that short the front belly and own the back. The forward strip from 20.47 to 22.67 is where defensive wings live cheaply.

Operate the 30-45DTE band - far enough out to harvest meaningful theta, close enough that the contango carry compounds before the long-dated wings start bleeding. Front-end 14.69 popping back toward spot is the early tell that the carry is breaking.

What it means for your trading

Steep Contango across the strip is the cleanest carry setup of the week; sell the front belly inside Iron Condor structures at 30-45DTE, not naked. Exit signal: 14.69 compressing toward 17.24.

Trading readSteep contango from 14.69 to 22.67 means market prices no event premium - vol-carry trade has its cleanest setup of the week.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.88% sits meaningfully rich to HV20 at 10.66 yet trades cheap to HV60 at 14.88 - the tape paid you over the smoother last month, but the two-month window remembers prior turbulence. VRP at 2.22% confirms a harvestable edge for short premium, but the gap is constructive rather than blowout. Size the harvest, don't gorge it.

The HV60 overhang is the discipline tell - wings are not free here, and structures that monetize the IV-RV gap without naked tail exposure deserve the bid. Iron condors and put spreads inside the walls fit; naked strangles do not.

The standout caveat sits in small-caps: IWM VRP at -0.55% is negative - you would be paying to take vol risk there. Keep premium selling concentrated in SPY and QQQ where the spread compensates; treat IWM as defined-risk only.

What it means for your trading

SPY VRP at 2.22% is harvestable but not extreme - disciplined short premium with real wings, not naked. Avoid IWM short vol outright: negative VRP at -0.55% pays you to take risk in the wrong direction.

Skew Convexity

Front-expiry quarter-delta skew prints 1.59% with put_25d at 18% sitting over ATM 15.99% and call_25d trailing at 16.41% - an orderly put bid, not a panic tail grab. Smile ratio 1.1% corroborates the read: hedges are being lifted methodically, downside is paid for, but the curve has not gone vertical.

The call wing is flat-to-inverted across the complex - nobody is paying up for upside, which is the cleanest tell that this is a hedging tape, not a chase tape. That asymmetry is structurally exploitable: long downside convexity should be expressed via put spreads rather than naked puts, financing the protection by selling the cheap call wing where skew refuses to bid.

Translation: own the put spread, sell the upside, let the skew shape pay for the hedge. Pure long puts overpay for a tail the market is not actually pricing in panic mode.

What it means for your trading

Skew at 1.59% with smile ratio 1.1% reflects orderly downside hedging while flat call wings make put spreads - financed by short calls - the structurally cheapest convexity available.

Vol-of-Vol Structure

VVIX at 93.33 against VIX 17.24 prints a ratio of 5.41 - squarely inside the Normal band. No bimodal pricing, no implied jump-risk premium baked into options-on-options. The vol-of-vol surface is not flagging a tape that wants to gap, and that is the green light to harvest premium at full clip rather than half.

Practically: Standard Size is the endorsed posture per signal_color Green. This is not a regime where defensive sizing is mandatory - the convexity charge embedded in VVIX is benign, so iron condor and calendar structures can be put on at standard notional without the half-size haircut you'd apply when VVIX/VIX runs hot.

The watch is asymmetric: if VVIX presses materially higher off 93.33 on a flat VIX, that decoupling is the early jump-risk tell - vol-of-vol leading vol is how dealers price tail before tail arrives. Until then, options on options remain cheap and the carry stays clean.

What it means for your trading

Vol-of-vol benign at Normal with ratio 5.41 endorses Standard Size; flag any sharp VVIX lift on a static VIX as the leading jump-risk signal.

Dispersion Spread

Index IV anchors near 12.88% with cross-strike dispersion at 75.12 - single-name correlation is loosening from the index complex, but the cross-asset regime stays Aligned at the headline level. The discordant note is IWM trading below its flip at 282.50 in Negative Gamma with VRP at -0.55% - small-cap idiosyncratic risk is the lone fragile leg under an otherwise suppressive vol tape.

That asymmetry dictates structure selection. Selling SPY and QQQ vol is the cleaner expression - VRP at 2.22% and 1.69% remains harvestable, dealer gamma in Positive Gamma dampens realized inside the walls, and dispersion is moderate rather than extreme, so single-name strangles don't out-earn the index condor on a risk-adjusted basis.

Iron condors on indices beat single-name strangles in this regime; index hedges work for SPY/QQQ exposures but not for IWM idiosyncratic tail - keep small-cap risk defined.

What it means for your trading

With dispersion at 75.12 and the cross-asset regime Aligned, index iron condors capture the cleanest premium while IWM's sub-flip fragility argues against any naked single-name short vol.

Liquidity & Microstructure

Open interest stacks heavily at 745.00 - the active call wall and dealer-flow magnet on any push higher - with a secondary cluster anchoring the 734.00 put wall. The aggregate OI center of gravity sits at 700, distant enough to be a slower-burn magnet rather than a session pin.

Spot is parked essentially on the flip at 738.65 - the level for the tape. Above it dealers dampen and the 734.00 - 740.00 band behaves as a fade box; below it they amplify and intraday range expands fast. Top-strike concentration of $1.76B at 740.00 caps upside chase, while the put wall is the structural floor - a break there is the regime-change trigger, not a level to fade.

Play the box: sell into 740.00, buy weakness toward 734.00, and treat any close below 738.65 as the cue to flatten short-vol exposure.

What it means for your trading

Microstructure is deep and well-defined - spot at 738.65 with walls at 734.00/740.00 gives a tradable fade box, but the flip itself is the knife-edge: lose it and dealer flow flips from dampening to amplifying.

Trading readDense positive-gamma stack between 734.00 and 740.00 makes that band a fade box - sell strength into the call wall, buy weakness near the put wall, only chase if the flip at 738.65 breaks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX at -$223.65B is the hostile leg of the book - a vol-up impulse forces dealers to sell delta, an accelerant that converts any orderly drift into a downside cascade. The Normal VVIX/VIX backdrop keeps that vanna ambush latent, not active, but the wiring is asymmetric: positive gamma cushions calm tape while negative vanna does the work the second realized picks up.

Charm at -$889.6M is modestly negative - late-session decay nudges dealer hedges to lean offered into the bell, the classic afternoon sell-then-stabilize profile rather than a directional shove. Pivot is the Gamma Flip at 738.6462449686; current bias is Supportive, and that label only holds while spot prints above it.

Trade it accordingly: harvest premium inside the walls while vanna stays dormant, but treat 738.6462449686 as the hard line - a break flips dealer flow from dampening to amplifying and turns the short-vol book against you in a single tick.

What it means for your trading

Vanna is the hidden short - positive gamma supports until vol rises, at which point negative VEX at -$223.65B forces dealer delta liquidation; the Supportive bias holds only above 738.6462449686.

Cross-Asset Confirmation

Cross-asset tape Aligned with MOVE at 81.53 sitting benign - no credit/rates impulse bleeding into equity vol, which is the precondition for leaning on the short-premium thesis at all. Fear & Greed prints Greed at 58, neither extreme nor contrarian - consensus comfort, not euphoria, not capitulation.

QQQ at 709.72 holds positive-gamma cushion above its flip and confirms tech leadership intact; SPY/QQQ regimes are aligned long. IWM at 280.16 is the lone discordant leg - below its flip in short gamma with negative VRP at -0.55%. Read this as equity-idiosyncratic small-cap fragility, not a macro/credit warning.

Operationally: index iron condors stay live, IWM short vol stays off the sheet. Trigger to upgrade hedges is 81.53 rising in lockstep with 17.24 - that joint move flips this from localized small-cap noise into systemic risk-off, and the carry trade breaks with it.

What it means for your trading

Cross-asset signals confirm a contained, equity-idiosyncratic regime - MOVE benign, sentiment Greed, indices aligned - with IWM the only fragile leg. Stay long premium-selling in SPY/QQQ; escalate hedges only if MOVE joins VIX higher.

Scenario EV

The scoring tape lands clean: Iron Condor wins with best score 44, comfortably ahead of the put-spread alternative at 31. Contango term structure, moderate-but-orderly skew, and positive index gamma combine to make the four-leg payoff the cleanest expression of the regime - wings finance themselves against flat call skew while the body harvests the 2.22% cushion.

Optimal DTE band 30-45 threads premium decay against event horizon without paying for tail convexity the market isn't pricing. Strangles are the inferior cousin here - hostile vanna at -$223.65B amplifies losses on any vol-up impulse, and naked short vol gets run over. Put spreads stay viable as the directional second choice if the 738.6462449686 pivot breaks.

Vehicle discipline matters: deploy in SPY and QQQ where gamma is Positive Gamma. Avoid IWM iron condors - negative VRP at -0.55% means you'd be paying to warehouse risk. VVIX/VIX at 5.41 endorses Standard Size.

What it means for your trading

Iron condors 30-45DTE on SPY/QQQ with strikes outside 734.00 - 740.00 is the trade; IWM stays off the menu.

Actionable Summary

Bottom line: harvest premium via Iron Condor structures in SPY and QQQ across the 30-45DTE window, short strikes pinned outside the 740.00 call wall and 734.00 put wall. Regime reads Elevated / Watchful with VVIX/VIX at 5.41, endorsing Standard Size - no half-size discount required.

Avoid naked short vol on IWM: VRP prints -0.55% and spot sits below flip at 282.50 in Negative Gamma - you are paid nothing to wear small-cap fragility. Finance SPY downside wings against the flat 16.41% call skew; the put-side bid at 18% stays orderly, not panicked.

Watch 738.6462449686 - break of that level flips dealer regime from Supportive to short-gamma accelerant and turns the iron condor against you fast. Exit short vol on the print, do not negotiate with it.

IEA 'red zone' July warning on oil is the macro tail risk vol sellers have been ignoring - backwardation risk in crude could re-rate equity vol mid-summer.

Cramer's confirmation that AI infra has replaced software as tech leadership matters for QQQ skew composition - concentrated leadership amplifies index gamma sensitivity.

India T-bill yields up 21bp on rate-hike expectations - EM rates volatility tends to bleed into DM equity vol with a lag, watch for confirmation.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 738.65 against a spot of 738.80. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.88% with a volatility risk premium of 2.22%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.24. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime