Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

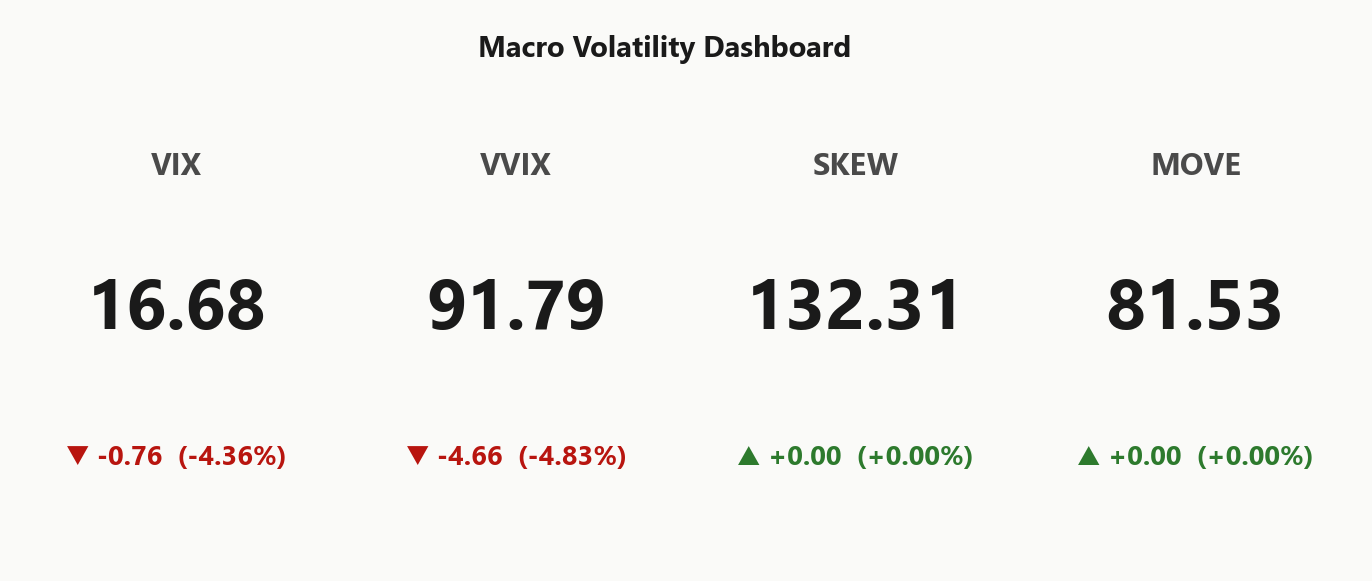

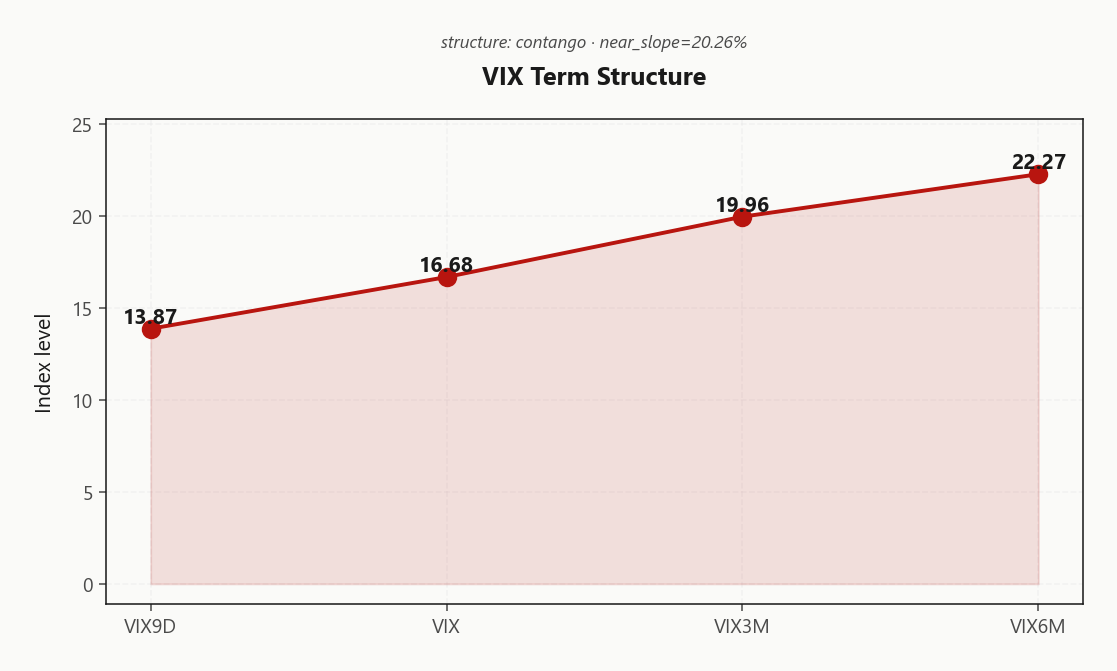

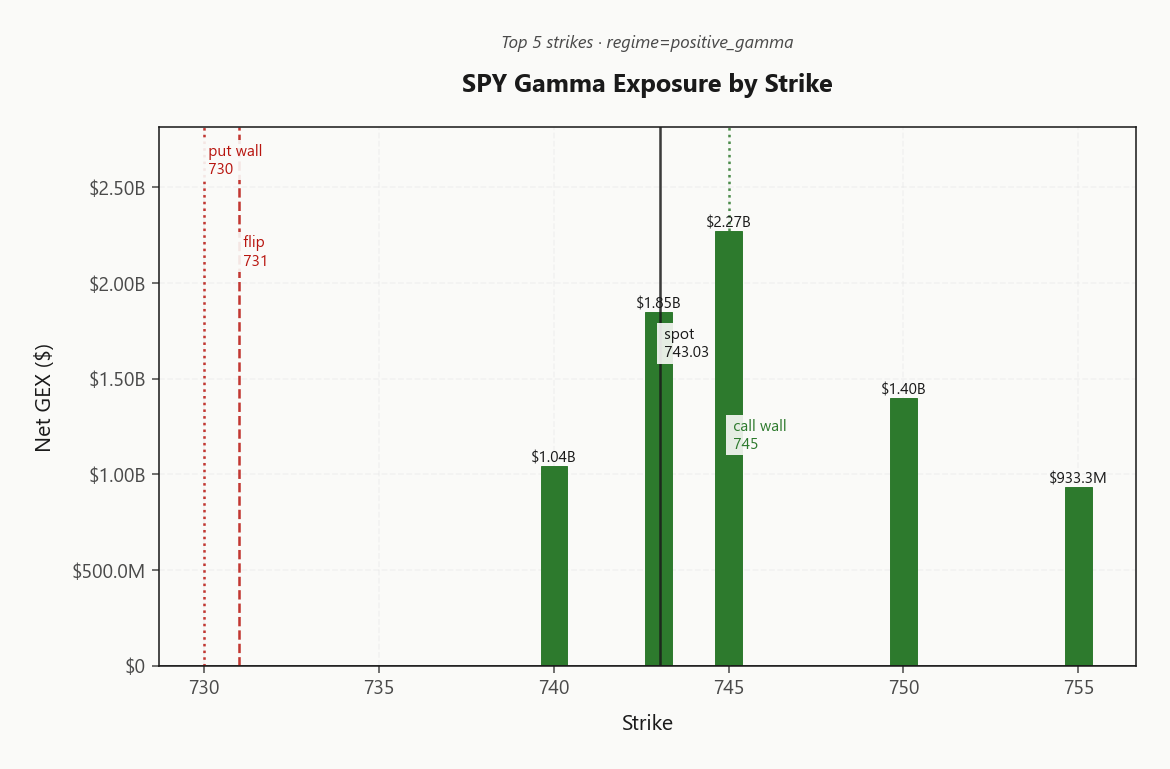

SPY closed at 743.03 with net GEX of $6.52B - firmly positive gamma, dealers dampening moves. Gamma flip sits at 731.00, call wall at 745.00, put wall at 730.00 - spot is pinned right against the upper magnet, where dealer flow turns from buy-the-dip to sell-the-rally. Vanna exposure of -$261.42B means a vol spike would force dealers to sell delta aggressively, so the cushion is conditional on VIX staying suppressed. VIX at 16.68 with VIX9D/VIX/VIX3M at 13.87/16.68/19.96 - steep contango, front carry rich. VRP of 2.34% vol points says options are paid handsomely over RV20 of 10.46. VVIX at 91.79 is benign - no jump premium being bid. Bottom line: sell vol structures (iron condors 30-45 DTE) over the call wall and below the put wall; avoid naked upside, the wall is the lid.

Positive gamma across index complex with steep VIX contango - mean-reversion regime intact

Index complex closes with dealers long gamma across SPY/QQQ/IWM and VIX in steep contango at 20.26%% slope - a textbook suppression regime. Vol-of-vol normalized at 5.50, VRP still paid over realized, and the scenario engine flags iron condors as the optimal structure. The single tension: SPY pinned right under its call wall at 745.00, where dealer flow flips from supportive to selling.

Regime Assessment

Tape sits in Elevated / Watchful with VIX printing 16.68 - squarely inside the elevated band, not the low-vol all-clear that pure carry-chasers want to see. Transition math is the punchline: panic probability over five sessions reads 0.05 while the drift-to-low odds over ten sessions sit at 0.45 - the regime is far more likely to bleed lower than break higher, but the bleed is slow.

Half-life of 15 sessions is the operative number. That stickiness is what gives the short-vol book its runway: the regime persists long enough to harvest forward carry in the 30-45 DTE bucket without needing a vol collapse to monetize. Cross-asset confirms - SPY/QQQ/IWM aligned long-gamma, VIX in Contango, and divergence reading Aligned.

Translation: harvest carry, keep a tail hedge live. Elevated-watchful is a sell-vol regime with a seatbelt, not a feet-off-the-brake regime.

What it means for your trading

Regime is Elevated / Watchful at VIX 16.68 - sticky over 15 sessions with panic-transition odds low, supporting short-vol carry while keeping tail hedges mandatory.

Trading readVIX down, VVIX down, MOVE flat, SKEW unchanged - all confirming risk-on, no divergence to flag. When the macro dashboard is this aligned, the regime call is high-conviction.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

Term structure is in Contango and steep enough to matter: VIX9D at 13.87 sits well below spot VIX at 16.68, with the 3M anchor at 19.96. The front is already discounting the calm - near slope of 20.26% confirms structural carry, and vol sellers are paid simply to let the curve roll down.

The richest pocket sits in the belly: the 30→60 forward implied prints 21.412407618, with the 60→90 stepping up to 24.3619416303 - that's where the eventual realized print historically undershoots hardest. Regime tag Steep Contango aligns with the scenario engine's optimal 30-45 DTE window for short-vol structures.

Trade the shape, not the level: sell the belly, stay short of the front-week noise, and watch VIX9D as the early-warning gauge - a lift back through spot VIX flips the carry signal and ends the roll-down trade.

What it means for your trading

Steep Steep Contango with VIX9D at 13.87 below VIX at 16.68 pays sellers to roll; the 30-45 DTE belly is the richest harvest zone.

Trading readSteep contango with the front discounting near-term calm - vol carry trade is paying. Slope this steep historically precedes either persistent calm or a sharp inversion; watch VIX9D for the early warning.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Implieds are sitting fat over realized: SPY ATM clears 12.8% against HV20 of 10.46, a 2.34% vol-point cushion that the tape simply isn't delivering. The derived signal flags Vrp Active - sellers carry the edge here, not the buyers.

The cone is decelerating, not accelerating: HV60 at 14.85 sits well above HV20, so the trailing window is fading off a hotter tape into something quieter. That's the tailwind for short-vol structures - you're paid forward while backward-looking realized cools into the print.

Cross-complex, the premium isn't uniform. QQQ VRP narrows to 1.97% and IWM thins out to 0.68%, so the cleanest real estate for harvesting carry remains SPY/SPX. Single-name short vol doesn't compensate for the idiosyncratic tail; concentrate the sell on the index where the premium is paid and the realized is cooperating.

What it means for your trading

Premium-to-realized at 2.34% vol points with HV60 above HV20 frames a textbook short-vol tailwind on SPY. Keep the harvest on the index - QQQ and IWM premiums don't pay enough for the single-name tail.

Skew Convexity

SPY's quarter-delta skew prints 0.62% with the put wing at 16.39% against an ATM print of 15.03% and the call wing nearly flush at 15.77%. The left tail is bid but ordered - insurance is being paid for, not chased. The call side is flat, confirming no upside scramble is being priced into the wing.

Smile ratio at 1.04% says the downside premium is modest, not panicked - a textbook hedged-not-hedging-now print. QQQ runs steeper at 2.48%, IWM at 1.98%, layering tech-tail and small-cap-tail bids on top of the index baseline. Cross-asset signal is Aligned; nothing in the wings is screaming.

Trade construction: put spreads dominate naked puts on cost-per-protection. The wing IV premium is real but the ratio is too flat to underwrite long single-leg vega. Sell the deep wing, own the body - fund tails with the skew, don't pay through it.

What it means for your trading

Skew at 0.62% with smile ratio 1.04% is steep but ordered - left tail bid, call wing flat. Put spreads structurally cheaper than naked tails; QQQ and IWM wings layer steeper for sector-specific hedges.

Vol-of-Vol Structure

VVIX prints 91.79 against spot VIX at 16.68, pegging the VVIX/VIX ratio at 5.50 - squarely in the Normal band. No binary jump premium is being bid into the wings; the second-derivative tape is calm, which validates the first-derivative call to be short vol.

VVIX bled another -4.83% on the session, confirming the risk-off premium is unwinding alongside spot VIX rather than hiding in the convexity. When vol-of-vol compresses in lockstep with VIX, dealers aren't pricing a fat-tail event - they're pricing mean reversion.

Sizing guidance from the regime engine: Standard Size. No haircut required on the iron condor book today - vol sellers don't need to half-size when the convexity market isn't paying for catastrophe. Watch for VVIX to lift independently of VIX; that's the early tell that the regime is about to break.

What it means for your trading

VVIX at 91.79 and the VVIX/VIX ratio at 5.50 sit in the Normal band - no jump premium bid, run Standard Size on short-vol structures.

Dispersion Spread

Index vol sits at 12.8% while 18.98% on QQQ and 20.89% on IWM stay meaningfully bid - a textbook dispersion print. The index surface is calm because the complex is Aligned on positive gamma and correlation suppression is doing its job; underneath, single-name vol is still pricing idiosyncratic earnings and headline risk that hasn't bled into the basket.

The signal reads Moderate: enough premium gap to keep dispersion sellers paid, not wide enough to chase. Translation - harvest the index leg, leave the single-name leg alone. Sell SPY/SPX vol where the VRP is healthiest and correlation is doing the dampening for you; avoid naked single-name short vol into the earnings tail where QQQ/IWM constituents still carry binary risk that isn't reflected in the index print.

What it means for your trading

Index IV at 12.8% vs single-name proxies at 18.98% and 20.89% says correlation is suppressing the basket while idiosyncratic risk lingers - favor SPY/SPX vol sales, skip the single-name leg.

Liquidity & Microstructure

The book is concentrated where it matters. 745.00 carries $2.27B of net GEX - the single heaviest dealer-long node on the chain and spot is parked right underneath it. That is the 745.00 call wall, and it is acting as a hard magnet into the bell.

The highest open interest strike sits down at 700, a deep OTM put base - structural hedges, not active flow. Above is the wall, below is the gamma flip at 731.00 with the put wall at 730.00 as the floor. With spot at 743.03, the cushion to the flip is thin but live - dealers still buying dips, still selling rallies.

Trade the polarity, not the level. Below the wall: dealer flow dampens; fade extremes back into the body. Above the wall: polarity inverts and the dampening becomes the accelerant. Sizing chases the wall; size where the dealers do the work.

What it means for your trading

OI clustered at 745.00 makes that strike the regime trigger - supportive below, suppressive into, and selling above. Spot pinned at the lid with the flip at 731.00 means the dampening cushion is real but conditional.

Trading readMassive long-gamma stack right at and above spot - dealers will fade any push higher into the call wall and catch dips toward the flip. The chart says fade extremes, don't chase.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna runs deeply negative at -$261.42B, the textbook vol-of-spot accelerant: if VIX lifts off the floor, dealers are forced to sell delta into weakness and the long-gamma cushion inverts into a liquidation tailwind. The positive-gamma dampening regime is therefore conditional, hostage to a quiet tape - not structural.

Charm flow prints -$366.2M into the bell, supportive on the SPY book as theta bleeds dealer-owned downside out of the surface. The pivot to watch is the charm flip at 745 - the Call Wall - where dealer bias rotates from supportive to sell-the-rally. Current read: Neutral, with spot pinned right at the trigger.

Trade construction: fade rallies into the pivot, respect the wall as a hard lid, and keep one tail hedge live against the vanna asymmetry. The cushion is real until VIX moves - then it isn't.

What it means for your trading

Vanna at -$261.42B makes the long-gamma regime conditional on suppressed VIX; charm at -$366.2M supports into the close but spot is pinned at the 745 pivot where dealer bias flips.

Cross-Asset Confirmation

Cross-asset tape offers no confirmation of stress - MOVE prints 81.53 with bond vol benign, and Fear & Greed sits at 58 in Greed territory. No credit-side cracks, no flight-to-quality bid, no MOVE/VIX divergence to flag. When rates vol refuses to bite, equity vol sellers get the green light.

The index complex confirms internally: QQQ 714.76 and IWM 282.67 both holding above their gamma flips, both in positive gamma regime alongside SPY. Cross-asset tone reads Unknown with regime divergence Aligned - small caps haven't broken ranks, tech hasn't decoupled, and the dampening dealer book is uniform across the complex.

Translation: this is the cleanest sell-vol confirmation the dashboard produces. Aligned regimes plus quiet rates vol plus sentiment short of euphoria equals a coherent backdrop for harvesting carry. IWM is the canary - first to lose its flip if dispersion bleeds wider.

What it means for your trading

Aligned positive-gamma regime across SPY/QQQ/IWM with MOVE at 81.53 and Fear & Greed at 58 - no cross-asset stress, vol-selling backdrop confirmed. Watch IWM's flip as the first crack signal.

Scenario EV

The scenario engine prints Iron Condor as the dominant structure with a composite score of 53, comfortably ahead of the put spread alternate at 39. Active VRP, benign VVIX at 91.79, and steep contango with VIX9D at 13.87 against spot 16.68 form the textbook backdrop for harvesting two-sided premium.

The optimal window sits in the 30-45 DTE bucket - far enough out to monetize the forward roll where the 21.412407618 belly is richest, far enough in to stay above the 0DTE gamma noise. Structure the wings outside the 745.00 call wall and 730.00 put wall; let dealer dampening do the work between them.

Sizing guidance per the VVIX/VIX ratio of 5.50 is Standard Size - no haircut, no jump premium to respect. Regime tag Elevated / Watchful with a 15-session half-life says the carry trade has runway.

What it means for your trading

Engine says iron condor at score 53, 30-45 DTE, wings outside the walls - standard sizing, VRP-paid carry, no vol-of-vol haircut required.

Actionable Summary

Bottom line: sell vol structured short, fade extremes into the walls, and keep one tail hedge live. The scenario engine flags Iron Condor as the optimal expression in the 30-45 DTE bucket - open the wings above the 745.00 call wall and below the 730.00 put wall to harvest the active VRP without sitting inside the gamma noise.

Tactical: fade rallies into 745, where dealer flow flips from supportive to a seller. Avoid naked long calls - the call wall is the lid; avoid single-name short vol while dispersion persists, since QQQ at 18.98% and IWM at 20.89% still command a premium over SPY at 12.8%. Index vol is the cleaner real estate.

Watch: VIX9D at 13.87 - a flip out of contango ends the carry trade in a hurry. Regime reads Elevated / Watchful, sticky for roughly 15 sessions on the baseline path, so harvest carry but do not mistake calm for an all-clear.

Billionaire family offices doubling down on chips/energy is a positioning tell - flows confirm the dispersion thesis between AI infra winners and broader equity.

Iran war's spillover to US farmers/food prices is the slow-burn inflation risk that keeps front-end rates and MOVE from collapsing further.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 731.00 against a spot of 743.03. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.8% with a volatility risk premium of 2.34%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.68. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime