Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

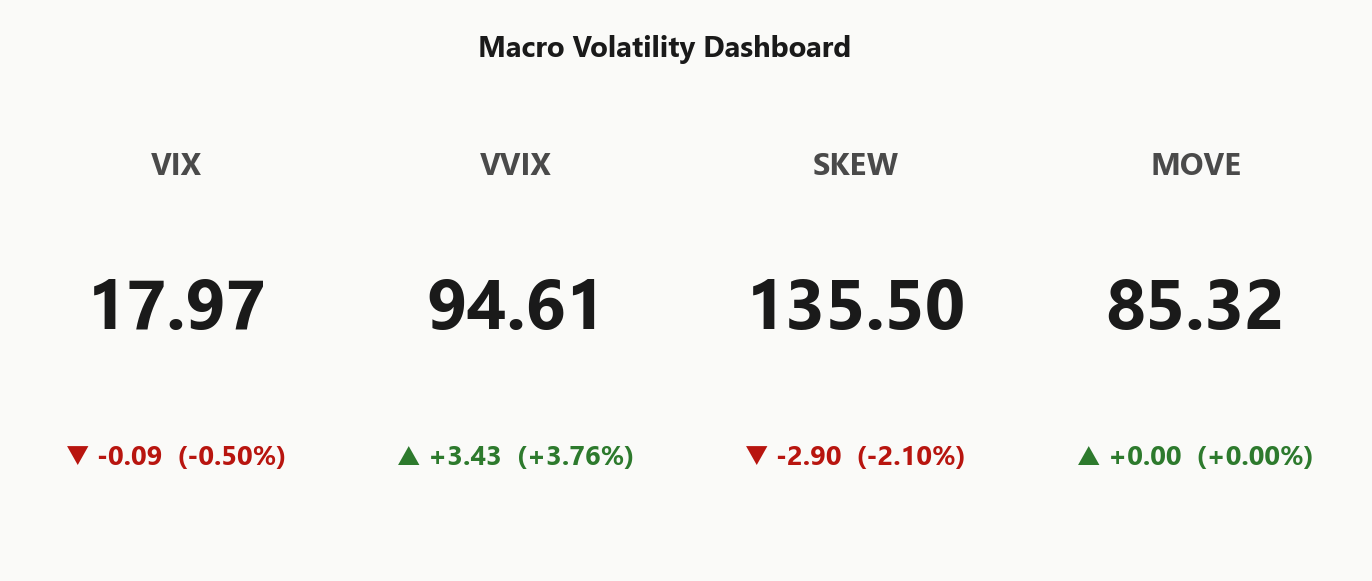

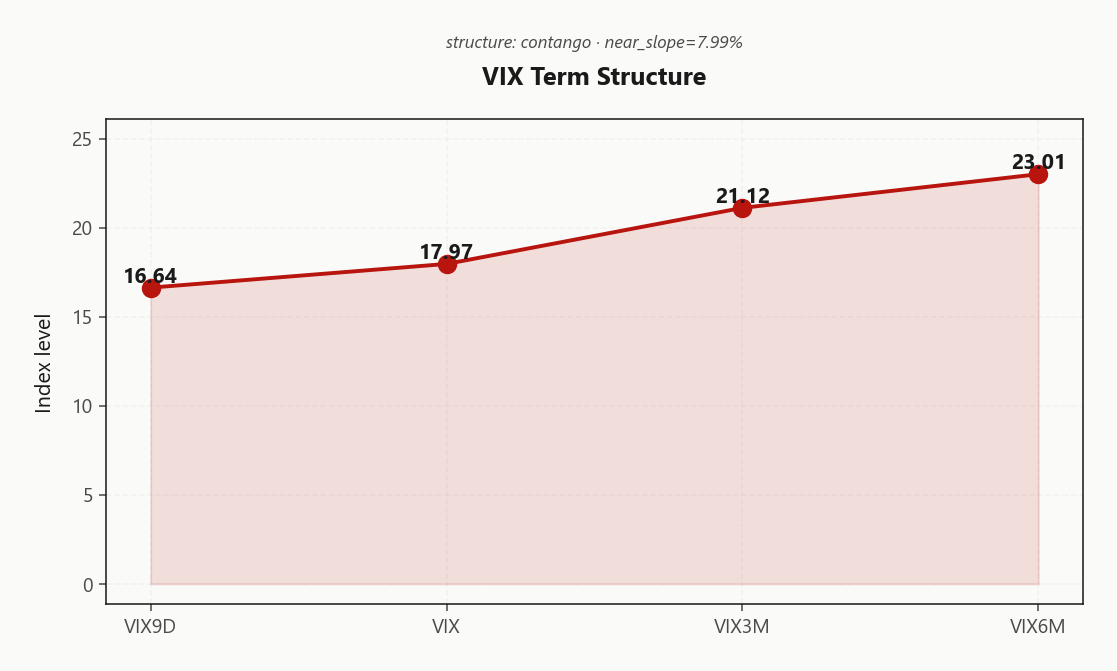

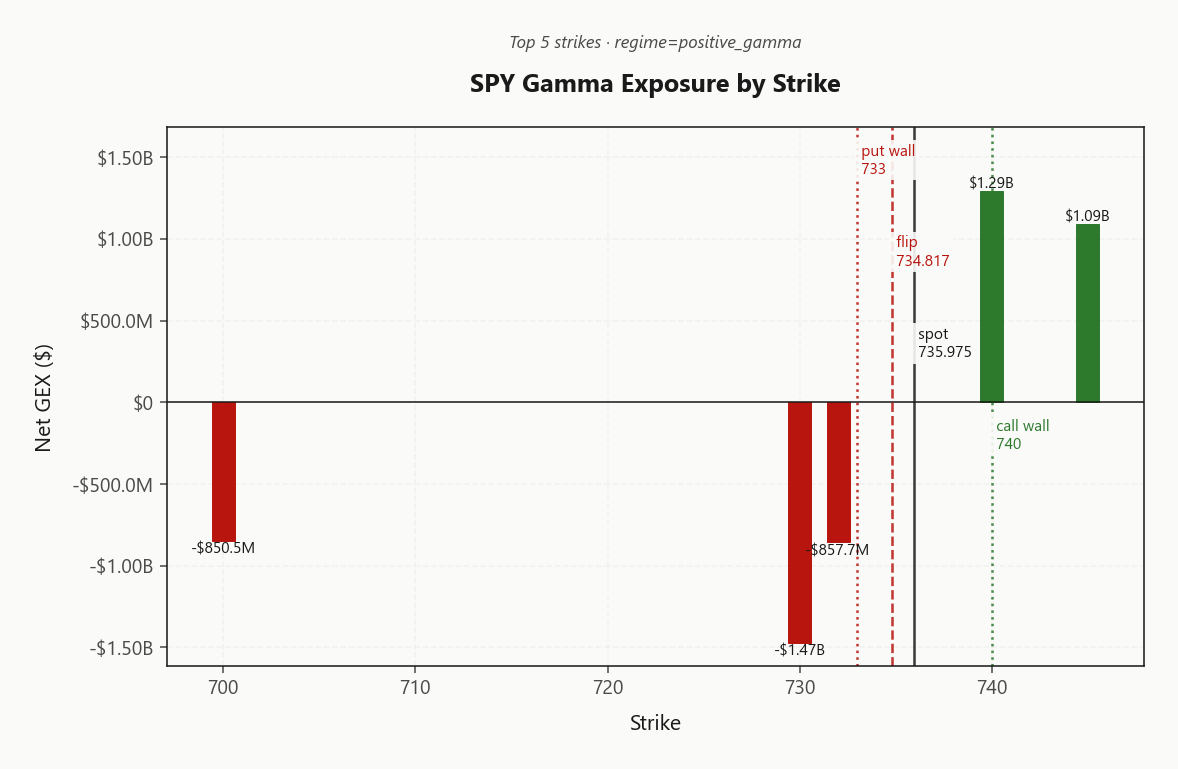

SPY trading at 735.98 with net GEX of -$4.88B - dealer-long-gamma regime, spot sitting just above the 734.82 flip. Call wall at 740.00 caps upside, put wall at 733.00 should provide support; max pain 718.00 pulls into expiry. Dealer vanna at -$215.13B is the tell - any vol uptick forces delta selling, so the gamma cushion is conditional on VIX staying calm. VIX at 18.30 with Steep Contango term structure (16.64/17.97/21.12) - carry trade alive, VRP at 4.26% pays you to be short premium. VVIX at 94.61 is benign but rising 3.76% - half-size if it crosses 100. IWM Negative Gamma below 275.99 flip is the divergence to watch; small-cap break would invalidate the SPX positive-gamma thesis. Bottom line: iron condor 30-45 DTE around 740.00/733.00 is the trade - keep size standard, add VIX call wing for tail.

Positive gamma cushion intact across SPY/QQQ, but IWM fragile below flip

Index complex opens in dealer-long-gamma mode with Positive Gamma on SPY/QQQ holding spot above flip, while IWM sits Negative Gamma as small-caps lag. VIX term structure remains in Steep Contango with Steep contango - vol sellers favored, but 94.61 VVIX whispers that vol-of-vol is rebuilding under the calm tape. Iran-war oil flow and dollar strength are the macro overlay - fade strength into walls but keep tail protection on.

Regime Assessment

Current regime reads Elevated / Watchful with VIX anchored at 17.97 - neither calm nor panic, but the watchful middle where dealer-long-gamma still dominates while vol-of-vol quietly rebuilds. Half-life of 15 sessions makes this regime sticky on the supportive side; probability of transition to panic over the next five sessions sits at 0.05, low but explicitly non-zero given the Iran-war overlay and creeping VVIX.

Decay-to-low-vol probability over ten sessions runs 0.45 - nearly coin-flip - meaning the modal path is grind-tighter, not breakout. Cross-asset tape confirms: SPY/QQQ Aligned in positive gamma, only IWM fragile beneath flip. The transition matrix is asymmetric: roughly ten-to-one in favor of decay over escalation.

Trade the asymmetry. Short premium with a tail hedge is the regime-consistent structure - harvest the VRP cushion while the half-life holds, but keep cheap convexity on for the small-but-real escalation tail.

What it means for your trading

Regime is Elevated / Watchful and sticky over a 15-session half-life, with decay odds (0.45) far outrunning escalation odds (0.05). Lean short-vol, carry a tail hedge.

Trading readVIX calm, VVIX creeping, SKEW rich, MOVE flat - vol-of-vol and tail premium are quietly building under a benign rates tape. That divergence pattern is the classic 'something's coming' setup; not actionable yet but worth flagging.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

VIX term structure prints Contango with the Steep Contango shape intact - 16.64 trading beneath 17.97 tells you the front end is discounting near-term realized to zero event premium, while 21.12 at the back keeps the carry stack paying. This is the classic Steep contango - vol sellers favored setup - short-dated vol decays into spot while the term premium funds the roll.

Front-to-back slope of 7.99%% is steep enough to be durable, not so steep it screams stress - the regime favors short-vol structures over calendar or long-vol expressions, because the curve does the work for you. Calendar trades get squeezed when contango is this deep; outright premium selling captures the full term decay.

The canary is slope compression. Any flattening of the 16.64→21.12 spread is the exit tell - front-end inversion would invalidate the carry thesis instantly. Until then, the curve geometry is the trade.

What it means for your trading

Steep Steep Contango with 16.64 under 17.97 and 21.12 anchoring the back is a textbook short-vol carry regime - sell premium into the curve, watch slope compression as the only exit signal.

Trading readSteep contango with VIX3M well above VIX = persistent carry on calendars and term VIX shorts. The slope is the trade - flattening would be the first regime-shift signal long before VIX prints crisis levels.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.53% sits well clear of HV20 at 10.27, leaving VRP at 4.26% - a rich cushion that pays you to wear gamma into a mean-reverting tape. This is the seller's print: implied is overcharging for realized that is actively decelerating into the bid.

The HV60 read at 14.82 running above HV20 confirms the structural cooling - volatility is bleeding off the longer window without going flat, so residual chop survives even as the near-term realized collapses. That gap is the harvest window: short premium gets paid for absorbing gamma into a regime that mean-reverts but hasn't gone dead.

HV5 acceleration is the canary we'd flag for a regime break, and it isn't present today. With VRP this rich and realized still decaying, the carry argument for selling into the Steep contango - vol sellers favored backdrop holds - fade the rich premium, but keep the wings on; the cushion narrows fast if HV5 lifts.

What it means for your trading

VRP of 4.26% with HV20 at 10.27 well below ATM IV at 14.53% is an active harvest window - sell premium, watch HV5 for the break signal.

Skew Convexity

The 2.44% quarter-delta skew print keeps downside paying up even as spot tape compresses - put quarter-delta IV at 21.7% sits a meaningful margin above ATM at 20.65%, the institutional hedge bid that refuses to fade. Smile_ratio at 1.13% confirms this is ordered steepening, not the crisis-style convex bid that shows up when tails go bid-only.

The call wing is the tell on the other side - call quarter-delta IV at 19.26% trails ATM, so no one is paying for upside chase. That asymmetry - bid downside, flat topside - is the textbook seller's smile under a Positive Gamma dealer book, and it dovetails with VRP at 4.26% still cushioning short premium.

Trade implication: with skew this rich, put-spreads dominate naked puts on a cost-per-unit-protection basis - finance the long leg by selling the steep wing. Outright put-buying overpays into the convexity bid; condor short wings inside 733.00/740.00 harvest the same skew without paying for it.

What it means for your trading

Quarter-delta skew at 2.44% with smile_ratio 1.13% is ordered, hedge-driven steepening - sell the wing via spreads, do not buy outright puts into this convexity bid.

Vol-of-Vol Structure

VVIX prints 94.61 against a 17.97 VIX - the ratio at 5.26 sits in the Normal band, but the optics flatter the tape. VVIX is bid 3.76%% while spot vol leaks lower; that fork is a stealth convexity bid, not a coincidence. Someone is paying up for the right to be long vol while the headline tape sleeps.

Sizing stays Standard Size - no haircut warranted on the print - but treat it as conditional. The ratio is creeping inside a normal range, which is exactly how vol-of-vol regimes rebuild before they're visible in VIX. The Iran tail and dollar bid give the convexity bid a narrative anchor.

Trigger discipline: if VVIX punches through the upper threshold mid-session, half-size all short-vol exposure on the spot - iron condors, premium-selling, calendar shorts. The carry trade implied by Steep Contango survives a VVIX of 94.61; it does not survive a VVIX through the century mark with VIX still pinned.

What it means for your trading

VVIX in the Normal band with the ratio at 5.26 keeps Standard Size appropriate, but the rising VVIX under a falling VIX is the early tell - cross the upper threshold and short-vol exposure gets halved.

Dispersion Spread

Index ATM IV is the tell: 14.53% on SPY against 21.87% QQQ and 20.37% IWM screens moderate at the headline, but the spread to single-name realized is wide as megacap idiosyncratic risk drives the constituent tape. Index vol is discounted by the correlation premium; the components are doing the work. Dispersion is alive - selling SPY premium captures that correlation discount while individual names get front-run by event-specific moves the index never feels.

QQQ richer than SPY is the giveaway - the AI complex is paying up for component convexity even as the basket compresses. IWM's 20.37% against a Negative Gamma backdrop says small-cap premium isn't worth touching; SPY's correlation harvest is. Prefer index iron condors to single-name straddles - the dispersion adjective is Moderate, not extreme, so size standard and let the basket do the smoothing.

What it means for your trading

Sell SPY at 14.53% over single names - the Aligned index complex is being underpriced relative to component dispersion. Iron condors on SPY beat single-name straddles this regime.

Liquidity & Microstructure

Open interest is racked tight between the 733.00 put wall and the 740.00 call wall, with the 734.82 gamma flip threading directly beneath spot at 735.98. That sliver of real estate is the entire battlefield - dealers are absorbing weakness above flip and will magnet price into 740.00 as upside develops. Fade strength into the wall; do not chase.

The dominant near-spot gamma node sits at 730.00 with net GEX of -$1.47B - that is the active flow, not the headline 700 high-OI print which reads as legacy retail residue parked well below spot. Cushion holds while spot stays above the flip; one wall-width below and the dealer book inverts hard, with support stripped and dips accelerated rather than bought.

What it means for your trading

Book is deep but the operative range is narrow - sell strength into 740.00, lean on 733.00 as floor, and treat 734.82 as the binary line where the entire support profile flips polarity.

Trading readDealers long gamma above the 734.82 flip means dips get bought and rips get sold into the 740.00 call wall - fade extremes, don't chase. Below the flip the flow inverts violently; that's the single level to watch.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Headline regime reads Positive Gamma, but the second-derivative book tells a different story: net VEX prints -$215.13B - dealer vanna is hostile. Any uptick in implied forces hedgers to sell delta into the move, turning a sleepy tape into an accelerant the moment 94.61 VVIX kicks. The gamma cushion is real, but it is conditional, not structural.

The offset lives in charm. Net CHEX at $93.8M means time decay is bidding dealer flow into the close - the supportive leg that keeps the tape pinned while vol stays anchored. Spot sits -0.1573150798 from the Gamma Flip pivot at 734.8172003418, current bias Supportive - close to the line, but on the right side of it.

Trade the asymmetry: harvest the charm bid via the Iron Condor inside 733.00/740.00, but keep a cheap VIX call wing on. If VVIX overruns its band, vanna overwhelms charm and the pivot breaks fast.

What it means for your trading

Positive gamma is the headline, hostile vanna is the truth - charm holds the tape into the close so long as spot stays above 734.8172003418 and VVIX stays contained. Lose either and dealer flow flips from cushion to accelerant.

Cross-Asset Confirmation

Cross-asset tape Aligned on the large-cap leg but fractured underneath: 85.32 on MOVE is flat - rates and credit are not corroborating any equity caution, and Fear & Greed at 60 (Greed) is constructive without being euphoric. This is not a credit-channel stress event; it is a localized small-cap weakness story with an Iran-oil macro overlay riding above it.

QQQ at 706.94 holds Positive Gamma alongside SPY, but IWM at 275.14 sits Negative Gamma below its flip - that is the divergence and the canary. Rates-FX channel is doing the tightening work in the background; equities aren't receiving the transmission yet.

Trade the tape as mean-reverting into SPY walls while the small-cap leg holds. A clean break of 275.99 on IWM is the first domino that would drag the index complex out of Positive Gamma and invalidate the condor thesis.

What it means for your trading

With MOVE at 85.32 and F&G in Greed, rates and sentiment confirm a benign large-cap tape - but IWM Negative Gamma below 275.99 is the single break-point that would flip the index complex from mean-reverting to trending.

Scenario EV

Scenario EV ranks Iron Condor the highest-scoring structure at 52, comfortably above the put-spread alternative at 43. The setup is textbook: Steep Contango across the term structure, an active VRP at 4.26%, and VVIX still parked in the Normal band at 94.61. Theta is the edge, defined-risk wings are the discipline.

Optimal window sits in the 30-45 DTE bucket - long enough to harvest the full contango decay between 16.64 and 21.12, short enough to keep gamma exposure manageable. Strike the short wings inside the 733.00 put wall and 740.00 call wall; that is where dealer flow does the work for you. Sizing stays at Standard Size - no VVIX haircut warranted yet.

Re-evaluate aggressively if VVIX punches through the upper band or if put skew at 2.44% steepens further. Both would flip the regime from harvest to defense.

Trade: deploy a Iron Condor on SPY in the 30-45 DTE window, shorts anchored inside the 733.00/740.00 walls. Regime reads Elevated / Watchful with steep VIX contango and an active VRP - vol sellers get paid, and dealer charm at the 734.8172003418 pivot keeps the bid supportive into close. Size standard while VVIX holds the Normal band.

Avoid: chasing IWM longs while spot sits beneath the 275.99 flip - the small-cap leg is the only fragile vector and a break there invalidates the index thesis. Skip naked single-name premium; dispersion is elevated and the index captures correlation discount more cleanly. No bets on backwardation - the curve geometry is structurally against you.

Watch & hedge: VVIX through 94.61 toward triple-digits, VIX9D/VIX inversion, or a MOVE jump - any one cracks the carry trade. Keep a cheap VIX call wing on for tail; the convexity is bid for a reason.

Russian oil revenue surging on Iran-war disruption tells you the supply shock is real and structural - keeps energy-driven inflation risk bid and pressures any rate-cut hopes.

'As stocks slump, cue Nvidia' frames NVDA as the index leadership barometer - single-stock concentration risk is the macro overlay traders need to monitor.

Iran threatening war 'beyond the region' is the tail-risk headline of the morning - explains why VVIX is creeping higher despite calm spot vol and justifies keeping cheap convexity on.

Oil slump on Trump comments creates two-way risk - the supply-crunch counter-narrative means oil-driven inflation could whipsaw, hostile for any clean directional macro view.

Dollar at six-week high on rate-hike bets and war uncertainty signals the rates-FX channel is doing the tightening work - watch for cross-asset stress transmission to equities.

CFTC probing pre-strike oil futures spike is the kind of structural-credibility headline that quietly raises the risk premium - not market-moving today, but feeds the slow VVIX bid.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 734.82 against a spot of 735.98. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.53% with a volatility risk premium of 4.26%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.97. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime