Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

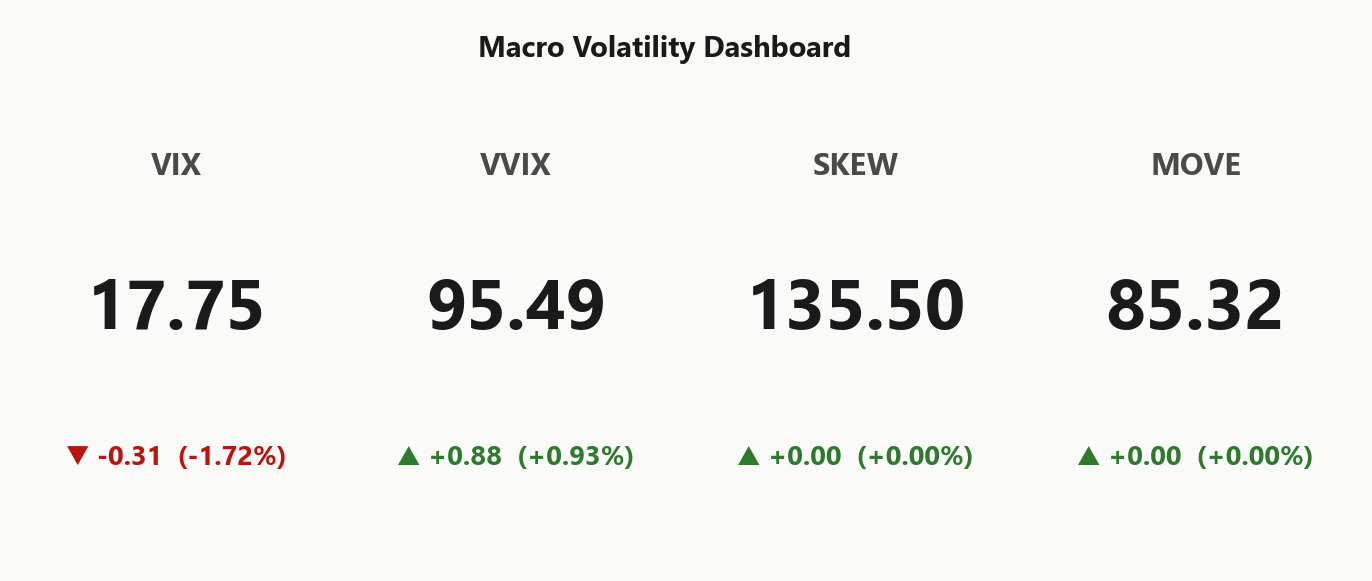

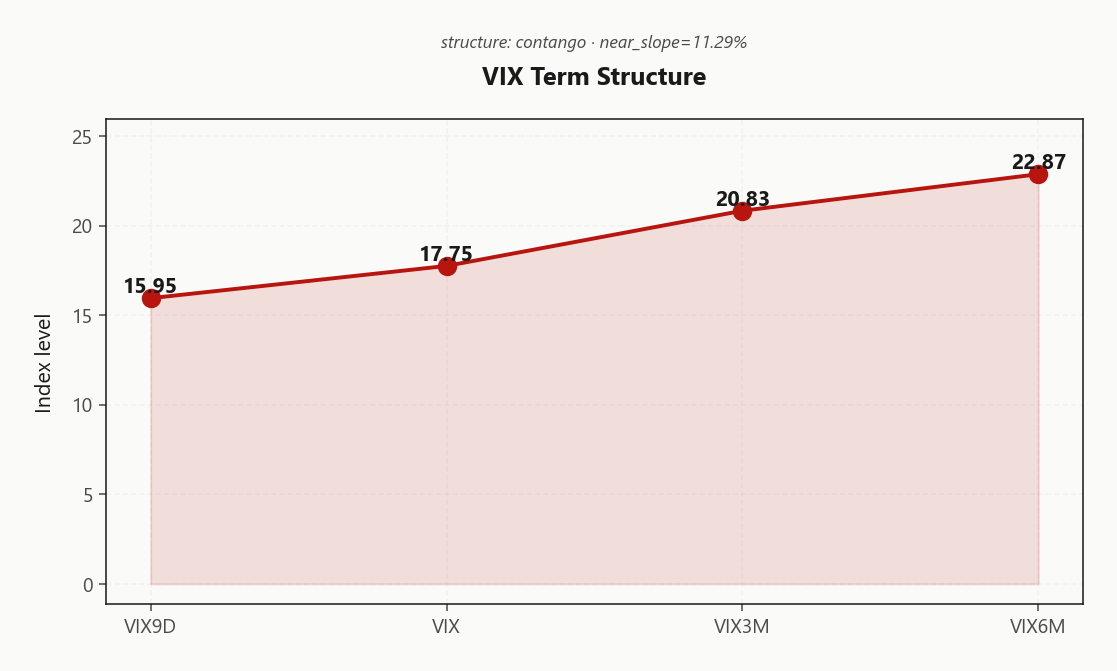

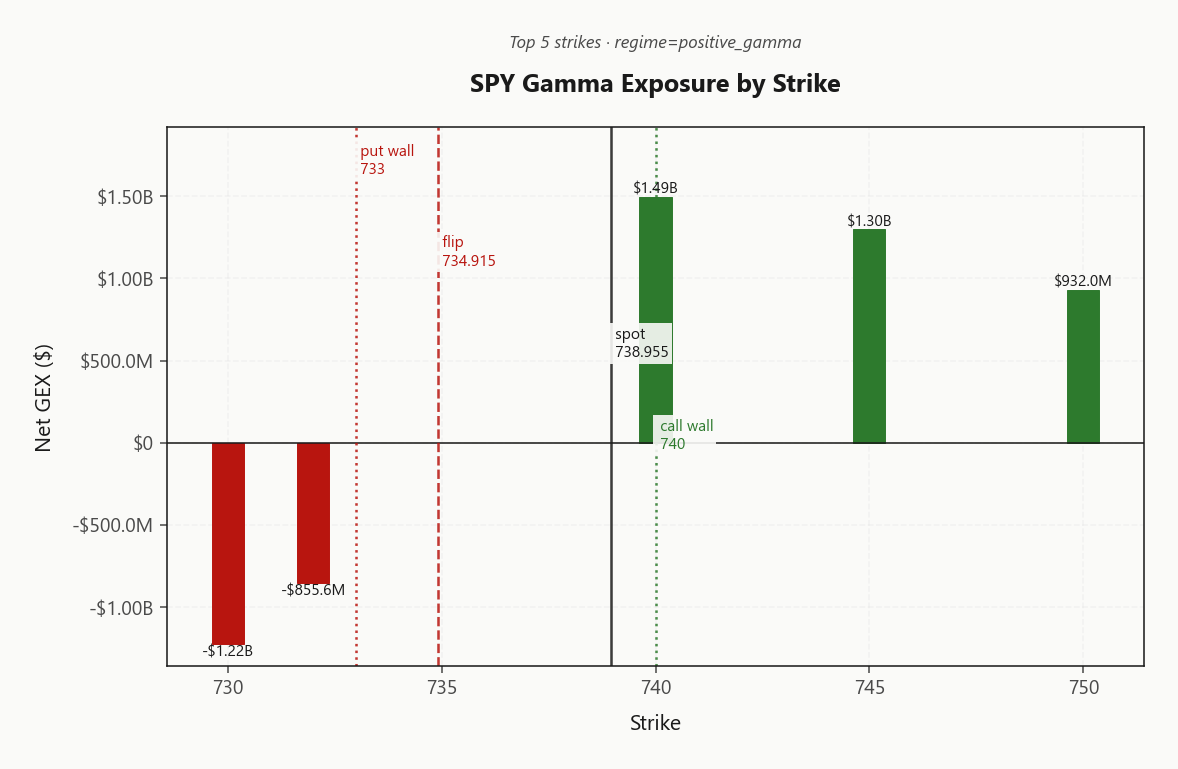

SPY 738.96 sits in Positive Gamma regime with net GEX -$1.79B - dealers long gamma, intraday moves get dampened. Key map: call wall 740.00 caps upside, put wall 733.00 catches downside, gamma flip 734.91 is the line where dealer flow inverts - spot 0.1414159184% above flip is a shallow cushion, not deep. Dealer positioning: net DEX $84.08B long, vanna -$237.95B says a vol spike flips dealers into delta-selling - that's the downside accelerant. Charm $89.1M mildly supportive into close. Vol read: VIX 17.75 (-1.72%%), term structure Contango with VIX9D 15.95 < VIX 17.75 < VIX3M 20.83 = vol sellers' carry intact, VRP 3.83% rich vs RV20 10.44. VVIX 95.49 normal - no jump-risk premium yet. Bottom line: Iron Condor between walls is the trade, sized standard, but watch VIX into NVDA tonight - a 734.91 break flips the regime.

Positive gamma cushion holds across index complex with Steep Contango term structure favoring premium sellers

SPY trades just below its 740.00 call wall with dealers long gamma - moves dampened, mean reversion the path of least resistance. VIX term structure in Steep Contango keeps vol sellers in the driver's seat, but VVIX at 95.49 and a 2.95%-point 25d put skew say the tape is paying up for tail insurance ahead of NVDA tonight. Cross-asset regime is Aligned - no macro break yet.

Regime Assessment

Regime reads Elevated / Watchful with VIX anchored at 17.75 - the tape sits in Elevated territory, neither compressed enough to chase short vol with conviction nor stressed enough to flip the playbook defensive.

Transition probabilities argue for stickiness: to-panic over five sessions runs at 0.05 while to-low over ten sits at 0.45, with a half-life of 15 sessions. Translation: the modal path is sideways drift, not regime break. NVDA tonight is the only credible accelerant, and even a clean print likely bleeds vol toward the low-regime side rather than triggering a panic transition.

Trade the regime, don't fight it - premium selling stays paid, but the watchful qualifier means standard sizing and defined risk through the event, with the gamma flip at 734.91 as the hard line where the thesis breaks.

What it means for your trading

Sticky Elevated / Watchful regime with a 15-session half-life favors carry trades over directional bets - modal path is drift, not transition.

Trading readVIX 17.75 soft, VVIX 95.49 normal, MOVE 85.32 flat - all four confirming each other for now. No regime-shift warning lights blinking, but VVIX is the one to watch into NVDA.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve prints textbook Steep Contango - VIX9D 15.95 < VIX 17.75 < VIX3M 20.83 < VIX6M 22.87. Near slope at 11.29% is structural, not event-driven - front-week carries no premium worth defending, and the curve pays sellers handsomely for staying short the front while the belly anchors.

The real edge sits in the forward implied between thirty and sixty days at 22.2104052192, with the sixty-to-ninety forward at 24.7423705412 - the curve is pricing a slow, orderly vol decay rather than any binary repricing. Short front-month, long thirty-to-forty-five DTE wings captures the slope without absorbing NVDA's overnight gamma.

Term structure Contango with near slope 11.29% keeps the carry trade paid, but the cleanest expression is selling the front against the 30-45 DTE belly where forward vol 22.2104052192 prices in decay rather than event risk.

Trading readSteep Contango with 9D-to-3M slope 11.29%% - vol carry is paid handsomely, market does not expect near-term stress; the trade is short front, long belly of the curve.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 14.27% against HV20 of 10.44 leaves a VRP of 3.83% points - sellers are being paid materially above what the tape is actually delivering. Realized has gone slow while the curve refuses to compress, and that gap is the carry.

Across the complex, QQQ runs the fattest premium at 4.52% points but the richness is contaminated - NVDA tonight is sitting inside that number, and the harvest looks cleaner than it is. IWM at 1.03% is the thinnest of the three; not enough edge to pay for the small-cap noise floor, skip it as a vehicle.

SPY is the cleanest short-vol expression today: meaningful VRP, no single-name binary contaminating the surface, and a positive gamma backdrop that suppresses the realized leg. Sell SPY/SPX vol into the carry, let QQQ trade the event, and leave IWM alone.

What it means for your trading

SPY VRP at 3.83% points is the cleanest short-vol harvest in the complex - QQQ richer at 4.52% but NVDA-contaminated, IWM too thin at 1.03% to bother with.

Skew Convexity

The 2.95%-point quarter-delta skew with smile ratio at 1.15% reads as an ordered downside bid - the tape is paying up for protection without crossing into panic. Put wing prints 22.28% against ATM 20.7%, while the call side sits flat at 19.33%. Translation: hedgers are bidding the left tail into NVDA tonight, but no one is reaching for upside convexity.

That asymmetric geometry dictates the structure choice. With the put wing carrying the premium and the call wing offering nothing back, naked puts are the expensive way to express downside - you're paying the steepest part of the surface outright. Put debit spreads finance the long leg by selling further-out strikes where skew is still rich, capturing the tail bid without overpaying for it. Call spreads, conversely, don't pay - the flat call wing means short calls collect little, so upside structures favor outright longs only if conviction warrants.

Net: skew is steep enough to monetize, not steep enough to chase. Spread the protection, don't buy it naked.

What it means for your trading

Quarter-delta skew at 2.95% with an ordered smile ratio of 1.15% says the left tail is bid into NVDA but not in panic - put debit spreads dominate naked puts on a risk-adjusted basis.

Vol-of-Vol Structure

VVIX prints 95.49 against spot VIX 17.75, putting the ratio at 5.38 - squarely in Normal territory. No jump-risk premium is being priced into the convexity of the vol surface; the second derivative is calm even as front-week skew bids up. That tells you the tape is paying for directional tail insurance, not for a regime break.

Sizing follows the signal: Standard Size. The Iron Condor sits inside its normal risk budget - no haircut for vol-of-vol stress, no scaling up just because VIX is soft. Premium-selling structures clear the vol-of-vol filter cleanly here.

One caveat: VVIX leads VIX on binary catalysts, and NVDA prints tonight. Re-mark the ratio post-close - a VVIX jump without a corresponding VIX move is the early tell that the surface is repricing convexity ahead of the spot vol. Until then, Normal reads as a green light for standard short-vol carry.

What it means for your trading

Vol-of-vol at 5.38 is Normal - no binary premium baked in, so Standard Size is appropriate. Watch VVIX, not VIX, for the first sign of a post-NVDA regime shift.

Dispersion Spread

QQQ ATM IV at 21.49% trades meaningfully rich to SPY at 14.27% - that spread is the market pricing single-name idiosyncratic risk, not index beta. Read it as NVDA tonight bleeding directly into the QQQ surface while the broad index sits in positive_gamma with cross-asset tape Aligned. The dispersion premium says implied correlation is compressing: mega-cap names are pricing their own event, the index is not.

Trade implication is clean - harvest vol where it's uncontaminated. SPY iron condors between 733.00 and 740.00 capture the VRP without owning NVDA's binary. Tech-name strangles look fat on screen but you are short the gamma the market is explicitly paying up to insure; the QQQ-minus-SPY IV gap is the receipt.

Avoid single-name vol selling into the earnings cluster - the dispersion spread will widen further if NVDA prints a tail, and short strangles in QQQ constituents are the wrong side of that asymmetry. Index condor, sized standard, is the disciplined expression.

What it means for your trading

QQQ IV richness over SPY at 21.49% vs 14.27% is event premium, not regime stress - sell index vol via SPY condors, leave single-name strangles alone into NVDA.

Liquidity & Microstructure

Order-book topography is unambiguous: highest OI cluster sits at 700 but the dominant magnet is the top GEX strike at 740.00, carrying $1.49B of dealer gamma - that's where the tape wants to pin. Spot 738.96 trades above the gamma flip at 734.91, so dealer hedging is currently dampening: rallies absorbed into the 740.00 call wall, dips bought back toward the 733.00 put wall.

The flip level is THE line. Above it, dealers buy weakness and sell strength - mean reversion is the path of least resistance and short-premium between the walls is paid. A break below 734.91 inverts that mechanic: hedging flips from suppressive to amplifying, and trend-following kinetics take over. With spot only 0.1414159184 from the flip, the cushion is shallow - respect it, don't lean on it.

What it means for your trading

Trade the range bounded by 733.00 and 740.00 while spot holds above 734.91; a breach of the flip is the regime-change signal and pulls every dampening assumption off the table.

Trading readTop strike at 740.00 acts as the dominant magnet today - spot pinning here between the put wall and call wall says fade strength into resistance, buy weakness into the cluster.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer vanna sits -$237.95B - deeply negative and the single most asymmetric line in the book. Translation: any meaningful VIX uptick mechanically forces dealers to sell delta to stay hedged, the classic vanna accelerant that turns a quiet drift into a directional slide. The cushion is real while spot holds; the trapdoor is real if vol pops.

Charm runs $89.1M - mildly supportive into the close, the standard time-decay tailwind that pins tape toward high-OI clusters as theta bleeds. It is a tailwind, not a thesis. Net bias reads Neutral with the inversion line at 740 - that is the level where the vanna/charm interplay flips from dampening to amplifying.

Playbook: respect the pivot at 740, harvest the gamma cushion while VIX is quiet, and treat any VVIX expansion as the tell that the negative-vanna book is about to do the work for you on the downside.

What it means for your trading

Vanna -$237.95B is the hidden accelerant - benign until VIX moves, then the dealer book becomes the seller. Charm $89.1M supports the pin into close, with 740 as the regime-flip line to watch.

Cross-Asset Confirmation

Cross-asset tape is Aligned and that is the load-bearing read here. MOVE at 85.32 sits flat - rates vol is not pricing the geopolitical headline cycle, which is the single cleanest signal that the Iran-deal noise and tariff chatter are not bleeding into credit transmission. Equity wobble without a rates-vol echo mean-reverts; equity wobble with MOVE breaking out is the one you hedge.

Breadth confirms: 709.32 on QQQ and 278.44 on IWM are tracking 738.96 on SPY without divergence - small-cap and tech-heavy complexes both sitting in positive_gamma alongside the index. No breadth break, no sector-rotation tell that would flag a regime crack.

Fear & Greed prints Greed at 61 - risk-on tilt is building, not extreme, but worth flagging as the contrarian setup if NVDA disappoints. Net read: isolated equity event-risk, not a macro shock. Carry the short-vol structure, do not buy index hedges on this tape.

What it means for your trading

Cross-asset signals are Aligned with MOVE at 85.32 flat and F&G in Greed - no credit or rates transmission means the equity wobble is positioning, not regime-change. Sustain the carry trade until MOVE or VVIX flags otherwise.

Scenario EV

The scenario EV grid lands on Iron Condor at 65, with the put spread trailing closely at 57 - close enough that desks running a directional bias can substitute without giving up meaningful edge. The condor wins on the back of the positive gamma cushion between 733.00 and 740.00, where dealer hedging dampens both tails and lets premium decay do the heavy lifting.

Carry sweet spot is 30-45 DTE. Front-week contracts price insufficient premium relative to NVDA event risk crammed into the next print, while forward vol at 22.2104052192 shows the curve paying handsomely into the belly. Sell the body, own wings further out if you want defined-risk through the catalyst.

Sizing stays standard - VVIX at 95.49 sits inside normal range, so no jump-premium adjustment required. Re-rack the book if spot punches through 734.91 - that's where the condor thesis breaks and the put spread becomes the better-scoring trade.

What it means for your trading

Iron condor at 65 edges out the put spread at 57; the 30-45 DTE belly captures VRP while sidestepping front-week NVDA event risk.

Actionable Summary

The setup synthesizes cleanly: Elevated / Watchful regime overlaid on a Steep Contango VIX curve with spot pinned in Positive Gamma territory - net GEX -$1.79B, dealers long, intraday moves dampened. The trade reads itself: Iron Condor bounded by the 733.00 put wall and 740.00 call wall, sized standard given VVIX 95.49 sitting in Normal territory with no jump premium embedded.

Watch the 740 charm pivot as the live tell; the hard line is the 734.91 gamma flip - break it and dealer flow inverts, net VEX -$237.95B turns vol spikes into delta-selling accelerant. Cross-asset is Aligned with MOVE 85.32 flat - no macro break to override the structural read.

Avoid: single-name vol selling into NVDA tonight (QQQ IV 21.49% richer than SPY 14.27% for a reason), naked puts with 25d skew at 2.95%, and 0DTE chase into pin risk at 740.00.

NVDA earnings tonight is the binary catalyst the entire vol surface is paying up for - QQQ single-name premium and put skew steepness directly reflect this event.

"As stocks slump, cue Nvidia" - the narrative that NVDA is now the proxy for index direction is exactly why dispersion trades favor index vol selling, not single-name.

Trump's "final stages" Iran deal language with attack-threats keeps a binary geopolitical bid under tail vol and partly explains why front-week put skew refuses to compress.

Six-week dollar high tied to rate-hike-bets and war uncertainty is the macro backdrop keeping MOVE sticky and capping how aggressively VIX can compress further.

Oil slumping on Trump comments while supply remains tight = mixed signal for energy and inflation expectations; doesn't break equity regime but caps the F&G rally.

Rupee at record low on oil + UST yields signals EM stress that hasn't yet transmitted to US credit - worth watching as the canary if cross-asset regime turns.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 734.91 against a spot of 738.96. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.27% with a volatility risk premium of 3.83%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.75. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime