Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

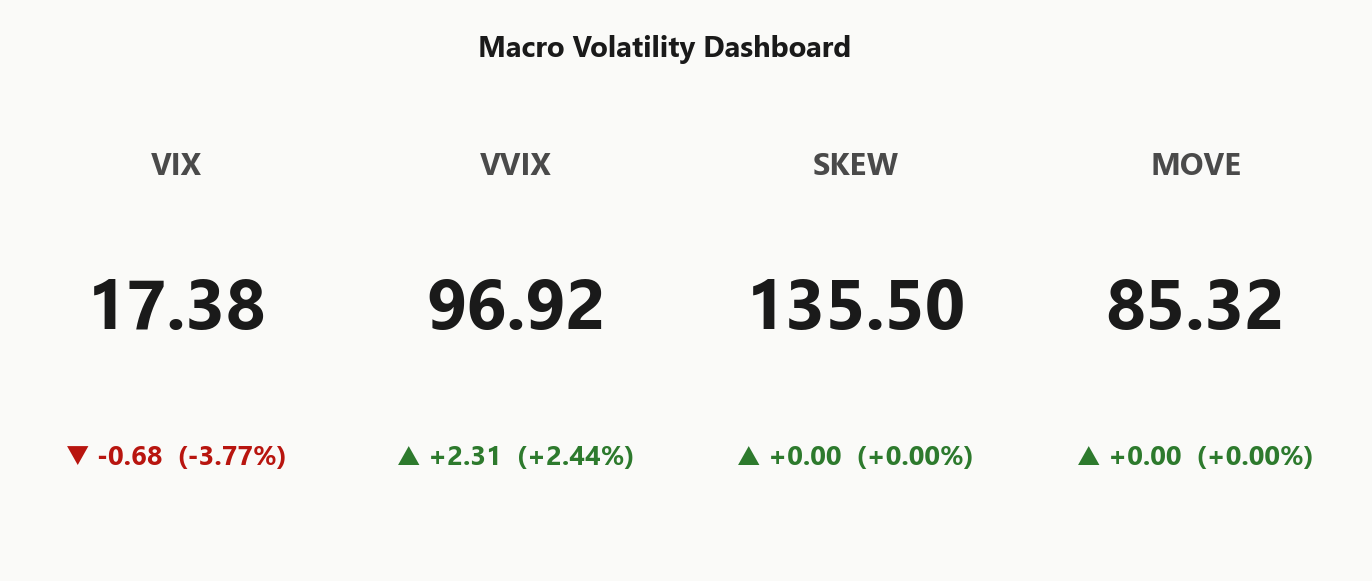

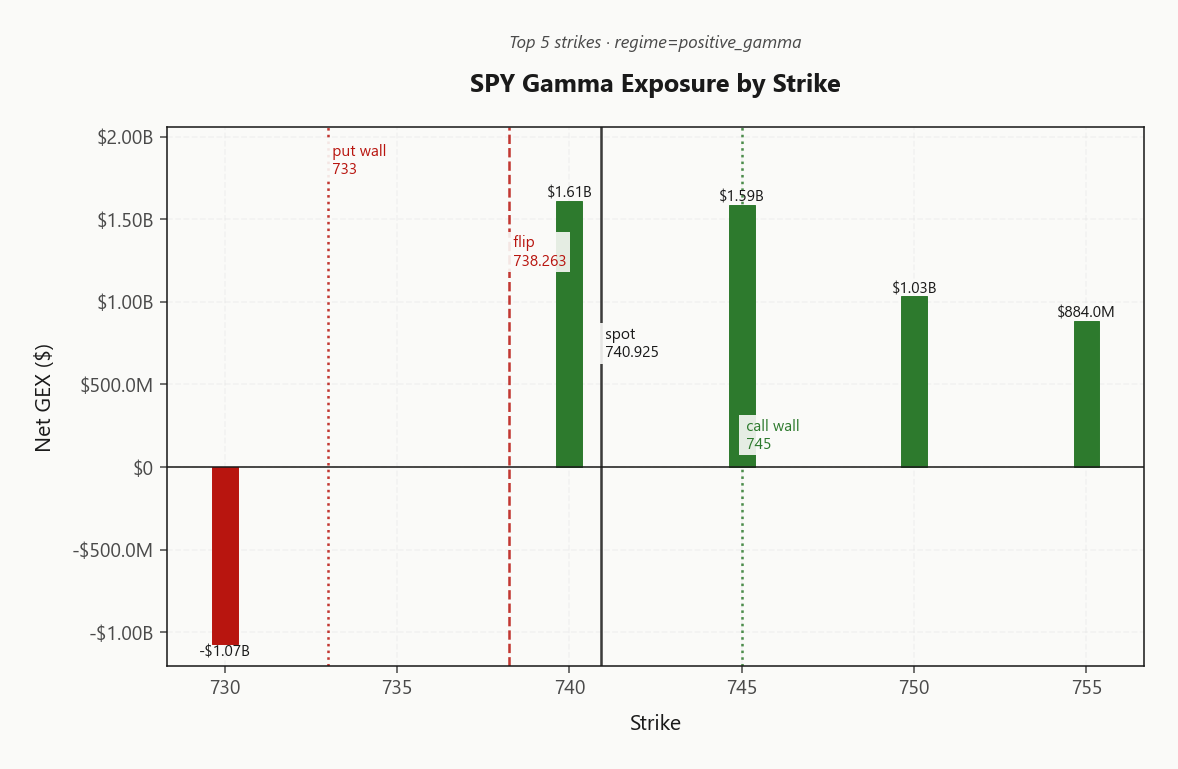

SPY closed at 740.93 with net GEX at $261.1M - positive_gamma regime, dealers long gamma, moves dampened. Call wall sits at 745.00 and put wall at 733.00, with the gamma flip at 738.26 - spot is just -0.3592996466% from the pivot, so the cushion is thin but intact. Dealers are short vanna (-$251.8B) meaning any vol spike forces delta selling - that's the asymmetric risk into tomorrow. VIX at 17.38 with term structure in Contango (VIX9D 15.19 / VIX3M 20.65) - VRP at 2.95% pts is paid for selling premium. VVIX at 96.92 drifting up flags tail demand creeping in despite spot stability. Bottom line: iron condors in 30-45 DTE are the carry trade, but keep size standard (Standard Size) and respect the flip - break of 738.26 flips dealer hedging from supportive to accelerant.

Positive gamma across index complex with steep contango - vol sellers paid, mean-reversion regime holding into close

SPY settled at 740.93 comfortably above the gamma flip at 738.26, leaving dealers long gamma and the tape dampened into the close. With VIX term structure in Contango and VVIX at 96.92, the carry trade is paid but vol-of-vol is creeping. Iron condors in the 30-45 window are the cleanest expression of this regime.

Regime Assessment

The tape is parked in an Elevated / Watchful regime - VIX at 17.38 places us squarely in the mid-teens band where dealer gamma cushions, vol carry pays, and tail demand stays orderly rather than disorderly. The transition matrix is asymmetric: probability of escalating to panic over the next week sits at 0.05, while the odds of compressing into a low-vol state over two weeks run at 0.45. Drift is toward complacency, not crisis.

Half-life of roughly 15 sessions tells you this regime is durable but not permanent - a fortnight of carry before the configuration meaningfully reshuffles. The current state is Elevated: watchful, not bearish; constructive, not complacent. Play the carry, but mark the calendar - half-life decay is real, and the regime exit will not announce itself in VIX before it shows up in VVIX at 96.92.

What it means for your trading

Elevated/watchful regime with asymmetric drift toward low-vol compression - half-life of 15 sessions makes the short-vol carry trade durable but finite. Panic probability at 0.05 is low, but VVIX divergence is the trigger to watch, not VIX itself.

Trading readVIX softening, VVIX bid, MOVE flat, SKEW elevated - divergence is the story. Equity vol-of-vol is creeping while everything else stays calm; that's the bookmark for when this regime ends.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

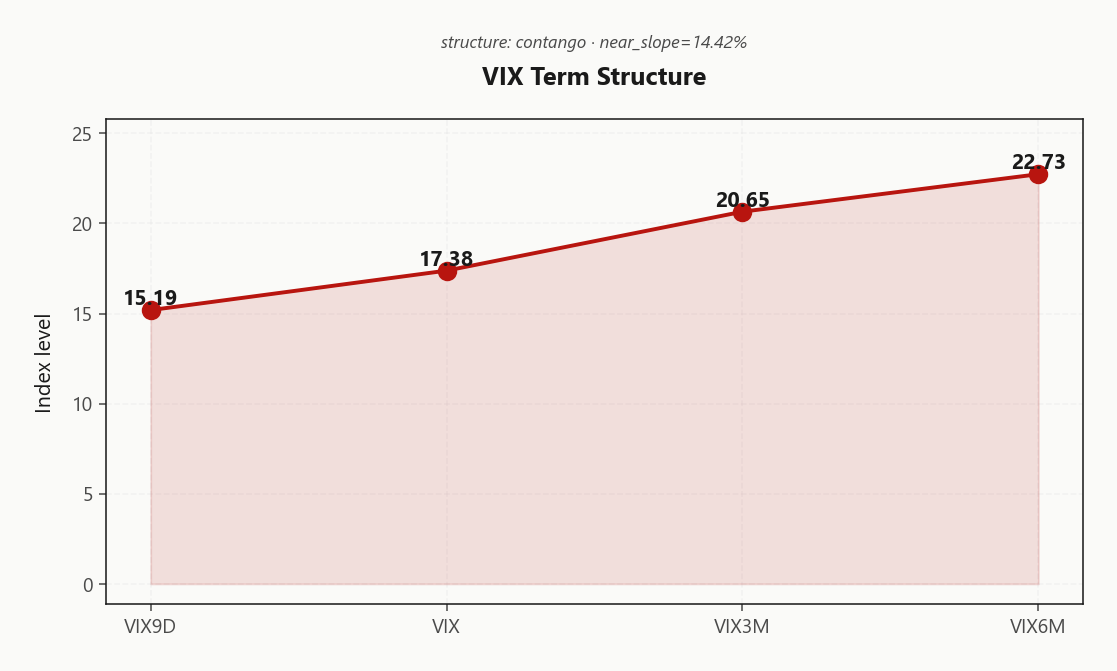

The VIX curve sits in Contango with 15.19 printing well below 20.65 and 22.73 at the long end - a textbook Steep Contango setup where the front-end carries the discount and the belly carries the premium. Spot VIX at 17.38 against the longer tenors leaves roll-down doing the heavy lifting; Steep contango - vol sellers favored is the operative regime label and it is paying short-vol carry without ambiguity.

Near-slope at 14.42%% confirms structural premium rather than event-driven kink - the curve is not flagging a concentrated catalyst, it is flagging persistent vol-supply imbalance. Forward 30-60 vol prints elevated relative to the front, putting the belly of the curve firmly in harvest territory.

The cleanest expression sits in the 30-45 DTE window, where roll-down compounds against decaying realized. Front-end is too noisy for naked premium and the back is too cheap to short - the belly is where the steepness pays without buying the event tail.

What it means for your trading

Steep contango with 15.19 versus 20.65 defines a Steep Contango regime that favors vol sellers in the 30-45 DTE belly. Carry the slope, avoid the front-month noise.

Trading readSteep contango with VIX9D meaningfully below VIX3M - vol carry is paid and the market is pricing zero near-term shock. The slope itself is the trade: roll-down on short front-end is the harvest mechanism.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 13.65% trades a clean spread over HV20 at 10.7 - the realized tape simply isn't delivering the moves the strip is pricing. With HV60 at 14.93 showing medium-term realized has already cooled, the curve of delivered vol is rolling down underneath an implied surface that hasn't followed it lower.

That gap leaves VRP at 2.95% points - harvest territory, not a stretched extreme. Premium sellers get paid to absorb gamma, and the Positive Gamma cushion at spot reinforces the carry. Short-vol structures dominate the scorecard: iron condors in the 30-45 DTE belly are the cleanest expression, with HV60 still bracketing the wings comfortably and HV20 well inside the breakevens.

Risk is mechanical - a sharp acceleration in near-term realized compresses this spread in days, not weeks. Keep sizing at Standard Size, watch intraday range against HV20, and respect that VRP is paid because the gamma flip at 738.26 still holds - break it and delivered vol catches up violently.

What it means for your trading

Implied carries a clean premium over recent realized at every horizon - VRP at 2.95% pts is harvest-grade and short-vol structures own the regime, contingent on the Positive Gamma cushion holding the spread from snapping shut on a realized-vol catch-up.

Skew Convexity

Skew is doing the work the tape isn't: put-wing IV at 20.49% sits well clear of ATM at 19.06%, while the call wing prints 17.47% - flat and unloved. Quarter-delta skew at 3.02% with a smile ratio of 1.17% tells you the tail is bid, but bid in an orderly way - no panic acceleration, no convex blow-out, just steady downside demand layered into an otherwise dampened book.

That asymmetry is the trade. With put wings rich and call wings cheap, naked downside hedges are overpaying for protection the smile is already pricing. Put-spreads finance the long leg by selling further-OTM strikes back into the steep wing - same downside cover, materially better entry. On the upside, the flat call surface means no premium to harvest there; covered-call overlays are tax-on-carry, not edge.

Bottom line: respect the tail bid but don't pay retail for it. Sell the skew, don't buy it - put-spread structure dominates naked puts in this convexity regime.

What it means for your trading

Steep 3.02% skew with smile ratio 1.17% signals ordered tail demand, not panic - put-spreads over naked puts for downside cover, and no edge in the flat call wing.

Vol-of-Vol Structure

The tell isn't in 17.38 - it's in 96.92. Spot vol bled lower into the close while VVIX ticked the other way, and that divergence is the one signal worth paying for in an otherwise sleepy tape. Dealers and dispersion desks are quietly bidding convexity even as the front-end of the curve gets sold; the 5.58 VVIX/VIX ratio is rich relative to where outright vol prints.

Level still reads Normal, so this is not a stop-out - sizing guidance stays Standard Size on the iron condor book. But the asymmetry has shifted: vol-of-vol is the early-warning indicator now, not VIX itself. A break of the prior VVIX range is the regime-change trigger; that's the line that flips the carry trade from paid to punished, well before 17.38 reprints.

Trade it as written - harvest the contango roll-down, keep clip standard - but move the alert from spot vol to vol-of-vol. The desks paying up for gamma-on-gamma are usually right first.

What it means for your trading

VVIX bid against a softer 17.38 is the cleanest early-warning on the tape; level is still Normal and sizing stays Standard Size, but the VVIX range break - not VIX - is what flips this regime.

Dispersion Spread

The dispersion tell is in the index-vs-constituent vol gap: SPY ATM prints at 13.65% while QQQ ATM carries 21.13% - a wedge that says correlation is moderate, idiosyncratic risk is doing the work. Index vol is cheap relative to what constituents are realizing, and that asymmetry is the entire trade.

Cross-strike IV dispersion reads modest at 5.94 with cross-expiry at 2.47 - the surface is ordered, not fractured. That's exactly the texture where index condors compound and single-name strangles get picked off by one bad print. With NVDA tonight and AAPL/MSFT leading the GEX rebalance, harvesting QQQ-level premium on a single ticker means underwriting event gamma you can't hedge.

Trade the wedge, not the ticker: SPY iron condors in the 30-45 DTE belly are the clean expression - index dampening absorbs the constituent noise, and the dispersion premium flows to you instead of through you.

What it means for your trading

Index vol at 13.65% is structurally cheap to QQQ's 21.13% - sell SPY condors, not single-name strangles, and let constituent dispersion subsidize the carry.

Liquidity & Microstructure

The book builds a gamma dampening sandwich: top strike 740.00 carries $1.61B of net GEX directly above spot, with the call wall capped at 745.00 and the highest-OI line anchored at 700. That stack is the corridor dealers defend into the close - supply leaning on rallies, bid leaning on dips, intraday tape compressed inside the band.

The single line that matters is the gamma flip at 738.26. Spot sits just -0.3592996466 away - cushion intact, but uncomfortably thin. Below it, the put wall at 733.00 becomes a magnet on any flush, and dealer hedging flips from supportive to accelerant. Above, the corridor up to 745.00 stays pinned.

Trade the band, respect the flip. Iron condors anchored inside the call wall / put wall corridor are clean; a print through 738.26 is the binary that voids the regime and forces de-risk.

What it means for your trading

Dealer gamma forms a dampening sandwich between 733.00 and 745.00, but spot is only -0.3592996466 from the gamma flip at 738.26 - the binary line where supportive flow turns into trend acceleration.

Trading readDealer gamma is densely stacked from the gamma flip up through the call wall - that band is the dampening corridor for tomorrow. Below the flip, gamma turns negative fast: any flush opens trend-following territory.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna sits deeply negative at -$251.8B - the asymmetric tell into tomorrow. Dealers are positioned to sell delta into any vol uptick, meaning the same desks cushioning the tape today flip to accelerants the moment IV bids. The gamma cushion isn't free; it's a function of vol staying suppressed, and the vanna book is the receipt.

Charm reads -$890.4M, layering late-session decay supply on top of the vanna setup. Time bleed mechanically lightens dealer hedges into the close, reinforcing the dampening corridor while spot holds above the pivot. The pivot itself - 738.2628590932, a Gamma Flip - currently registers Supportive, with spot only -0.3592996466 away.

This is binary, not gradient. Above the pivot, dealer flow is the mean-reversion engine; below it, the negative vanna book and charm decay compound into trend acceleration. One level, one regime switch - manage size against the flip, not the spot.

What it means for your trading

Net VEX at -$251.8B is the asymmetric risk: dealers cushion now but sell delta into any vol spike. Watch the pivot at 738.2628590932 - break and the regime flips from supportive to accelerant.

Cross-Asset Confirmation

Cross-asset tape confirms the equity vol bid is unconfirmed - MOVE at 85.32 sits flat, Treasury vol is asleep, and the credit channel is offering zero corroboration to a tail bid in SPX options. With QQQ printing 712.18 and IWM at 279.71 - both above their respective gamma flips and labeled positive_gamma - the index complex is Aligned on the dampening side. No cross-asset divergence, no regime break.

Fear & Greed reads Greed at 61 - sentiment is paid for the carry but nowhere near extreme greed, so there is no contrarian exhaustion signal yet. Cross-asset tone reads Unknown, which is exactly what you want under a short-vol mandate: nothing screaming.

Iran headline noise is just that - noise - unless and until it cracks the bond tape. MOVE is the tell: a flat print here means the geopolitical premium stays bottled in VIX9D where contango eats it. The day this regime breaks, MOVE moves first and credit spreads widen before SPY skew goes bid.

What it means for your trading

Cross-asset confirms equity vol-selling carries: MOVE flat at 85.32, QQQ and IWM both positive_gamma-Aligned, sentiment paid but not extreme at 61. The credit/Treasury vol channel is the canary - watch MOVE, not headlines.

Scenario EV

The scorecard prints clean: Iron Condor at 55, with the put-spread alternative trailing at 46. VRP is paid, the positive_gamma cushion is intact with spot anchored above the flip, and the term structure sits in Contango - three legs of the carry trade aligned in the same direction.

The belly of the curve is where the edge concentrates. Optimal DTE prints 30-45, capturing roll-down between 15.19 front-end and 20.65 mid-curve while sidestepping the event premium loaded into the very front. Iron condor strikes wrap naturally around the call wall at 745.00 and the put wall at 733.00, with the gamma flip at 738.26 as the single binary kill-switch.

Sizing stays Standard Size - VVIX at 96.92 reads normal, no haircut warranted yet, but the vol-of-vol creep is the bookmark for when this regime exhausts.

What it means for your trading

Iron condor in 30-45 DTE is the cleanest expression of paid VRP, positive_gamma cushion, and steep contango - keep size Standard Size and respect the flip at 738.26 as the regime-flip line.

Actionable Summary

Bottom line: short-vol regime is intact and the trade is an Iron Condor in the 30-45 DTE belly. SPY at 740.93 sits on the supportive side of the gamma flip with dealers long gamma, VIX term structure in Contango, and VRP at 2.95% paying the carry. Regime label reads Elevated / Watchful with a half-life near 15 sessions - durable but not permanent.

Watch level: the gamma flip at 738.2628590932 is the single binary line. Above it, dealer flow dampens; below it, vanna at -$251.8B forces delta selling and the tape accelerates. Avoid naked downside hedges - put wing is rich at 20.49% versus ATM, so spread the protection - and skip single-name short strangles where dispersion still bites.

Sizing:Standard Size. VVIX at 96.92 creeping while VIX softens is the early-warning bookmark - no haircut yet, but that divergence is what flips the regime before VIX does.

What it means for your trading

Stay short vol via Iron Condor in 30-45 DTE at Standard Size, with the gamma flip at 738.2628590932 as the hard line that flips dealer hedging from supportive to accelerant. Skip naked single-name premium and naked downside - the edge is in index spreads while Elevated / Watchful holds.

Trump's Iran rhetoric oscillation is the textbook driver of geopolitical premium that sits in VIX9D - every flip-flop pumps front-end vol the term structure is fading

'Trump blinks at bond market' is the only news that actually matters for regime durability - MOVE flat right now is the proof, but it's the canary that flips this from carry to crisis

Rupee at record low + Treasury yield strain = the EM/credit channel to watch; if this widens, MOVE finally moves and the equity vol regime breaks

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 738.26 against a spot of 740.93. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.65% with a volatility risk premium of 2.95%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.38. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime