Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

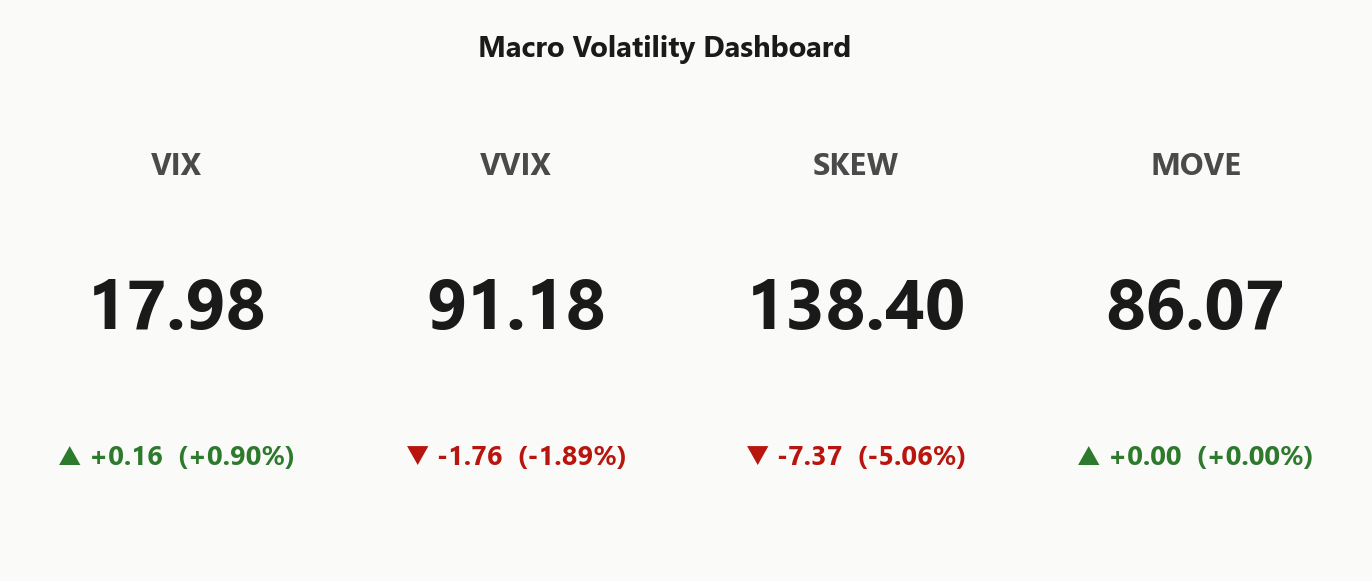

SPY trades at 733.62, sitting just under the gamma flip at 738.67 with net GEX of -$5.86B - that's a Negative Gamma tape where dealers amplify moves rather than dampen them. Call wall stacks at 740.00, put wall at 730.00, and 0DTE alone is 23.9% of total gamma - intraday is going to be jumpy. QQQ is the outlier, holding Positive Gamma with spot well above its flip at 599.78, so tech absorbs shocks while SPY/IWM transmit them. Dealer vanna at -$185.82B means any vol uptick forces more delta selling - that's the asymmetry to respect. VIX sits at 17.98 in Contango with VVIX at 91.18, VRP 4.83% - vol carry exists but is not extreme. F&G at 61 (Greed) shows no panic priced in despite the Iran headlines. Bottom line: trade the SPY/QQQ split - defined-risk iron condors in the 30-45 DTE window, avoid undefined short premium in SPY below 738.67.

Index complex is split - SPY sits below its gamma flip at 738.67 in Negative Gamma while QQQ holds Positive Gamma well above its flip. Vol surface stays in Steep Contango with VVIX at 91.18 - carry is paid but dealer flow is hostile in SPY/IWM and friendly in QQQ. The trade is the divergence, not the direction.

Regime Assessment

Regime tag: Elevated / Watchful with VIX anchored at 17.98 - not crisis, not complacency, the middle zone where positioning matters more than direction. Transition probabilities frame the window cleanly: 0.05 chance of cracking to panic over five sessions, 0.45 chance of decaying to low-vol over ten. The panic tail is live but thin; the mean-reversion path is closer to a coin flip.

Half-life on the current state is 15 sessions - moderately sticky, meaning structures sized for this regime should carry inside that window rather than fight it. The Iran tape keeps the panic transition non-zero, but credit and sentiment refuse to confirm escalation, so the base case is decay, not break.

Trade implication: stay inside the half-life, lean into the Qqq Heavier SPY-versus-QQQ split, and respect that the panic probability - while small - is not zero with headline risk on tape.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - plan trades inside that window, with mean-reversion to low-vol nearly a coin flip and panic transition contained at 0.05.

Trading readVIX up, VVIX down, SKEW down - divergence between spot vol bid and tail/vol-of-vol bid says the elevated front is mechanical hedging, not real panic pricing.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

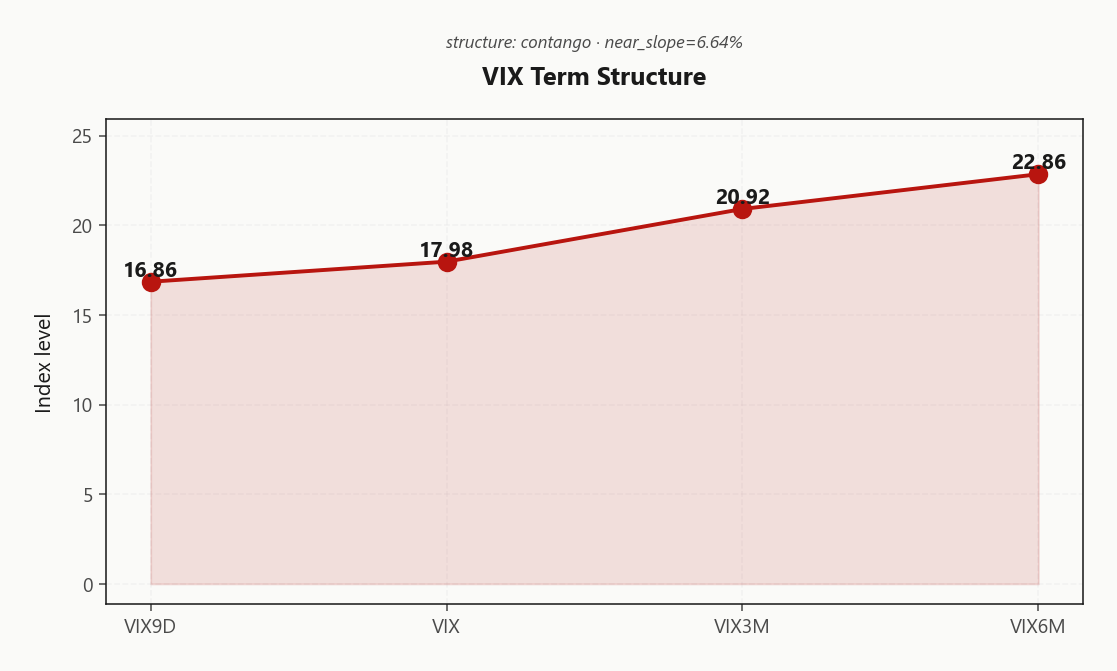

Forward 30-to-60 lands at 22.244761181 with 60-to-90 at 24.6477747474 - the carry exists and pays, but it is muted versus deep-contango regimes where the back tells you to sell everything with a wing. VVIX at 91.18 keeps vol-of-vol in the Normal zone, so the curve is honest, not distorted by jump pricing.

Operational read: vol sellers are favored, with cleanest edge in the 30-45 DTE window - far enough out the curve to harvest the slope, short enough of duration to avoid the back-end risk premium, and crucially outside the front-week zone where Iran headline risk can still gap an unhedged short.

What it means for your trading

Steep contango with VIX9D 16.86 < VIX 17.98 < VIX3M 20.92 pays sellers, but muted forward carry at 22.244761181 means concentrate in 30-45 DTE - front-week is exposed to headline gap risk.

Trading readContango with slope 6.64% - short-vol carry is paid, but the steepness says the market expects today's elevated front to come down, not blow out.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV on SPY at 15.54% trades a clean premium to HV20 10.71, with HV60 14.87 showing realized has cooled off the longer baseline. VRP of 4.83% is paid - options are rich to what the tape has actually delivered, and the carry is real. The catch: spot sits in Negative Gamma, so the path between print and expiry is jumpier than the implied/realized spread suggests.

QQQ ATM IV at 22.74% runs materially hotter than SPY with VRP 5.31% - single-name tech vol is funding the index complex, and it's where the cleanest harvest lives given QQQ's positive-gamma cushion. IWM VRP 3.7% rounds out the picture: premium is paid across the board, but the regime split dictates structure.

Trade: sell the premium, but wing it. Naked short gamma below SPY flip is the wrong expression - defined-risk condors in QQQ and spreads in SPY capture the carry without eating the path.

What it means for your trading

VRP 4.83% says sell premium; Negative Gamma says do it with wings. QQQ's 5.31% is the cleaner harvest given its positive-gamma cushion.

Skew Convexity

Quarter-delta put skew prints 2.71% with a smile ratio of 1.14% - left-tail pricing is ordered, not panicked. Put 25d IV at 22.41% against ATM 20.8% is a modest downside premium; call 25d at 19.7% trades below ATM, meaning the market is not paying for upside convexity. Wings are bid for hedge, not for crash.

IWM tells a different story - quarter-delta skew at 3.71% sits steeper than SPY, with small-caps absorbing the tail premium the index complex refuses to pay. That's consistent with the Negative Gamma profile and the cross-asset divergence reading of Qqq Heavier.

Section signal reads Skew Steep: skew is steep enough that naked long puts are inefficient - put spreads dominate on cost-per-unit, and call overwriting still gets paid despite the flat upside curve. Lean into structured downside, fade naked tail.

What it means for your trading

Ordered put bid with no upside conviction - skew is steep but not panicked, so prefer put spreads over naked puts and harvest the call wing where 19.7% sits below 20.8%. IWM at 3.71% is where the real tail premium lives.

Vol-of-Vol Structure

VVIX prints 91.18 against a VIX of 17.98, putting the ratio at 5.07 - squarely in the Normal zone. The vol-of-vol tape is down on the day (-1.89%) even with Iran headlines live, which tells you jump-risk pricing is softening, not stacking. No bimodal distribution baked into wing vega here.

Translation: this is an orderly vol regime, not a binary one. Sizing guidance reads Standard Size - you do not need to half-size structures, and the carry trade in 30-45 DTE iron condors is intact. The market is paying you to underwrite vol-of-vol at these levels.

What flips the script: any spike that breaks VVIX out of the normal band would signal binary positioning reasserting and force a re-rack on size. Until then, treat the VVIX print as a green light for premium harvest - the dealer-flow asymmetry in SPY is a path concern, not a vol-of-vol concern.

What it means for your trading

VVIX at 91.18 with a VVIX/VIX ratio of 5.07 confirms an orderly, non-binary vol regime - Standard Size is appropriate, and only a spike above the normal band would force a sizing rethink.

Dispersion Spread

QQQ ATM IV at 22.74% runs materially hotter than SPY's 15.54% - classic single-name dispersion paying the carriers. Megacap idiosyncratic vol is doing the work; index correlation dilutes the constituent premium when it lands at the SPY level, which is precisely why index hedges look cheap on a per-unit basis right now.

The cleaner harvest is at the index. SPY VRP at 4.83% is a tractable carry - defined-risk wings around the put wall at 730.00 and call wall at 740.00 beat chasing single-name premium that requires you to absorb each constituent's path risk. Dispersion as a trade is for vol-arb books; for directional risk-takers, sell the index where correlation is the silent partner.

Section signal reads Moderate - paid but not extreme. Don't size like a dislocation; size like a regime.

What it means for your trading

QQQ IV at 22.74% over SPY's 15.54% says single-name dispersion is the funder - harvest at the index level where SPY VRP 4.83% offers cleaner carry than chasing constituent premium.

Liquidity & Microstructure

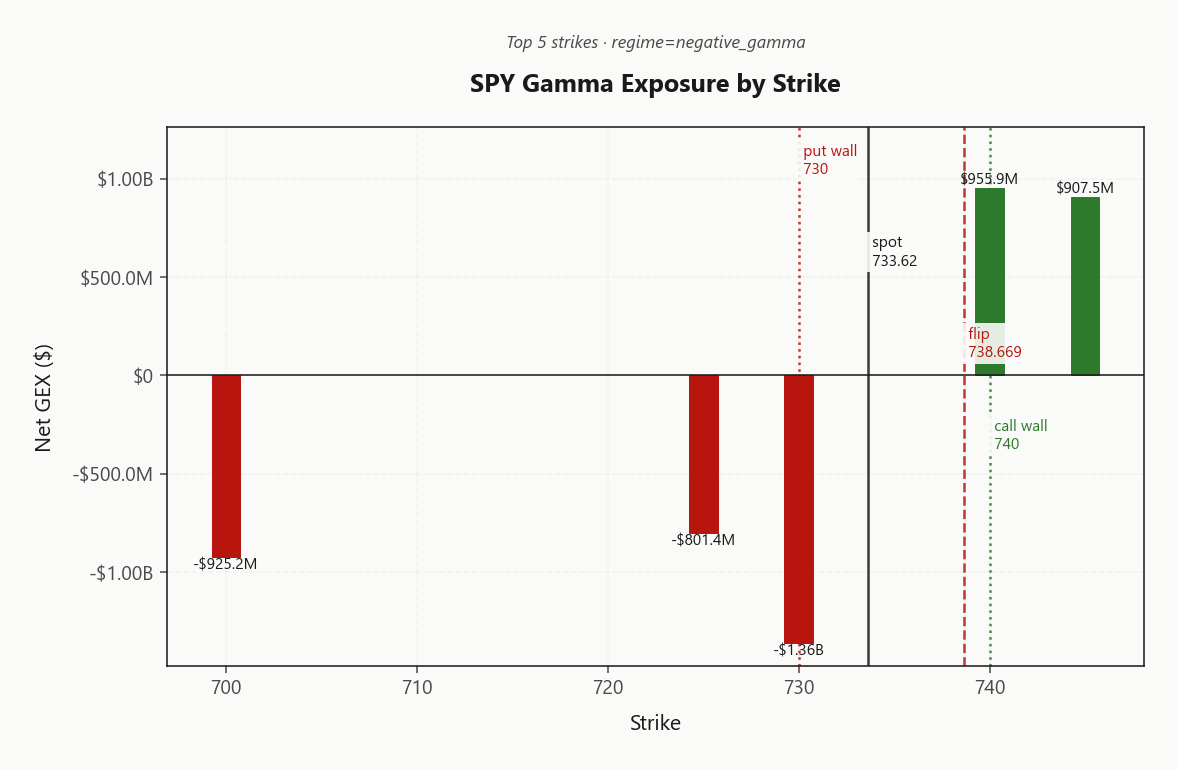

The book pins to 738.67 as the magnet - spot at 733.62 sits below the flip, putting dealers firmly in Negative Gamma where every uptick fights hedging and every downtick gets amplified. Highest OI parks at 700, a legacy hedge stack well below spot - informational, not the active battleground.

The live fight is at 730.00, carrying net GEX of -$1.36B - the put wall at 730.00 is where dealer short-gamma bites hardest. Above, the call wall at 740.00 caps any squeeze; between them, dealers transmit rather than absorb.

Trade the edges, not the middle. Reclaim of 738.67 flips the regime to dampening and unwinds the vanna acceleration risk; a clean break of 730.00 opens momentum to the downside with no dealer brake until the next OI shelf.

What it means for your trading

Gamma flip at 738.67 is the only level that matters - above it dealers stabilize, below it they amplify, and spot at 733.62 sits on the wrong side. Put wall 730.00 is the line; lose it and momentum opens up.

Trading readSPY's gamma profile is short below 738.67 and long above 740.00 - the tape between these levels is where dealers amplify any move. Trade the edges, not the middle.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The operational pivot is 730 - a Put Wall sitting -0.4934434721 from spot at 733.62. Current bias reads Neutral, but that label flips the moment that level breaks - lose it and momentum opens; reclaim it and dealer hedging starts dampening rather than amplifying.

The accelerant is concentration: 0DTE carries 23.9% of total gamma, so the vanna/charm transmission is most violent into the afternoon. Below the gamma flip at 738.67, do not write undefined short premium - the vanna kick on any 91.18 reset is real, and QQQ at Positive Gamma will not save SPY books.

What it means for your trading

Three greeks aligned against the long with -$185.82B as the lever - trade defined-risk only below 738.67 and watch 730 for the bias flip.

Cross-Asset Confirmation

Rate vol and sentiment refuse to confirm the equity-vol bid. MOVE sits at 86.07 - credit is not flagging stress - while Fear & Greed prints 61 (Greed) straight into the Iran tape. When the sentiment gauge refuses to crack on geopolitics and rate vol stays benign, you are looking at geopolitical premium without macro contagion - a mean-reverting setup, not a compounding crisis.

The index complex echoes the same split. QQQ at 701.32 holds Positive Gamma while IWM at 271.87 sits in Negative Gamma - large-cap dealer books absorb the shock, small-caps transmit it. Cross-asset signal reads Aligned; the divergence direction is Qqq Heavier.

Trade the divergence, not the headline. Long QQQ vol-carry against short IWM tail, defined-risk only below SPY's flip at 738.67. The breakdown trigger is MOVE leaking higher with F&G rolling under - until then, fade panic prints.

What it means for your trading

Credit calm at 86.07 and Greed sentiment veto the equity-vol regime shift; the QQQ-absorbs / IWM-transmits split is the playable asymmetry, not the Iran tape itself.

Scenario EV

Scoring lands on Iron Condor as the top structure at 55, beating the directional put spread at 47 - wings on both sides clear the regime test cleanly. VRP is paid at 4.83%, term structure runs Contango, and VVIX sits in the Normal zone - three independent reads all saying carry exists without binary tail pricing.

Sweet spot is the 30-45 DTE window - far enough from 0DTE chop and Iran headline gamma, close enough that theta still bites before event premium decays out the curve. Body candidate sits between max pain at 715.00 and the put wall at 730.00; call wing prints behind 740.00.

Sizing stays at Standard Size - no need to shrink with VVIX where it is, but the tail hedge is cheap enough to layer if SPY loses 738.67. Sell the wings, not the middle.

What it means for your trading

Iron condor at 55 beats put spread at 47 - deploy in the 30-45 window with body around 715.00, sized Standard Size.

DO: Iron Condor in the 30-45 DTE window, sized Standard Size - scenario score 55 beats the put-spread alternative at 47. Fade strength into the SPY call wall at 740.00; buy weakness toward the put wall at 730.00 only with defined-risk wings. Pair the condor with long QQQ premium harvest against short SPY/IWM exposure to monetise the regime divergence.

WATCH: SPY 730 - the Put Wall pivot, currently -0.4934434721 from spot, flips dealer bias. AVOID: undefined short puts below 738.67 - net VEX at -$185.82B means any vol uptick forces dealer delta-selling and the vanna doom-loop is live.

What it means for your trading

Sell the Iron Condor in 30-45 DTE with QQQ as the cleaner host, gate the trade on SPY reclaiming 738.67, and keep wings in place below 730.00 where dealer vanna at -$185.82B accelerates downside.

Iran peace proposal with US troop withdrawal is the biggest single tape-mover today - any de-escalation crushes the put skew premium baked into wing IVs.

Reuters framing of the ceasefire as 'knife edge' captures why front-week SPY IV stays bid even as VVIX softens - binary headline risk priced into 0DTE-to-1W.

Gold near six-week low on rate-hike bets is the cross-asset confirmation that this is being priced as a growth/inflation scare, not a flight-to-quality panic.

Dollar strength on Fed-vs-Middle-East mix is the cleanest read on positioning - DXY bid while VIX stays subdued = institutional belief in mean reversion.

Trump signaling delay on Iran strike is exactly the kind of headline that justifies selling premium in the 30-45 window - event risk being pushed out the curve.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 738.67 against a spot of 733.62. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.54% with a volatility risk premium of 4.83%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.98. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime