Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY trades at 734.48, sitting in Negative Gamma territory with net GEX of -$5.88B - dealers are short gamma and any move gets amplified. Key levels: call wall at 740.00, put wall at 730.00, gamma flip at 738.68; spot is below the flip, so dealers sell into weakness and buy into strength. Dealer positioning shows net vanna at -$192.67B - rising vol pushes dealers to sell delta, making downside accelerant if VIX kicks. Vol regime: VIX at 18.16, VVIX at 95.86, term structure in Contango with near slope at 6.26%% - VRP remains positive at 3.75%, so options are rich to recent realized. Cross-asset: QQQ holds Positive Gamma above its flip at 599.78 while IWM sits in Negative Gamma - divergence is Qqq Heavier. Recommended structure for the regime is Iron Condor in the 30-45 DTE window, sizing at Standard Size. Bottom line: trade SPY mean-reversion only above the flip; below it, expect trend extension toward 730.00 or 700.

SPY sits below its gamma flip at 738.68 with dealers short gamma, while QQQ holds firmly above its own flip in positive-gamma territory - a textbook regime divergence with the tech complex acting as stabilizer. VIX term structure remains in contango at Contango and VVIX prints Normal, so the vol-seller carry trade is intact even as charm pivot signals destabilizing dealer flow on SPY. Bottom line: fade into walls on QQQ, but respect amplification risk on SPY until spot reclaims 738.68.

Regime Assessment

Vol regime registers Elevated / Watchful with VIX printing 18.16 - the tape sits in Elevated territory but conspicuously lacks the convexity bid that defines true stress. Neither a break to panic nor a melt to the low band is being priced; this is the long middle of the vol distribution, and it is sticky.

Half-life pegs at 15 sessions - meaningful mean-reversion is a multi-week affair, not a one-print event. The five-session panic transition probability prints at 0.05 against a ten-session melt-to-low probability of 0.45. The asymmetry favors accepting carry over paying for tails.

Operational read: short-premium structures get paid for sitting still, but size them as if the regime persists - because statistically it does. Reload the same trade after each refresh and resist pressing for a one-way resolution the transition matrix says is not coming.

What it means for your trading

The Elevated / Watchful regime with half-life 15 sessions is the operating backdrop: stay short premium, sized for persistence, and stop hunting a binary break the probabilities don't support.

Trading readVIX up, VVIX up faster, SKEW elevated, MOVE quiet - equity vol-of-vol is doing the worrying while credit stays calm. This is geopolitical-headline pricing, not a credit regime shift.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

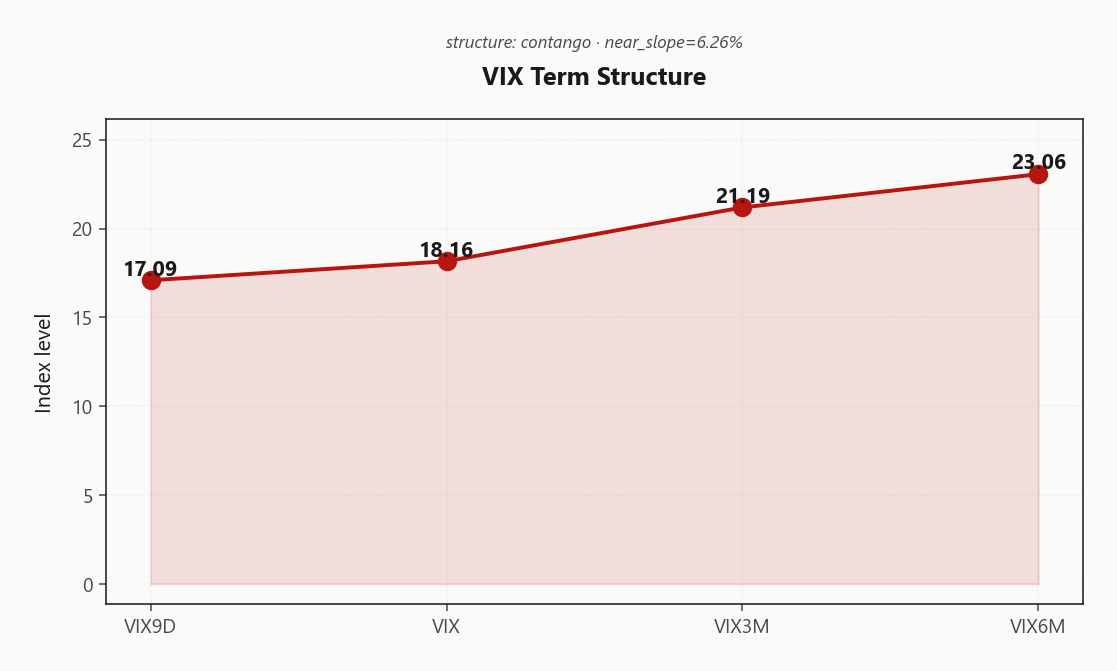

Forward Vol Geometry

The vol curve sits in Contango, with VIX9D at 17.09 stacking cleanly below spot VIX at 18.16 and VIX3M at 21.19 - zero event premium being priced into the front. Forward 30→60 vol prints 22.5528568035 with the 60→90 leg extending to 24.7893344001, confirming the Steep Contango read.

Near-slope of 6.26% is the carry edge, but the cleanest expression sits in the 30-60 DTE belly where forward implieds bake in meaningful cheapness versus spot vol. The 6M anchor at 23.06 caps back-end compression, leaving the belly as the structural sweet spot for roll harvesting.

Net read: Steep contango - vol sellers favored. Sell front gamma, own belly vega; calendars in the 30-45 DTE window monetize the slope without paying for tail premium the curve is explicitly refusing to underwrite.

What it means for your trading

Curve regime is Steep contango - vol sellers favored with no near-term event kink - the 30-60 DTE belly offers the cleanest forward-vol carry against spot, favoring calendar and diagonal structures over front-month naked premium.

Trading readContango with 6.26%% near-slope - vol carry trade is live and the market is not pricing any near-term stress event.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV prints 14.34% against an HV20 of 10.59, leaving a clean VRP of 3.75% vol points on the table. Realized cooled hard into the print - HV20 sits well below the trailing HV60 of 14.85, so the recent tape has been quieter than the two-month base while implieds refused to follow it down.

That gap is meaningful but not crowded - premium sellers are getting paid for the carry without the reflexive squeeze risk of a stretched short-vol book. The IV/RV wedge supports defined-risk short-premium structures, particularly when overlaid on positive-gamma single names where dealer hedging dampens path risk rather than amplifying it.

Pair the rich vol with the Positive Gamma cushion in QQQ rather than pressing it against SPY's sub-flip tape - that's where the VRP edge converts to realized P&L instead of getting chopped by amplification flow.

What it means for your trading

Implieds at 14.34% are richly priced versus realized of 10.59, but the 3.75%-point VRP is exploitable rather than crowded - favor defined-risk premium selling, ideally anchored on positive-gamma underliers.

Skew Convexity

The quarter-delta put-call skew on SPY prints 2.59% vol points with a smile ratio of 1.15% - downside is bid, but the curve is orderly, not panicked. Put quarter-delta IV at 19.54% sits clearly rich to ATM at 18.16%, while call quarter-delta lags at 16.95% - a textbook hedged-but-not-hunted profile with zero upside chase being priced.

Read the smile: puts pay a premium, calls are flat-to-cheap, and there is no crash bid clawing the near-dated wings. That argues for monetizing the skew via defined-risk put structures rather than outright tail-buying - the carry cost on naked puts is real with VRP still positive, and the wings are not where the convexity lives today.

Net: put spreads over naked puts, sell the inflated put quarter-delta against a further-OTM long, and resist financing with short calls - the upside is cheap for a reason, and giving it away into the 740.00 wall is dollar-foolish.

What it means for your trading

Skew at 2.59% with smile ratio 1.15% is steep-but-orderly - express downside views through put spreads to harvest the bid skew without paying for tails.

Vol-of-Vol Structure

VVIX prints 95.86 against VIX at 18.16, a ratio of 5.28 that parks vol-of-vol squarely in Normal territory. No bimodal pricing, no jump premium being paid - the tape is not bracing for a binary. That keeps the carry trade clean and argues for Standard Size on premium-short structures rather than the defensive trim the headlines might suggest.

The quiet flag is the intraday tape: VVIX is up 5.13%% while spot VIX barely budges. That's geopolitical-headline pricing - convexity getting bid without front-month following - and it's exactly the kind of asymmetric tell that precedes a vol-of-vol regime shift if the ceasefire narrative cracks. Watch the close: another leg higher in VVIX without VIX confirmation flips the sizing call.

What it means for your trading

Vol-of-vol reads Normal at a VVIX/VIX of 5.28, supporting Standard Size - but the 5.13%% VVIX pop without a VIX echo is a quiet convexity bid worth monitoring into the close.

Dispersion Spread

Index-level vol is trading at a meaningful discount to its constituents: SPY ATM IV prints 14.34% against QQQ at 21.16% and IWM at 19.93%. That gap is the dispersion tell - correlation is being marked lower, single-name vol is doing the work, and the index complex is the cheap leg of the carry. With QQQ in Positive Gamma above its flip while SPY sits Negative Gamma, the mega-cap divergence - led by the AAPL / NVDA / MSFT cohort - is precisely what's holding index correlation suppressed.

Translation for the book: index hedges are not capturing today's idiosyncratic event risk, so paying SPX premium for downside protection is the wrong vehicle. Lean the other way - short SPY/SPX premium into the 740.00 / 730.00 envelope and own select single-name vol where catalysts live. The dispersion trade is paying; the QQQ-vs-SPY IV spread is the cleanest expression.

What it means for your trading

Index IV at 14.34% trading well inside QQQ 21.16% and IWM 19.93% means correlation is suppressed and dispersion is paying - sell index premium, own single-name vol.

Liquidity & Microstructure

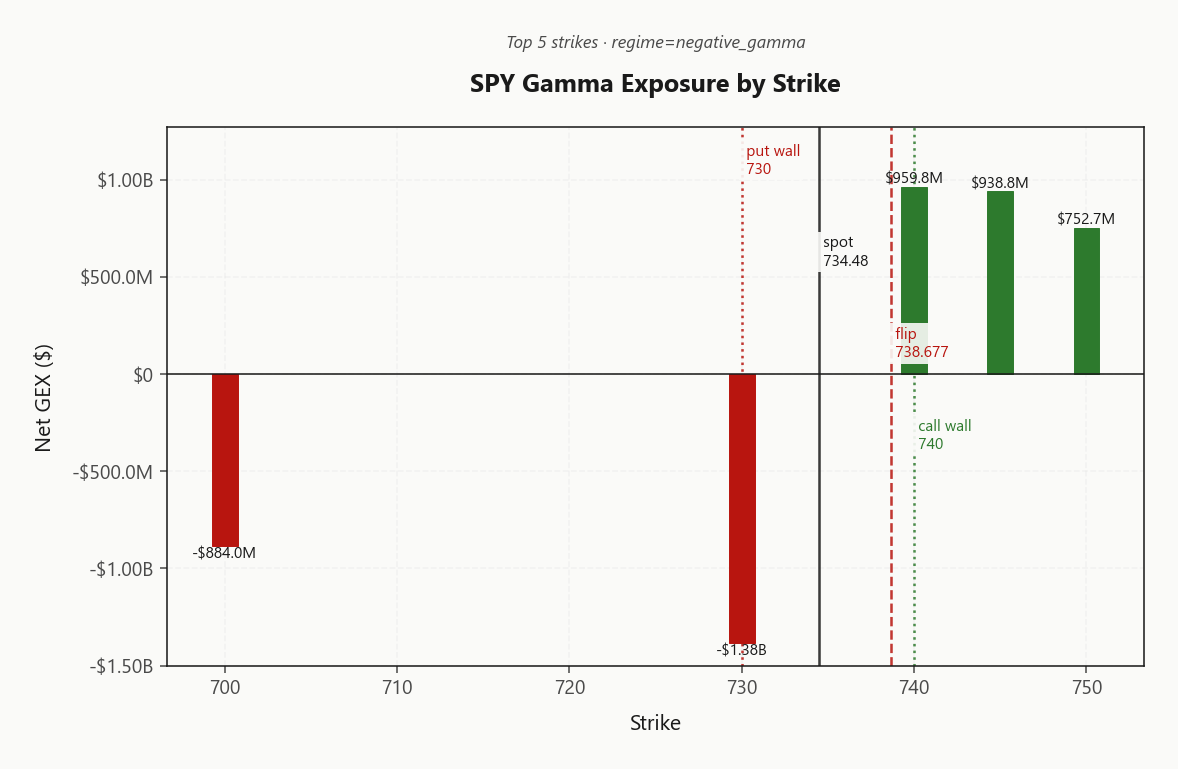

The book is anchored at the 700 top-OI strike, but the active gravity well is 730.00, where -$1.38B of negative GEX is concentrating dealer hedging flow into a single node. With spot tracking below the gamma flip at 738.68, that node is acting as a magnet rather than a wall - every tick lower forces incremental supply, every tick higher pulls covering bids.

The structural map runs put wall 730.00, gamma flip 738.68, call wall 740.00. Until spot reclaims the flip, dealer flow is destabilizing - sell-into-weakness, buy-into-strength - and the path of least resistance is range extension toward the put wall complex. Above the flip the same book inverts into a stabilizing, mean-reverting bid.

Trade it: respect 738.68 as the regime line. Below, fade rallies into the heavy strike and defend toward 730.00; above, sell premium against 740.00 with confidence the book damps the tape.

What it means for your trading

Spot below 738.68 with the heaviest GEX node at 730.00 means dealer flow is currently an accelerant, not a brake - reclaim of the flip is the only thing that flips the book back to stabilizing.

Trading readSPY's heaviest negative-GEX cluster sits just above spot - the tape is in a sell-rallies, buy-dips amplification zone until 738.68 is reclaimed. Above that level, dealer flow flips to stabilizing.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The whole regime hinges on 738.6765500115 - the charm pivot mapped to the gamma flip. Current bias is Destabilizing with spot trading below the line, meaning dealer flow amplifies rather than dampens. Reclaim flips desks from sellers-of-weakness to buyers-of-strength; failure leaves the trio of greeks misaligned and the tape gappy.

Trade implication: respect the asymmetry. Long-vol hedges via VVIX-sensitive structures pay if spot rolls; defined-risk premium sales only above the pivot. Below it, vanna does the steering.

What it means for your trading

Vanna is the accelerant and charm the weak floor - until SPY reclaims 738.6765500115, dealer hedging amplifies any move and the bias stays Destabilizing.

Cross-Asset Confirmation

Cross-asset tape reads as an equity-led wobble, not a credit or macro regime shift. MOVE sits at 86.07 - rates vol is quiet, credit channels show no stress, and the bond complex is refusing to confirm the equity flinch. Fear & Greed prints 61 in Greed territory, which keeps the broader risk appetite on the constructive side of neutral.

The story underneath is the regime split: QQQ holds 701.23 above its flip in Positive Gamma, while IWM at 273.19 sits weak in Negative Gamma sub-flip territory. Cross-asset regime divergence reads Qqq Heavier - mega-cap tech is doing the stabilizing work while small-caps absorb the fragility.

Without credit or rates confirmation, this is a mean-reversion setup, not a regime change. Fade weakness toward QQQ's flip as the cushion; respect IWM as the canary if MOVE or VVIX start aligning to the downside.

What it means for your trading

MOVE at 86.07 and F&G in Greed confirm equity isolation - no credit or macro contagion. Base case stays mean-reversion until IWM-led weakness gets a MOVE confirmation.

Scenario EV

Scoring favors Iron Condor in the 30-45 DTE window, printing 50 against a put spread at 41. With VIX term structure in Contango and VVIX parked at Normal, the carry geometry pays defined-risk premium sellers cleanly - naked strangles get no marginal edge for the gamma risk taken.

Anchor short wings outside 730.00 and 740.00, sized at Standard Size. The belly of the curve is where forward vol implies the richest carry against spot, and the 30-45 tenor sidesteps the destabilizing charm pivot at 738.6765500115 without reaching into back-month vega exposure.

Caveat: SPY trades Negative Gamma below the flip at 738.68 - stand down condor deployment on the index leg until spot reclaims, or shift the structure onto Positive Gamma QQQ where dealer flow stabilizes rather than amplifies.

What it means for your trading

Iron condor at 30-45 DTE is the cleanest expression of contango carry plus normal vol-of-vol, scoring 50 versus put spread 41. Deploy on QQQ first, gate the SPY leg on a reclaim of 738.68.

Actionable Summary

Bottom line: deploy Iron Condor structures in the 30-45 DTE window, anchoring short strikes outside 730.00 and 740.00. The trade earns its keep from Contango carry and a live VRP of 3.75%, with VVIX still parked in Normal territory at 95.86 - size Standard Size.

The level that matters is 738.6765500115: above it, dealer flow turns stabilizing and rallies into the call wall are fadeable; below it, vanna and charm align Destabilizing and downside extends toward 730.00. Avoid naked short premium on SPY until spot reclaims the flip - pivot to long-vol if VVIX breaks higher from 95.86. Regime call: Elevated / Watchful, with QQQ Positive Gamma doing the cushioning while SPY works through the sub-flip air pocket.

What it means for your trading

Sell defined-risk premium outside the walls in the 30-45 window; trade above 738.6765500115 as mean-reverting and below it as trend-extending.

G7 finance ministers acknowledging the need for action on imbalances is a soft signal that policy coordination remains intact - markets care because it lowers tail risk of unilateral FX/trade moves.

Iran's peace proposal including US troop withdrawal terms is the headline that's keeping a ceiling on oil and helping equity indices despite the equity weakness - directly explains the VIX/VVIX divergence.

Reuters framing the ceasefire as 'on a knife edge' is exactly the kind of binary-event setup that pumps VVIX without lifting spot VIX - vol-of-vol bid is rational.

Inflation fears taking root keeps the rates side priced for caution, which is why MOVE has not collapsed even as equity vol stays contained - credit/equity vol decoupling matters for hedge construction.

Dollar strength on Fed outlook is a quiet tightening signal that puts a soft ceiling on equity multiples - relevant for anyone selling upside calls into the 740.00 wall.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.30 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 738.68 against a spot of 734.48. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.34% with a volatility risk premium of 3.75%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.16. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime