Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

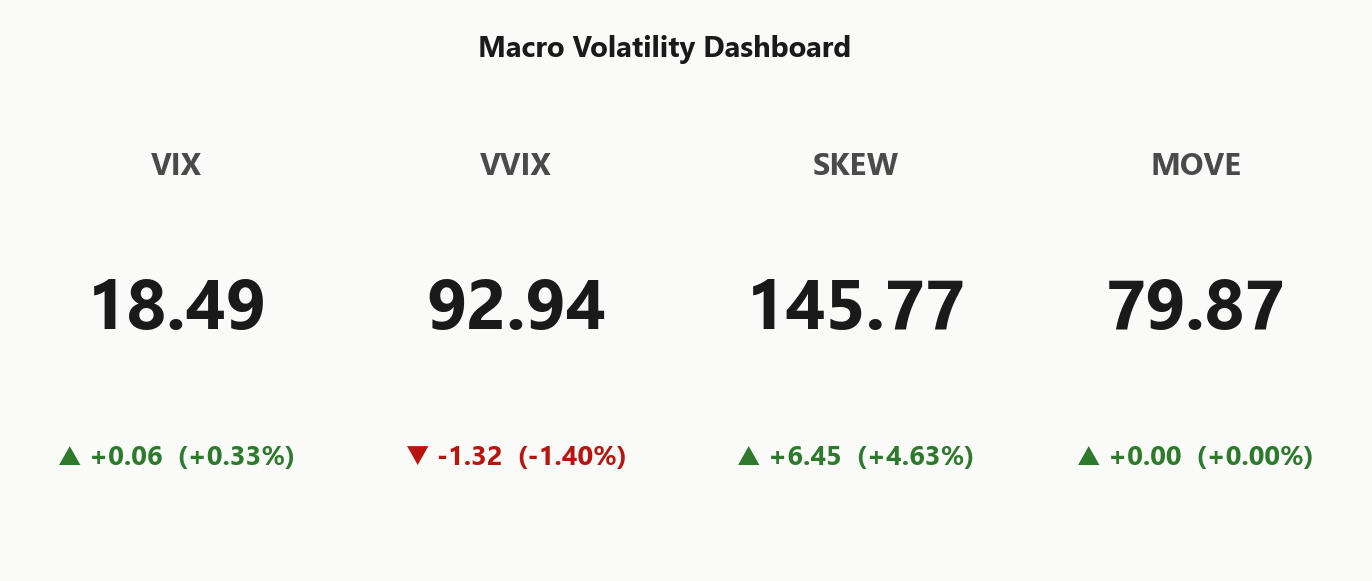

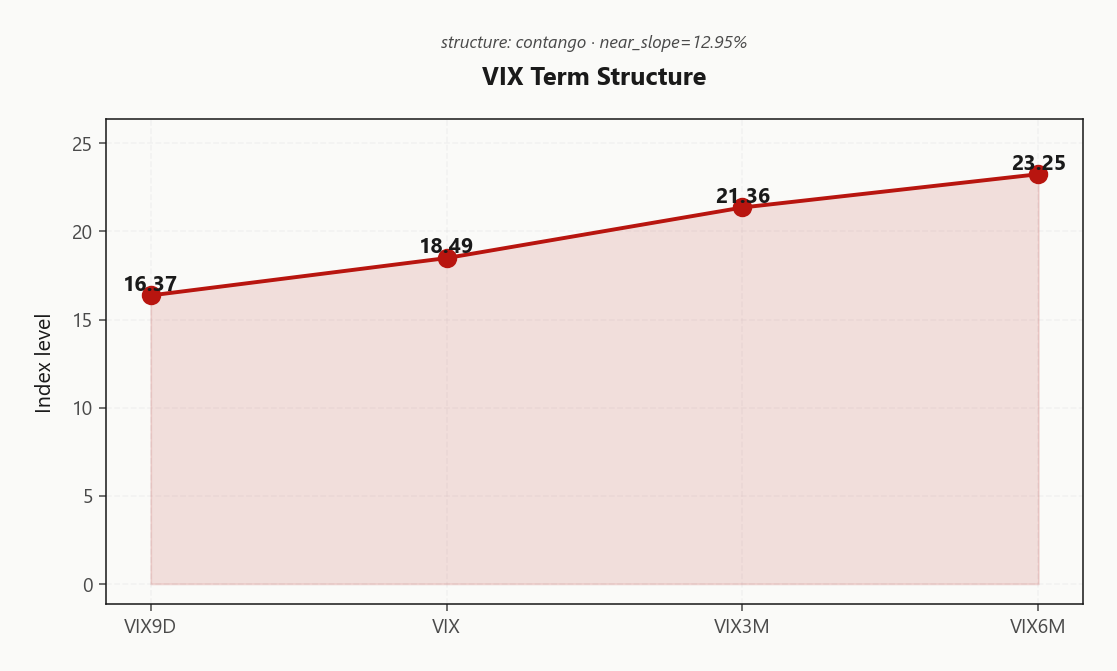

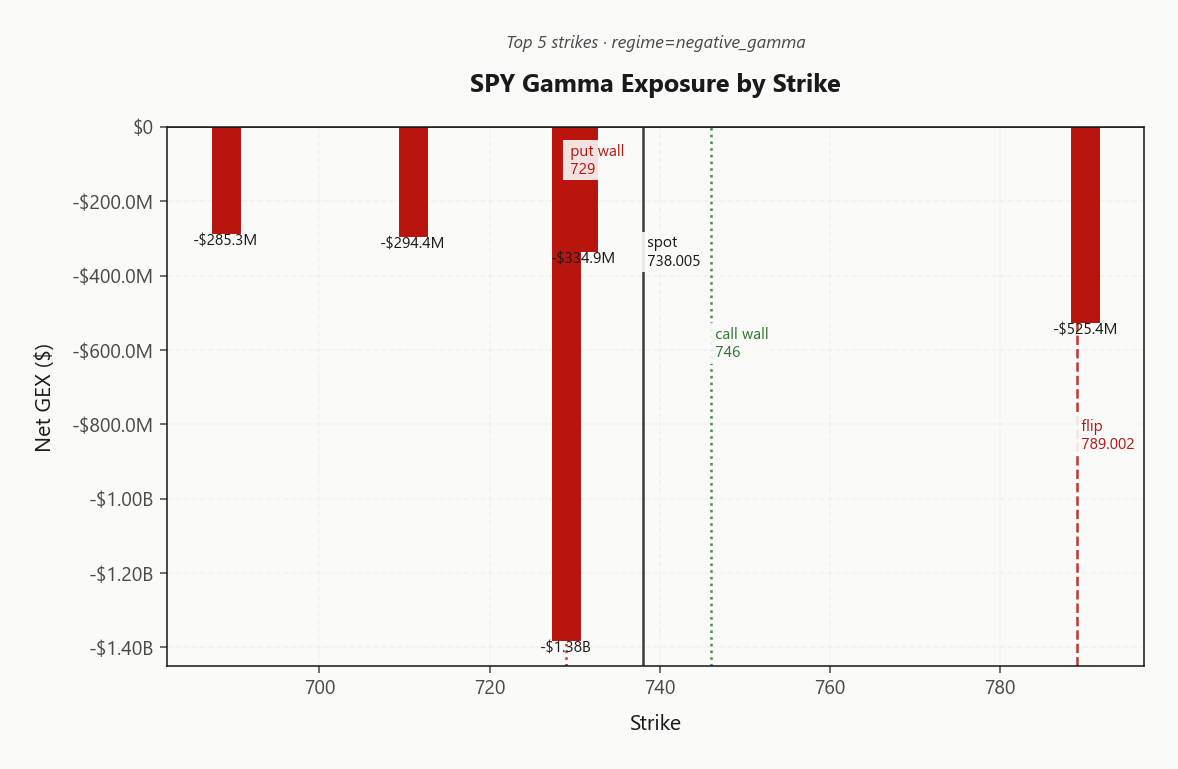

SPY trades at 738.01 with net GEX -$4B - squarely in Negative Gamma territory and well below the gamma flip at 789.00. Call wall sits at 746.00, put wall at 729.00, with the heaviest OI cluster up at 790 - meaning dealers amplify moves in both directions until spot reclaims 789.00. Dealer vanna at -$48.04B says any vol spike forces additional delta selling, and charm at -$1.3M adds late-day pressure. VIX at 18.49 with term structure Contango and near-slope 12.95%% confirms vol sellers are still paid the carry, and VVIX at 92.94 keeps sizing Standard Size. VRP at 3.91% with ATM IV 14.61% over HV20 10.7 means options are rich to recent realized. Bottom line: structure favors Iron Condor in the 30-45 DTE window - avoid naked short gamma until spot reclaims the flip.

Negative gamma across index complex with Steep Contango VIX curve - amplified moves, vol sellers still paid

SPY sits deep below the gamma flip at 789.00 with dealers short gamma across the index complex, meaning every move gets amplified rather than dampened. Yet VIX term structure remains in Steep Contango and VVIX prints Normal, so the carry trade still pays - just sized smaller. The tension: short-dated dealer flow is hostile, but forward vol geometry rewards patient premium sellers.

Regime Assessment

Regime sits Elevated - Elevated / Watchful - with VIX printing 18.49 against a backdrop of negative gamma across the index complex and uninterrupted contango through 23.25. The tape is fragile but not fracturing: dealers amplify moves below the flip at 789.00, yet VVIX at 92.94 and the Normal vol-of-vol read say no binary jump premium is being paid.

Transition probabilities matter more than today's print. Move-to-panic over five sessions sits at 0.05 - a low bar absent a fresh catalyst - while decay-to-low over ten sessions runs 0.45, the asymmetry that funds the carry. Cross-asset reads Aligned: SPY, QQQ and IWM all sub-flip, MOVE at 79.87 not confirming equity stress.

Half-life clocks 15 sessions - this regime is sticky, fade trades have runway. Structure favors Iron Condor in the 30-45 DTE window; the watchful label means sized standard, not pressed.

What it means for your trading

Elevated but stable - half-life of 15 sessions and to-low odds of 0.45 say premium sellers get paid to wait, while 0.05 panic odds keep tail hedges cheap-enough to carry.

Trading readVIX up, VVIX down, SKEW up, MOVE flat - divergence is the story: equity tail is being paid up while vol-of-vol softens and bond vol stays calm. That mix usually means positioning, not fundamentals, is driving the bid for tails.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX complex is in Steep Contango from the front through the back: 16.37 on VIX9D ramps to 18.49 spot, 21.36 at three-month, and 23.25 out to six - an uninterrupted upward staircase. Term structure prints Contango with near-slope at 12.95%%, wide enough to fund meaningful roll-down for sellers who can stomach the gamma backdrop.

The forward kink is where the edge lives. Forward 30-60 vol at 22.6590897875 sits well above spot VIX, with forward 60-90 stretching further to 24.9975078758 - the curve is pricing structurally higher vol later, not stress now. That geometry is the textbook calendar setup and tilts the carry trade firmly into the 30-45 DTE window.

Regime label reads Steep Contango, signal green. Lean into the middle of the curve, fund roll-down with the front, and let the backs do the hedging work.

What it means for your trading

VIX Contango from VIX9D through VIX6M with the forward 30-60 kink at 22.6590897875 defines a Steep Contango regime - sell front, harvest in the 30-45 DTE pocket where the curve pays best.

Trading readContango at every kink with VIX3M well above spot VIX - the vol-carry trade is mechanically there and the market is NOT pricing stress, it's pricing structurally elevated baseline. Sell front, hedge with backs.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.61% sits comfortably rich to HV20 at 10.7 - the cleanest VRP print of the session and the structural reason premium sellers are still being paid despite the negative gamma backdrop. Realized has been compressed while implied holds its bid, and HV60 at 14.97 printing above the 20-day tells you the realized path is decelerating, not accelerating into the tape.

VRP at 3.91% quantifies the carry: options are demonstrably rich to what the underlying has actually delivered. This is the textbook harvest setup - implieds anchored by dealer short-gamma defensiveness and headline tail bid, while the realized engine keeps grinding lower. The math favors the seller.

The caveat is non-trivial. With dealers short gamma and net VEX -$48.04B, any RV bump translates to outsized spot moves - the same negative convexity that keeps IV firm will punish naked short gamma if realized snaps higher. Size the harvest in the 30-45 DTE window with defined wings, not open-ended exposure.

What it means for your trading

VRP at 3.91% with ATM IV 14.61% well above HV20 10.7 is an active short-vol harvest signal, but negative gamma means the trade only pays cleanly when expressed as defined-risk condors in the 30-45 DTE window - not naked premium.

Skew Convexity

Quarter-delta put skew is steep at 2.43% with the smile ratio printing 1.16% - the left wing is convex, the right is asleep. Put-25d IV at 18.08% against ATM 16.34% and call-25d 15.65% says downside is being bid up while upside conviction is absent. Classic defensive posture: hedgers are paying for tail, no one is reaching for calls.

SKEW index at 145.77 corroborates the intensifying tail bid, and with VVIX still Normal the convexity is being paid through the wing, not through vol-of-vol. That mix favors structure over outright: finance long puts via call-wing sales, lean on put-spreads instead of naked premium, and let the condor wings sit outside the put wall at 729.00 where dealer-buying re-engages.

Bottom line: the wing is rich enough to sell against, not cheap enough to chase. Spread structures harvest the skew without paying the steep put-25d premium outright.

What it means for your trading

Steep put skew with muted call wing and SKEW at 145.77 - express downside via spreads, not naked puts, and harvest the wing premium through condors with strikes anchored outside 729.00.

Vol-of-Vol Structure

VVIX prints 92.94 against VIX at 18.49, putting the ratio at 5.03 - squarely Normal with no binary jump-risk premium being paid. The vol-of-vol surface is not bracing for a regime break; the tape is pricing an elevated baseline, not a tail event.

That benign signal is the green light for sizing. Guidance reads Standard Size - no need to trim condors or calendars on jump-risk grounds, even with dealers short gamma below the flip. The setup is asymmetric in your favor: forward vol geometry pays, VVIX is not flagging dislocation, and the Iron Condor in the 30-45 DTE window collects clean.

The watch item is VVIX softening into a stable-to-firmer VIX - that's the structural green light for premium harvest. The break condition is VVIX expanding faster than VIX: ratio lift toward the upper band re-prices every short-gamma book and forces a sizing cut before the surface gaps. Until then, stay full-sized inside the playbook.

What it means for your trading

Vol-of-vol at Normal with VVIX/VIX ratio at 5.03 clears premium sellers to run Standard Size; watch any VVIX expansion against a steady VIX as the first tell that the regime is breaking.

Dispersion Spread

Index vol is bid but unevenly: SPY ATM IV prints 14.61% while QQQ carries 22.93% and IWM 22.04% - tech and small-cap are paying a meaningful premium over the broad tape, telegraphing that idiosyncratic risk is being priced into the high-beta sleeves while the index proper trades closer to fair.

With cross-asset regime Aligned and all three complexes in Negative Gamma, correlation is moderate rather than crashing - exactly the geometry where SPY/SPX condors capture true index dispersion rather than single-name noise. The richer QQQ and IWM vol reflects component-level uncertainty that an index hedge cannot fully neutralize.

Bottom line: prefer broad-index premium sales in the 30-45 DTE window over single-name strangles. Naked short gamma in individual names is hostile while index GEX is negative and component IV is bid - let the dispersion work for you by selling the index, not the constituents.

What it means for your trading

QQQ at 22.93% and IWM at 22.04% priced well above SPY's 14.61% signals component-level fragility - sell the index, not the names.

Liquidity & Microstructure

Order-book topology is the tell today. Spot sits below the 789.00 gamma flip with the heaviest OI cluster parked up at 790 - a dealer magnet on any rally, but only after the call wall at 746.00 is taken. Below the flip, every dip gets sold harder and every rip into the upper strikes gets faded; the regime line is binary, not gradient.

The dominant pin sits on the put side: top strike 729.00 carries GEX of -$1.38B, anchoring the structure and reinforcing the 729.00 floor where dealer-buying mechanically kicks in. That's where the flow inverts on the downside - and where premium-sellers want their short put wings to sit.

Trade the topology, not the tape: structure is Deep, the walls are clean, and reclaim of 789.00 flips dealer flow from amplifier to dampener in one print.

What it means for your trading

Microstructure is bimodal around the 789.00 flip: below it dealers amplify, above it they suppress, with the 729.00 floor and 790 magnet bracketing the action. Set condor wings outside the walls and treat reclaim of the flip as the only signal that matters.

Trading readDealer dampening sits above at the 746.00 call wall and the 790 OI magnet, while amplification dominates the put-wall side at 729.00 - until spot reclaims 789.00, every dip gets sold harder and every rip into walls gets faded.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer vanna prints -$48.04B - deeply negative, meaning any uptick in 18.49 forces additional delta selling and accelerates downside. Charm reinforces the same direction at -$1.3M, layering late-session pressure as theta bleeds delta out of the book. Three Greeks pulling the same way: short gamma amplifies the tape, hostile vanna feeds on any vol spike, and charm tilts the close lower.

The pivot to watch is 746 - the Call Wall doubles as the charm inflection. Spot sits below it with current bias Neutral, meaning neither side carries dealer flow as a tailwind. Reclaim the pivot and the vanna/charm complex inverts from headwind to support; fail it and the negative-VEX feedback loop stays live into every VIX tick higher.

What it means for your trading

Vanna at -$48.04B and charm at -$1.3M are aligned hostile - the Call Wall at 746 is the regime line where dealer flow flips from accelerant to brake.

Cross-Asset Confirmation

Cross-asset signal reads positioning, not panic. MOVE at 79.87 shows bond vol refusing to confirm the equity tape - if this were a credit shock, rates vol would be screaming, and it isn't. Fear & Greed prints Greed at a score of 63, which is the tell: sentiment hasn't capitulated, this is dealer mechanics meeting Iran-war headline drag, not a fundamental break.

The index complex is in full alignment. QQQ at 707.39 and IWM at 276.46 both sit below their gamma flips alongside SPY - three negative-gamma books pulling the same direction, with cross-asset tone tagged Unknown and regime divergence Aligned. There is no safe-haven index hiding inside the complex today; fragility is uniform.

Practical read: with bonds calm and sentiment still greedy, the premium-selling carry trade survives, but the absence of a divergence lead means any break travels in correlated fashion. Keep tail hedges on, lean condors over directional puts.

What it means for your trading

MOVE at 79.87 and F&G at Greed say this is a positioning wobble, not a credit event - but with QQQ 707.39 and IWM 276.46 both below their flips in Aligned fashion, downside would travel correlated. Sell premium with wings, not naked.

Scenario EV

Structure of the day is Iron Condor in the 30-45 DTE window, scoring 53 against the alternative book. The geometry pays: Steep Contango VIX curve funds the roll-down, VRP reads Unknown with ATM IV at 14.61% over HV20 at 10.7, and VVIX at 92.94 keeps sizing at Standard Size. Wings outside the 746.00 call wall and 729.00 put wall, body straddling the OI magnet at 790.

Put-spread directional book scores 44 - meaningfully behind the condor because 2.43% skew is already paying for downside, and buying what the tape is bid for is the loser's trade. The charm pivot at 746 is the regime line; until spot reclaims it, dealer flow stays Neutral and naked short gamma in 0DTE is uncompensated against negative net GEX of -$4B.

Execution: sell the condor, finance tail puts with call-wing sales given flat upside skew, watch 746 for the flip signal.

What it means for your trading

Best risk-adjusted harvest is Iron Condor in 30-45 DTE - contango funds the carry, VRP at Unknown confirms the edge, and the put-spread score of 44 loses because skew is already bid. Avoid 0DTE naked gamma until spot reclaims 746.

Watch: charm pivot 746 is the regime line - reclaim flips dealer flow from amplifier to dampener; until then, spot below 789.00 keeps net VEX -$48.04B and CHEX -$1.3M pulling in the hostile direction. Regime reads Elevated / Watchful with half-life 15 sessions - fades have time.

Avoid: 0DTE naked short gamma, single-name strangles, and naked puts - skew at 2.43% is already paying. Hedge: tail puts financed by call-wing sales given the flat call skew.

What it means for your trading

Sell Iron Condor in 30-45 DTE with wings outside the walls; treat charm pivot 746 as the regime line and keep sizing Standard Size while VVIX is benign.

BoE-cut signal from the IMF in the middle of an Iran-war inflation scare is the kind of policy split that re-prices global rates and feeds the bond rout - direct read-through to MOVE and the front of the VIX curve.

A revised Iranian ceasefire proposal handed to Washington is the single biggest tail-risk-off catalyst on the wire today - if it gains traction, expect SKEW to compress and put skew to flatten fast.

Large bond-put bets pointing to higher rates confirm the global bond rout narrative - bearish for duration, supports the elevated MOVE backdrop and any TLT puts already in books.

Berkshire's disclosed Alphabet stake doubling explains the GOOGL GEX print and is the cleanest single-name catalyst in the tape - dealer positioning is now chasing a known long whale.

Trump's commentary on Intel raises the prospect of expanded government equity stakes - semis already volatile, this adds a policy-overhang component to single-name vol pricing.

The President explicitly linking Fed rate cuts to Iran war resolution converts a geopolitical headline into a Fed-path catalyst - every vol seller needs to discount cut hopes accordingly.

Bessent pushing G7 sanctions coordination keeps the Iran premium structurally bid in oil and credit - supports the call to keep tail hedges on even while selling 30-45 DTE premium.

Global bond rout deepening on inflation fears is the macro thread tying the day together - when bonds sell on stagflation worry, equity vol has a hard time decaying smoothly.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.43 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in Negative Gamma gamma with net dealer GEX at -$4B. The gamma flip sits at 789.00, with the call wall at 746.00 and the put wall at 729.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 789.00 against a spot of 738.01. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.61% with a volatility risk premium of 3.91%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.49. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime