Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

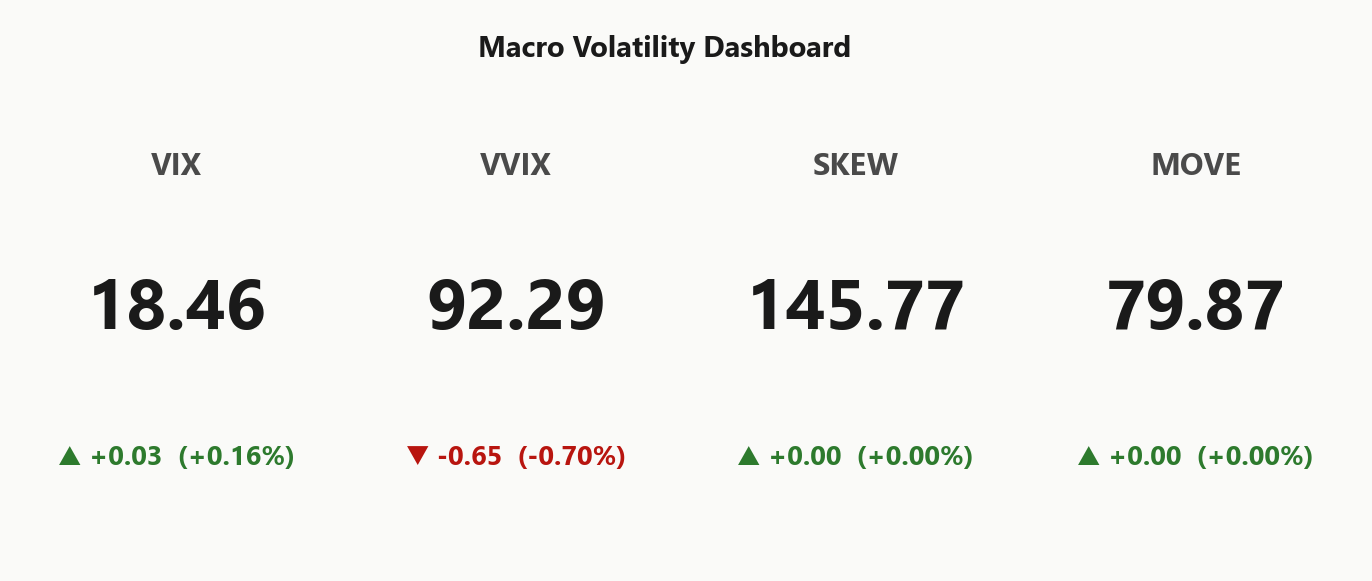

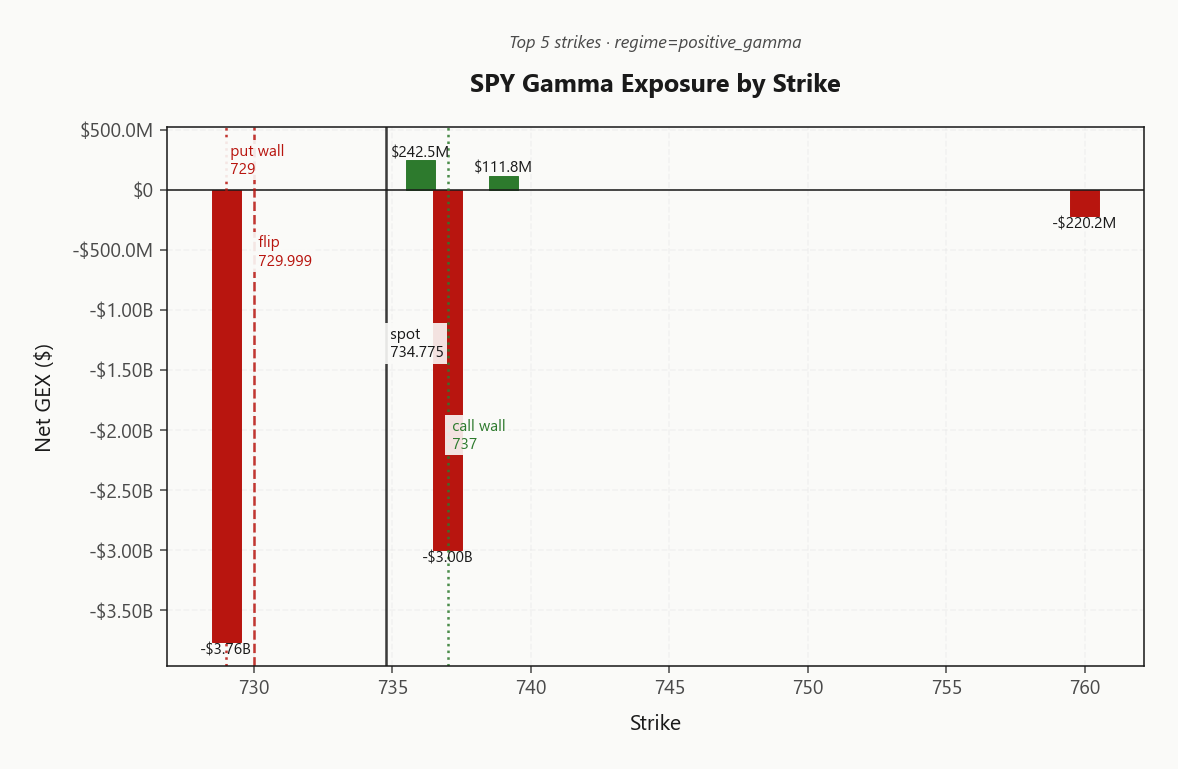

SPY trading 734.78 with regime Positive Gamma and net GEX -$7.25B - dealers long gamma, intraday moves get dampened. Call wall sits at 737.00, put wall at 729.00, gamma flip at 730.00; spot is comfortably above flip so dealer hedging supports dips. Net vanna -$185.57B means a vol spike still flips dealers to delta-sellers - vanna remains the hostile vector here. VIX at 18.46 with VIX9D/VIX3M term in Contango (6.77%% slope) and VVIX 92.29 signals normal-range vol-of-vol; VRP 5.07% keeps short premium attractive. Iran headlines and bond rout chatter justify keeping the tail hedge on. Bottom line: fade strength into 737.00, buy dips into 730.00, sized via iron condor in 30-45 DTE.

Positive gamma intact across complex with VIX at 18.46; contango carries, but skew steepening near-term

Index complex remains in Positive Gamma with spot above flip and VIX term in Contango - the textbook vol-seller's tape. But near-dated put skew at 2.44% and persistent Iran-war headlines mean the left tail keeps getting bid even as VVIX sits at 92.29. Bias remains mean-reversion inside the call wall / put wall channel; chase nothing until 730.00 breaks.

Regime Assessment

Regime stamp: Elevated / Watchful with VIX anchored at 18.46. The transition matrix puts panic-regime migration over the next week at 0.05 and reversion to a low-vol state over two weeks at 0.45 - asymmetric toward calm, but not yet inviting size-up. Half-life of 15 sessions says this state is moderately sticky; expect it to persist, not pivot.

The structural backdrop reinforces the read - cross-asset complex is Aligned in Positive Gamma, VIX term in Contango, VVIX at 92.29 showing no bimodal pricing. Carry trades remain paid, but the Iran-headline cycle is the override vector. A clean catalyst - sanctions escalation, MOVE breakout past 79.87 - collapses the half-life fast.

Trade the regime, respect the override: Iron Condor in 30-45 DTE, standard sizing per Standard Size, tail hedge stays on.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - sticky enough to sell premium against, asymmetric toward 0.45 reversion over 0.45 probability. Iran-headline shock is the only realistic accelerant past the 0.05 panic threshold.

Trading readVIX, VVIX, MOVE all aligned in low-stress range; SKEW at 145.77 is the elevated one - tail pricing is the leading indicator if the rest catches up.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

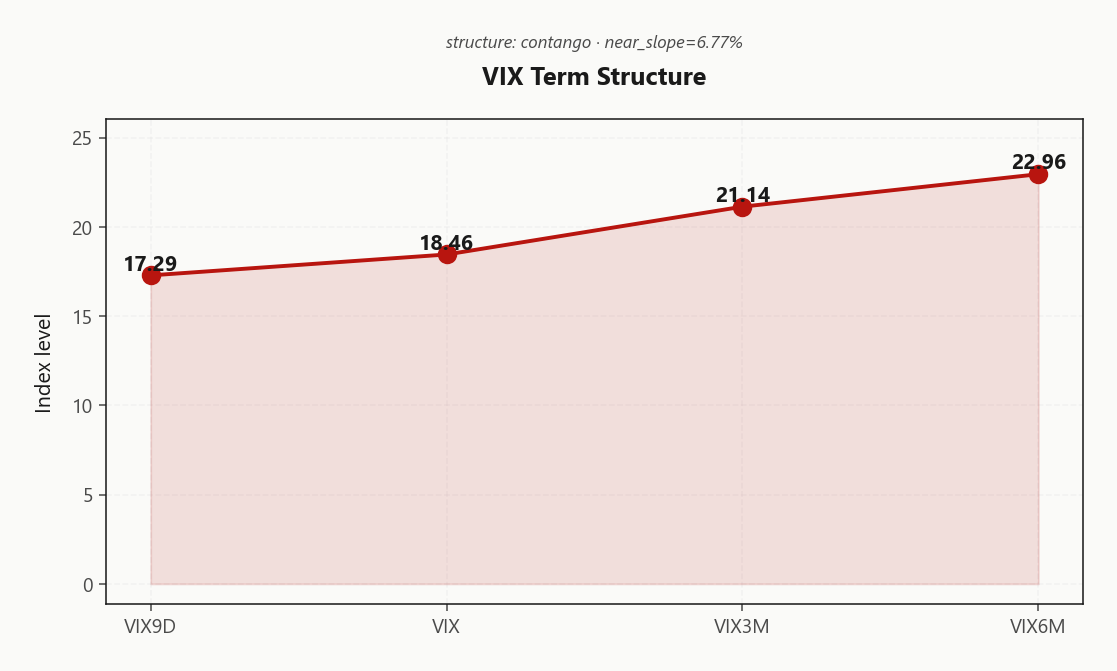

Term structure prints clean Contango with VIX9D at 17.29 below spot VIX 18.46, both anchored below VIX3M 21.14 and VIX6M 22.96 - the textbook carry curve. Front-end discount is mild but the back-half stretch is what matters: forward 30-60 implied at 22.3598658314 sits above spot VIX, telling you the Iran-war event premium is being priced further out, not into tomorrow's tape.

Regime tag: Steep Contango - sellers paid, and paid cleanly. The DTE-5 surface bump at 16.45 is the single-expiry event kink to route around; everything past it sits in carry territory. Calendar structures dominate: short the front-month where realized refuses to deliver, own the back-month where the tail premium actually lives.

Trade expression: sell front, hedge back. Don't fight the curve - it's paying you to hold it.

What it means for your trading

Term structure in Steep Contango with forward 30-60 at 22.3598658314 above spot VIX 18.46 - event risk is back-loaded, making front-month sales hedged with longer-dated length the highest-edge expression.

Trading readSteep Contango with 6.77%% slope means the market is paying for back-dated risk, not front-dated - sell front, hedge back. Classic event-risk-priced-further-out curve.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 16.08% sits comfortably north of HV20 11.01, leaving a 5.07% VRP that pays sellers cleanly for risk the tape isn't actually delivering. Short-window realized has compressed beneath HV60 15.03 - the deceleration is the tell: chop, not trend, and options are still being marked for a move the underlying refuses to print.

With implied riding above every realized bucket, the cheap-to-rich rotation only triggers on a genuine VIX break higher; absent that, premium-selling is the path of least resistance and iron-condor carry compounds. Long-vol needs a delivered move, not a headline - until HV starts catching up to IV, the seller stays paid.

What it means for your trading

Implied at 16.08% against decelerating realized (HV20 11.01 < HV60 15.03) keeps the 5.07% VRP firmly in seller-favored territory. Flip the bias only if VIX breaks higher and realized starts catching up - not before.

Skew Convexity

The quarter-delta skew prints at 2.44% with a smile ratio of 1.15% - unambiguously above parity, the left tail is being bid while the right side fades. Put 18.8% against call 16.36% with ATM anchored at 17.66% spells out the asymmetry: downside convexity is the line getting paid, upside is being monetized into the long-gamma cap.

IWM corroborates and then some - 4.59% sits steepest in the complex, the canonical tell that small-caps wear the tail-vulnerability premium when geopolitical headlines are the dominant vector. Section signal reads Skew Steep, consistent with cross-asset alignment at Aligned rather than active stress.

Trade implication: put spreads, not naked puts. Convexity is no longer cheap and selling the wing against the body recoups the steepening you'd otherwise pay through in outrights. Skip the lottery-ticket downside; the market has already repriced it.

What it means for your trading

Quarter-delta skew at 2.44% and smile ratio 1.15% confirm the left tail is bid - finance long downside via put spreads, not outright puts, since IWM at 4.59% flags the small-cap wing as the most expensive convexity in the complex.

Vol-of-Vol Structure

VVIX prints 92.29 against VIX 18.46, pinning the ratio at 5.00 - squarely in Normal territory. The tape is not pricing a bimodal outcome; jump premium is absent, and the convexity-of-convexity bid that usually precedes a regime break has yet to assert itself. Vol-of-vol is behaving, even as front-end skew steepens and Iran-war headlines refuse to leave the wire.

Sizing guidance flips to Standard Size - no half-size discount required, no defensive trim into the carry trade. The Green read on this axis is the cleanest green light in the dashboard, and it directly unlocks the iron condor in 30-45 DTE at full risk budget rather than the headline-discounted clip.

The watch item: a VVIX breakout would front-run any VIX move and is the earliest tell that the Iran headline cycle has shifted from geopolitical noise to cross-asset contagion. Until the ratio leaves Normal, stay short premium and let the curve work.

What it means for your trading

Vol-of-vol sits in Normal regime with VVIX/VIX at 5.00 - no jump premium priced, sizing runs Standard Size. Monitor VVIX as the leading tell for headline-driven regime breaks.

Dispersion Spread

Index vol sits stubbornly cheap to its components: SPY ATM IV prints 16.08% against QQQ at 22.76% and IWM at 21.15%. That gap is the tell - single-name and sector vol is absorbing the headline tape while the index surface stays pinned, a textbook Moderate dispersion read with correlations soft enough that index hedges leak premium against any names-led drawdown.

IWM at 21.15% reinforces the small-cap risk premium - the high-beta tail is doing the work the SPX surface refuses to price. Implication: sell index vol, not single-name vol. SPY/SPX premium-selling structures carry better here because the dispersion math punishes index buyers and rewards index sellers; chasing rich name-level IV is the wrong side of the same trade.

Bias stays with the index premium-seller, sized standard per the Normal VVIX read. Single-name longs hedge with name puts, not SPX; index books harvest the compression until correlation re-couples.

What it means for your trading

Dispersion is doing what dispersion does - index vol at 16.08% stays suppressed while QQQ 22.76% and IWM 21.15% carry the risk premium. Lean index-short-vol, name-level-hedged.

Liquidity & Microstructure

The book anchors at 729, where highest OI converges with the put wall and stacks the largest dealer footprint in the complex - top strike carries -$3.76B of net GEX, the mean-reversion magnet for any intraday drift. With spot riding above 730.00, dealer hedging mechanically buys weakness and fades strength; the regime reads Deep and the channel is well-defined.

Upside is capped into 737.00 where the call wall absorbs gamma supply, while 729.00 defines the cushion on the downside. The flip line at 730.00 is the binary - above it dealers dampen, below it they amplify. Cross-asset reads Aligned, so no internal break to chase.

Trade the channel: fade pushes into 737.00, accumulate dips into 730.00, and treat the 729 cluster as the gravitational center until OI migrates.

What it means for your trading

Dealer book is deep and well-anchored between 729.00 and 737.00 with the flip at 730.00 - mean-reversion has structural backing until spot pierces flip.

Trading readDealers parked long-gamma between 729.00 and 737.00 - within that channel, every push gets faded; outside it, dealers turn into trend-amplifiers. Trade the chop, not the breakout.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The flow-pivot line lands at 737 - a Call Wall anchor where dealer hedging direction inverts. Current bias reads Neutral with signal Yellow, meaning the cushion is real but conditional. Hold the line and the long-gamma mean-reversion tape persists; lose it and vanna takes over.

Trade implication: positive gamma keeps intraday chop contained, but the negative-vanna overhang means tail hedges remain priced correctly - don't strip them for carry alone.

What it means for your trading

Vanna at -$185.57B is the hidden short-vol exposure beneath a long-gamma surface; the charm pivot at 737 is the level that gates whether dealer flow stays supportive or flips destabilizing.

Cross-Asset Confirmation

Bond vol is the tell. MOVE at 79.87 sits well inside stress thresholds even as the global bond-rout narrative dominates the tape - credit channels are not transmitting the Iran headline into rates volatility. That distinction matters: this is a geopolitical premium, not a credit-cycle premium, and the two compound very differently into equity vol.

Inside the equity complex, QQQ at 700.34 and IWM at 275.14 hold the same Positive Gamma stance as SPY - cross-asset tone reads Unknown with regime divergence Aligned. No internal fracture between large-cap, tech, or small-cap dealer books; small-caps would lead any regime break and they are not leading.

Fear & Greed prints Greed at 62 - positioning still leans long, with room to deteriorate before any contrarian fear bid surfaces. Mean-reversion bias stays intact; the headline-driven tail compresses on resolution rather than compounding through credit. Watch IWM and MOVE for the first crack.

What it means for your trading

Cross-asset signals confirm a geopolitical, not credit-driven, vol bid - MOVE contained at 79.87, indices aligned in AlignedPositive Gamma, and Fear & Greed at 62 still tilts long. Mean-reversion remains the working bias until IWM or MOVE breaks rank.

Scenario EV

Highest-EV structure prints Iron Condor with a composite score of 53, edging the next-best put spread alternative at 45. The sweet spot lands in the 30-45 DTE window - far enough out to clear tomorrow's front-end event premium spike, near enough to harvest before the back-half vol pickup priced into VIX3M at 21.14.

VRP read comes through Unknown, but the underlying carry math still favors the seller: ATM IV at 16.08% sits comfortably rich to HV20 at 11.01, and the steep contango curve does the term-structure work for you. Sizing runs Standard Size per the VVIX/VIX ratio at 5.00 - no bimodal premium to half-size around.

Pin the short call leg below 737.00, the short put above 730.00. The dealer-long-gamma channel does the heavy lifting; collect theta inside the walls, let microstructure pin the tape.

Bottom line: the highest-EV trade remains a Iron Condor in 30-45 DTE - past the front-end event premium, ahead of the back-half vol pickup, and squarely inside the dealer-supported channel. Fade strength into the 737.00 call wall, buy dips into the 730.00 flip; with spot above flip and regime tagged Positive Gamma, dealer hedging mechanically dampens both directions.

Avoid naked short puts - skew at 2.44% is bid and the left tail is no longer cheap; spread the downside instead. Avoid chasing breakouts - positive gamma caps rips into the call wall, and VVIX at 92.29 says no jump premium is being paid yet. Sizing stays standard per Standard Size.

Watch 737 - that is where dealer flow flips and the mean-reversion thesis breaks. Regime currently reads Elevated / Watchful; Iran headlines are the override risk.

What it means for your trading

Sell premium inside the wall-to-wall channel via Iron Condor in 30-45 DTE, fade into 737.00 and buy dips into 730.00; flow flips at 737.

Iran-war peace proposal headline is the single biggest tail-risk decay catalyst - any concrete progress collapses front-end IV and steep skew overnight.

Global bond rout deepening on Iran-war inflation risk is the cross-asset confirmation thread - if MOVE breaks higher, equity vol regime flips fast.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.61 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 730.00 against a spot of 734.78. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.08% with a volatility risk premium of 5.07%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.46. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime