Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

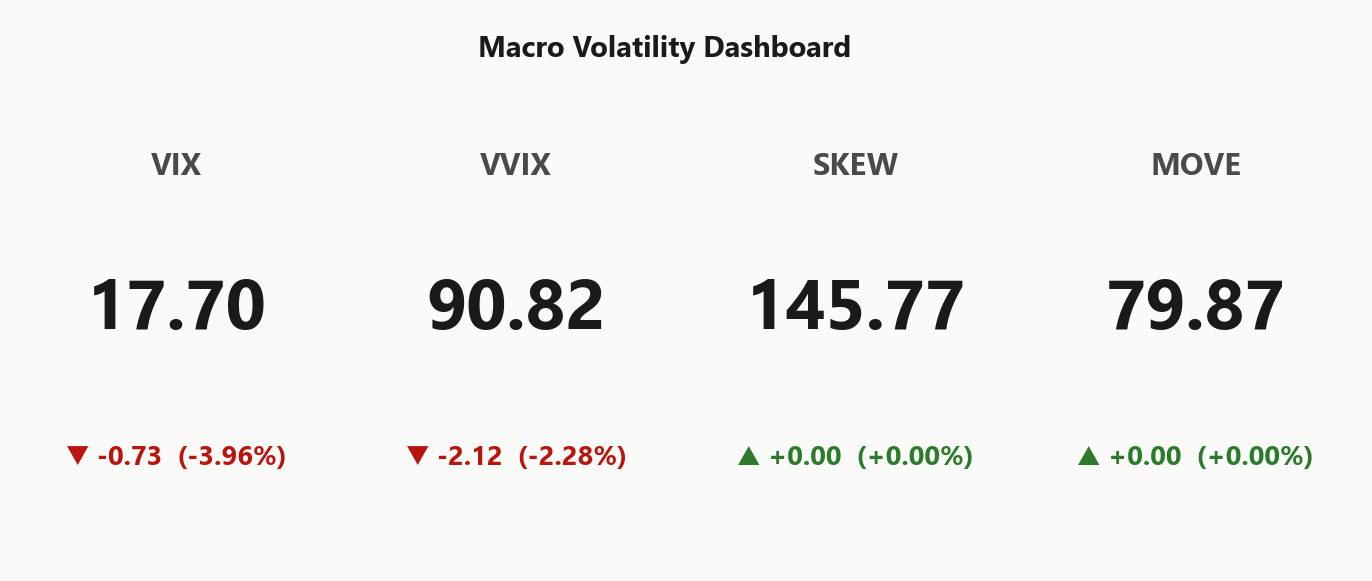

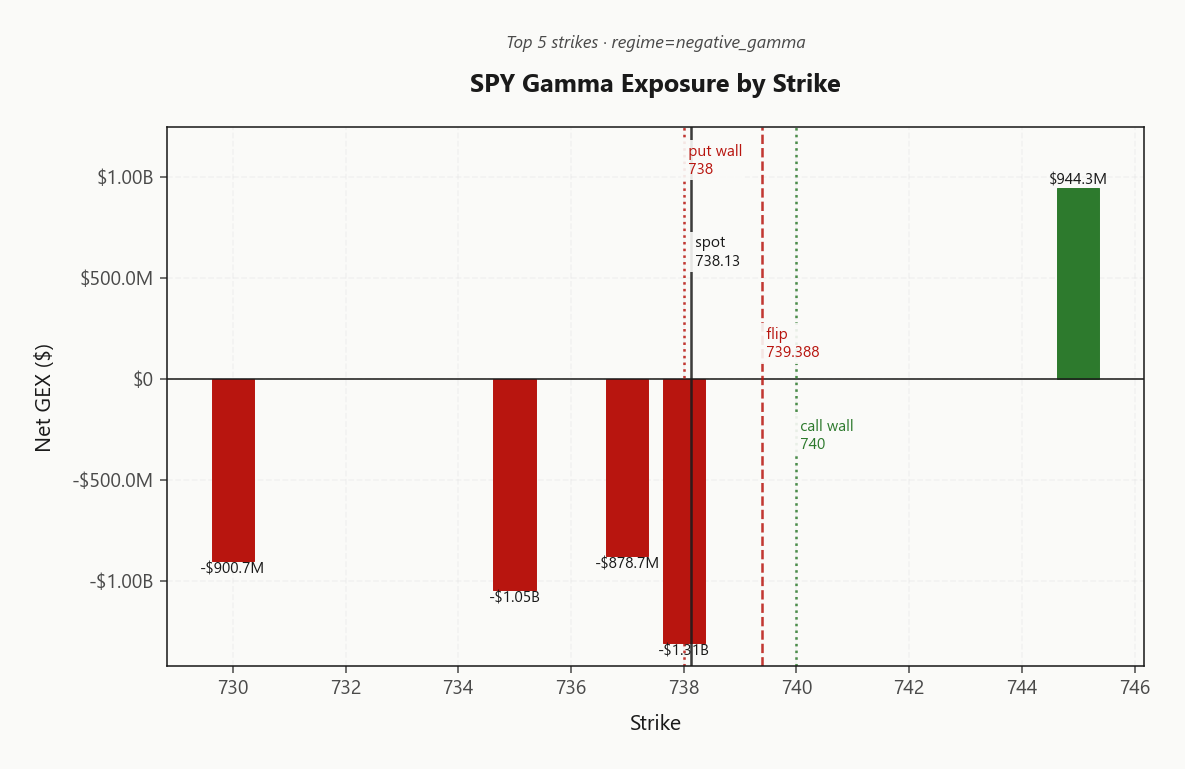

SPY closed at 738.13 sitting precisely on the 738.00 put wall with dealers in Negative Gamma - net GEX at -$4.53B and gamma flip just overhead at 739.39. Call wall caps at 740.00, with the largest OI cluster down at 700 - a wide trading corridor with the immediate battle inside a tight band. Dealers run net VEX of -$211.29B (vol-up = more selling pressure) and charm modestly positive at $76.2M into Tuesday's expiries. VIX at 17.70 with term structure Contango (7.14%% near slope) keeps the carry trade open; VVIX at 90.82 signals Normal jump risk - standard sizing. VRP for SPY runs 3.74% vol points over HV20 of 10.67, so options are clearly rich to recent realized. QQQ holds Positive Gamma above 599.78 - the divergence (Qqq Heavier) is today's lead. Bottom line: scenario EV ranks Iron Condor in the 30-45 window - sell vol around the 738.00/740.00 corridor but keep wings tight because a break of 738.00 unlocks dealer selling into negative gamma.

SPY pinned at put wall in negative gamma while QQQ holds positive - cross-index divergence is today's lead.

SPY closed pinned at 738.00 with dealers in negative gamma while QQQ remains comfortably above its flip in Positive Gamma - a classic cross-index divergence that Qqq Heavier. VIX term structure stays in Contango with VVIX benign at 90.82, so vol sellers retain carry, but SPY's gamma instability means short-strangle sizing should respect the put wall break. Iron condor scored top in scenario EV at the 30-45 DTE window.

Regime Assessment

The tape sits in an Elevated / Watchful regime with VIX anchored at 17.70 - comfortable but not complacent, which is exactly the band where carry pays without inviting a fade.

Transition math favors persistence: the model assigns only 0.05 probability of a panic break over five sessions versus a meaningful 0.45 chance of fading lower across ten. The asymmetry is clear - the regime is far more likely to bleed quiet than to crack loud.

Half-life clocks at 15 sessions, so this watchful posture is sticky, not transient. Don't fade it - trade with it: harvest the premium that an elevated-but-orderly vol surface offers, but respect the left tail with defined-risk structures rather than naked short gamma. The carry is the edge; the wings are the discipline.

What it means for your trading

With panic odds at 0.05 versus fade odds at 0.45 and a 15-session half-life, the Elevated / Watchful regime rewards traders who sell vol with defined wings rather than chase a regime change.

Trading readVIX easing, VVIX easing, MOVE quiet, SKEW elevated but stable - every macro vol gauge is confirming a suppressive regime. No divergence to flag = lean into the carry trade, but keep an eye on SKEW as the canary if put demand expands.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

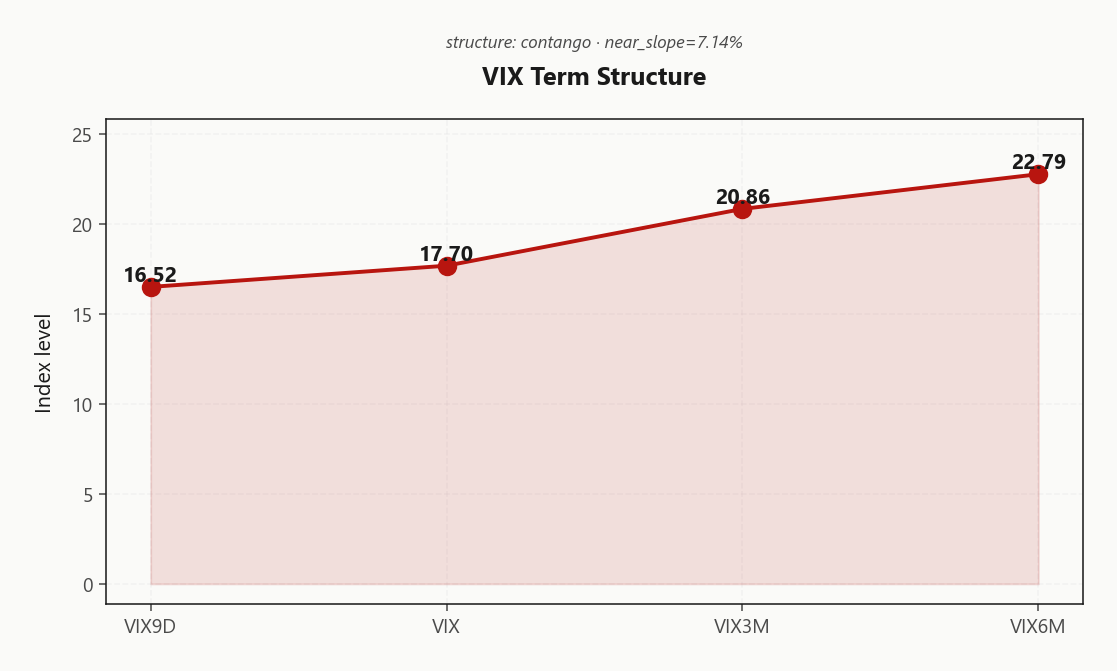

The VIX complex stacks in fully ordered Contango from 16.52 on the front through 17.70, 20.86 and out to 22.79 at the long end. Near slope prints 7.14%% - the carry trade is wide open and structurally healthy for vol sellers.

Forward vol from the thirty- to sixty-day node sits at 22.2725032271, with the sixty-to-ninety extension at 24.5688542671 - rolldown, not spot vol direction, is the dominant edge. There is no backwardation kink anywhere in the curve, which means the tape is not paying for a specific catalyst; nothing is priced as binary.

Regime reads Steep contango - vol sellers favored. The sweet spot is the 30-45 DTE bucket where curve decay is steepest and you sit far enough from the gamma noise at the front. Until a flattening print appears in the near slope, lean into the carry.

What it means for your trading

Ordered Contango across the full VIX stack with a healthy 7.14%% near slope and no event kink - rolldown is the trade. Target the 30-45 window where the curve pays you most to wait.

Trading readSteep, ordered contango all the way out - the vol-sellers' carry trade is fully intact. A flattening or backwardation print would be the first warning; until then, rolldown harvesting in 30-45 DTE remains the dominant edge.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 14.41% trades comfortably above HV20 of 10.67 - options are unambiguously rich to what the tape has actually delivered. HV60 at 14.96 sitting above HV20 confirms realized is decelerating, not accelerating, which reinforces the mean-reversion path for implied lower. The VRP reads 3.74% vol points - a paid-to-sell condition at the index level, not a marginal one.

Cross-index, the dispersion picture sharpens the trade. QQQ VRP runs wider at 4.53%, with single-name tech vol paying meaningfully more than the SPY complex - the cleanest carry seat in the book. IWM VRP is the thinnest cushion at 2.18%, so short-vol structures there carry the least margin of safety against a realized re-acceleration in small caps.

Bottom line: lean into premium selling where VRP is fattest - QQQ overlays preferred, SPY in the middle, IWM only with tight wings.

What it means for your trading

Index IV is clearly rich to recent realized with HV decelerating - the suppressive VRP regime supports premium selling, with QQQ offering the widest cushion and IWM the thinnest.

Skew Convexity

The smile is leaning left in an ordered way, not a panicked one. SPY's quarter-delta put IV prints 16.29% against an ATM of 15.14%, with the skew measure at 2.07% and smile ratio 1.15% - puts are bid persistently, but the curve isn't kinked the way a true crash bid would force it. Translation: left tail is being accumulated as insurance, not chased as a trade.

The upside is the more telling tell. Call-side quarter-delta IV at 14.22% sits below ATM - zero upside convexity demand, nobody paying for melt-up optionality. That asymmetry is the position: hedged-but-not-hopeful. IWM's skew steepens further to 2.23%, confirming the small-cap tail is where the genuine nervousness lives, consistent with IWM sitting in negative gamma with the thinnest cushion.

Tactically, this shape favors put spreads over naked puts - the steepness means short legs subsidize long legs meaningfully - while covered-call writing harvests minimal premium given the flat upside curve. Wing-cheapening is real enough to make iron condor superior to short strangle in the recommended DTE window.

What it means for your trading

Put skew is steep but ordered, call skew flat - defensive positioning in place without panic, with IWM at 2.23% the tail to watch. Express downside through put spreads, not naked puts, and let the cheap wings carry the iron condor structure.

Vol-of-Vol Structure

VVIX prints 90.82 against VIX at 17.70, planting the ratio at 5.13 - squarely in the Normal band. No convexity bid, no jump premium being paid, no bimodal crush-or-spike pricing embedded in the surface. The tape is not bracing for a regime break; it's bracing for nothing in particular.

Vol-of-vol is easing into the close at -2.28% on the session - fear-of-fear bleeding out alongside spot VIX. With no convex hedging demand stacking up behind the front of the curve, short-vol structures clear the sizing test: guidance reads Standard Size, meaning full book risk is on the table rather than the half-size cap a stressed VVIX print would impose.

Translation for the desk: lean into the carry. Iron condors and put-spread overlays size to standard risk units, and the absence of a convexity premium means wing pricing is honest - what you pay is what the surface thinks the tail is worth, not a panic markup.

What it means for your trading

Vol-of-vol sits at Normal with the VVIX/VIX ratio at 5.13 and VVIX easing -2.28% - green light for Standard Size on short-vol structures, no jump-premium tax to pay.

Dispersion Spread

The dispersion print is the cleanest setup on the screen today: 21.76% ATM in QQQ against 14.41% in SPY is a roughly half-again volatility premium at the index level, and the VRP gap confirms it - 4.53% in QQQ versus 3.74% in SPY. Tech single-name vol is doing the heavy lifting; index correlation is moderate, so the index tape is being dampened by the constituents rather than the other way around.

Operationally that flips the hedging calculus. Single-name puts in the QQQ complex are rich relative to what the index will actually realize, so SPY/SPX overlay is the efficient protection here, not constituent protection. IWM at 20.23% is the other side of the trade - small-cap ATM isn't paying a premium for the realized it's printing, the thinnest cushion to be short vol and the place dispersion offers the least margin.

What it means for your trading

Sell dispersion through the index: short QQQ vol where the constituent premium is richest, hedge with SPY overlay rather than single-name puts, and steer clear of IWM as a short-vol vehicle where the cushion is thinnest.

Liquidity & Microstructure

The structural anchor sits well below spot at 700, the 715.00 max-pain zone - a deep OI shelf that frames the broader corridor but isn't where today's battle is being fought. The active gamma fight has compressed right at the put wall, with the top GEX strike at 738.00 carrying net GEX of -$1.31B - dealers stacked short gamma exactly where price closed.

The gamma flip sits just overhead at 739.39, effectively kissing the 740.00 call wall - a tight battleground against the 738.00 put wall below. Reclaim the flip and stabilizing dealer flow re-engages; lose the put wall and dealer selling amplifies any downside extension into the OI void back toward 700.

The flip is the single hinge for the next session - asymmetric dealer impact on either side of it.

What it means for your trading

Microstructure is binary around 739.39: above it dealers stabilize, below the 738.00 put wall they accelerate downside toward the 700 OI shelf. Trade the corridor, but treat the put wall as the non-negotiable stop.

Trading readHeavy negative gamma cluster sits right where SPY closed - the put wall is the magnet AND the trapdoor. Above the gamma flip dealers stabilize; below it they amplify, so the next directional move is asymmetric in dealer impact.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints deeply negative at -$211.29B - vanna is an accelerant, not a stabilizer. Any re-expansion in IV from here forces dealers to lengthen their short delta exactly as spot weakens, and the feedback loop sits coiled under the tape rather than dormant. Charm offers the only counterweight: $76.2M of net CHEX delivers a modest positive carry into the bell, the small hand of time decay holding the pin together while vol stays quiet.

The book's hinge is the put wall itself at 738 - pivot type reads Put Wall with current bias Neutral, spot sitting precisely on the line. A break of 738.00 tips dealer flow to the sellers and vanna goes to work on the downside; a reclaim of 739.39 re-enables the stabilizing regime overhead. Asymmetric outcomes, single decision level.

What it means for your trading

Vanna is loaded as a downside accelerant at -$211.29B while charm carries a thin positive bid at $76.2M - the put wall at 738 is the binary pivot, with break-below handing flow to sellers and reclaim-above restoring dealer stabilization.

Cross-Asset Confirmation

Cross-asset gauges refuse to confirm equity fragility. MOVE sits at 79.87 - bond vol is quiet, with zero stress signal bleeding from rates into the equity tape. Fear & Greed reads Greed at 62, sentiment leaning constructive rather than defensive. No credit, no rates, no sentiment confirmation of the pin story.

The split is internal to equities. SPY at 738.13 sits in negative gamma against QQQ at 705.33 holding its cushion above flip - divergence direction reads Qqq Heavier, with tech carrying the positive-gamma weight while the broad tape pins. IWM at 276.03 mirrors SPY's posture but with thinner cushion.

Read: this is an SPY-specific microstructure pin, not a macro shock. Mega-cap positioning is doing the cushioning work in QQQ; without a MOVE-side or sentiment confirmation, fade systemic-risk framing and trade the corridor on its own merits.

What it means for your trading

With MOVE at 79.87 and Fear & Greed at 62 (Greed), no cross-asset gauge confirms equity fragility - the SPY/QQQ regime split (Qqq Heavier) is mechanical positioning, not a macro signal.

Scenario EV

Scenario EV ranks Iron Condor top of the book at a score of 44, with the put spread alternative trailing at 34 as the defensive plan B. The setup is mechanical: VRP is active, term structure holds Contango, and vol-of-vol prints Normal - three confirmations stacked, so the carry trade is the trade.

Sweet spot is the 30-45 DTE bucket - far enough from 0DTE gamma noise to dodge the pin volatility, close enough to harvest the steepest part of the rolldown curve. VVIX in its normal band means Standard Size applies: no half-size cap, full book risk is on the table. Condor wins over strangle because skew at 2.07% cheapens the wings meaningfully - you collect protection at a discount.

Center the structure inside the 738.00/740.00 corridor and exit short-vol on a clean break of the put wall.

What it means for your trading

Iron condor at score 44 in the 30-45 window is the cleanest expression of active VRP plus Contango carry; standard sizing per Normal VVIX, with the put spread at 34 as the defensive fallback.

Actionable Summary

Trade:Iron Condor in the 30-45 DTE window, wings sized to the SPY corridor between the 738.00 put wall and 740.00 call wall. Carry is paid by Contango term structure and an active VRP of 3.74% against HV20 at 10.67.

Watch: the charm pivot at 738 - a break of the put wall flips dealer flow into an accelerant given net VEX at -$211.29B, and is the cue to exit short-vol structures. Avoid naked SPY puts below the 739.39 flip where negative gamma amplifies, and avoid call chasing above 740.00.

Hedge with SPY/SPX overlay rather than single-name puts - QQQ VRP at 4.53% prints richer than index, so dispersion favors index protection. Regime reads Elevated / Watchful: sticky for roughly 15 sessions, trade with the carry but respect the tail.

What it means for your trading

Sell the corridor in 30-45 DTE iron condors anchored to 738.00/740.00, with the 738 pivot as the kill switch. The Elevated / Watchful regime favors carry harvesting but punishes naked downside below the flip.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.81 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 739.39 against a spot of 738.13. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.41% with a volatility risk premium of 3.74%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.70. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime