Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

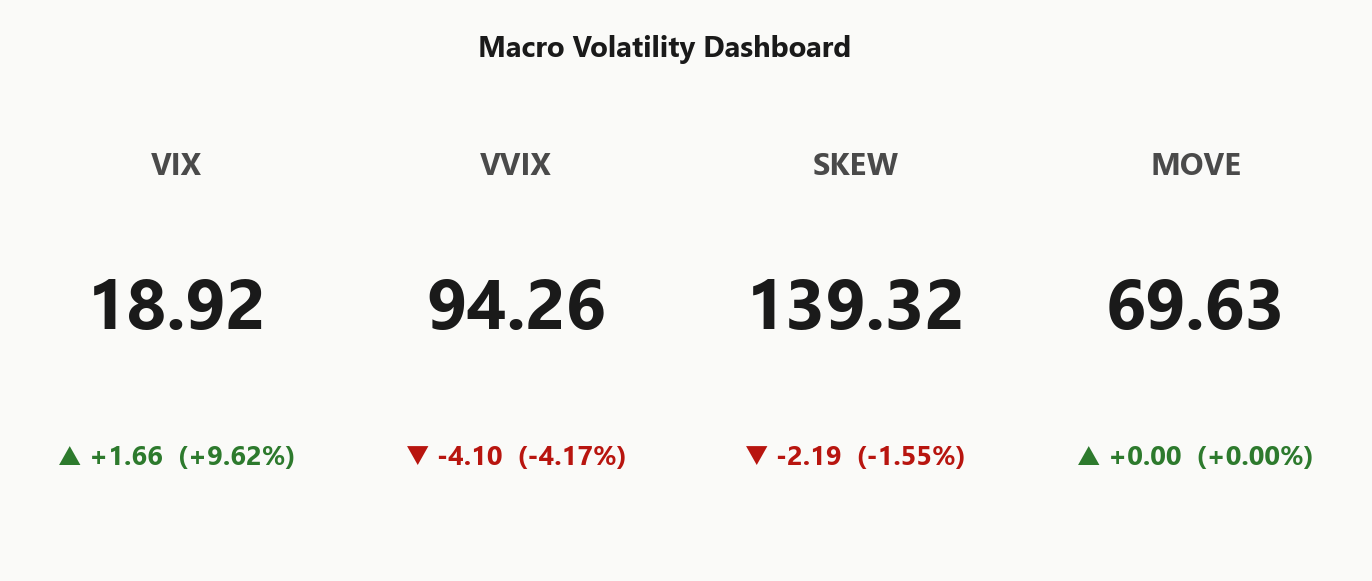

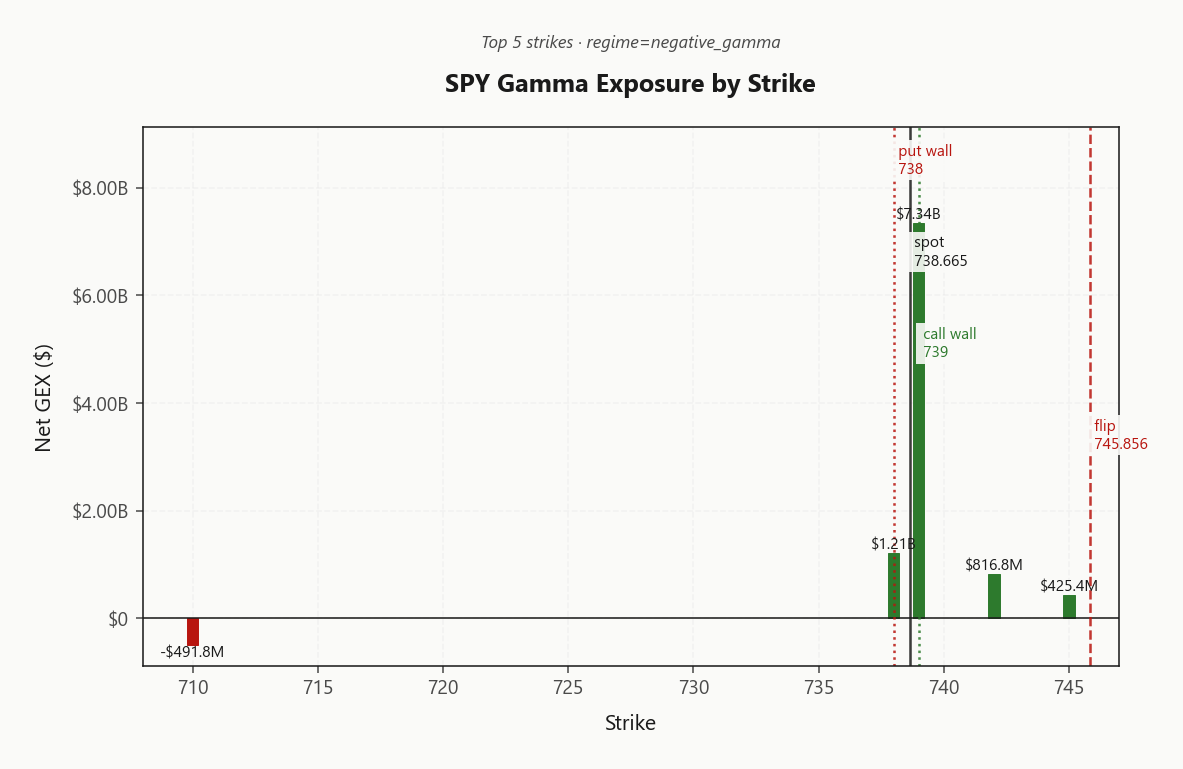

SPY at 738.67 sits in Negative Gamma with net GEX at $8.69B - dealers short gamma, moves amplified. Key levels: call wall 739.00, put wall 738.00, and the critical gamma flip at 745.86 which sits above spot (0.0453520879% away) - spot needs to reclaim that to flip dealer flow stabilizing. Vanna is hostile at -$61.14B: any further VIX uptick forces dealers to sell delta into weakness, and charm at -$34.5M keeps pressure on into close. Vol read: VIX up 9.62% to 18.92 but term still Contango with VIX3M at 20.85 - VRP at 5.35% stays rich, but VVIX at 94.26 signals normal jump-risk pricing. Cross-asset stress is real: Treasury yields blowing out, oil bid on Iran headlines, SPX off -1.27%. Bottom line - sell premium with defined-risk Iron Condor structures in the 30-45 DTE window, fade strength into the call wall but cut size if 738.00 breaks because short-gamma below flip means downside accelerates.

Negative gamma across complex with VIX bid 9.62% on Iran/oil shock - amplification risk live

SPY trades into negative gamma at 738.67 with the gamma flip overhead at 745.86 - dealer hedging amplifies moves until spot reclaims that level. VIX popped 9.62% on oil and Treasury-yield stress while term structure stays in Contango, so the carry trade lives but tails are getting bid. Lean iron condor structures inside the call wall / put wall band; treat any break of 738.00 as a trend-day trigger.

Regime Assessment

Regime reads Elevated / Watchful with the model parked in Elevated at a VIX print of 18.92 - squarely in the bid-but-not-panic band where dealer hedging amplifies but cross-asset contagion has not engaged. Transition math says a panic escalation over the next five sessions runs at 0.05, while the snap back to a low-vol state inside ten sessions sits at 0.45 - asymmetry favors fade, not chase.

Half-life clocks 15 sessions, so this print decays on its own absent a fresh catalyst: the elevated state is watchful, not sticky. Pair that with cross-asset tone reading Aligned across the complex and term structure holding Contango, and the playbook stays premium-seller with defined risk - keep size standard, let mean reversion do the work, and reassess only if MOVE confirms or charm pivot at 739 fails to hold the line.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - panic odds at 0.05 versus normalization at 0.45 tilt the edge toward fading vol, not chasing it.

Trading readVIX up, VVIX down, SKEW down, MOVE flat - divergence says equity vol is bid in isolation, not yet a contagious cross-asset stress event. Watch MOVE for the regime-shift confirm.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

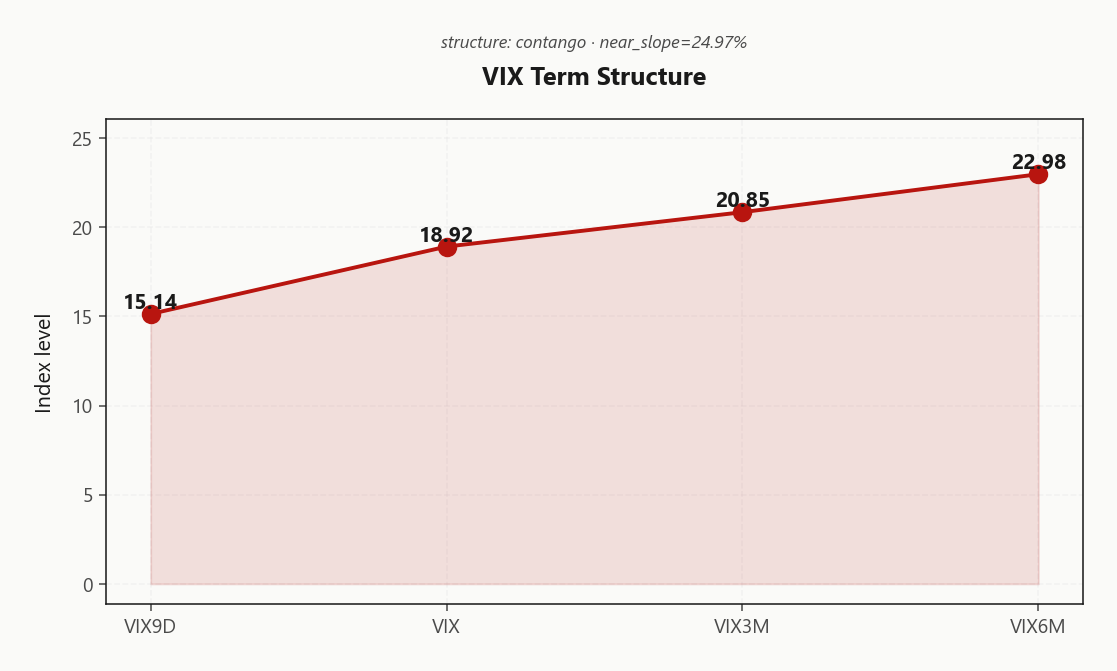

Term structure is unambiguous: VIX9D at 15.14 trades under spot VIX at 18.92, with VIX3M 20.85 and VIX6M 22.98 anchoring the back end well above. The shape is Contango with a near slope of 24.97% - front-week event premium is being paid, but the structural vol-selling carry beyond the event window is fully intact.

Forward 30→60 implies 21.7508746951, with 60→90 extending to 24.9286642241. That's the cleanest edge on the board: the belly is pricing what the front is panicking about, and the curve hasn't broken. Regime reads Steep Contango - sellers favored beyond 30 DTE, hedgers buying the belly rather than chasing the wings.

Practical translation: lift premium in the 30-45 band where forward implieds reset cheaper than spot VIX suggests. Hedge demand belongs in the belly, not the front-month tail where event risk is already priced.

What it means for your trading

Term structure stays in Contango with a Steep Contango regime - front-week event premium is real but the back end is signaling carry intact, so vol sellers retain the edge in the 30-45 window.

Trading readContango with front pop - the vol carry trade is still alive in the belly and back end, but the curve is warning event premium has entered the front week.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 16.17% trades meaningfully above 20-day realized at 10.82, leaving VRP at 5.35% - the index premium is still paying you to be short vol despite the session's pop. Crucially, HV20 sits under HV60 at 15.03, so realized has been decelerating into this tape, not accelerating. The vol pop is an implied-side event, not a realized-side regime change.

That asymmetry is the trade: implied above both HV20 and HV60 means premium harvest is live across the curve, and sellers retain the structural edge so long as the tape doesn't crack 738.00. The signal to abandon the carry is HV expansion through HV60 - that's the regime-change tell, not the VIX print itself.

Tactically: lean into Iron Condor in the 30-45 DTE band where the VRP cushion is fattest, but size honestly given dealers sit in Negative Gamma below the flip at 745.86. Premium is rich; the path to collecting it is not.

What it means for your trading

Implied at 16.17% richens to a decelerating realized tape (HV20 10.82 under HV60 15.03), keeping VRP at 5.35% harvestable. Flip the bias only if HV breaks above HV60 or spot loses 738.00.

Skew Convexity

Quarter-delta puts trade at 14.68% against ATM at 13.15% and the symmetric call wing marked at 11.89% - a put-over-call skew of 2.79% with smile ratio 1.24%. Left tail is unambiguously bid; the right wing trades at a discount to the at-the-money strike, which is the market's way of saying nobody is paying for an upside chase here.

Smile ratio north of parity confirms put dominance - this isn't a generic vol bid, it's a directional convexity bid for downside. With the call wing offered, structures that monetize both sides of the distribution capture the asymmetry the tape is paying for. Naked downside is expensive; the put-spread expression strips the over-bid wing against the cheaper ATM body and pays for itself with the steepness of the skew curve.

Trade implication: hedgers should fund downside via vertical put spreads rather than buying outright tails, and premium sellers should harvest the elevated put wing without leaving the call wing naked - Iron Condor captures both wings cleanly given the asymmetric pricing.

What it means for your trading

Skew at 2.79% with smile ratio 1.24% signals the tail is already richly priced - fund hedges with put spreads, not naked puts, and prefer Iron Condor over single-sided downside structures.

Vol-of-Vol Structure

VVIX at 94.26 against VIX 18.92 prints a ratio of 4.98 - squarely in Normal territory. The tell: VVIX faded-4.17% while spot VIX rallied 9.62%. That's orderly repricing, not a bimodal distribution being marked up. The market is paying for vol, not for the optionality on vol - convexity buyers stayed home.

Practically, no jump-risk premium spike means the tail of the tail is not being bid. Short-vol structures don't carry the gap-risk surcharge they would in a true panic regime, and the second-derivative carry stays intact even as front-end VIX shifts higher on the Iran/oil tape.

Sizing: Standard Size on premium-selling structures - greenlight for defined-risk condors and put spreads in the 30-45 DTE band. The vol-of-vol gate is open; concentrate the risk budget on direction and skew, not on convexity hedges you don't need to pay for today.

What it means for your trading

Vol-of-vol at Normal with VVIX fading -4.17% into the VIX pop confirms orderly repricing, not panic - keep premium-selling sizing at Standard Size.

Dispersion Spread

Index premium is conspicuously cheap to the single-stock complex: SPY ATM IV prints 16.17% against QQQ at 24.72% and IWM at 23.1%. The Iran/oil shock is leaking into names with idiosyncratic energy and supply-chain leverage, not into the index basket itself - correlation isn't tightening enough to drag SPY vol up to where its components are pricing.

That gap is the trade. Sell index vol, hedge selectively in single names. Dispersion is biased long correlation here - if the macro shock generalizes, SPY catches up to QQQ/IWM and index sellers get hurt while component owners are already paid. Until then, SPX/SPY condors capture richer relative carry than single-name structures whose premium already reflects the geopolitical tail.

Cross-asset regime is Aligned short-gamma, so the dispersion isn't a vol-regime divergence - it's a concentration story. Trade it as such: index short, single-name long on a basket basis, not name-by-name conviction.

What it means for your trading

SPY ATM IV at 16.17% trades well under QQQ 24.72% and IWM 23.1% - sell index premium, hedge with single-name longs to express the long-correlation dispersion view.

Liquidity & Microstructure

The book pins around the 739.00 mega-cluster carrying $7.34B of net GEX - that strike is the magnet and it sits flush against the 739.00 call wall, the exact level where dealer flow flips from chase to fade. Spot is trapped below the gamma flip at 745.86, which keeps the whole structure in amplification mode: sells get sold, rallies get faded into the wall.

Downside structure leans on the 738.00 put wall as the first dealer pivot - a clean break there flips hedging from absorbing to chasing, and the next gravity well is the far-OTM 505 OI legacy print, which carries no gamma weight today and won't catch the tape. Until spot reclaims 745.86, fade strength into the wall, defined-risk, and treat the put wall as the exit, not a bounce.

What it means for your trading

Liquidity is deep but hostile: the 739.00 magnet caps upside while spot below 745.86 keeps dealers amplifying; lose 738.00 and the tape runs unopposed.

Trading readNegative-gamma regime with the magnet just overhead at the call wall - dealers amplify moves until spot reclaims the flip; below flip, every push lower gets sold harder.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna and charm are aligned hostile. Net VEX prints -$61.14B - every further tick higher in VIX mechanically forces dealers to sell delta into weakness, the textbook accelerant that turns an orderly drift into a slide. Layered on top, net CHEX at -$34.5M means time decay itself is leaning the book short into the bell; dealers don't need a fresh catalyst to press, the clock is doing the work.

The line in the sand is 739 - the Call Wall sitting 0.0453520879 above spot. Bias reads Neutral, which is the polite way of saying spot has to reclaim that pivot before dealer flow flips from amplifier to cushion. Until then, treat strength as fade-able into the call wall and any break of 738.00 as confirmation that the vanna-charm tandem is escorting the tape lower into close.

What it means for your trading

Vanna and charm are both pressing dealers short - VEX at -$61.14B guarantees a VIX uptick amplifies downside, while CHEX at -$34.5M drags the book lower into the bell. Reclaim of 739 is the single trigger that flips the regime; absent that, fade strength.

Cross-Asset Confirmation

Cross-asset tape reads Unknown but not contagious: VIX is bid 9.62% while MOVE sits at 69.63 with no Treasury-vol confirmation despite the yield blowout in headlines. Credit is not panicking - this is an isolated geopolitical/oil shock, not a funding event.

Sentiment confirms the disconnect: Fear & Greed still reads Greed at 65, nowhere near capitulation. Yet the equity complex is uniformly short-gamma - QQQ at 707.44 and IWM at 277.93 both trade below their flips, Aligned with SPY's negative-gamma stance. No index is offering dealer cushion to absorb the shock.

Playbook: mean reversion until MOVE breaks higher. The single confirm that flips this from fadable shake to compounding stress is Treasury vol joining the bid. Until then, lean into Iron Condor structures and treat the oil tape as the proximate vol driver, not the credit channel.

What it means for your trading

VIX-only stress with MOVE at 69.63 and F&G Greed at 65 keeps this in geopolitical-shock territory, not credit unwind. Aligned short-gamma across SPY/QQQ/IWM amplifies intraday moves but mean-reversion playbook holds unless Treasury vol confirms.

Scenario EV

The book scores Iron Condor at 58 versus put spread at 50 - skew is already paying for naked downside via 2.79%, so harvesting both wings dominates a single-side structure. VRP read prints Unknown, but with ATM IV at 16.17% sitting above HV20 at 10.82 the premium is there to be sold against defined risk.

Park the structure in the 30-45 DTE window - far enough from spot to dodge the 0DTE gamma whipsaw through the 745.86 flip, close enough that the front-end vol pop into VIX at 18.92 still pays. Contango on the term keeps theta on your side, and VVIX at 94.26 in Normal territory greenlights Standard Size.

Anchor wings outside the 739.00 / 738.00 band and treat a break of 738.00 as the cut-and-walk trigger - short-gamma below flip means the downside wing convexes against you fast.

What it means for your trading

Lead with Iron Condor at score 58 in the 30-45 DTE band - condor captures both wings where put spread can't, with standard size cleared by VVIX in Normal.

Actionable Summary

Bottom line: sell defined-risk premium via Iron Condor structures pivoting around 739, with the 30-45 DTE band giving you VRP at 5.35% without 0DTE whipsaw through the flip. Avoid naked vol selling and chasing 0DTE puts after the VIX bid to 18.92 - vanna at -$61.14B and charm at -$34.5M are both hostile, so size standard, not aggressive.

Watch level: reclaim of 745.86 flips dealer flow from amplification to cushion mode; until then, spot at 738.67 sits below flip and every push lower gets sold harder. Trigger: a break of 738.00 is the trend-day signal - cut shorts, exit premium, step aside. Fade strength into 739.00 while the Contango curve and Aligned complex keep the mean-reversion playbook live.

Context: regime Elevated / Watchful, half-life 15 sessions - this fades absent fresh catalyst, but MOVE at 69.63 is the credit-channel tell to watch.

What it means for your trading

Defined-risk Iron Condor around 739 is the trade; 745.86 reclaim flips the regime supportive, 738.00 break is the exit.

Cramer's morning checklist captures the regime cleanly: rising oil and yields with falling futures is the exact combo that turns dealer short-gamma into trend-day downside.

30Y at multi-month highs is the credit-channel risk - if MOVE follows, this stops being an isolated equity event and becomes the kind of compounding shock the regime can't fade.

China-sanctions optionality on Iranian oil buyers is a wildcard - any softening would crater the oil bid that's driving today's risk-off and likely snap VIX lower fast.

Airline cancellations are a tape-level signal that the conflict is constraining real activity - relevant for travel, energy, and insurer single-name dispersion.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.82 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 745.86 against a spot of 738.67. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.17% with a volatility risk premium of 5.35%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.92. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime