Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

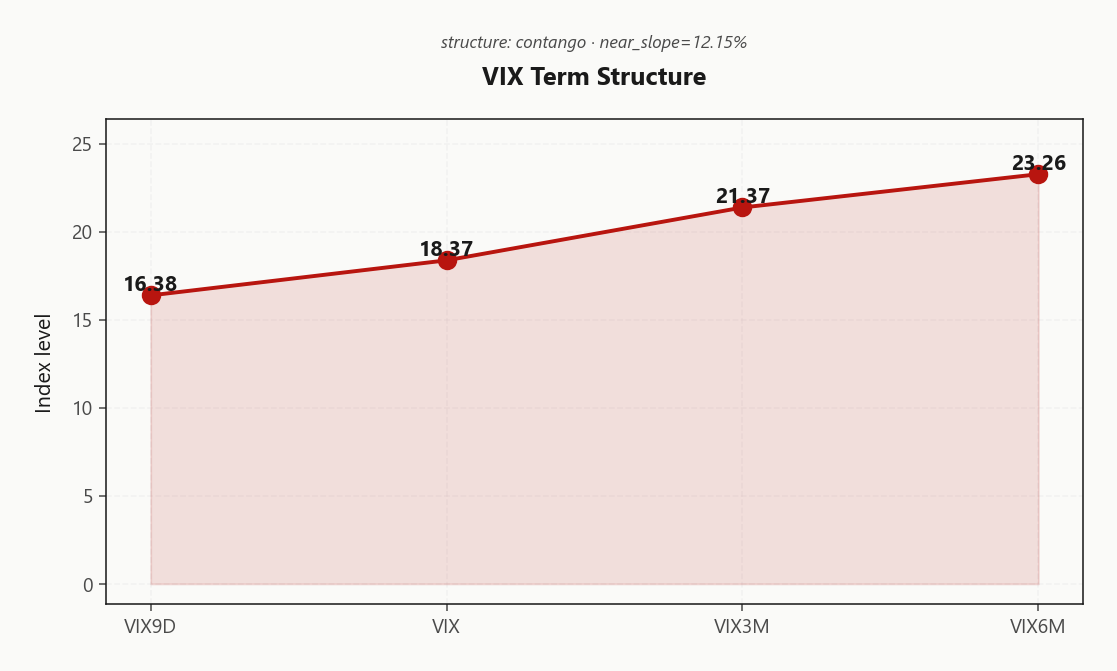

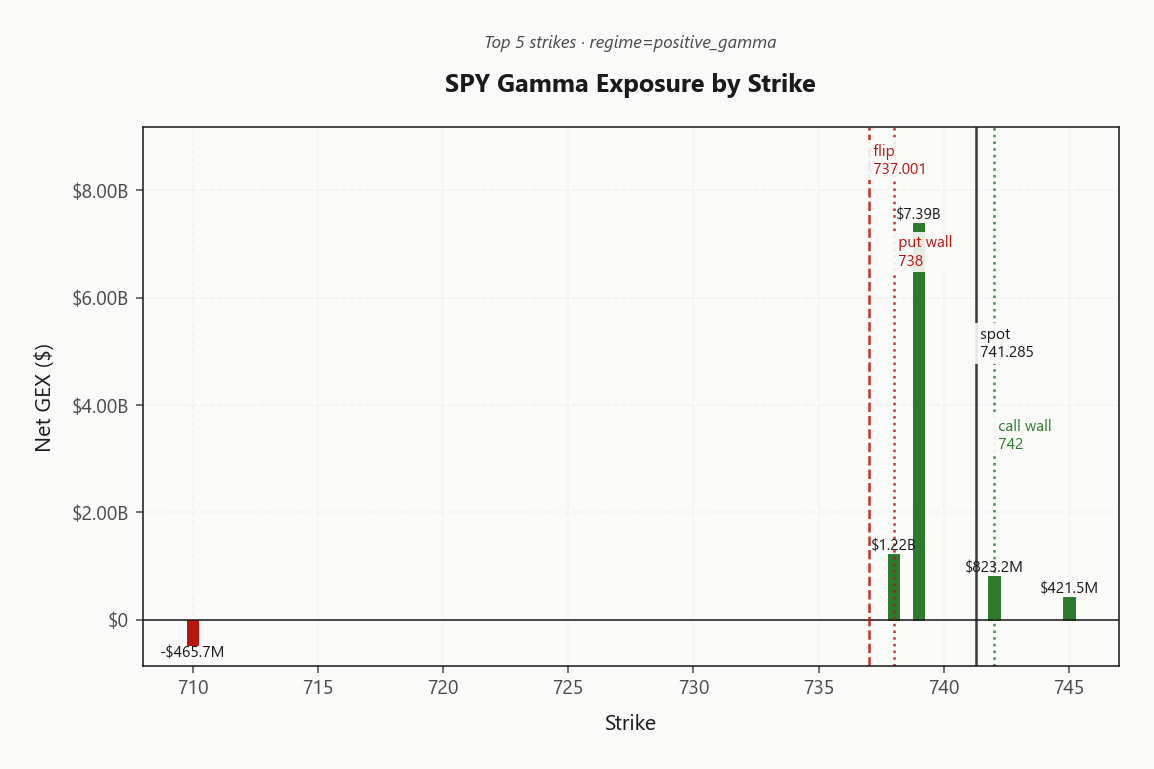

SPY trades at 741.29 in a Positive Gamma regime with net GEX of $8.86B - dealers long gamma, moves get dampened. Call wall sits at 742.00, put wall at 738.00, gamma flip at 737.00 - spot is right at the upper wall, meaning pin pressure dominates intraday but a break above 742.00 forces dealers to chase. Dealer vanna is heavily negative at -$65.82B - if VIX keeps grinding higher from 18.37, expect downside delta to be sold into weakness. VIX term is in Contango with VIX9D 16.38 under VIX 18.37 under VIX3M 21.37 - front-end carry is intact and VRP runs 4.52% vol points rich to 20-day realized 10.27. Crucially QQQ is Negative Gamma with net GEX -$912M and IWM is Negative Gamma - the index is NOT confirming SPY's calm. Bottom line: sell premium in SPY with iron condors 30-45 DTE around the 738.00/742.00 corridor, but trim size and avoid naked short vol in QQQ/IWM where dealers amplify.

SPY positive gamma cushion above flip while QQQ/IWM sit short gamma - index complex split

SPY is locked in a positive-gamma corridor between the put wall and call wall while QQQ and IWM both sit below their gamma flips - a classic cross-asset divergence where the index headline masks fragility under the surface. VIX term structure remains in steep contango with VVIX benign, so vol sellers still have carry, but Iran/oil headlines and a 6.43%% VIX pop warn that the calm is rented, not owned. The actionable read: harvest premium via defined-risk structures in SPY, stay smaller and more defensive in QQQ/IWM where dealer flow amplifies rather than dampens.

Regime Assessment

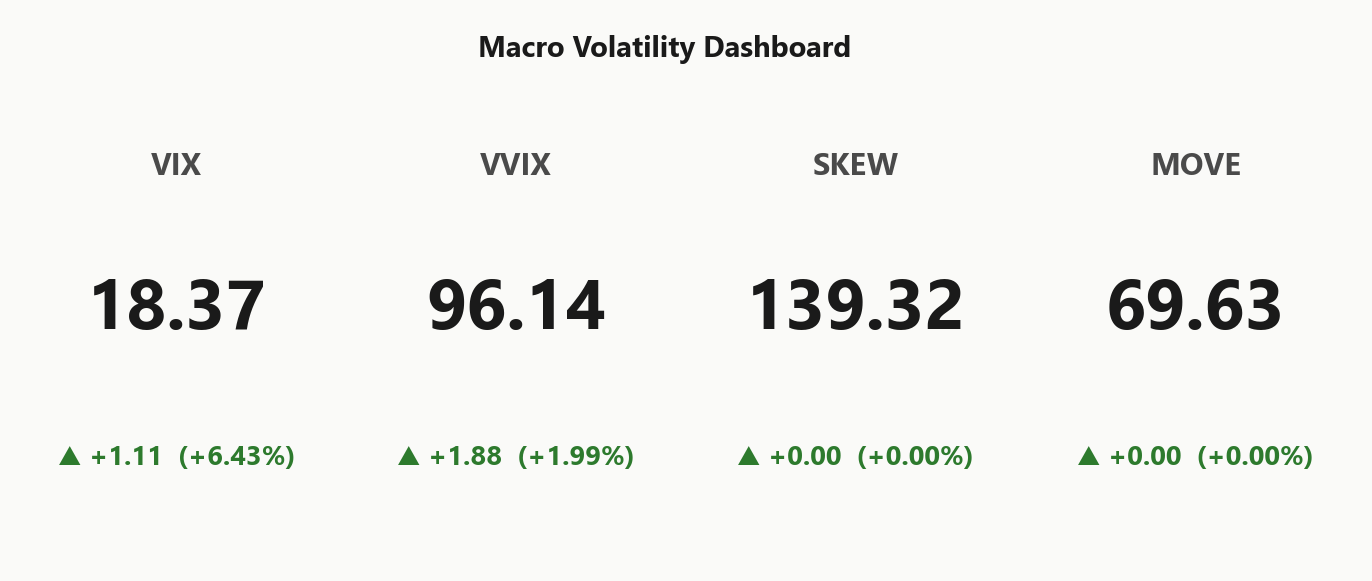

The tape sits in an Elevated / Watchful regime with VIX anchored at 18.37 - not panic, not calm, but the middle band where dealer mechanics still function and tail hedges still earn their keep. Transition probabilities tell the story: panic odds over five sessions are pinned at 0.05, while the path back to a low-vol regime over ten sessions sits at 0.45 - modal outcome is grind, not break.

Half-life of 15 sessions confirms this regime is sticky but not entrenched. That's the operative nuance: long enough to monetize via 30-45 DTE structures, short enough that Iran headline risk remains the obvious accelerant. The cross-asset split - SPY Positive Gamma while QQQ and IWM trade Negative Gamma - is the fragility tell underneath the index calm.

Trade the regime you have: harvest premium where dealer flow dampens. Hedge the regime that could come: keep convexity on the books, watch the SPY gamma flip and VVIX as the trip wires that flip the script.

What it means for your trading

Regime label Elevated / Watchful with panic probability 0.05 over five sessions and half-life of 15 - position for the current grind, but keep tail hedges live for the Iran-driven transition risk.

Trading readVIX up, VVIX benign, MOVE quiet, SKEW elevated - the dashboard says elevated-watchful, not panic. The divergence to watch is VIX rising while MOVE stays low - if MOVE catches up, the macro-credit channel turns active.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve stacks cleanly: 16.38 under 18.37 under 21.37 under 23.26 - Contango through every tenor with the near slope at 12.15%. No event premium priced into the front; the market is paying carry to anyone willing to sit short.

Forward 30-60 and 60-90 vols both step up cleanly off the spot curve, so the term structure isn't just steep on the surface - it's properly ordered through the back. Regime reads Steep Contango: Steep contango - vol sellers favored. No inversion stress at the 30d/3m or 3m/6m joints means the curve isn't telegraphing a near-term shock even with Iran headlines hot.

The trade is in the belly. Front-week premium gets killed by headline whip; the back end carries too little theta to pay for the wait. 30-45 DTE is where the slope compounds against realized fastest - calendar-style harvest and iron condors anchored to that bucket extract the curve's shape, not just its level.

What it means for your trading

Steep Contango from 16.38 through 23.26 with a clean forward step-up - vol sellers are paid, and the 30-45 DTE belly is where the curve's carry compounds hardest against realized.

Trading readSteep contango through every tenor says the market is not pricing a near-term shock - the curve favors vol sellers. Watch for VIX9D crossing VIX as the canary; that inversion is the regime kill signal.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.79% sits materially above 20-day realized 10.27, leaving the variance risk premium fat at 4.52% vol points - options are expensive relative to what spot has actually been doing.

The realized term itself is decelerating: HV20 10.27 prints well under HV60 14.91, confirming the tape has been quieter into the current window than the trailing two months. That deceleration is the structural tailwind for short-vol carry - implieds haven't marked down to match, and the gap is being paid.

Caveat: the richness isn't free money. The premium embeds Iran tail compensation, not a pricing error. Harvest the body where dealer flow dampens - SPY long-gamma corridor - and leave QQQ/IWM premium alone, where Negative Gamma dealer positioning amplifies rather than absorbs the move you're short.

What it means for your trading

VRP active and rich versus a decelerating realized path - premium sellers favored in SPY's long-gamma anchor, but the IV/HV gap is tail compensation for Iran headline risk, so harvest structurally and respect the wing.

Skew Convexity

Quarter-delta skew has steepened to 2.63% vol points with the smile ratio printing 1.28% - puts at 11.93% sit a wide margin above calls at 9.3% against an ATM of 10.78%. This is an ordered downside bid, not a panic - the tail is being paid for in size while the upside wing trades flat to inverted, signaling zero dealer or fast-money conviction on a melt-up.

The Iran headline tape is doing the work: vanna at -$65.82B means any further VIX grind from 18.37 forces dealers to dump delta into weakness, which is exactly the convexity the put wing is pricing. With cross-asset regime Spy Heavier and QQQ already Negative Gamma, downside convexity is the cleanest book in the complex.

Trade: spread the put side - debit put spreads or condor put wings inside the 738.00 shelf. Do not sell naked downside into this skew; the wing is paying for a reason. Calls at 9.3% are lottery tickets - own them outright as cheap upside convexity, don't finance them by shorting puts.

What it means for your trading

Downside is bid in an orderly, paid-for way while upside trades depressed - structure the book with put spreads not naked puts, and treat calls at 9.3% as cheap convexity rather than collateral to short.

Vol-of-Vol Structure

VVIX sits at 96.14 against a VIX print of 18.37, putting the ratio at 5.23 - squarely in the Normal band. Translation: the tape is pricing vol drift, not a binary. Despite the Iran headline overhang and a 6.43% VIX pop, the jump-risk channel is dormant - no panic bid in second-moment vol means short-vol structures get sized Standard Size, not defensively trimmed.

The implication runs straight through the strategy stack: VVIX benign is the green light that lets the iron condor score top the book at 54, because the wings aren't being repriced by a convexity bid. That changes the moment VVIX clears the 110 handle - that's the trip wire into half-size, wider wings, and a meaningful cut to gross premium sold. Until then, the carry is real and the body is harvestable.

Keep the convexity tail on regardless: with VVIX this contained, OTM wings and ratio'd tails are cheap relative to the body you're selling. Iran tape is the headline accelerant - own a little gamma against the carry book and let the ratio do the warning.

What it means for your trading

VVIX at 96.14 against VIX 18.37 keeps vol-of-vol in the Normal band - size short premium Standard Size but pre-stage the cut at VVIX 110.

Dispersion Spread

Index vol sits anchored with SPY ATM IV at 14.79% while the single-name AI complex churns underneath - AMZN leads the GEX-shift tape in the Negative direction, with META and NVDA rounding out a mover list whose absolute deltas dwarf anything the index itself is doing. Dispersion is moderate but the signature is clean: idiosyncratic vol concentrated in mega-cap names, not in the basket.

Translation for the book: SPY/SPX premium sale carries the cleanest edge because the index dampener stays intact while the constituent vol burns off into single-name event tape. Iron condors on the index harvest the calm; single-name short strangles on NVDA or AMZN are paying for a reason - that's name-specific risk, not free carry.

Corollary: hedging single-name AI exposure with index puts underperforms in this regime. The correlation isn't there when SPY is Positive Gamma and the movers are trading on their own catalysts - buy the name's own wing or skip the hedge.

What it means for your trading

Moderate dispersion with index IV at 14.79% firm against an AI-mover tape led by AMZN (Negative) - sell SPY premium, leave single-name strangles alone, and hedge names with name wings rather than index puts.

Liquidity & Microstructure

SPY's book is anchored by a single mega-strike magnet at 739.00 carrying $7.39B of net GEX - the rest of the strike ladder is noise by comparison. With spot parked above the gamma flip at 737.00, dealers are mechanically buying dips and fading rips inside the corridor, which is exactly why intraday range keeps compressing into the magnet.

The 742.00 call wall caps chasers from above while the 738.00 put wall cushions from below - trade the corridor, fade the extremes. Note the highest OI strike sits at 505, a legacy cluster well detached from current price action; the live magnet is the gamma-weighted strike near spot, not the headline OI print.

The level that matters is 737.00. Hold it and the Positive Gamma regime stays intact - dampening, mean-reverting, condor-friendly. Lose it and SPY joins QQQ (Negative Gamma) and IWM (Negative Gamma) in amplification mode, where every dealer hedge feeds the move rather than absorbs it. That is the regime trigger.

What it means for your trading

SPY is pinned to a single dominant gamma strike with dealers absorbing flow between 738.00 and 742.00; a clean break of 737.00 inverts the regime and aligns SPY with the already-fragile QQQ/IWM tape.

Trading readSPY's gex profile is dominated by a single mega-strike near spot - that's the magnet the tape pins to until it breaks. Above the call wall dealers chase; below the put wall they sell - trade the corridor, fade the extremes.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna sits deeply negative at -$65.82B - the trapdoor under the long-gamma cushion. If 18.37 grinds higher from here, dealers are forced to sell delta into weakness, and that vol-up/delta-down feedback compounds any pullback the gamma book would otherwise dampen. Gamma says mean-revert; vanna says chase the downside. The two are pulling opposite directions, which is exactly why the tape looks placid intraday while skew keeps bidding the tails.

Charm prints modestly negative at -$34.5M - a secondary drag, biased toward end-of-day pressure on dated puts as time decay rolls dealer hedges. It's a tailwind for pin behavior into the bell, not a primary driver. Vanna is the story; charm is the footnote.

The pivot is the Call Wall at 742, current bias Neutral. Above it dealer flow changes character - forced chase replaces absorption. Bottom line: vanna posture is hostile if VIX breaks its recent range, standard otherwise. Size to the trapdoor, not the cushion.

What it means for your trading

Vanna at -$65.82B is the asymmetric risk - a VIX break-out from 18.37 turns dealer flow procyclical and overrides the positive-gamma anchor. Trade the corridor, but keep tail hedges on through the 742 pivot.

Cross-Asset Confirmation

The index complex is split: SPY holds a Positive Gamma posture above its flip while QQQ at 711.28 and IWM at 278.18 both trade Negative Gamma beneath theirs. Regime divergence reads Spy Heavier - textbook late-cycle setup where headline index calm masks tech and small-cap fragility underneath. Trade SPY for mean reversion inside the corridor; treat QQQ and IWM as trend vehicles where dealer flow amplifies rather than dampens.

Sentiment hasn't caught up to the tape. Fear & Greed still prints Greed at 64 even as VIX pops on Iran headlines - complacency-versus-price divergence that historically resolves through price, not sentiment. MOVE at 69.63 alongside a thirty-year north of five handles and a bid in crude says this is a macro-credit channel, not an equity-isolated wobble.

Bottom line: harvest SPY premium with defined-risk structure, stay smaller in QQQ and IWM, and watch the SPY flip - if it breaks while F&G is still in greed, the catch-up trade is violent.

What it means for your trading

SPY's long-gamma cushion is the only thing standing between an orderly tape and a tech-led drawdown; with QQQ and IWM already Negative Gamma and sentiment still in Greed, the asymmetric risk is sentiment catching down to MOVE at 69.63.

Scenario EV

The strategy stack ranks Iron Condor at the top with a score of 54, edging out the put spread at 45. The setup is clean: VRP is Unknown, VVIX sits in the Normal band, and SPY anchors the book in a Positive Gamma regime - defined-risk wings get paid without dealer flow turning hostile inside the corridor.

Put spread is the runner-up and the natural fit for a tape where put skew rides above call skew, but the capped reward leaves carry on the table when the long-gamma anchor is already doing the dampening work. The 30-45 DTE bucket is the sweet spot - far enough out to bleed VRP, short enough to redeploy, and crucially past the front-week Iran-headline whip that punishes naked 0DTE shorts.

Sizing standard per Standard Size - VVIX has not yet tripped the half-size threshold. Anchor the structure inside the 738.00/742.00 corridor and let the gamma flip at 737.00 be the kill switch.

What it means for your trading

Iron condor wins the scorecard at 54 over put spread at 45 - VRP active, VVIX benign, SPY long-gamma anchor align in the 30-45 DTE window. Standard sizing holds until VVIX breaks regime.

Actionable Summary

BLUF: Sell premium in SPY via Iron Condor structures in the 30-45 DTE bucket, anchored between the 738.00 put wall and 742.00 call wall. Long-gamma cushion above the 737.00 flip, an active VRP, and benign VVIX at 96.14 all align - carry compounds while dealer flow dampens intraday whip.

Avoid naked short vol in QQQ (Negative Gamma) and IWM (Negative Gamma) where dealers amplify rather than absorb. Avoid naked index puts - skew sits at 2.63%, so spread the put side rather than sell the wing outright. Tail hedges stay warranted while Iran headline tape and the 69.63 MOVE backdrop keep credit-channel risk live.

Watch: the SPY gamma flip at 737.00 - a break inverts the regime to QQQ/IWM-style amplification - and the charm pivot at 742 where dealer flow changes character. Regime reads Elevated / Watchful: trade what you have, hedge what could come.

What it means for your trading

Harvest defined-risk premium in SPY's long-gamma corridor between 738.00 and 742.00, stay defensive in QQQ/IWM, and treat the 737.00 flip as the regime trip wire.

Iran no-trust posture toward US sustains the geopolitical tail premium baked into front-end skew - this is why puts still bid even with VIX in contango.

BRICS divisions over the Iran war = no coordinated de-escalation path, keeps the energy-led inflation tail alive and reinforces MOVE-implied bond stress.

A US pivot on Chinese sanctions for Iran oil buyers would be the single largest near-term de-escalation catalyst - watch the tape react to any concrete announcement.

European equities tumbling on Iran/inflation worries is the cross-asset confirmation that this is a macro shock, not US-isolated - strengthens the credit-channel read.

Airline cancellations are the real-economy signal that this isn't just headline risk - supply-chain and travel disruption feed into Q2 GDP and inflation expectations.

Oil bid on stalling peace hopes is the direct transmission belt from geopolitics to inflation to bonds to equity vol - track oil to forecast the vol path.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.82 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 737.00 against a spot of 741.29. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.79% with a volatility risk premium of 4.52%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.37. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime