Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

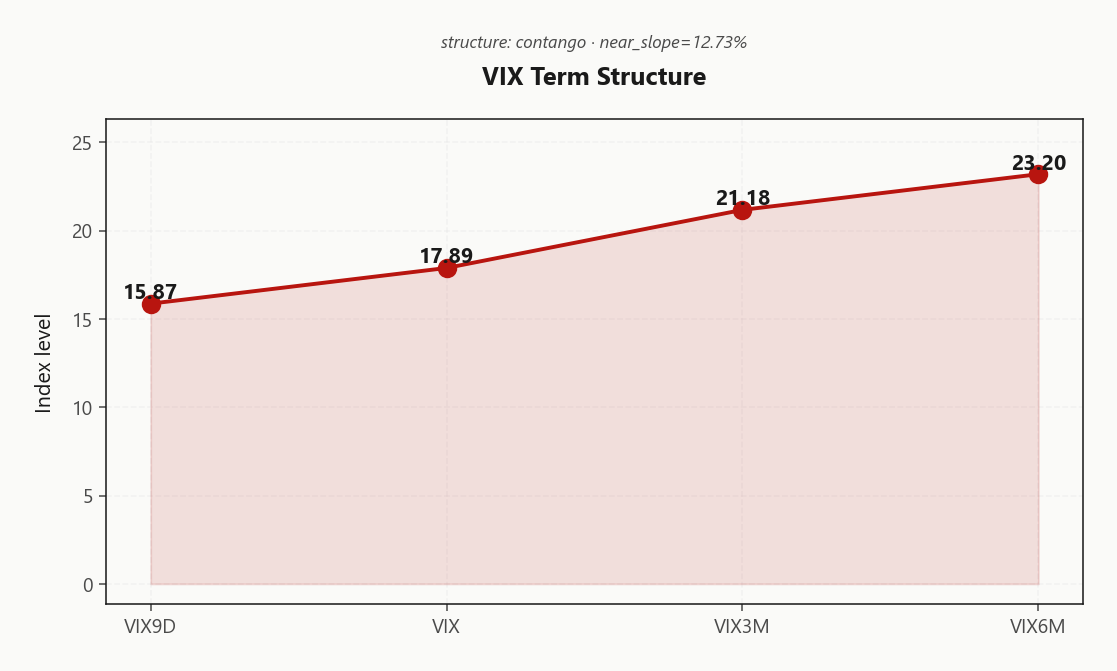

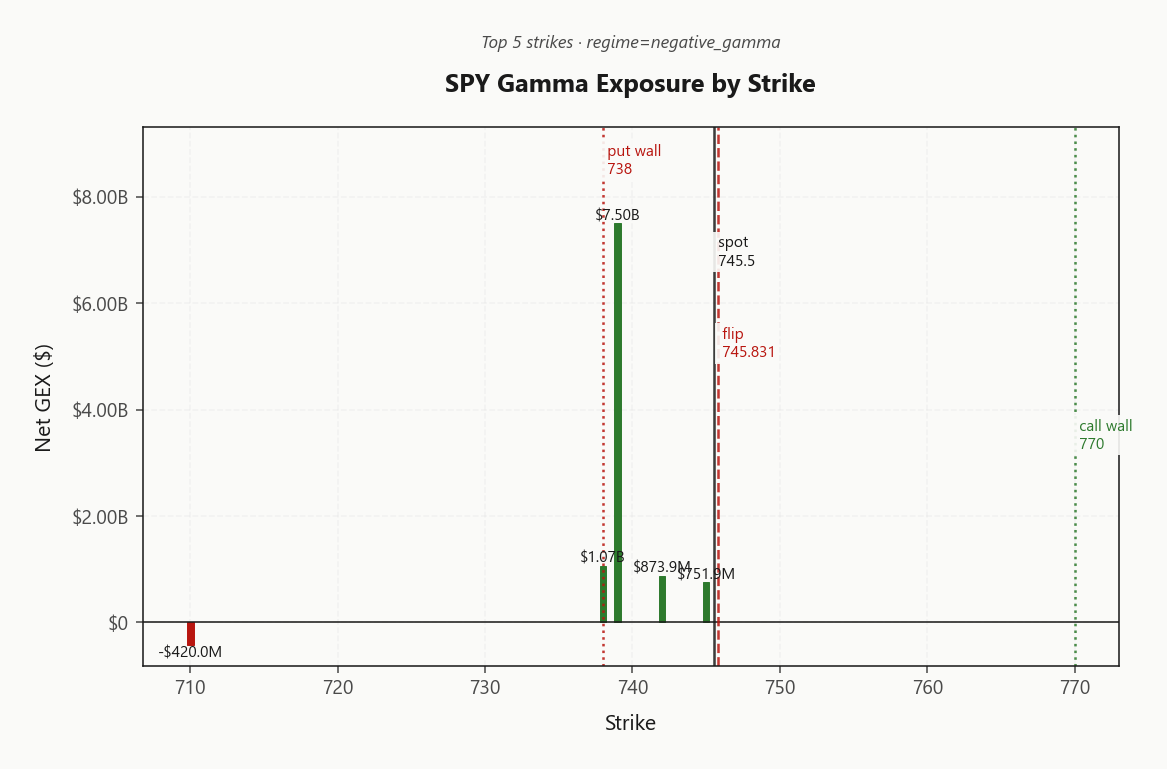

SPY at 745.50 sits effectively on top of gamma flip 745.83 with net GEX $9.65B - technically negative_gamma but the cushion is razor-thin, expect chop with directional risk only on a clean break. Call wall 770.00, put wall 738.00, max pain 713.00 - the 739.00 strike is the dominant magnet with $7.5B of concentrated gamma. Dealer vanna -$76.26B is destabilizing on any vol pop, but charm $202.2M provides supportive bid into close. VIX 17.89 with term structure Contango (vix9d 15.87 → vix3m 21.18) - front-month VRP 4.92% is rich. QQQ holds positive gamma at $82M with spot above flip 715.26, IWM short gamma at $84.2M - divergence flags single-name pressure under index calm. Bottom line: sell premium in 30-45 DTE iron condors, half-size if VIX breaks 17.89, watch 745.83 as the tape's true compass.

SPY trades within a hair of its gamma flip at 745.83, putting dealers on a knife edge between dampening and amplifying flow while QQQ holds positive gamma. VIX term structure in Steep Contango with VVIX at 98.36 keeps vol-of-vol benign, favoring premium harvest. The cross-asset split - QQQ stable, SPY/IWM short gamma - is today's lead story and the tell for whether mean-reversion or trend wins.

Regime Assessment

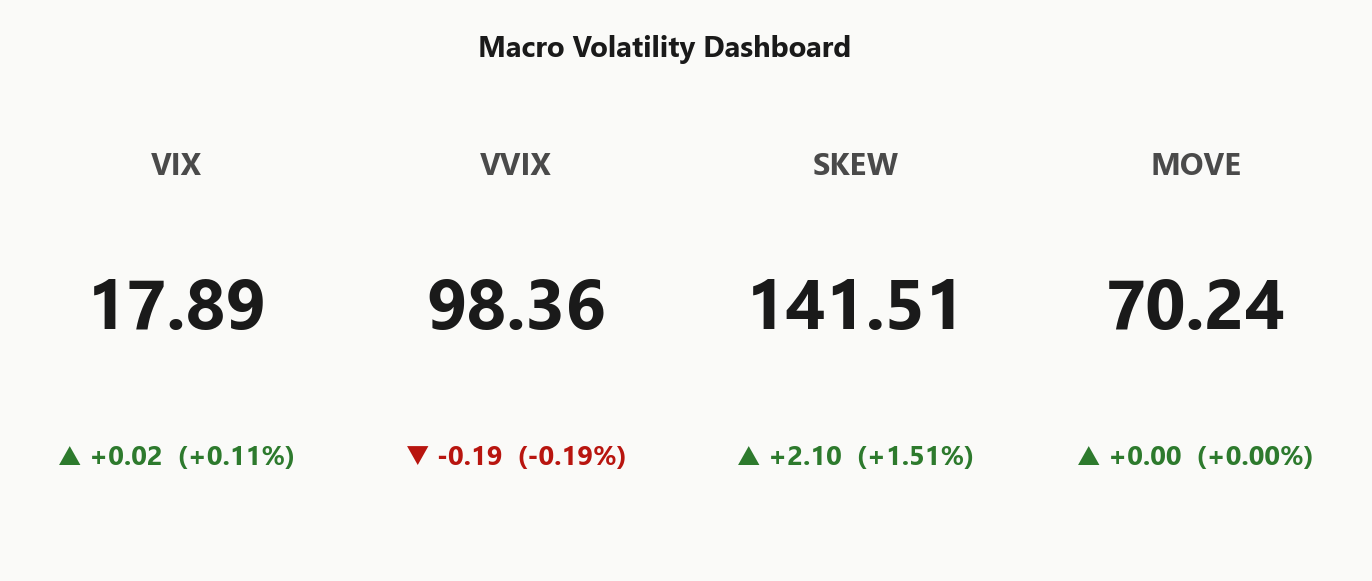

Current regime reads Elevated and labels out as Elevated / Watchful with VIX anchored at 17.89 - neither the somnolent low-vol carry tape nor a panic print, but the watchful middle where premium sellers still earn and tail buyers still overpay.

The transition matrix favors decay over escalation: probability of slipping to a low-vol regime over the next ten sessions runs at 0.45 versus only 0.05 of jumping to panic in five. Half-life of 15 sessions says this state is moderately sticky - long enough to build positions into, too short to treat as the new permanent backdrop.

Yellow signal, not red. Be alert, not defensive: standard sizing on premium harvest, keep tail hedges small and dated, and let the asymmetric decay path do the heavy lifting. The regime rewards patience over preemption.

What it means for your trading

Regime sits in the Elevated / Watchful band with the decay path materially more probable than the panic path over the relevant horizon - build short-vol exposure with conviction but keep convex tail risk on as a small, dated overlay.

Trading readVIX, VVIX, SKEW and MOVE are aligned in a benign-but-watchful regime - no two are screaming divergent stress, which is the green light for premium harvest and the warning sign that complacency itself is the risk.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

VIX term structure prints Contango with the front sloping 12.73% from vix9d 15.87 through spot VIX 17.89 to vix3m 21.18 and vix6m 23.20 - Steep contango - vol sellers favored. With vix9d sitting that far below vix3m, the tape is pricing zero near-term event premium; this is a structural carry trade, not a transient quirk.

Front-month futures basis at 18.39% above spot confirms the read - no event-driven backwardation lurking, the curve is doing exactly what the systematic short-vol complex needs it to do. Forward 30/60 at 22.6464688197 versus forward 60/90 at 25.0576854478 shows the steepest roll-down sits in the belly.

That belly is the harvest zone. 30-45 DTE captures the fattest roll-down without pressing into the gamma cliff where charm and pin risk dominate. Sell the curve where it's steepest, let theta work, leave the wings.

What it means for your trading

Term structure is in Steep Contango with no event premium priced - the belly of the curve is the cleanest premium harvest, and front-month futures basis at 18.39% confirms no backwardation risk priming a regime flip.

Trading readSteep contango from vix9d through vix6m says the carry trade is firmly in place and the market expects no near-term shock - sellers of the belly get paid, and only a contango-flatten event would invalidate that read.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.68% sits stubbornly above HV20 9.76, leaving the variance risk premium at 4.92% - options are demonstrably rich to what the tape has actually delivered, and defined-risk sellers collect the spread.

The term structure of realized tells the second half of the story: HV60 at 14.72 prints meaningfully above HV20, so realized has been decelerating, not accelerating. The market is calming faster than the IV complex is willing to rerate, and that lag is the harvest. No realized-vol acceleration signal here to flag a regime break.

Edge sits with defined-risk premium sellers - not naked vol. With dealer vanna hostile and the gamma flip a hair from spot, the IV-RV gap is the cleanest carry on the page; let the convergence do the work into time decay.

What it means for your trading

Wide IV-over-realized gap with HV20 below HV60 - implied vol is sticky against a decelerating tape, and the 4.92% VRP pays defined-risk sellers cleanly without requiring a directional view.

Skew Convexity

Quarter-delta skew prints 2.31% with smile ratio 1.15% - steep but orderly. Put-side 18.22% sits well bid above ATM 17.15%, while the call wing prints a flat 15.91%. Hedgers are paying up methodically for downside protection; this is mechanical convexity demand, not panic.

The flat call wing is the tell: zero upside conviction in the listed market. Overwrites collect no skew tailwind, and outright long calls get no help from the surface. CBOE SKEW at 141.51 sits elevated but stable - embedded tail demand is structural, not freshly bid into a shock.

Structure follows the surface: put spreads dominate naked puts at this skew, since the back leg recoups the convexity premium you're paying on the front. Fade the wings for premium harvest, but express directional downside through defined-risk spreads rather than buying the rich quarter-delta outright.

What it means for your trading

Skew at 2.31% is steep-but-orderly with a flat call wing - put spreads beat naked puts, and overwrites get no skew lift. SKEW 141.51 elevated but stable confirms structural hedging, not panic positioning.

Vol-of-Vol Structure

VVIX prints 98.36 against VIX 17.89, putting the ratio at 5.50 - squarely in Normal territory. No embedded jump premium, no binary event being priced. The convexity bid is asleep.

That collapses the case for defensive haircuts. Sizing guidance reads Standard Size, meaning short-vol structures carry at full weight rather than the tail-shy half-clip you'd run if VVIX were screaming. Convexity buyers have no edge here - paying up for gamma-of-gamma when the second derivative is this quiet is a slow bleed.

Watch the ratio, not the absolute level: a VVIX pop without a VIX move is the early tell that someone is reaching for tails. Until then, fade vol-of-vol the same way you fade vol - sell the wing, harvest the decay, and let the regime do the work.

What it means for your trading

VVIX/VIX at 5.50 marks a Normal vol-of-vol regime - no jump premium, no haircut required. Run Standard Size on short-vol structures and ignore the convexity bid.

Dispersion Spread

Index tape is sleepwalking while single-name vol is wide awake. SPY ATM IV at 14.68% sits muted against QQQ at 24.21% and IWM at 20.84% - a textbook Moderate dispersion print where correlation has softened enough to detach the index from its components.

The implication is mechanical: index puts underprotect a single-name book here. Basis risk on hedging mega-cap convexity with SPY puts is real and widening, particularly given QQQ's premium to SPY and IWM's elevated wing. Leave single-name vol to dedicated dispersion desks - chasing it through SPX is paying for the wrong gamma.

Cleanest harvest is on the index leg: SPY/SPX premium is the dispersion-trade short side, and selling it without a single-name long book just collects the correlation discount neat. QQQ at 24.21% offers the fatter premium for those willing to wear concentrated AI-complex exposure.

What it means for your trading

Dispersion is flagged Moderate - sell SPY/SPX vol, do not use it as a single-name hedge. QQQ at 24.21% versus SPY at 14.68% is the carry signature.

Liquidity & Microstructure

The book's center of gravity has migrated to the front of the strip: top strike 739.00 carries $7.5B of concentrated dealer gamma, a magnet sitting essentially on top of spot. Highest OI at 530 is structural and far from the tape - ignore it for intraday navigation. OI-weighted DTE of 120 sessions confirms a balanced near-versus-far book, so the gamma cluster at the front is doing the work today.

Gamma flip 745.83 is the entire regime in one number - spot is within pennies, and the cushion is razor-thin. Hold above and dealer hedging dampens; pierce it and they amplify into the move. The bracket is clean: call wall 770.00 caps upside, put wall 738.00 caps downside, with the active battle compressed into the strikes between.

Microstructure reads deep but precarious. Trade the bracket while it holds; treat any clean break of 745.83 as a regime change, not a dip.

What it means for your trading

Liquidity is deep around the front-strike magnet at 739.00, but the gamma flip 745.83 sitting on top of spot means dampening and amplifying regimes are one tick apart. Fade extremes inside the 738.00 - 770.00 bracket; respect the flip as today's true compass.

Trading readGamma is concentrated right around spot at the 739.00 cluster - the tape will magnetize there, with mean-reversion above and amplification below the flip; the entire day's character pivots on whether spot holds above or breaks below.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$76.26B - deeply negative, which means dealers shed delta as vol expands and become an outright accelerant on any downside vol pop. The book is coiled hostile: a VIX expansion converts the dealer complex from passive to procyclical in seconds, so any fresh put exposure should be half-sized until the vanna footprint releases.

Offsetting that, CHEX at $202.2M is positive and supplies a supportive bid as charm decay drags hedges back toward pinned strikes into the bell - particularly potent on Fri-pinned expiries where the time-decay vector compounds. Charm is your friend into the close; vanna is the enemy on any intraday vol shock.

The pivot sits at 745.8306114757 - coincident with the gamma flip itself, making it the single most important level on the page. Current bias reads Destabilizing with signal flagged Red: trade the pin, but keep convex tail hedges small, dated, and ready for a clean break of the pivot.

What it means for your trading

Vanna at -$76.26B is the destabilizer on any VIX expansion while charm at $202.2M cushions into the close - pivot 745.8306114757 is the regime compass with current bias Destabilizing.

Cross-Asset Confirmation

MOVE at 70.24 sits subdued - the rates and credit complex is not priming an equity vol shock, which strips out the macro accelerant that usually turns dealer short gamma into a cascade. Fear & Greed prints 64 (Greed) - sentiment is crowded long without tipping into euphoria, contrarian caution warranted but not yet a fade trigger.

The lead story is the cross-asset regime split. QQQ holds positive_gamma at $82M with spot above flip - tech mega-cap is the index's stabilizer and the bullish tell that leadership remains intact. SPY hangs on its flip in negative_gamma while IWM sits short gamma at $84.2M, flagging small-cap and credit-sensitive stress beneath the index calm. Divergence direction prints Qqq Heavier - the break, when it comes, almost certainly originates in IWM before contaminating the top.

What it means for your trading

Benign MOVE plus crowded-long sentiment plus QQQ-anchored positive gamma argues for premium harvest while watching IWM as the canary - the cross-asset signal is aligned for short vol, but the divergence direction Qqq Heavier means small-caps lead the regime test.

Scenario EV

The scoring model crowns Iron Condor at 71, comfortably ahead of the put spread at 62 - the math reflects what the tape is already telling you. Rich VRP at 4.92%, term structure in Steep Contango, and a Normal vol-of-vol regime hand the seller carry on three axes simultaneously, while the call wall at 770.00 and put wall at 738.00 bracket spot with surgical cleanliness.

Optimal DTE sits in the 30-45 window - far enough out to harvest roll-down without parking inside the gamma cliff, close enough that theta does real work. Strike the short call at or just inside 770.00, the short put at or just inside 738.00, and size Standard Size - VVIX at 98.36 embeds no jump premium worth haircutting around.

Skip naked strangles. With the gamma flip at 745.83 sitting within a hair of spot, defined-risk wings dominate uncapped tails - vanna at -$76.26B turns hostile on any VIX shock, and the condor's long wings are the insurance the strangle can't price.

What it means for your trading

Iron condor at Iron Condor scoring 71 in 30-45 DTE - shorts at 770.00/738.00, standard size, defined wings non-negotiable given the gamma-flip proximity.

Watch:745.8306114757 is the compass - spot is a hair Destabilizing of the gamma flip at 745.83, and a clean break flips dealer flow from dampening to amplifying. QQQ holding Positive Gamma at $82M versus SPY/IWM short gamma (Qqq Heavier) is today's tell - if the divergence resolves down, IWM leads.

Avoid: naked puts (skew at 2.31% means you're paying up), naked upside calls (no skew edge), and index hedges against single-name books - dispersion is alive. Hedge tail risk small and dated; vanna at -$76.26B only bites on a VIX shock, and front-end contango from 15.87 to 21.18 says none is priced.

White House oil-price scrambling under Iran war pressure keeps the energy-vol bid alive - watch crude-linked names and any defensive flow into puts on macro-sensitive sectors.

Xi's open-wider message to Trump's CEO delegation including Musk, Huang, Cook is a near-term tailwind for mega-cap tech and the source of today's META/GOOGL dealer GEX firming.

Iran allowing Chinese vessels through Hormuz is a de-escalation tell - partial relief for the Iran-war risk premium pricing into oil and equity tail hedges.

Trump-Xi summit framed as Iran-mediation venue - outcome will dictate near-term crude path and is the single biggest geopolitical catalyst overhanging the tape this week.

Asia Pacific banks raising provisions on Iran-war credit risk is a slow-burn macro story - watch for spillover to MOVE and US credit spreads if it accelerates.

Fresh Hormuz ship attacks during Trump-Xi diplomatic window keeps a floor under oil vol and tail-risk hedging in macro-sensitive equity sectors.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.82 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 745.83 against a spot of 745.50. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.68% with a volatility risk premium of 4.92%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.89. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime