Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

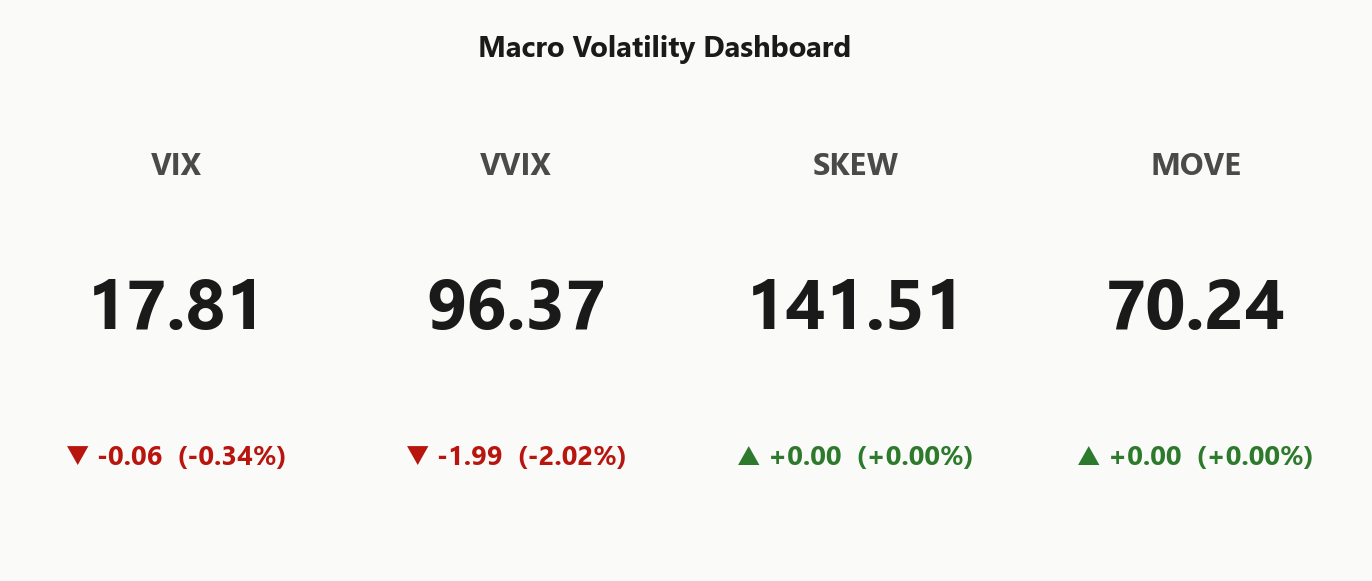

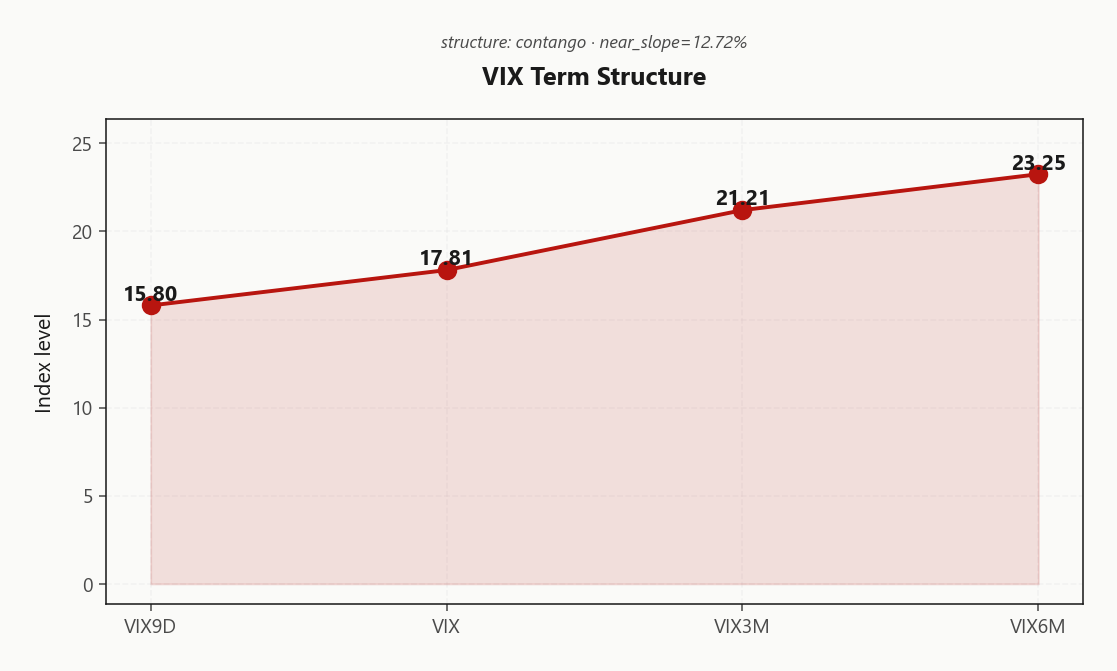

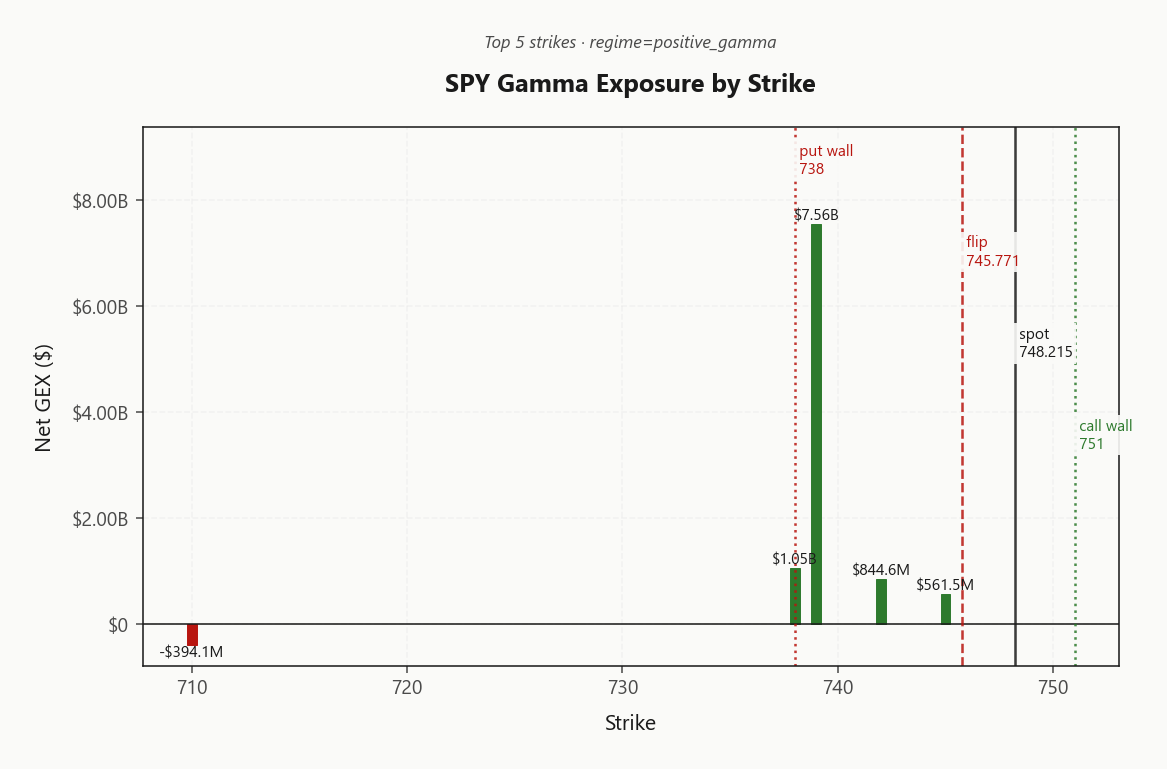

SPY at 748.22 sits in deep positive gamma with net GEX at $10.06B - dealers long gamma, moves dampened, mean-reversion the base case. Key levels: call wall 751.00, put wall 738.00, gamma flip 745.77 - spot trading just above the flip means the cushion is real but thin; a break below flips dealers from supportive to amplifying. Dealer positioning: net DEX $46.1B long, vanna -$79.47B negative (vol-up = sell delta, downside accelerant on a spike), charm supportive into close. Vol read: VIX 17.81, term structure Contango with VIX9D 15.80 under VIX3M 21.21, VRP active at 4.19%, VVIX normal at 96.37. Skew steepening at the 25d level (2.08%) says puts still bid relative to calls - pay for tail with spreads, not naked. Bottom line: iron condor structures in the 30-45 DTE window are the highest-EV trade today; size standard, but respect 745.77 as the hard line where dealer flow flips.

Positive gamma across index complex with steep contango - vol sellers favored, spot pinned above flip at 745.77

SPY trades above its gamma flip at 745.77 with dealers long gamma - moves dampened, mean-reversion favored into the call wall at 751.00. VIX term structure sits in steep contango (Contango) with VVIX at 96.37, blessing vol-selling structures. Cross-asset tone is aligned: SPY, QQQ, IWM all in positive_gamma, but Iran-war headlines and crude pressure keep tail hedges relevant.

Regime Assessment

The tape sits in Elevated / Watchful territory - not panic, not complacency. VIX at 17.81 anchors the elevated band, and the regime-classifier reads Elevated with a half-life of 15 sessions. Translation: this state is sticky absent a fresh catalyst, and the transition odds confirm it - probability of jumping to panic over the next five sessions sits at 0.05, while the path back to a low-vol regime over ten sessions clears at 0.45.

That asymmetry - low near-term tail probability, meaningful but not dominant odds of vol compression - is the trader's mandate to trade for mean-reversion within the regime, not for the regime break. Cross-asset confirmation is Aligned, with SPY, QQQ and IWM all reading Positive Gamma; nothing in the equity complex is leading a breakdown.

Operational read: the elevated/watchful label says size for chop, fade extremes, but keep a finger on the 745.7705445897 trip-wire. That's where sticky becomes slippery.

What it means for your trading

Regime is Elevated / Watchful with VIX at 17.81 and a 15-session half-life - sticky, mean-reverting, low odds of a panic transition. Trade the range, not the break.

Trading readVIX moderate, VVIX normal, SKEW elevated, MOVE muted - VIX and MOVE not confirming each other tells you rates vol is asleep while equity tail is bid. That divergence usually resolves toward the more nervous asset, which is equities.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

VIX term structure prints textbook Contango with VIX9D at 15.80 sitting cleanly under spot VIX at 17.81 - classic short-dated suppression that pays the carry but leaves zero cushion if a headline jolts the front. The back end tells the harder story: VIX3M at 21.21 against VIX6M at 23.25 embeds structural risk premium that the tape is unwilling to discount, consistent with the Iran headline tail and crude stress sitting just off-screen.

Forward 30-to-60 vol resolves to 22.7199933979, and that is exactly where calendar trades earn their carry - short the suppressed front, own the back where the premium lives. The Steep Contango regime label keeps vol sellers favored, but the 30-45 DTE band is the disciplined window: far enough from event-week gamma to avoid being the bagholder on a tape bomb, close enough that contango decay is still doing real work.

What it means for your trading

Sell the slope, not the spot - work the 30-45 DTE pocket where Steep Contango still pays carry without parking premium under the headline tail.

Trading readVIX9D under VIX under VIX3M under VIX6M is textbook contango - the vol carry trade is paid, but the slope between front and 3-month is structural risk premium for headline-driven moves, not free money.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 14.1% sits meaningfully rich to HV20 at 9.91, leaving VRP active at 4.19% - options are paying premium that recent tape has not earned. Realized is decelerating, not accelerating: HV60 at 14.77 trades above HV20, confirming the cooling impulse rather than a brewing expansion. Short-premium structures get paid here, but the cushion is the carry, not directional conviction.

With regime positive_gamma intact and term structure in Contango, the harvest sits cleanly in the 30-45 DTE band where carry compounds without sitting at the headline-exposed front week. Index VRP runs richer than constituents on average - sell SPX/SPY vol over single names, and let dispersion alpha live on the long-vol side via top movers like META. Tail-hedge cost remains justified given Iran/crude headline risk; pay for it with spreads, not naked wings.

What it means for your trading

Implieds rich, realized cooling - VRP at 4.19% is the trade, harvested in the 30-45 DTE band via defined-risk structures rather than naked premium.

Skew Convexity

The quarter-delta wing tells the cleaner story than the ATM print: put IV at 15.94% sits well above call IV at 13.86% against an ATM of 13.97%, leaving skew at 2.08% and a smile ratio of 1.15%. Left tail is bid, right tail is asleep - the surface is paying you to underwrite upside and charging you to own downside.

Translation for structure selection: the call wing is flat enough that selling upside vol is a clean carry trade against the Positive Gamma backdrop and Contango term structure, but naked long puts overpay the wing premium that skew is signaling. Express downside convexity through put spreads - finance the rich wing by selling the further-out strike - rather than paying the full smile.

Net: skew geometry favors iron condors with the call side doing the heavy lifting on credit, and any directional hedge built as a defined-risk put spread, not a naked wing.

What it means for your trading

Quarter-delta skew of 2.08% and smile ratio 1.15% confirm a bid left tail and flat call wing - sell upside vol cleanly, but structure downside as put spreads to avoid paying the wing premium.

Vol-of-Vol Structure

VVIX prints 96.37 against spot VIX at 17.81 - the ratio sits squarely in the Normal zone, with no bimodal crush-or-spike premium embedded in the convexity surface. Translation: the vol-of-vol tape is not pricing a regime break, and short-premium structures get the green light at Standard Size.

That said, VVIX is the live dial, not a static read. With Iran-headline tail risk and crude pressure still in the background, a sudden bid in VVIX is the leading tell before VIX itself moves - and before dealer gamma flips supportive-to-amplifying around 745.77. Deploy iron condors in the 30-45 DTE window with full size today, but pre-commit to halving short-vol exposure if VVIX punches above the upper-normal band.

What it means for your trading

VVIX at 96.37 vs VIX 17.81 reads Normal - convexity not bid, sizing stays standard. Treat VVIX as the real-time tripwire: a sharp pop is the cue to halve short-vol exposure before VIX even moves.

Dispersion Spread

Index vol is paid but 14.1% sits below 23.29% - tech dispersion is live, and single-name IV is doing work the index tape isn't capturing. Correlation reads moderate, which means index hedges leak idiosyncratic risk: the dispersion premium has migrated into the constituents, not the wrapper. Sell SPY/SPX vol against single-name vol - the index VRP at 4.19% is the richer pocket while the single names carry the realized noise.

The top GEX mover today is META, with AMZN shifting the other way - that split is the dispersion alpha in plain sight. Cross-asset regime is Aligned across SPY/QQQ/IWM in positive_gamma, so the index complex moves as one and the edge is in the names underneath, not the rotation between indices.

Structure: iron condors on SPY/SPX in the 30-45 DTE band capture the index VRP cleanly; single-name strangles overpay for vol the index isn't pricing. Lean index-short, single-name-flat.

What it means for your trading

Index VRP at 4.19% is richer than the dispersion-bleeding single-name complex - sell SPY/SPX iron condors in the 30-45 DTE window and let the constituents carry their own idiosyncratic risk.

Liquidity & Microstructure

The strike book brackets spot tightly: call wall at 751.00 caps the upside drift while the put wall at 738.00 anchors the downside, with top-strike GEX concentration at 739.00 carrying $7.56B of dealer inventory - a magnet dense enough to dampen any directional impulse that lacks a catalyst.

Spot sits just above the gamma flip at 745.77, and that proximity is the entire story. Spot-above-flip status (True) keeps dealer hedging supportive - buying dips, selling rips inside the 738.00 - 751.00 channel. Lose flip and the polarity inverts: dealers sell weakness, and the cushion becomes the accelerant.

Ignore the headline OI print at 530 - that's stale LEAP residue, not today's pin. The live battleground is the flip-to-call-wall corridor, and the line in the sand is 745.77.

What it means for your trading

Microstructure is constructive but thin: with spot only marginally above 745.77 and dealer GEX clustered at 739.00, mean-reversion holds inside the 738.00 - 751.00 channel - but a clean break of the flip flips dealer flow from supportive to amplifying.

Trading readMassive call-side GEX concentrates around 739.00 acting as a dealer magnet and dampener for upside drift, while put wall at 738.00 bracketing the downside - fade strength into the call wall, avoid chasing breakouts until spot clears the dense supply zone.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks are telling two stories at once. Net VEX prints at -$79.47B - deeply negative - which means any uptick in implied vol forces dealers to sell delta into weakness, the classic downside accelerant. Net CHEX runs positive at $201.4M, so charm decay is mechanically lifting dealer delta as the day burns, a supportive bid that typically firms the tape into the close.

The line in the sand is the charm pivot at 745.7705445897, coincident with the gamma flip. Spot holds above it, so current bias reads Supportive - dealers absorb dips, fade rips. Lose the pivot and the vanna pipe lights up: a coincident VIX bid flips the supportive flow into amplifying flow, and the cushion becomes the catalyst.

Trade it as conditional regime: positive_gamma above pivot, mean-revert; below pivot, respect the vanna asymmetry and stand aside.

What it means for your trading

Charm is the friend into the close, vanna is the enemy on any vol spike - and the entire stance hinges on spot holding 745.7705445897.

Cross-Asset Confirmation

Rates vol is asleep: MOVE at 70.24 shows no credit stress and no macro panic bleeding through the fixed-income complex. That matters because every meaningful equity regime break of the last cycle was prefigured by a rates-vol bid - its absence here tells you the Iran headlines and crude tape are a headline tail, not a confirmed shock. Trade the equity book accordingly: respect the geopolitical convexity, but do not pay for a macro hedge the bond market isn't pricing.

The equity complex is cohesive. QQQ at 720.93 and IWM at 285.00 sit alongside SPY in Positive Gamma, with cross-asset tone flagged Aligned and divergence reading False. No index is leading a break; alpha lives in single-name dispersion, not rotation.

The wrinkle: Fear & Greed at 66 (Greed) is the contrarian caution flag - sentiment is leaning crowded long into a geopolitical tail. Hold the iron condor thesis, but keep tail hedges live via spreads.

What it means for your trading

Rates and credit refuse to confirm a regime break - MOVE at 70.24 alongside aligned positive_gamma across SPY/QQQ/IWM keeps the equity complex cohesive. Iran/crude is the asymmetric tail, and Greed sentiment argues for defined-risk structures over chasing.

Scenario EV

Structure of the day is the Iron Condor, scoring 68 against a put-spread alternative at 58. Positive gamma above the flip at 745.77, term structure in Contango, and VVIX sitting Normal at 96.37 form the tripod - premium is paid, vol-of-vol is not flashing, and dealers are supportive into close.

Deploy in the 30-45 DTE window. Front-end carry is real but headline-exposed; the belly of the curve harvests the contango slope from 15.80 through 21.21 without sitting on top of Iran tape risk. VRP read is Unknown, but ATM IV at 14.1% against HV20 at 9.91 tells you premium is rich to realized.

Iron condor over strangles for one reason: defined risk. Iran headlines and crude pressure are the asymmetric tail; wings are cheap insurance against the spike that flips dealers from supportive to amplifying at 745.7705445897. Standard size - VVIX gives the green light, but discipline holds.

What it means for your trading

Iron condor in the 30-45 DTE band is the highest-EV trade with score 68 - contango plus normal VVIX plus positive gamma is the textbook short-premium tripod. Defined wings, standard size, and respect 745.7705445897 as the line where the thesis breaks.

Actionable Summary

Trade:Iron Condor in the 30-45 DTE band, standard size. Positive gamma across SPY/QQQ/IWM, VIX term structure in Contango, and an active VRP at 4.19% stack the carry in favor of defined-risk premium sellers. VVIX at 96.37 sits in normal range - no jump premium tax on sizing.

Avoid naked long puts: 25-delta skew at 2.08% is paying up, so wing protection comes via put spreads, not outright. Avoid front-week short premium into the Iran headline tail - VIX9D at 15.80 is suppressed but a single tape-bomb re-rates the entire front end.

Watch745.7705445897 - the gamma flip is the regime-break line. Above it, dealers stay supportive into the 751.00 call wall; below, they flip from cushion to accelerant with net VEX at -$79.47B. Regime Elevated / Watchful: sticky, mean-revert within.

What it means for your trading

Highest-EV trade is a Iron Condor in 30-45 DTE - collect VRP under Elevated / Watchful conditions, hedge tail with put spreads, and treat 745.7705445897 as the hard line where dealer flow flips amplifying.

Bessent's disinflation call paired with Warsh at the Fed reshapes rate-path expectations - a dovish lean would compress vol risk premium and accelerate the contango carry trade

Sinking of a cargo vessel off Oman escalates the Iran-conflict tail risk - crude vol and tanker insurance pressure feed back into equity vol via energy/staples sectors

White House scrambling for gas-price relief signals the political pain threshold is being hit - any unilateral SPR release or production push would dampen the energy-led vol bid

A vessel seized off Fujairah heading toward Iranian waters is exactly the kind of incremental escalation that pulls front-end VIX from suppressed to bid - watch VIX9D specifically

Xi's 'open wider' messaging to Musk/Cook/Huang is a tactical de-escalation signal that supports mega-cap tech multiples and explains positive GEX shifts in META/GOOGL/TSLA

Crude markets pricing in a Xi-Trump summit as an Iran circuit-breaker - if the summit disappoints, energy vol re-prices and feeds through to equity skew within days

Cisco's AI 'supercycle' call and 14% rip is the macro confirmation that AI infrastructure capex is intact - this underwrites the bid in semis (AMD, AVGO) and mega-cap tech

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.82 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 745.77 against a spot of 748.22. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.1% with a volatility risk premium of 4.19%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.81. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime