Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

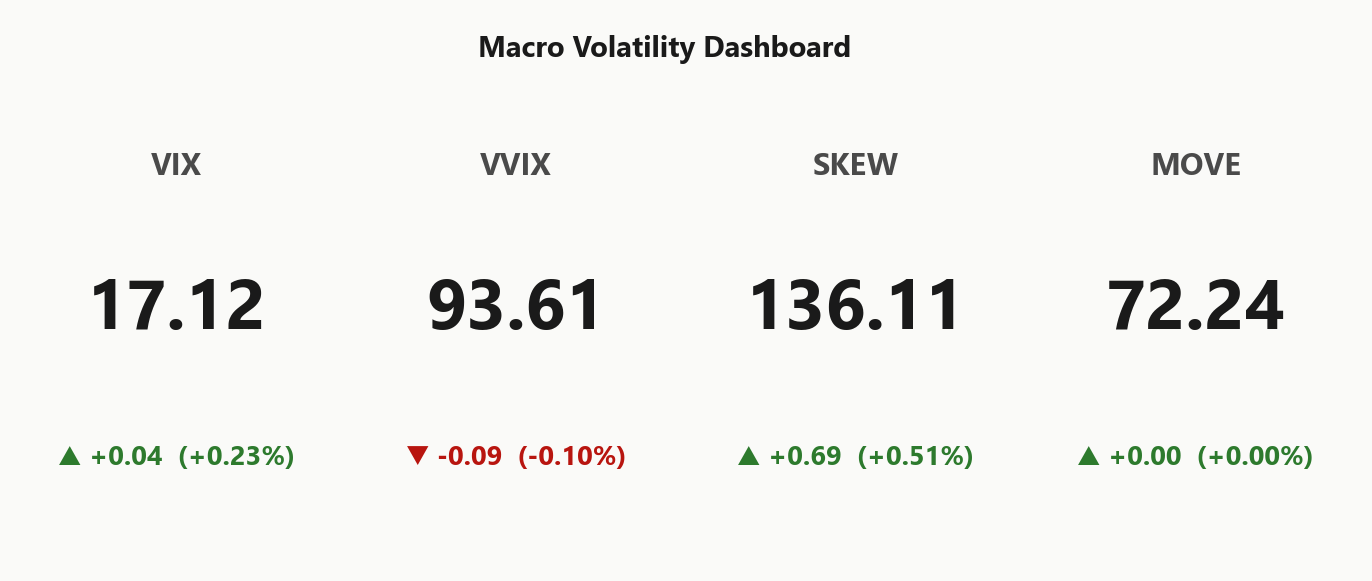

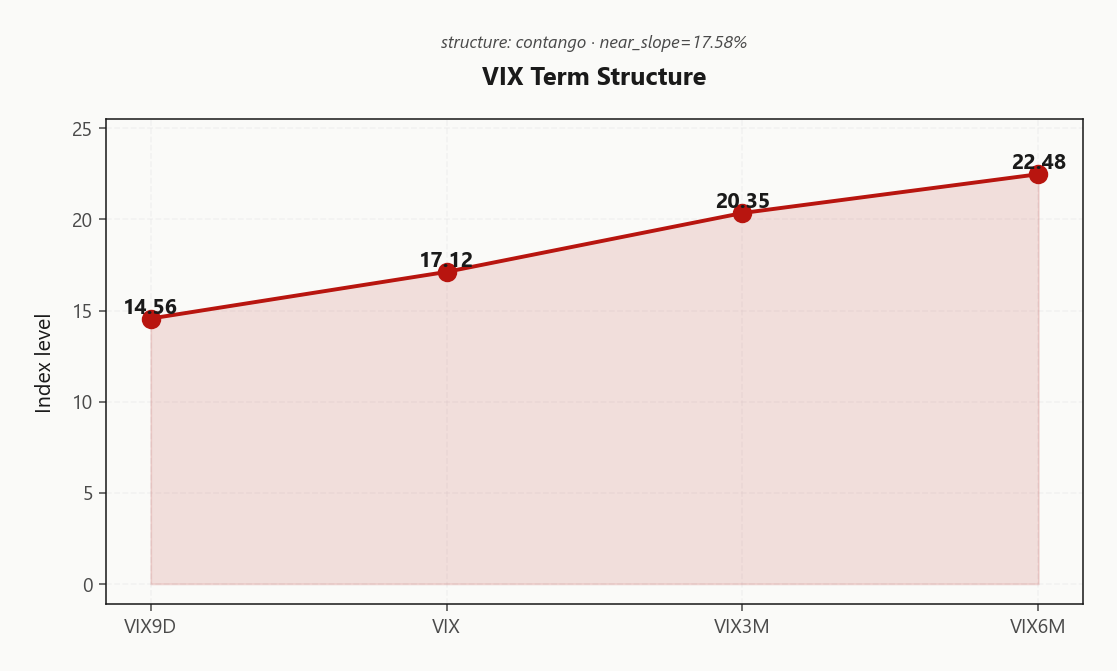

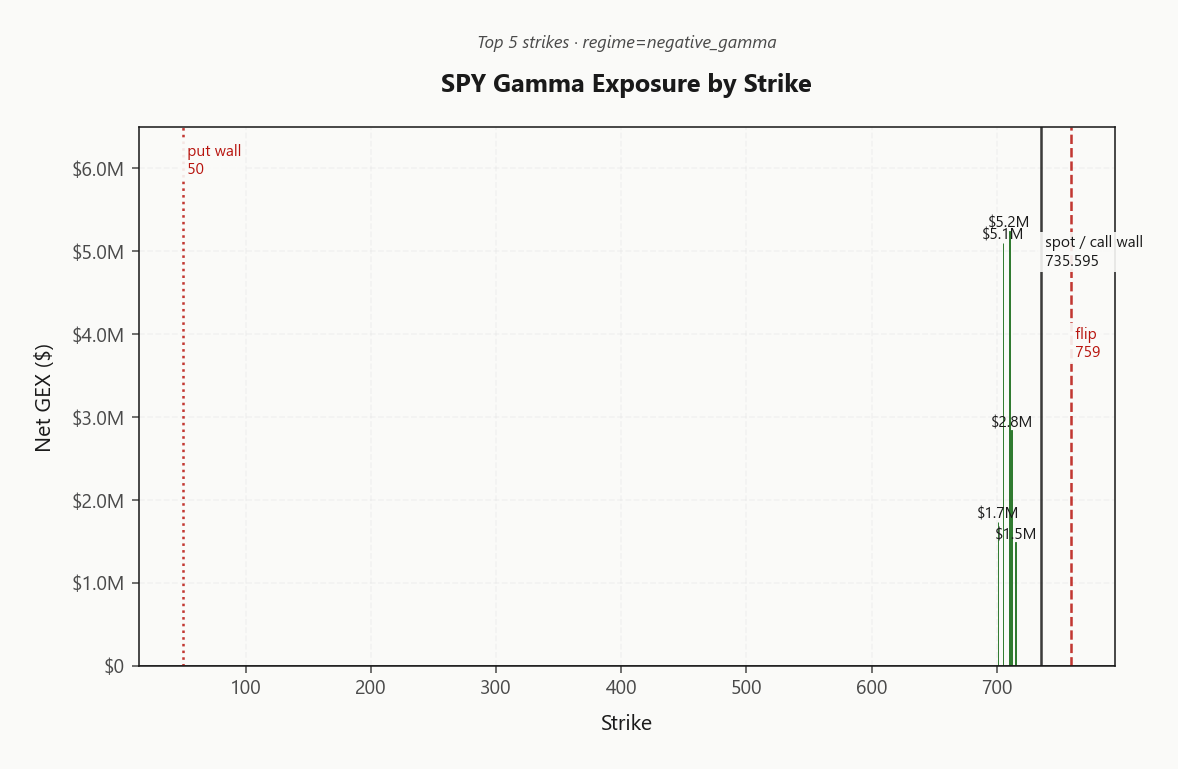

SPY at 735.19 sits in Negative Gamma with net GEX at $30.7M - dealers short, moves amplified, but spot is pinned right under the 736.00 call wall with the gamma flip overhead at 759.00. Key levels: call wall 736.00 acts as the magnet/cap, top OI cluster sits at 705, and the charm pivot at 736 (0.1101756009% away) flips dealer flow direction. Dealer vanna sits at -$299.7M and charm at -$303.4K - modestly hostile if vol expands, neutral otherwise. Vol read: VIX 17.12 with VIX9D 14.56 and VIX3M 20.35 - steep contango (17.58%% slope), VRP at 2.62% live, VVIX benign at 93.61. QQQ and IWM are in Positive Gamma above their flips - that's where the cushion is. Bottom line: structure of the day is Iron Condor in the 30-45 DTE window - sell premium against the QQQ/IWM long-gamma layer, but trim SPY exposure into 736.00 given negative-gamma whip risk.

Steep contango with SPY short-gamma below 736.00 - index complex split between QQQ/IWM cushions and SPY pin risk

SPY trades in negative gamma at 735.19 pinned just under the 736.00 call wall, while QQQ and IWM sit comfortably above their gamma flips with dealer cushion intact. VIX term structure is steeply in contango at 17.58%% near-slope, VVIX/VIX ratio benign, and Fear & Greed reads Greed - a constructive vol-selling backdrop interrupted only by lingering Mideast tape risk. The divergence between SPY's short-gamma posture and QQQ/IWM's long-gamma stability is today's lead story.

Regime Assessment

Regime read: Elevated / Watchful. VIX at 17.12 sits in the watchful zone - elevated enough to keep hedgers paying up, calm enough to keep the contango carry intact. The transition matrix says probability of escalating to panic over the next five sessions is only 0.05, while the odds of decaying back into the low regime over ten sessions run 0.45 - the base case is drift lower, not blow-out higher.

The number that matters most is half-life: 15 sessions. That's a sticky regime, not a knife-edge. Vol spikes in this state get faded, not chased - they mean-revert before they compound. The implication is straightforward: keep selling premium into the steep contango, but size the carry to survive a single bad print rather than scaling for a directional vol-down trade.

Cross-asset confirms - MOVE benign, divergence reads Qqq Heavier, and Fear & Greed at Greed - but with SKEW bid at 136.11, this is sticky, not sleepy. Fade spikes; respect the tape.

What it means for your trading

Regime is Elevated / Watchful with VIX at 17.12, half-life 15 sessions and panic-transition probability only 0.05 - fade vol spikes into the contango, don't chase them.

Trading readVIX, VVIX, MOVE all calm-to-normal but SKEW is elevated at 136.11 - the four indicators aren't fully aligned. The tail bid in SKEW is the divergence to watch; usually it's an early-warning before VIX moves.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The curve prints a clean contango stack: 14.56 on VIX9D rolling under spot VIX at 17.12, ladder up through VIX3M at 20.35 and VIX6M at 22.48. Near-slope at 17.58%% stamps the structure as Contango - no event premium being underwritten in the front tenors, which is exactly the curve shape that pays vol sellers and punishes anyone reaching for tail.

Forward 30→60 vol resolves to 21.7861550073, with the 60→90 segment extending higher still - carry is intact and the slope hasn't been arbitraged flat. The regime label reads Steep Contango, qualified as Steep contango - vol sellers favored. Translation: the curve is doing the work, theta is the alpha source, and the front belly is where the geometry concentrates.

The actionable edge sits in the 30-45 DTE window - steepest slope, fastest decay, cleanest distance from the 0DTE pin noise. Sell the belly, finance the wing, respect the curve while it's offering you this much premium relative to realized.

What it means for your trading

Curve geometry is unambiguously vol-seller carry - Steep contango - vol sellers favored with near-slope at 17.58%%. Concentrate premium-selling in the 30-45 DTE belly where slope and theta compound.

Trading readSteep contango with near-slope at 17.58%% - vol-carry trade is fully greenlit by the curve. The catch: contango this clean is also what fails fastest when a tape shock hits, so size the carry to survive a single bad print.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV carries a clean premium over realized across the index complex. SPY prints 12.92% against HV20 of 10.3, leaving live VRP at 2.62% - genuinely harvestable, not a chase. The deceleration tell is HV60 at 15.04 sitting above HV20 - recent tape has been calming, which is exactly when options pricing looks rich relative to what the market is actually delivering.

Across the triad, QQQ wears the widest premium with VRP at 4.79% - richest of the core three and the cleanest home for a premium-selling tilt. IWM at 3.37% backs the same conclusion with a small-cap beta kicker. SPY's narrower spread reflects pin-risk drag, not absent edge.

Read: this is cheap-to-sell territory, not chase-vol territory. Stack the carry on the QQQ/IWM long-gamma cushion where dealers dampen rather than amplify, and let realized's deceleration do the work into theta.

What it means for your trading

VRP is alive across the index complex with QQQ richest at 4.79% and SPY clean at 2.62% versus HV20 of 10.3 - premium-selling carry, not vol-chasing, is the harvestable trade.

Skew Convexity

Quarter-delta put skew is bid across the index complex and the asymmetry is doing the talking. SPY prints a 2.84% skew with smile ratio at 1.33% - downside vol pays up while the call wing trades cheap. Put quarter-delta IV at 11.58% against call quarter-delta at 8.74% versus ATM at 10.14% is a textbook ordered-hedging signature, not a panic bid.

QQQ leads the steepening at 3.38% - the richest of the triad and consistent with mega-cap downside demand sitting underneath the long-gamma cushion. IWM rounds the read at 2.61%. The smile shape is uniform: puts paying, calls muted, no convexity bid on the upside.

Trade implication: harvest the skew via put-spreads rather than naked wings - the upper strike finances the convexity cap and you collect the steep end without warehousing tail. Call-side credit is thin enough that any short-call structure should sit anchored to the 736.00 magnet, not stretched for premium.

What it means for your trading

Quarter-delta put skew at 2.84% on SPY and 3.38% on QQQ reflects ordered hedging demand rather than panic - collect the asymmetry through put-spreads, not naked puts, and treat call-side premium as too thin to chase.

Vol-of-Vol Structure

VVIX prints 93.61 against VIX 17.12 - squarely Normal territory with the ratio at 5.47. No bimodal jump premium is being priced; the vol-of-vol surface refuses to flag tail anxiety even with Mideast tape risk live. Sizing guidance: Standard Size - no defensive haircut required to harvest the carry.

The lone dissonance is SKEW at 136.11, holding an elevated bid that betrays chronic crash-hedging demand even as VVIX yawns. That divergence is structural, not panic - ordered tail buying against a calm spot vol regime, consistent with the steep 2.84% 25-delta put skew and a benign 72.24 MOVE print.

Net: greenlight standard-size premium harvest in the 30-45 belly. VVIX isn't telling you to half-size; SKEW is telling you to keep wings, not strangle naked. Iron condor over short-strangle, full clip.

What it means for your trading

Vol-of-vol is benign at 93.61 with the ratio 5.47 - no jump premium, full-size carry greenlit - but elevated SKEW at 136.11 argues for defined-risk wings over naked premium.

Dispersion Spread

Dispersion is alive under a calm index tape. SPY ATM at 12.92% sits well below QQQ at 19.18% and IWM at 20.51% - the index spread is compressed while single-stock vol across the mega-cap movers runs visibly hotter than the headline. Idiosyncratic risk is concentrating in names, not in the tape, and the AAPL/TSLA/AMZN/GOOGL/MSFT GEX rebuild is doing the lifting on the QQQ surface.

That asymmetry rewires the hedge calculus. With index ATM this rich-to-realized and the cross-asset read Qqq Heavier, index puts are an inefficient sleeve against single-name event risk - they price the tape, not the dispersion. Harvest the index VRP where it's cleanest: 19.18% over realized via the recommended Iron Condor, leaning on the QQQ/IWM long-gamma cushion.

On single-name vol, stay a buyer or stand aside - naked short single-stock premium into a dispersion regime is the worst expression of the same view that works at the index level.

What it means for your trading

Index spread between SPY 12.92% and QQQ 19.18% compressed while single-stock vol runs hot - sell index vol via Iron Condor, leave single-name premium alone or own it selectively.

Liquidity & Microstructure

SPY trades in Negative Gamma with the gamma flip overhead at 759.00, leaving dealers in amplifier mode below the line. The 736.00 call wall and the 705 OI cluster form a stacked magnet/cap above spot - the top strike at 710.00 alone carries $5.2M of net GEX, anchoring the tape. Reclaim of 736.00 is the dealer-flow flip line: above it, hedging dampens; below, it whips.

QQQ sits comfortably above its flip at 694.11 and IWM mirrors the cushion - that is where the long-gamma stabilizer lives today, and where premium-selling carry compounds cleanly. The 50.00 put wall is structurally distant; downside risk is all about the negative-gamma layer, not a wall break.

Intraday driver is unambiguous: 85.5% of SPY gamma sits in 0DTE, so pin behavior around 736.00 dictates whether the tape chops or trends into the bell.

What it means for your trading

Lean QQQ/IWM long-gamma cushion for premium harvest; trim SPY exposure into 736.00 until spot reclaims 759.00 and dealer flow flips from amplifier to dampener.

Trading readSPY's GEX layout shows a wall of positive call gamma stacking from the highest-OI strike up into the call wall - that's a magnet/cap, not a launchpad. Trade is to fade strength into 736.00 and respect the negative-gamma layer below the flip.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer vanna sits firmly negative across the index complex - SPY net VEX at -$299.7M and QQQ at -$190.24B point the same way: a vol expansion forces dealers to sell delta into weakness, an accelerant rather than a stabilizer. Charm is the smaller cousin but rhymes - SPY net CHEX at -$303.4K bleeds modestly unsupportive into the close, no rescue from time decay.

The single line that matters is the charm pivot at 736, doubling as the Call Wall and currently 0.1101756009 away. Bias reads Neutral here, but that label is knife-edge: a break below flips dealer flow from passive to amplifying, and a reclaim of 736.00 is what converts the same greeks from headwind to tailwind.

Watch the call wall - it is the inflection where vanna stops biting and charm stops leaking. Until then, treat any vol uptick as a self-reinforcing move, not a fade.

What it means for your trading

Negative vanna and unsupportive charm mean a vol expansion gets amplified, not absorbed - the 736 pivot is the dealer-flow inflection that decides whether today's tape pins or unwinds.

Cross-Asset Confirmation

Cross-asset tape is not flagging stress - MOVE prints at 72.24 with bond vol unchanged, credit spreads quiet, and Fear & Greed reading Greed at 67. This is the signature of an isolated equity-tape pin, not a macro shock bleeding through the system.

The cushion lives outside SPY: QQQ at 702.51 sits cleanly above its gamma flip at 694.11, and IWM at 282.77 holds above 279.23 - both in positive_gamma with dealer flow stabilizing. SPY is the lone soft spot below its flip, making the divergence read Qqq Heavier.

Iran tape risk lingers but is not bleeding into rates or credit - the carry trade keeps its license until that changes. Watch MOVE and the QQQ/IWM flip lines as the early-warning set; if those crack first, the contango sell stops working.

What it means for your trading

Calm cross-asset backdrop - MOVE at 72.24 and Fear & Greed in Greed - confirms SPY's negative-gamma posture is idiosyncratic, not systemic. Stay structurally short vol against the QQQ/IWM long-gamma cushion until either MOVE reprices or QQQ loses 694.11.

Scenario EV

Structure of the day: Iron Condor in the 30-45 DTE belly, scoring 60 against a put-spread alternative at 50. The carry case is clean: VRP live at 2.62%, term structure in Contango with near-slope at 17.58%, and VVIX benign at 93.61 - no bimodal jump-risk premium to defend against, sizing guidance reads Standard Size.

Iron condor wins over short-strangle because 2.84% put skew makes the downside wing pricing-efficient - collect the convexity, cap the tail. Anchor the short put wing under 50.00 and the short call wing into 736.00, leaning the structure on QQQ/IWM's Positive Gamma cushion above their flips rather than SPY's Negative Gamma layer where whip risk lives.

QQQ carries the richest VRP at 4.79% - that's where the cleanest condor sits. Iron condor scores 60; put-spread 50. Trim SPY exposure into 736.00, respect the charm pivot at 736, and let theta do the work.

Structure of the day: Iron Condor in the 30-45 DTE belly, anchored on the QQQ/IWM long-gamma cushion where dealer flow mean-reverts. SPY sits in Negative Gamma below its flip at 759.00, so trim directional exposure into the 736.00 call wall and only flip constructive once spot reclaims the flip. QQQ above 694.11 and IWM above 279.23 are where premium-selling carries cleanly.

The charm pivot at 736 is the bias-flip line - current read Neutral, distance 0.1101756009. Iran tape risk is the live exogenous - micro-hedge with a cheap put-spread, do not size up. Regime reads Elevated / Watchful with half-life 15 sessions: sticky, fade vol spikes rather than chase. Avoid naked single-name vol selling - dispersion is alive.

What it means for your trading

Sell the Iron Condor on QQQ/IWM in 30-45 DTE; treat SPY as pin-risk territory until spot reclaims 759.00 and respect 736.00 as the dealer-flow inflection.

Dollar weakening despite US-Iran clashes is a tell - markets are treating the conflict as containable, which supports the contango/vol-sell setup but also primes a sharp reversal if the read flips.

Wall Street week-ahead framing - US-China meeting plus Iran plus data trifecta means event premium will come back into the curve as we approach the window.

Toyota's $4.3B Iran-war hit is the first hard corporate guidance damage - if more multinationals echo this, single-stock vol stays bid even with index VIX calm.

Mideast peace breakout scenario list matters because the market is implicitly priced for status-quo - any peace headline forces a fast cross-asset rotation.

Trump's ceasefire-still-holds framing is the headline that's been keeping VIX contained - every flare-up is a cliff-edge for the contango trade.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 16.94 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in Negative Gamma gamma with net dealer GEX at $30.7M. The gamma flip sits at 759.00, with the call wall at 736.00 and the put wall at 50.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 759.00 against a spot of 735.19. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.92% with a volatility risk premium of 2.62%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.12. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime