Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

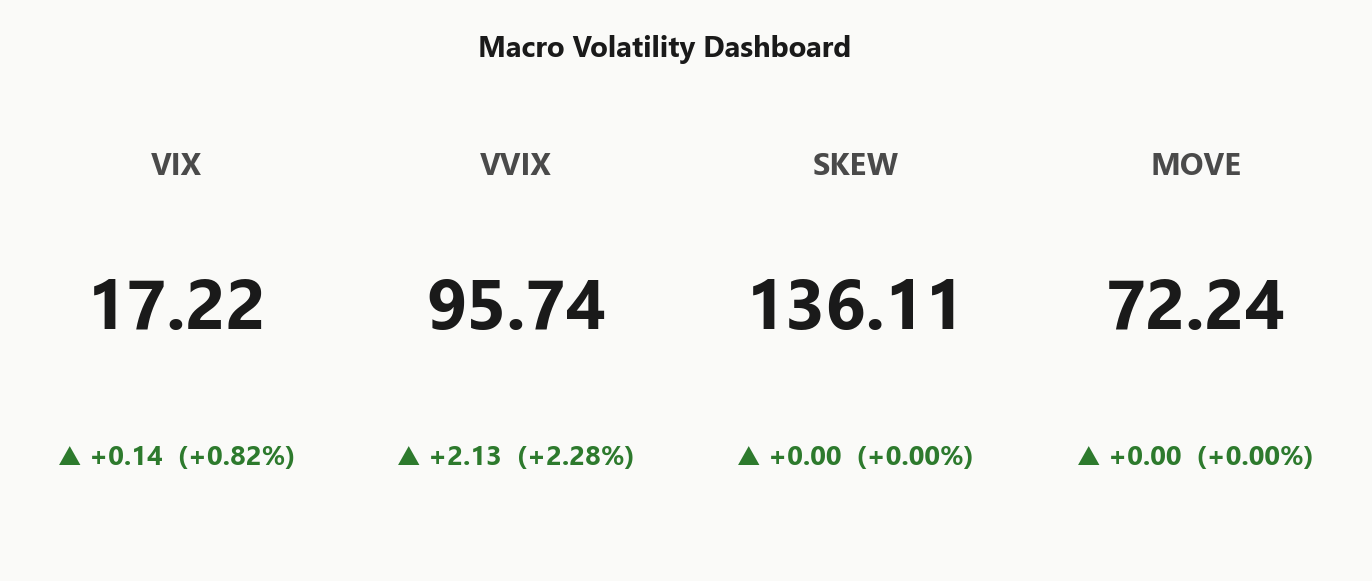

SPY at 737.54 in Positive Gamma with net GEX $10.28B - dealers long gamma, moves dampened. Call wall stacks at 740.00 (sticky resistance), put wall at 710.00, gamma flip at 710.99 sitting well below spot - that's a deep cushion. Dealer vanna -$304.4B means vol up triggers delta selling - downside accelerant if VIX spikes; charm -$15.7M skews dealers as sellers into close. VIX at 17.22 with VIX9D 14.93 below VIX3M 20.47 = Contango, slope 15.34%% - carry is paid. VRP 2.71% with VVIX 95.74 (Normal) - sell premium at standard size, optimal DTE 30-45. Bottom line: Iron Condor between put wall and call wall is the trade; IWM negative GEX is the canary - watch 279.18.

Positive gamma cushion across index complex; VIX at 17.22 with steep contango favors vol sellers

SPY at 737.54 sits above gamma flip 710.99 with dealers long gamma - moves get dampened, mean reversion wins. VIX term structure in Contango with VVIX at 95.74 keeps vol sellers paid, but Iran tape risk and elevated regime label warrant tail hedges. IWM is the fragile sister - net GEX flipped -$146.6M with spot just above flip 279.18.

Regime Assessment

Regime tag prints Elevated / Watchful with VIX anchored at 17.22 - sticky enough to harvest, not so quiet that you stop paying for tails. Transition probability to panic over five sessions sits at 0.05: small, non-zero, and exactly the slice the Iran tape can light. The mirror leg - drift back to low-vol over ten sessions - runs 0.45, which makes the grind the base case.

Half-life of 15 sessions is the operative number. That horizon validates carrying short premium at the recommended 30-45 window while keeping a long-dated tail on. Cross-asset reads Aligned at the index level, but IWM's net GEX at -$146.6M is the dissent - that's where regime-break risk shows first, well before SPY's flip at 710.99 comes into play.

Trade the regime, hedge the label. Carry the Iron Condor; don't lever it.

What it means for your trading

Regime is Elevated / Watchful with half-life 15 sessions and panic probability 0.05 - sticky enough to sell premium, watchful enough to keep tails on.

Trading readVIX modest, VVIX normal, SKEW elevated, MOVE benign - three of four confirm calm, only SKEW flags tail demand. That's a contained regime with one quiet hedge bid, not a confirmed risk-off setup.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

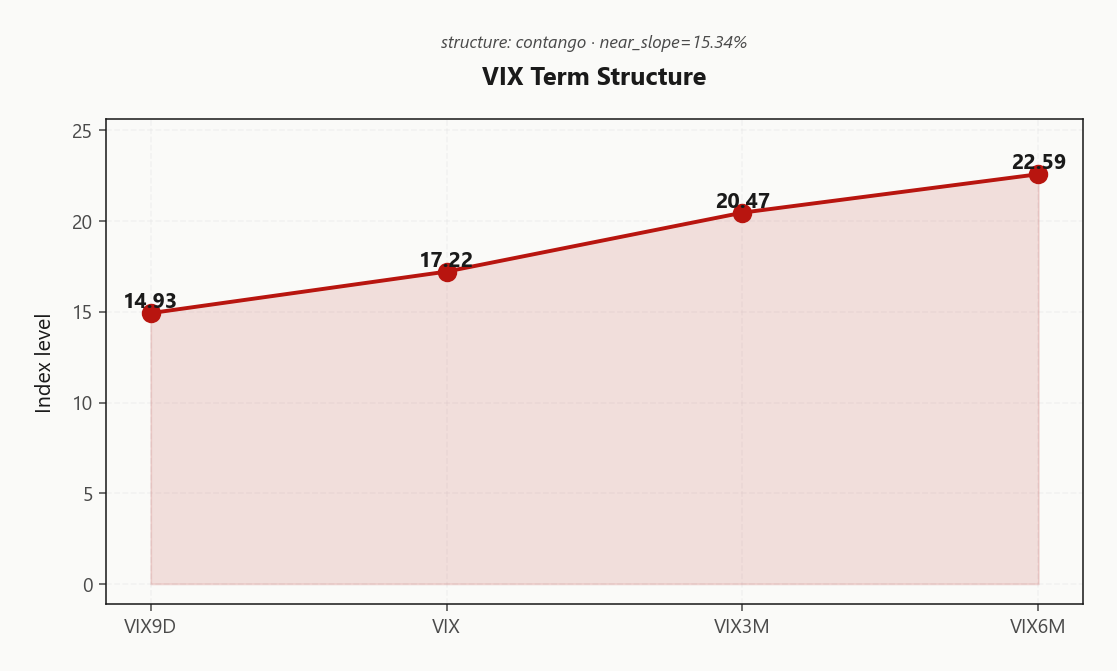

The VIX curve prints a textbook Contango stack: 14.93 on the front, 17.22 spot, 20.47 three-month, 22.59 six-month - a clean upward slope with near-term roll at 15.34%%. Front is suppressed, back is elevated; the market accepts today's calm and charges for forward stress.

Forward 30-to-60 implied prints 21.9149982888 and 60-to-90 lifts to 24.5274397359 - that mid-twenties forward is where the Iran tape, US-China meeting, and the data calendar are being warehoused. This is Steep contango - vol sellers favored: structural carry, not panic. The curve isn't kinked, it's tilted.

The edge sits at 30-45 DTE where forward implied is richest relative to spot vol. Sell the belly, hedge the wing with longer-dated back-month - calendars and short premium fit the slope. The steepness itself is the warning bell: when forward starts compressing toward spot, the carry is over before the tape tells you.

What it means for your trading

VIX curve in Steep Contango with front 14.93 well under three-month 20.47 - vol sellers favored at 30-45 DTE where forward implied is richest. Watch curve flattening as the early exit signal.

Trading readSteep contango with the front well below the long end says vol carry is paid and the market accepts current calm but charges for forward risk. Short front-month vol, hedged with long back-month, is the clean carry trade.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 13.11% sits materially above HV20 of 10.4 - option buyers are overpaying for a tape that has been cooling, not heating. The IV-RV spread translates directly into 2.71% of VRP, and that's the carry print premium sellers want stamped on the desk.

HV60 at 15.09 running above HV20 confirms the deceleration: recent realized has bled lower while the longer window still carries the ghost of prior tape. That term shape is the structural tell - the gap is widest in the belly of the curve, which is why 30-45 DTE is the structural sweet spot, not the front weeklies.

VRP is active across the term and the regime tag reads Vrp Active. Sell premium with discipline - the spread tells you exactly how many vol points you're being paid to underwrite this regime, and at this gap the Iron Condor is the cleanest expression.

What it means for your trading

VRP active with ATM IV at 13.11% versus HV20 at 10.4 - short premium is the carry, sized to the IV-RV gap. HV60 above HV20 says realized is decelerating, which means the rich implied is regime-pricing not catch-up - sell the 30-45 DTE belly.

Skew Convexity

The smile is doing exactly what an orderly hedging tape looks like: put quarter-delta IV at 10.65% sits materially above call quarter-delta IV at 8.08%, with ATM anchored at 9.08%. That's the left tail being bid, not chased - structural downside hedging from real-money books, not a panic grab.

Smile ratio prints 1.32% with the quarter-delta skew at 2.57% - above one, but nowhere near a capitulation reading. The call wing is flat: no upside conviction premium being paid, which is the tell that any melt-up into the 740.00 call wall is unhedged at the wing. Right tail is cheap, left tail is rich, and the asymmetry is paid for.

Trade implication is mechanical: put spreads over naked puts. You finance the long leg by selling into a steep, demanded skew rather than paying it outright - the structure monetizes the put bid while keeping defined-risk protection intact. For upside, vertical call structures stay cheap given the flat wing.

What it means for your trading

Skew is steep but ordered - put quarter-delta IV well above call quarter-delta IV with smile ratio at 1.32% reflects hedging demand, not panic. Sell the rich left side via put spreads; the flat call wing leaves upside verticals cheap.

Vol-of-Vol Structure

VVIX prints 95.74 against VIX 17.22, a ratio of 5.56 that sits squarely in the Normal band. No binary jump premium is being priced into the vol surface - the market is paying for direction, not for a regime break. That gives the carry trade clean air.

Sizing guidance follows the read: Standard Size on short premium structures. With VVIX/VIX in standard range there is no bimodal pricing to respect, no convexity demand bleeding into spot vol. The Iron Condor at 30-45 DTE goes on at full clip, not throttled.

The trigger to halve size is a VVIX rip mid-session - that move historically front-runs VIX by minutes, not hours. Watch the VVIX delta tape, not the VIX print. If VVIX breaches the panic shelf while VIX is still near 17.22, that is the early-warning to lift exposure before the underlying repricing shows up in the index.

What it means for your trading

Vol-of-vol benign at Normal with ratio 5.56 - short premium goes on at Standard Size. VVIX is the leading indicator; a sudden expansion is the cue to cut before VIX confirms.

Dispersion Spread

QQQ ATM IV at 20.29% sits materially above SPY ATM IV at 13.11% - single-stock dispersion is alive in tech, and index hedges are underpricing idiosyncratic mover risk. The spread is the tell: QQQ's vol surface is being lifted by names, not by the index itself, with NVDA and AAPL anchoring the gamma rebuild while META and NFLX lean the other way. That cross-current is what dispersion looks like before it shows up in realized.

Preferred trade: short premium in SPY over QQQ. Index correlation is doing more work in SPY - selling vol there harvests the cleaner risk-premium, while QQQ short strangles take direct exposure to single-name catalyst risk that the implied is correctly pricing. IWM ATM IV at 20.22% reinforces the read: small-cap vol is bid for fragility, not dispersion.

Iron condor in SPY between the put wall and call wall captures the dispersion advantage cleanly - defined-risk, index-correlation carry, no idiosyncratic tail. Avoid QQQ short strangles and naked single-name short vol in mega-cap tech; the dispersion premium is there because it should be.

What it means for your trading

Dispersion premium present in tech: QQQ implied at 20.29% above SPY at 13.11% argues for SPY iron condors over QQQ short strangles. Index correlation carries SPY short vol cleanly while QQQ short premium absorbs single-name catalyst risk that's correctly priced.

Liquidity & Microstructure

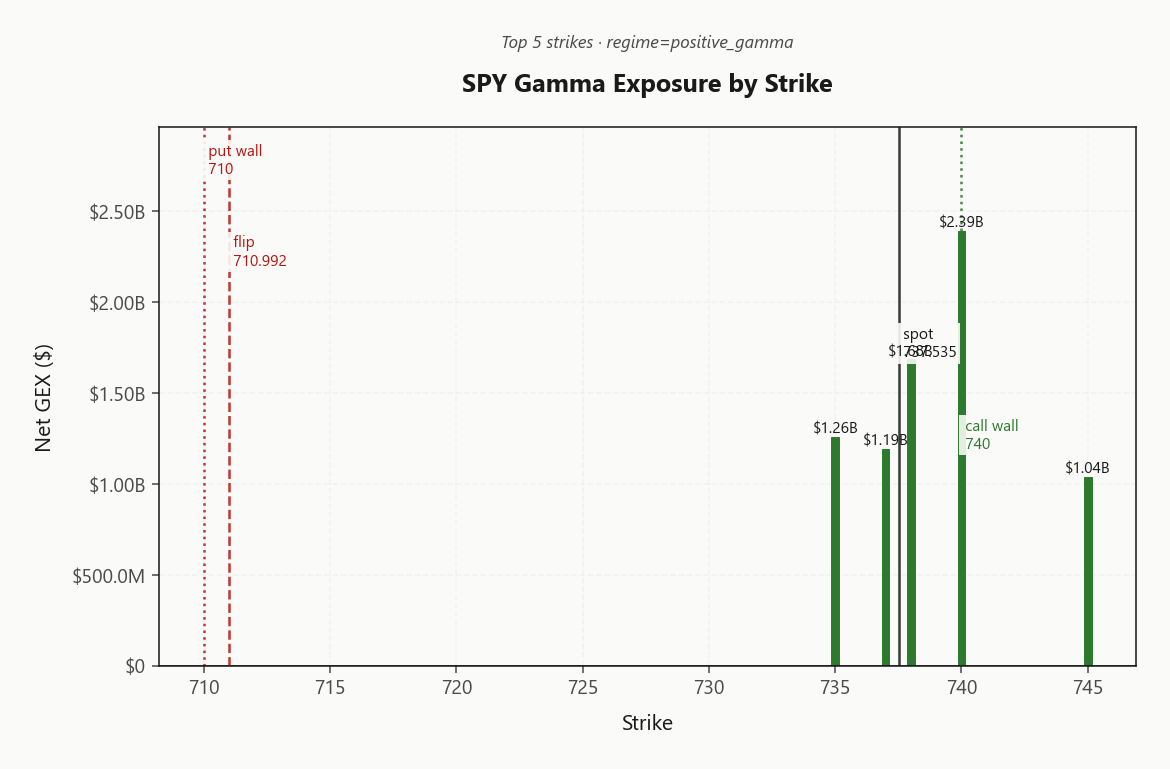

SPY's book is anchored by a dominant call OI cluster at 740.00, where the deepest positive GEX strike sits at 740.00 with $2.39B of dealer length - that's the sticky resistance dealers defend, absorbing pressure on every test. Spot at 737.54 sits well above the gamma flip at 710.99, putting the tape squarely in Positive Gamma: dealer flow buys dips, sells rips, and grinds the range tighter into the close.

Below the put wall at 710.00, the highest-OI strike at 700 is where put hedging lives - the de facto floor where structural protection clusters. Between that floor and the 740.00 ceiling, mean reversion wins; outside it, the profile thins fast.

The single level that flips behavior is 710.99. Above it dealers dampen; below it they amplify. That's the trapdoor - trade the range while it holds, and treat a flip break as the cue to stand down on short premium and re-engage tail hedges.

What it means for your trading

Spot above 710.99 with the call wall stacked at 740.00 defines a mean-reversion regime bounded by the 710.00 floor; a loss of the flip is the only setup that converts dealer flow from dampener to accelerant.

Trading readMassive positive gamma stacked at the call wall and across the upper strikes - dealers cushion rallies into resistance and absorb dips above the gamma flip. Below the flip the profile thins fast, so spot losing the flip flips dealer flow from dampener to amplifier.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

The vanna-charm stack tells a different story than gamma alone. Net VEX prints -$304.4B - deeply negative - which means a vol bid flips dealers into delta sellers. A VIX pop here is not absorbed; it is amplified into spot. That is the asymmetry hiding underneath the positive gamma cushion: calm tape gets dampened, but a vol shock gets accelerated to the downside.

Charm tells the late-tape story. Net CHEX at -$15.7M skews dealers as sellers as the clock bleeds - time decay pushes hedges out, not in. The pivot sits at 740 (Call Wall): above it, dealer flow caps the tape; below it, dealers stabilize and the cushion reasserts. Current bias is Neutral - neither support nor pressure has the wheel.

Trade the divergent stack: harvest the gamma dampener, but keep a long-vol tail on. The cushion is real until it isn't, and vanna decides when.

What it means for your trading

Positive gamma masks a vol-spike accelerant - net VEX at -$304.4B and net CHEX at -$15.7M mean dealers sell delta into a VIX pop and bleed offers into the close. Watch 740 as the dealer-flow pivot; current bias is Neutral.

Cross-Asset Confirmation

Cross-asset tape reads Aligned with no credit-shock signature: MOVE at 72.24 keeps bond vol benign, Fear & Greed prints 67 (Greed), and VIX at 17.22 sits modest against VVIX 95.74. The Iran tape is driving the marginal vol bid, but the suite says geopolitical, not systemic - event-vol with a mean-reverting profile, not regime-vol.

Underneath the calm, IWM is the dissenter. Net GEX has flipped to -$146.6M with spot at 283.66, while SPY at 737.54 and QQQ at 708.61 hold deep positive gamma. That's selective small-cap fragility under index complex calm - not a market-wide warning, but the canary slot is filled.

Trade the divergence: index short premium fits the Unknown tone, but watch the 279.18 flip as the leading indicator. If contagion comes, it breaks small-cap first.

What it means for your trading

Cross-asset confirms geopolitical event-vol over systemic stress - MOVE benign, F&G in Greed, VIX modest. IWM net GEX at -$146.6M is the canary; watch 279.18 for the first sign of break.

Scenario EV

The scoring race resolves cleanly: Iron Condor takes the top slot at 61, ahead of the put-spread alternative. The trifecta is doing the work - VRP active per the IV-HV gap, VVIX Normal at 95.74, and SPY locked in Positive Gamma with spot well above the 710.99 flip. Defined-risk premium between 710.00 and 740.00 is the cleanest expression of dampened tape plus paid carry.

DTE selection is not negotiable: 30-45 sits exactly where the term structure pays the most - VIX9D at 14.93 against VIX3M at 20.47 in Contango with near slope 15.34%%. Sell the call wall and buy above; sell the put wall and buy below. Standard size per Standard Size; halve only if VVIX breaches the panic threshold mid-trade.

What it means for your trading

Iron condor at 30-45 DTE wins the regime - score 61 on positive gamma, active VRP, and Normal vol-of-vol. Watch 279.18 as the cross-asset cancel signal.

Actionable Summary

Bottom line: sell premium with structure. The trade is a Iron Condor at 30-45 DTE, sold between the put wall at 710.00 and the call wall at 740.00. SPY sits in Positive Gamma with net GEX $10.28B, dealers dampening moves while VRP at 2.71% and VVIX at 95.74 (Normal) keep carry paid at standard size.

Watch 710.99 as the trapdoor - losing it flips dealer flow from dampener to amplifier, and negative VEX at -$304.4B turns any VIX pop into a downside accelerant. The dealer-flow pivot is 740 (Call Wall); current bias reads Neutral. IWM is the canary - net GEX at -$146.6M with the flip at 279.18 is the leading tell for index break.

Avoid naked puts - the put quarter-delta skew at 2.57% is rich, use spreads. Skip QQQ short strangles given live tech dispersion. Hedge cheaply with a long-dated VIX call spread or SPY tail put while VVIX prices benign relative to the Elevated / Watchful regime.

Iran tanker seizure in Gulf of Oman is the live geopolitical wire driving the VIX bid - energy supply chain risk feeds straight into ES overnight gaps.

Dollar weakening on Iran resolution hopes is the cross-asset tell that markets are pricing de-escalation, not escalation - risk-on confirmation underneath the noise.

Reuters' peace-scenario asset map is the framework traders need to position the dollar/oil/equity rotation if Iran de-escalates - actionable cross-asset playbook.

Toyota's Iran-war hit telegraphs corporate earnings exposure to the conflict - earnings season risk gets a new dimension beyond rates and demand.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.22 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.99 against a spot of 737.54. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.11% with a volatility risk premium of 2.71%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.22. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime