Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

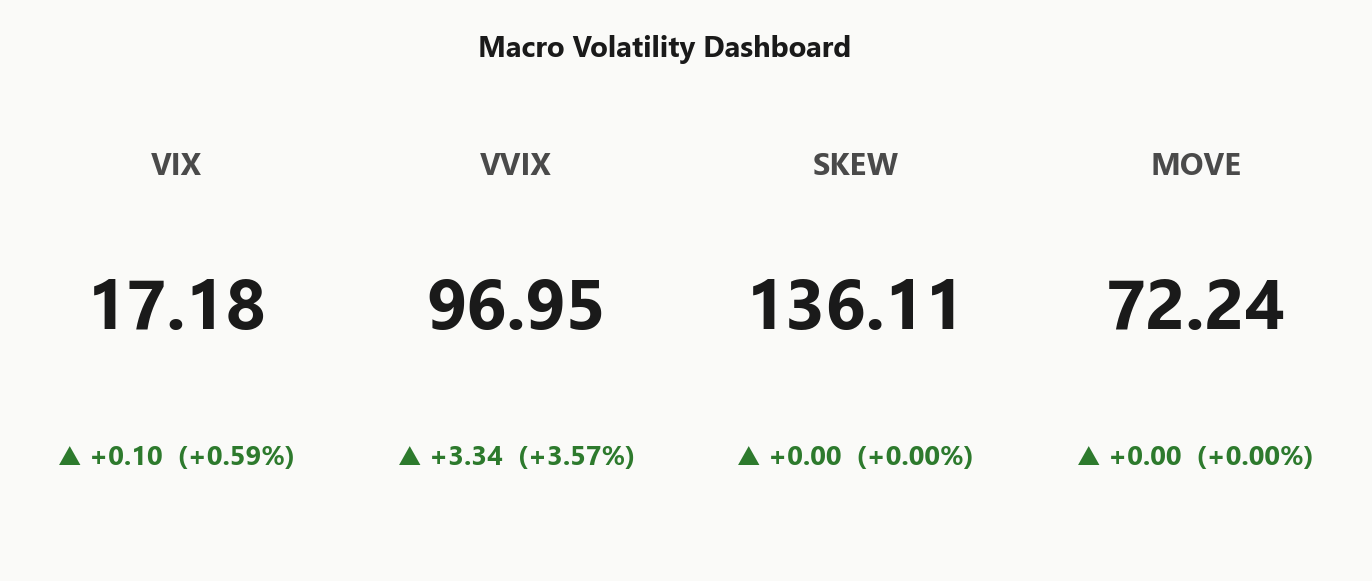

SPY closed at 737.49 in a deep positive-gamma regime, net GEX $12.07B with dealers long gamma - moves dampened, mean-reversion the path of least resistance. Call wall at 738.00 caps upside while put wall 710.00 and gamma flip 710.98 sit far below spot, giving roughly 0.0698319288% headroom of cushion above the inflection. Dealer hedging is supportive: spot down 1% triggers $12.07B of dealer buying, charm pressure is mild, vanna risk only activates if vol spikes hard. VIX at 17.18 with VIX9D at 14.14 and VIX3M at 20.52 = steep contango and rich VRP of 1.59%, but VVIX ticked up 3.57%% - the market is paying up for vol-of-vol quietly. Bottom line: sell premium in 30-45 DTE iron condors anchored on 738.00 and 710.00, fade strength into the wall, and only flip defensive if SPY breaches 710.98.

Positive gamma across index complex with steep VIX contango - vol sellers in control, mean-reversion regime intact

Index complex closes the week locked in positive-gamma mean-reversion mode with SPY at 737.49 parked just below the call wall at 738.00 and well above gamma flip at 710.98. Steep VIX contango (21.5%% slope) and a normal VVIX/VIX ratio give vol sellers structural carry, though VVIX ticked up 3.57%% - a quiet bid for tail convexity worth noting. Cross-asset is aligned, no regime divergence between SPY and QQQ, leaving the actionable trade as iron condors in the 30-45 DTE window.

Regime Assessment

Regime reads Elevated / Watchful with VIX anchored at 17.18 - the yellow light, not the red one. Transition probabilities tell the whole story: only 0.05 odds of escalating to panic over the next five sessions, while the path lower carries 0.45 probability of dropping into the low-vol bucket inside ten. Asymmetry favors normalization, but the door is not slammed shut.

Half-life of 15 sessions makes this regime sticky - don't expect a clean break in either direction. That stickiness is what underwrites the carry trade: contango keeps paying, VRP stays harvestable, and dealer positioning has time to entrench. The watchful posture is a sizing instruction, not a directional one.

Trade the regime you have, not the one you fear. Run standard size on premium-harvest structures, keep tail hedges cheap and standing, and let the deterioration come to you before pre-empting it. The yellow flag earns its keep only if VIX stops behaving - until then, sticky-elevated is a feature, not a bug.

What it means for your trading

Regime is Elevated / Watchful with sticky 15-session half-life and skewed transition odds - short-vol carry remains the path, but size to the yellow signal, not the green.

Trading readVIX subdued, VVIX firming, SKEW elevated, MOVE quiet - equity vol-of-vol and skew are quietly bidding while rates and headline VIX shrug, a textbook precursor pattern worth respecting.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

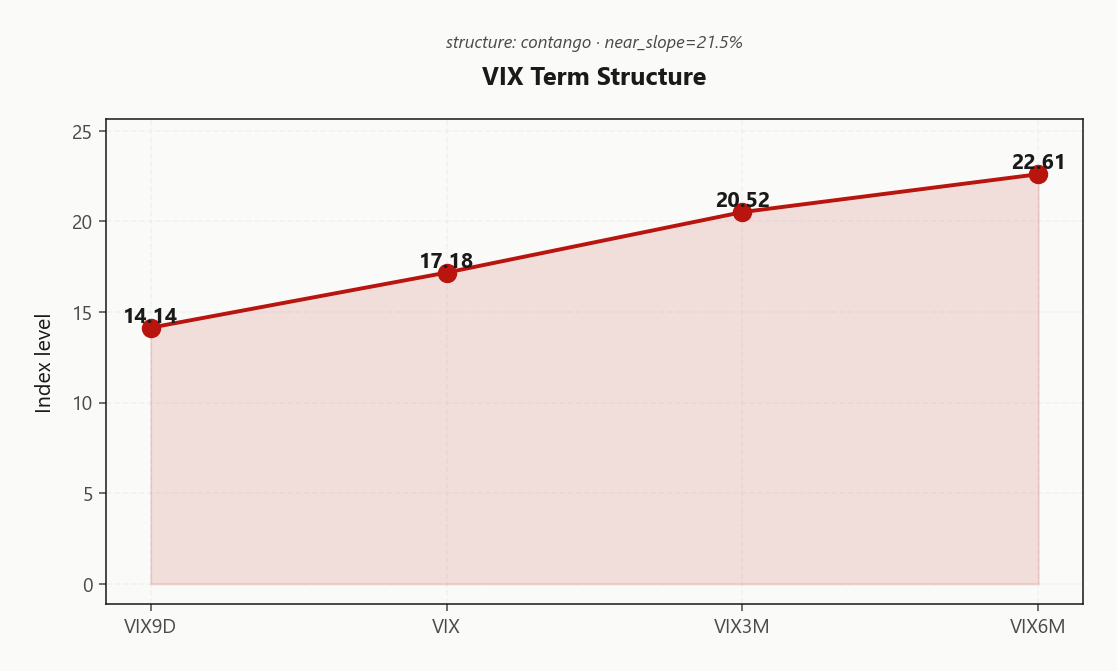

The VIX curve is in Contango with a near-slope of 21.5% - VIX9D at 14.14 sits well below spot VIX 17.18, while VIX3M 20.52 and VIX6M 22.61 anchor the back end. Classic carry-friendly geometry: the front is pricing near-term complacency while the back end is paid for normalization, not stress.

Forward 30-60 implied prints at 22.0006681717 - vol sellers are paid to wait, and the roll-down does the work. The signal reads Steep contango - vol sellers favored, which we interpret as structural carry, not event premium. Translation: short the front, hedge convexity further out where the curve actually pays you to own gamma.

Premium-harvest sweet spot is 30-45 DTE - far enough to clip the contango roll, short enough to avoid stale-vol drift if the back end softens. Front-end pops are the risk; the slope is steep enough that any spike in VIX9D would generate outsized mark-to-market pain on naked short-front structures.

What it means for your trading

Curve is Steep Contango with VIX9D well under VIX3M - short front-end vol, hedge with longer-dated convexity, and concentrate harvest in 30-45 DTE.

Trading readSteep contango with VIX9D 14.14 well under VIX3M 20.52 - the carry trade pays, but the slope is steep enough that any front-end pop produces outsized roll losses.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 11.99% sits comfortably above HV20 of 10.4, keeping VRP active at 1.59% - options remain rich to recent realized and short-vol structures continue to clear premium. With HV60 at 15.09 printing above HV20, realized is decelerating from a higher base, reinforcing the case that the implied-realized wedge is structural, not a rounding artifact.

Cross-asset, QQQ VRP at 3.39% is stretched materially further than the index, flagging tech as the cleaner premium-sale name into the 30-45 DTE window. IWM VRP at 1.7% is thinner - small-caps don't pay enough for the gap risk, skip them for vol harvest. ATM IV consistent with the elevated regime label means short-vol is paid, but sized to a regime that can re-rate quickly.

What it means for your trading

VRP is live across the index complex with QQQ (3.39%) the fattest carry versus SPY (1.59%); rotate premium-sale weight toward tech and skip IWM at 1.7%.

Skew Convexity

Quarter-delta put skew prints at 1.85% vol points with the smile ratio at 1.27% - downside is paying up in ordered fashion while the call wing sits muted. Put 25d IV at 8.84% against ATM 7.49% and call 25d at 6.99% traces the classic hedger bid, not capitulation flow. SKEW prints 136.11, corroborating that tail convexity is being accumulated quietly even with VIX subdued.

The implication for structure is clear: with downside vol this rich relative to ATM, naked long puts overpay for protection - spread the put wing and let the steepness of the smile finance the carry. Call skew is flat enough that there is no upside-conviction premium to harvest from short calls beyond the wall mechanics already in play.

Net: tail convexity bid, body unchanged, call wing a non-event - a regime where put-spread protection and call-side premium sales sit on the same side of the trade.

What it means for your trading

Steep, ordered put skew at 1.85% with SKEW at 136.11 says hedgers are paying up methodically, not panicking - favor put spreads over naked puts and let the flat call wing keep upside structures cheap to finance.

Vol-of-Vol Structure

VVIX prints 96.95 against a VIX of 17.18, putting the ratio at 5.64 - squarely in the Normal band. No bimodal tail-event premium baked in, no panic geometry; vol-of-vol is behaving like a calm-tape companion to the steep contango.

The tell is the divergence: VVIX ticked up 3.57% on a session where headline VIX barely moved. That's a quiet convexity bid - hedgers paying up for gamma-on-gamma without dragging the front of the curve with them. Not enough to flip the regime, but enough to flag that someone is positioning for a re-rating, not just rolling.

Sizing guidance: Standard Size. Green light for standard short-vol weight on the iron condor harvest - no need to trim for tail premium, no reason to chase either. The convexity bid is a watch-item, not a size-cut catalyst.

What it means for your trading

Vol-of-vol sits in the normal regime at a VVIX/VIX ratio of 5.64, but a 3.57% VVIX print on a flat-VIX day is a quiet convexity bid worth tracking. Standard sizing per Standard Size - harvest at full weight, but flag any further VVIX/VIX widening.

Dispersion Spread

Cross-asset vol surfaces sit in moderate dispersion: SPY ATM IV at 11.99% prints materially below QQQ at 18.82%, with IWM richer at 18.86%. Tech is carrying the dispersion premium - single-name AI rotation is bleeding into the QQQ surface without lifting the index proper, while small-cap premium remains intact on idiosyncratic balance-sheet sensitivity.

The spread argues against the reflex to short single-name vol on the back of an index hedge. Index gamma is parked positive and dampening realized at the SPY level, but QQQ-implied is paying for component dispersion that index correlation isn't suppressing - naked single-name short-vol gets no help from the SPY pin. Cleaner edge: harvest at the index.

Translation: SPY/SPX iron condors capture the structural carry without taking the dispersion leg; QQQ offers a fatter premium for traders willing to wear the AI-rotation gamma. Watch single-name earnings drift - a widening QQQ-vs-SPY spread is the first tell that dispersion is breaking out of moderate and into a regime worth trading directly.

What it means for your trading

Moderate dispersion with QQQ ATM IV at 18.82% well above SPY's 11.99% - sell index vol, skip single-name harvest until the spread widens further.

Liquidity & Microstructure

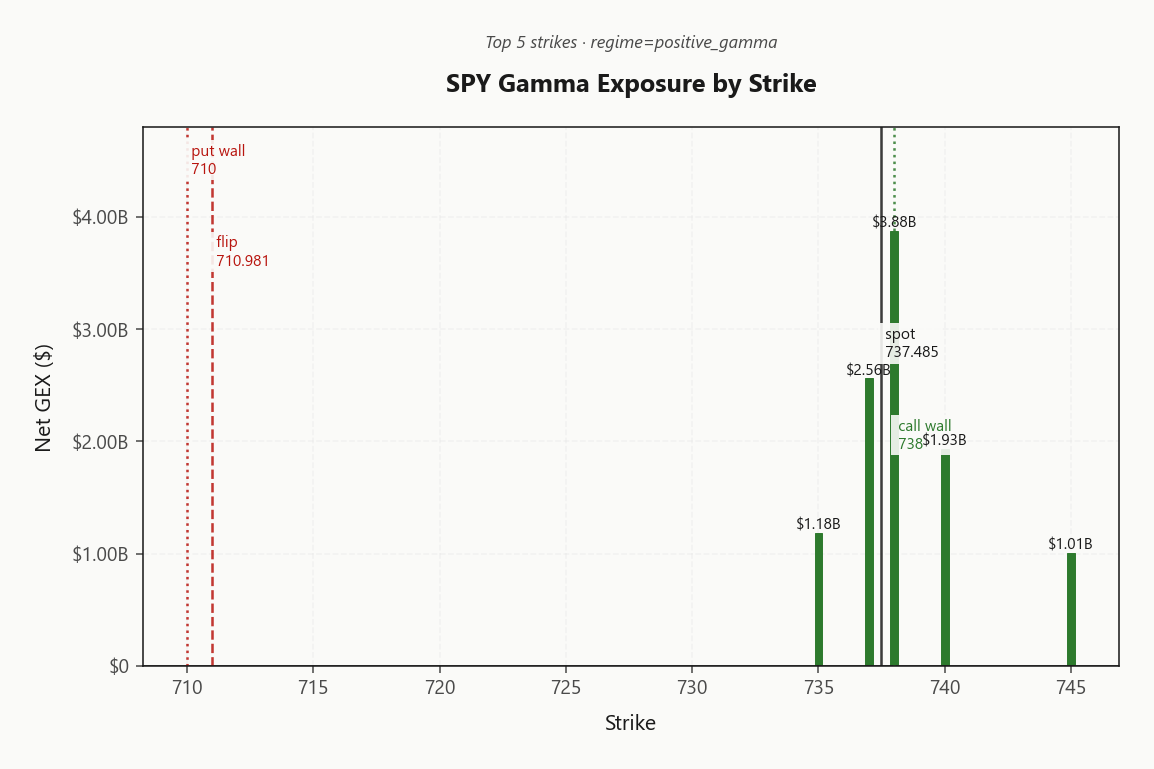

SPY's strike map is unambiguously top-heavy: the dominant GEX node parks right at 738.00 with $3.88B of dealer length stacked into the 738.00 call wall, while the highest open-interest cluster at 700 sits well below spot - that's standing hedge concentration, not an active magnet. Spot pinned just under the wall with the 710.00 put wall and gamma flip 710.98 aligned far underneath leaves a deep cushion above the inflection.

Above flip means dealer flow is supportive: routine pullbacks get bought, rallies get fade-sold into the wall. The structure is deep and one-sided enough that downside hedging only mechanically flips on a real break of 710.98. Intraday, with 0DTE carrying 60.4% of total gamma, expect chop and pinning around the top-strike cluster - the dominant driver of tape behavior into the bell.

What it means for your trading

Strike topology is textbook positive-gamma: top GEX at 738.00 caps upside while 710.00/710.98 alignment leaves a wide buffer below - fade strength into the wall, only flip defensive on a clean break of flip.

Trading readMassive positive gamma stacked at and just above spot through the call wall 738.00 means dealers dampen rallies and buy dips - fade strength into the wall, don't chase, and only flip defensive if spot breaks 710.98.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The charm pivot anchors at 738, classified as the Call Wall - meaning the same level capping spot is also the inflection where vanna/charm flow flips sign. Spot sits a hair below it with current bias tagged Neutral, distance to pivot just 0.0698319288 - flow is delicately balanced, pinned just under the wall.

Net-net: vanna is the latent risk, not the active one. Hold the regime view while VIX stays contained; if it doesn't, the negative VEX cashes in fast and dealer selling stacks on top of any slide.

What it means for your trading

Vanna risk is loaded but dormant - a vol spike converts it into amplified downside via dealer delta selling, while charm pressure into the close stays mild. The pivot at 738 doubles as the call wall and the regime trigger; bias stays Neutral until that level breaks.

Cross-Asset Confirmation

Cross-asset tape reads Aligned with no fracture between the equity benchmarks. QQQ at 711.19 and IWM at 284.32 both sit above their respective gamma flips, mirroring SPY's positive-gamma posture - the index complex is moving as one block, not telegraphing the sort of small-cap or tech-led divergence that typically front-runs a regime break.

Rates vol corroborates the calm: MOVE at 72.24 is nowhere near stress thresholds, so there is no credit-shock signature bleeding into equity skew. Fear & Greed prints 67 (Greed) - warm enough to warrant contrarian discipline but well shy of the euphoria zone that demands defensive positioning. Cross-asset tone Unknown confirms this is benign drift, not a setup pricing in tail risk.

Trade the alignment: short premium structures get a green light from the cross-asset book, with no rates or breadth signal arguing for a hedge overlay beyond standard wing protection.

What it means for your trading

Equity complex aligned positive-gamma, MOVE at 72.24 quiet and F&G in Greed at 67 - no cross-asset signal contradicting the short-vol thesis. Watch for QQQ/IWM to break from SPY before respecting any stress trade.

Scenario EV

Scoring favors Iron Condor at 49 versus put-spread at 37 - premium harvest is the path of least resistance with a best score of 49 flagging moderate edge, not a fat pitch. Anchor wings on the 738.00 call wall and 710.00 put wall to lean on dealer positioning rather than fight it.

The 30-45 DTE window is the sweet spot - far enough out to harvest the steep VIX contango carry, far enough in to dodge the gamma sensitivity of the front weeklies. With VVIX in normal regime, sizing stays at Standard Size; no convexity premium argues for cutting risk here.

Run the structure, fade strength into the wall, and only flip defensive if the tape breaches 710.98.

Trade: sell Iron Condor in the 30-45 DTE window, wings anchored on the 738.00 call wall above and the 710.00 put wall below. Spot pinned just under the wall with VRP at 1.59% and a Elevated / Watchful regime is the textbook premium-harvest setup — carry pays, dealer flow dampens, mean-reversion is the path of least resistance.

Avoid: naked short calls into the wall — reward is asymmetric versus a breakout through 738. Skip long single-leg vol with VRP this rich; you are paying the carry the condor harvests. Size:Standard Size given VVIX in normal range.

Watch: the gamma flip at 710.98 is the regime-flip trigger — a clean breach pulls dealers short gamma and flips the tape from fade-strength to chase-weakness. Above flip, stay short premium; below it, cut size and respect the new flow.

What it means for your trading

Premium harvest via Iron Condor in 30-45 DTE bracketed by 738.00/710.00 is the cleanest expression of a positive-gamma, contango-rich tape. 710.98 is the line in the sand — defend the structure above it, defend capital below it.

AI leadership rotation away from NVDA toward Intel, AMD, and memory names is exactly the kind of intra-tech reshuffling that can keep QQQ's positive-gamma regime intact while reshaping single-name dispersion

Rubio's questioning of allied support on Iran adds incremental geopolitical premium to the tail - relevant for why skew remains steep despite calm spot

Bond vigilantes circling gilts is the kind of cross-border rates signal that can spill into US duration and revive MOVE if it gathers momentum

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.18 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.98 against a spot of 737.49. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 11.99% with a volatility risk premium of 1.59%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.18. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime