Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

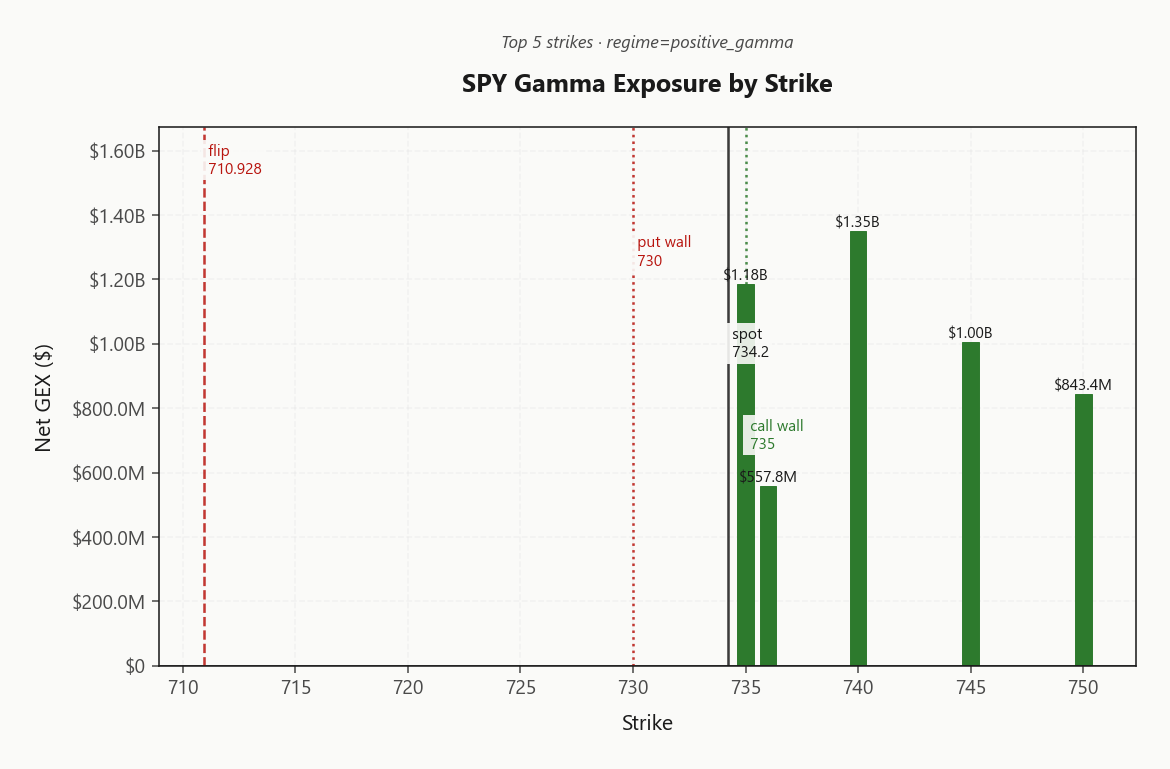

SPY at 734.20 sits in Positive Gamma with net GEX of $5.19B - dealers dampening moves and favoring mean reversion. Call wall 735.00 caps upside while put wall 730.00 backstops, with the gamma flip well below at 710.93 - a deep cushion as long as spot holds above. Vanna at -$294.64B flags that any vol spike turns dealers into delta sellers, so the cushion is conditional on calm. Charm at -$8.2M adds modest pin pressure into the close. VIX at 17.32 with VIX9D at 14.76 and VIX3M at 20.57 prints Contango - vol-seller carry is on. VRP at 2.43% confirms options remain rich to realized. VVIX at 93.70 is normal - no jump premium distortion, standard sizing. Bottom line: Iron Condor in the 30-45 bucket is the path of least resistance; fade strength into 735.00, treat a break of 710.93 as the regime-change line.

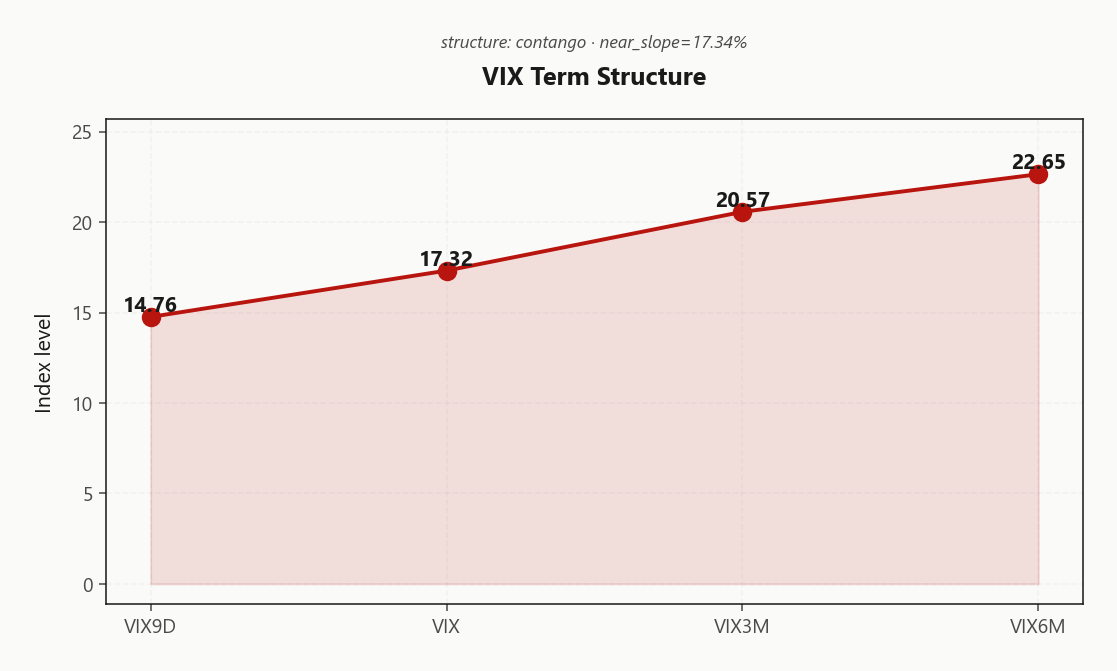

Positive gamma cushion intact across index complex with VIX in steep contango at 17.32

Index complex enters the open with dealers long gamma across SPY, QQQ, and IWM, while VIX sits at 17.32 with a Contango term structure. Iran de-escalation headlines and AMD-led AI strength have compressed near-dated vol while leaving vol-of-vol normal. Spot pinned near the call wall sets up classic mean-reversion tape unless the gamma flip breaks.

Regime Assessment

Current regime reads Elevated / Watchful with VIX anchored at 17.32 - sticky enough to fade, not so calm that tails can be ignored. Half-life of 15 sessions is the operative number: it tells you the regime is durable enough to underwrite 30-45 DTE structures without the rug pulling mid-trade.

Transition math is the tell. Probability of a panic break in five sessions sits at 0.05 - small but non-trivial - while the to-low migration over ten sessions runs 0.45. Translation: the modal path is further compression, not escalation, but the right tail still demands respect. Cross-asset alignment at Aligned reinforces the base case.

Trade it accordingly: harvest VRP through Iron Condor in the 30-45 bucket, keep tail hedges resident, and treat a VVIX breach above the calm threshold paired with VIX reclaiming the elevated handle as the regime-change trigger - not the headline du jour.

What it means for your trading

Regime prints Elevated / Watchful at VIX 17.32 with a 15-session half-life - durable enough for medium-DTE vol selling, with the to-low path at 0.45 dominating the panic tail at 0.05.

Trading readVIX, VVIX, SKEW, and MOVE all sit in the calm-confirming quadrant - no divergence yet, which is what the positive-gamma regime needs; the first crack would likely show up in VVIX moving north of 110 ahead of a spot break.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve prints Contango with VIX9D at 14.76 trading below spot VIX at 17.32 - no near-term event premium baked in. The slope from VIX to VIX3M at 20.57 runs at 17.34%, steep enough to fund calendar carry without binary event drag.

Forward 30-60 vol at 22.0158159058 versus forward 60-90 at 24.554431372 tells you where the curve is pricing the most uncertainty - back-end pays for duration, front-end is being given away. The Steep contango - vol sellers favored regime is the textbook short-front, own-back setup.

Sweet spot for harvest sits in the 30-45 bucket: far enough out that slope steepness funds the structure, close enough that theta still bites. Sell front, own back, let the curve do the work.

What it means for your trading

Steep contango from 14.76 through the back-end with a Steep Contango forward read greenlights structural short-vol carry. The 30-45 DTE bucket is where slope and theta meet without paying for tail premium.

Trading readContango with VIX9D below VIX and VIX3M well above means the carry trade is paying - short front, long back, and the slope is steep enough to absorb modest near-term vol bumps without flipping.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.62% trades well clear of HV20 at 10.19 - the tape hasn't moved, but options are still being paid to hold the bag. VRP at 2.43% confirms the carry is alive, and that spread is the cleanest read on why short-vol structures keep clearing premium without working for it.

The HV20 versus HV60 gap is the tell: realized has been compressing, not accelerating, while HV60 at 15 still anchors a meaningfully higher fair vol. That asymmetry is the structural argument for harvesting front-end IV - short-dated optionality is rich to recent realized, but the longer lookback prevents the curve from collapsing outright. Iron condors and calendars in 30-45 sit in the pocket where ATM-RV spread does the heaviest lifting.

The risk to the trade is HV5 - any acceleration there drags HV20 higher and compresses VRP from the realized side before IV reprices. Until that prints, the Vrp Active read holds and short-vol harvest is the path of least resistance.

What it means for your trading

VRP at 2.43% with ATM IV at 12.62% versus HV20 at 10.19 keeps the short-vol carry intact, while HV60 at 15 anchors fair vol higher - watch HV5 acceleration as the early warning that realized is catching up.

Skew Convexity

Quarter-delta skew prints 2.84% with the put wing carrying 17.05% against a flat call wing at 14.21% - ordered downside hedging, not a panic bid. Smile ratio at 1.2% against ATM 14.63% confirms a put-heavy bias without the tail blow-out signature that would force a regime rethink.

Trade implication: downside still pays, so put spreads structurally dominate naked puts - selling the steep wing while owning further-out strikes captures the skew curvature without leaving naked tail. Flat call skew is the other half of the message - zero upside conviction premium means covered calls and call-side legs of Iron Condor structures clear cheap. Far-tail convexity remains underbid; for books that want disaster insurance, this is the print to scale into rather than chase after a vol shock.

What it means for your trading

Skew is steep but ordered - put spreads over naked puts, covered calls cheap, far-tail convexity still on sale while VVIX prints Normal.

Vol-of-Vol Structure

VVIX at 93.70 prints Normal - the vol surface is not pricing a bimodal jump, and there's no fat-tail premium distorting the wings. The VVIX/VIX ratio at 5.41 sits squarely in the calm-regime band, which means convexity on vol itself is being given away rather than bid.

Sizing guidance reads Standard Size: full-clip iron condors and short strangles, no half-sizing tax for jump risk. With VIX at 17.32 and vol-of-vol benign, the short-premium book runs at standard notional - the surface is paying you to carry, not punishing you for it.

The trigger to flip is mechanical, not discretionary: VVIX north of 110 is the first signal that jump premium is being repriced into the surface. Until then, treat vol-of-vol as a green light on the structures the rest of the book already favors - the cushion is intact and sized for it.

What it means for your trading

Vol-of-vol prints Normal with VVIX/VIX at 5.41 - full-size short-vol structures cleared, no jump-premium tax. Watch VVIX through 110 as the regime-distortion line.

Dispersion Spread

Index vol is the cheap leg of the book. SPY ATM IV at 12.62% sits materially below QQQ at 18.81% and IWM at 20.4% - single-name surfaces are carrying the dispersion premium while the index complex prices in the dampening from positive gamma and Aligned cross-asset regimes.

The trade geometry is clean: long single-name vol, short index vol remains the structural edge while correlation stays suppressed. Index hedges are underpaying relative to name-level risk in the AI complex, and SPX/SPY vol is the cleanest harvest vehicle into the 30-45 bucket. Better edge selling index than picking off rich single-name premium one ticker at a time.

The asymmetric risk is a correlation snap. If a macro catalyst forces names to move together, index vol catches up to single-name vol fast - and the gap from 12.62% back toward the QQQ/IWM cohort closes violently. Until then, the dispersion trade is paid; treat any narrowing of the index-to-name spread as the first tell that correlation is regime-shifting.

What it means for your trading

Sell index vol against single-name longs while the spread between 12.62% and 18.81%/20.4% stays wide - a correlation snap is the only thing that closes it, and it closes fast.

Liquidity & Microstructure

The strike map is doing the work here: a dense OI cluster at 700 anchors the book while the call wall at 735.00 sits a tick above spot, capping melt-up flow into a ceiling dealers are paid to defend. The top GEX strike at 740.00 carries $1.35B of concentrated hedging - that's where dealer rebalancing flow gets loudest on any drift.

Beneath spot, the put wall at 730.00 is the first organic bid layer, but the real line is the gamma flip down at 710.93. Above it, dealers dampen; below it, hedging flow inverts and amplifies. Treat the corridor between 730.00 and 735.00 as the mean-reversion lane and 710.93 as the regime-change trigger that turns dealers into accelerants.

What it means for your trading

Microstructure is deep and pinned: fade strength into 735.00, lean on 730.00 for support, and only flip bearish on a clean break of 710.93.

Trading readMassive call wall stack into 735.00 caps upside flow while the put wall at 730.00 provides organic support - fade strength into the wall, buy dips toward the put wall, treat anything below the gamma flip as regime-change territory.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$294.64B - meaningfully short vanna. Translation: any uptick in implied vol forces dealers into delta sales, so the positive-gamma cushion is conditional on a calm tape. Vanna is the hidden short that only shows up when VIX wakes up; until then it sits dormant beneath the gamma dampening.

Trade implication: the cushion holds while VVIX stays anchored, but a vol pop converts dealers from gamma-dampeners to vanna-driven sellers in a single tick. Treat 735 as the neutral-to-directional flip and keep tail hedges live against the latent vanna short.

What it means for your trading

Gamma is the visible cushion; vanna at -$294.64B is the latent short waiting on a vol spike, while charm at -$8.2M contributes only mild close-side pin pressure. Bias stays Neutral until 735 breaks.

Cross-Asset Confirmation

Cross-asset tape reads Aligned: MOVE at 70.63 sits benign, killing the rates-driven equity tail before it starts. QQQ at 696.21 and IWM at 285.07 both hold positive_gamma alongside SPY - no index is leaning out of the regime, no credit-equity divergence to fade.

Sentiment is the one stretched wire. Fear & Greed prints 68 at Greed against a calm vol surface - contrarian caution flag, not a sell signal. Pair it with the steep Contango in VIX and the message is consistent: harvest the carry, keep tail hedges on the book, don't chase.

The catalyst pattern is geopolitical relief, not credit shock - Iran de-escalation compresses front-end premium without forcing a rotation. That's the textbook mean-reverting setup: dealers long gamma across the index complex, MOVE flat, VVIX at 93.70 confirming no jump premium leaking in.

What it means for your trading

Cross-asset alignment is intact - MOVE benign, all three index ETFs in positive_gamma, sentiment stretched but not panicked. Trade the regime, but treat F&G Greed as the reminder to keep convexity on the book while selling VRP.

Scenario EV

The structure tape ranks Iron Condor top of book at 60, ahead of the put spread alternative - VRP rich at 2.43%, vol-of-vol benign at 93.70, and the regime sticky in Positive Gamma. Carry is paid to wait, and there is no jump premium distorting the wings.

The 30-45 DTE bucket is where theta bite meets manageable gamma - short enough to harvest the steep front of the curve below 20.57, long enough to sidestep the binary event tape that compresses any single session. Sell the call wing into 735.00, anchor the put wing above 730.00, and treat 710.93 as the line that invalidates the trade.

Sizing stays standard - VVIX in the normal band means no half-sizing, no fat-tail surcharge. The put spread alternative scores cleanly behind at structure level; reserve it for a regime breach below the flip, not the base case.

What it means for your trading

Iron Condor in 30-45 DTE is the path of least resistance with VRP rich, VVIX normal, and dealers long gamma. Score 60 beats the put spread alternative - fade strength into 735.00, flip thesis on a break of 710.93.

Actionable Summary

Path of least resistance is harvesting VRP through Iron Condor structures in the 30-45 bucket - SPY anchored at 734.20 in Positive Gamma with net GEX of $5.19B keeps dealers dampening, while VIX in Contango at 17.32 funds the carry and VVIX at 93.70 greenlights standard sizing.

Trade the range: fade strength into the 735.00 call wall, buy dips toward 730.00. Skew at 2.84% rules out naked short tails - put spreads only. Charm pivot 735 is the bias flip; 710.93 is the regime breakdown line where dealer flow inverts.

Avoid chasing breakouts above the wall - pin pressure caps. Regime reads Elevated / Watchful: sticky enough to size, not complacent enough to ignore the vanna short embedded in -$294.64B.

Gold rallying alongside equity strength while oil slides on Iran peace hopes flags a classic geopolitical-relief tape - risk-on with safe-haven bid is a signature of compressing tail premia.

Trump-Xi summit headlines are the next macro fulcrum - front-end VIX pricing assumes orderly outcomes, so any tape disruption hits the steep contango first.

China asking banks to pause loans to US-sanctioned refiners is a quiet escalation in the energy/financial sanctions chain - watch crude vol and credit spreads for second-order effects.

S&P and Nasdaq fresh records on AMD-led AI rally is the structural backdrop - earnings momentum justifies the positive-gamma regime and explains compressed implied vol despite stretched sentiment.

Occidental scrapping new oil hedges as Iran war fuels volatility signals corporate hedgers are stepping back precisely when retail vol is compressing - a divergence worth watching.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.23 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.93 against a spot of 734.20. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.62% with a volatility risk premium of 2.43%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.32. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime