Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

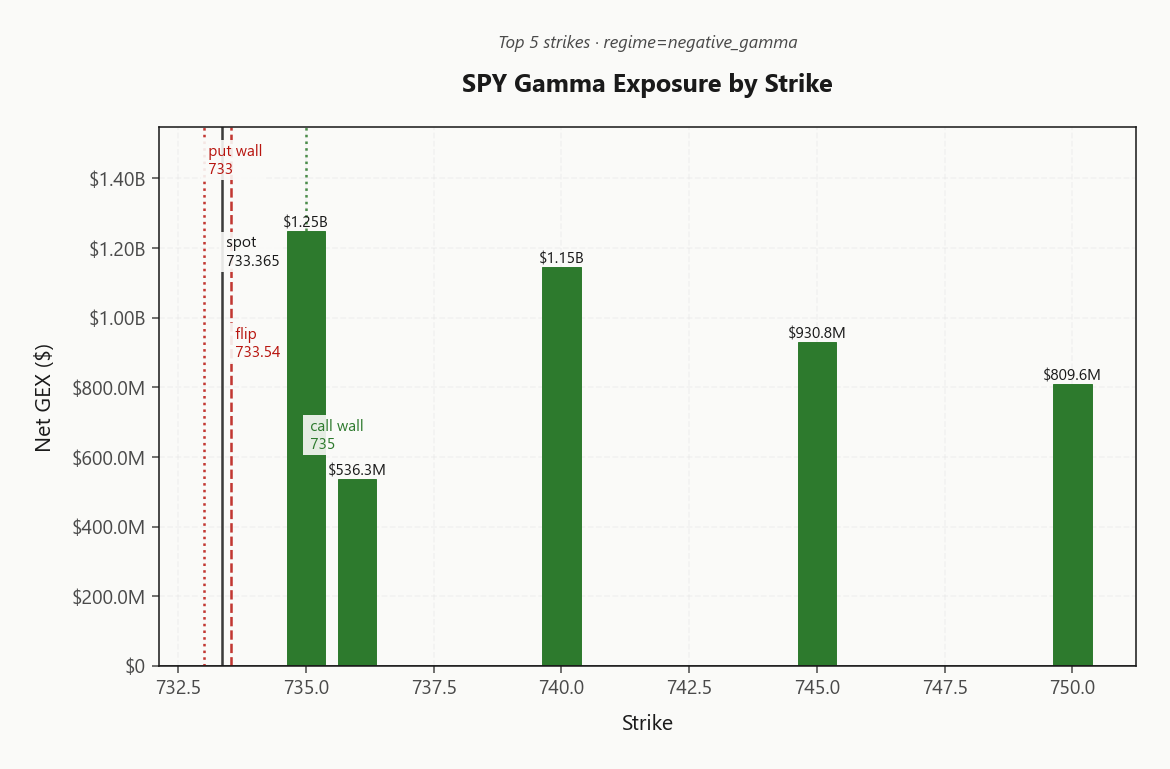

SPY at 733.37 sits within a fraction of its gamma flip 733.54, with net GEX $3.99B barely positive but the regime tagged Negative Gamma - dealers are unhedged either way, and any directional break gets amplified. Call wall 735.00 caps upside while put wall 733.00 sits right at spot, making the 733.54 - 735.00 band the entire battleground today. Dealer vanna -$286.49B and charm -$10.4M are both pulling negative - vol up means dealer selling, time decay means selling pressure into the close. VIX at 17.32 with term structure Contango and VVIX/VIX ratio 5.32 keeps vol sellers paid, but the Destabilizing pivot bias means tail hedges remain warranted. QQQ stays Positive Gamma above its flip 689.23 - that's the divergence story (Qqq Heavier) and the cleanest place to express vol-selling. IWM at 283.39 is Negative Gamma with the highest 0DTE share 41.2% - avoid naked structures there. Bottom line: Iron Condor in the 30-45 window on QQQ, fade SPY strength into 735.00, sidestep IWM directional bets.

SPY pinned at gamma flip 733.54 with negative gamma; QQQ cushioned, IWM fragile.

SPY trades right on top of its gamma flip at 733.54, putting dealers in destabilizing territory while QQQ remains comfortably above its flip in positive gamma. With VIX in steep contango and VVIX normal, the carry trade is intact - but the SPY/QQQ regime divergence (Qqq Heavier) and IWM's negative gamma backdrop argue for defined-risk structures only. Iron condors at the 30-45 window screen best.

Regime Assessment

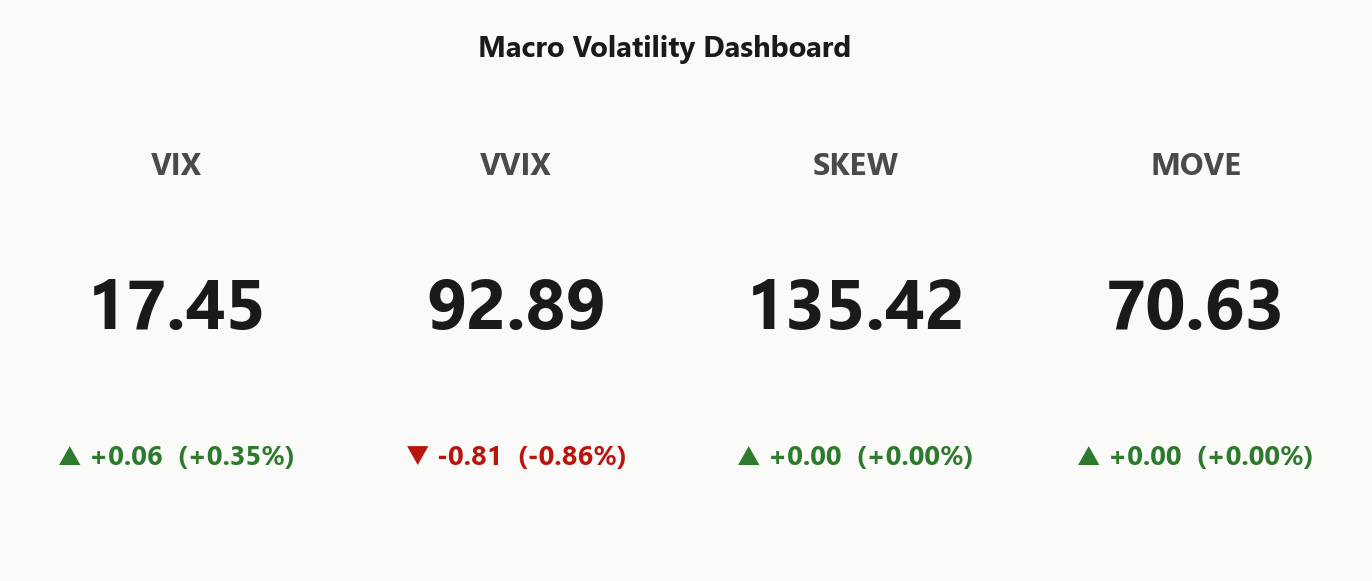

Regime tags Elevated / Watchful with VIX anchored at 17.45 - watchful, not stressed. The half-life of 15 sessions tells you this state is sticky enough to lean into, not fade against. Transition probability to panic over five sessions sits at 0.05, while the drift back toward low-vol over ten sessions runs 0.45 - the asymmetry favors carry.

That low panic-transition probability is the green light for premium-selling. With VVIX/VIX ratio in Normal territory and term structure Contango, the regime pays you to be short vol - but the Destabilizing charm pivot keeps tail hedges relevant. Lean into structures sized to the half-life, not against it.

What it means for your trading

Regime is Elevated with sticky half-life and minimal panic-transition odds - premium harvest is the trade, defined-risk the discipline.

Trading readVIX, VVIX and MOVE all confirm the suppressive regime; SKEW at 135.42 adds modest tail bid but nothing alarming - confirmation across instruments, no divergence flag.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

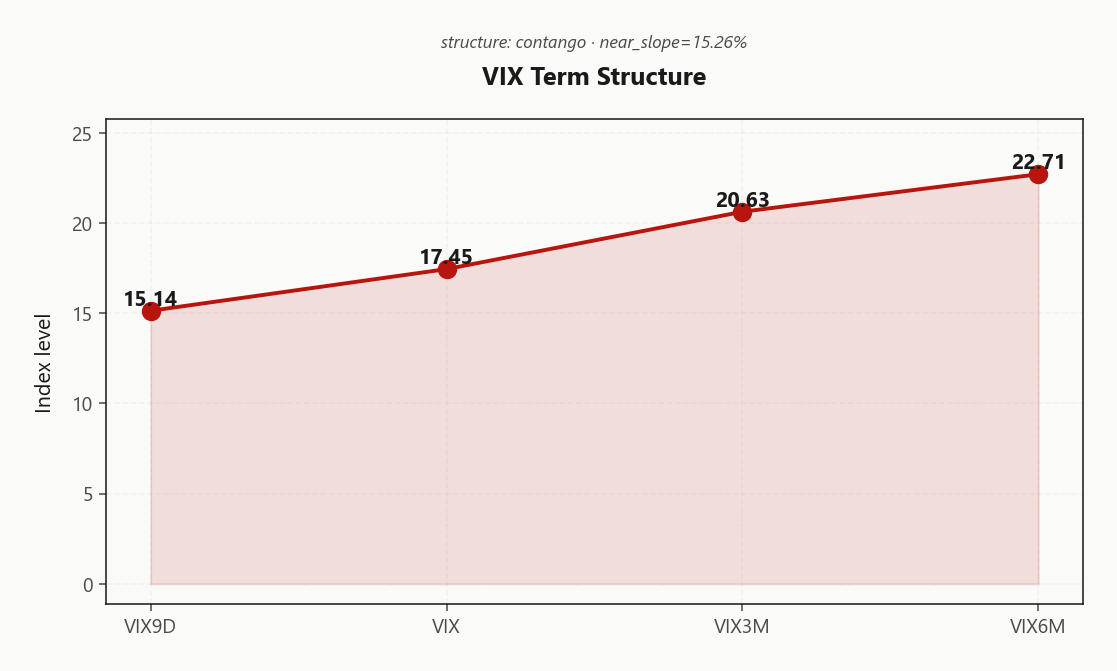

The VIX curve prints textbook Contango from VIX9D 15.14 through spot VIX 17.45 out to VIX3M 20.63 - the front end sitting below cash confirms no near-term event premium is being priced, and the carry trade pays sellers across the term complex.

Forward 30-to-60 vol implied by the curve runs at 22.0486756972, well clear of spot, while forward 60-to-90 extends to 24.6148593333 - calendars get paid by the shape itself, before any realized cooperation. The Steep Contango regime tag means structural short-vol carry dominates directional bets here; sell front, own the belly, let the curve do the work.

Best edge sits in the 30-45 window - far enough from the gamma-pin tape to escape 0DTE noise, close enough that forward vol is fully absorbing the contango. Steep contango - vol sellers favored.

What it means for your trading

Curve shape is doing the work - Contango from VIX9D 15.14 through VIX3M 20.63 keeps short-vol carry intact, and the Steep Contango forward print favors calendar and condor structures in the 30-45 window over directional exposure.

ATM IV at 12.76% sits well above HV20 10.24, with VRP 2.52% active across the curve - the IV-RV spread is Moderate Premium and short premium is getting paid. RV5 11.05 versus RV20 10.25 shows realized is decelerating, not accelerating into the tape.

HV60 15 printing above HV20 confirms recent realized has cooled while options stay rich - the term shape says cushion has been built, not burned. That cooling-RV-into-richer-IV configuration is the textbook setup for income structures over long convexity; you don't need spot to move, you need it to drift.

The scenario engine ranks iron condor at 59 ahead of put spreads at 49, reflecting where the VRP harvest cleanly lines up. Express it in the 30-45 window where forward vol fully prices event premium without 0DTE pin noise.

What it means for your trading

With ATM IV 12.76% running rich to HV20 10.24 and realized decelerating, the VRP 2.52% is a paid carry - lean into iron condors in the 30-45 window rather than long convexity.

Skew Convexity

The 3.06% quarter-delta skew with a smile ratio of 1.22% tells the cleanest story on the board: puts are paying up, but they're paying up orderly. Put quarter-delta IV at 16.75% against ATM 14.6% and call quarter-delta 13.69% traces a textbook downside premium curve - no left-tail bid, no crash convexity hoarding, just steady hedging demand.

SKEW index at 135.42 corroborates: tail pricing sits in the normal-hedging band, not the panic band. That matters for structure selection - when the wing isn't bid asymmetrically, naked puts overpay for protection you can replicate cheaper with put spreads. Sell the wing, own the body.

With VVIX/VIX at 5.32 and term structure Contango, the convexity signal is ordered, not bid. Spread protection beats outright puts here, and put-spread financing via the call wing remains attractive given the flat upside skew.

What it means for your trading

Skew at 3.06% with smile ratio 1.22% reflects orderly downside hedging, not tail panic - favor put spreads over naked puts and finance via the flat call wing.

Vol-of-Vol Structure

VVIX at 92.89 against spot VIX 17.45 prints a ratio of 5.32 - squarely in the Normal band. No jump-risk premium is being paid, which means the tape isn't pricing a bimodal outcome and the convexity-of-convexity bid that typically precedes vol shocks is absent.

That tells you the harness is signaling Standard Size - full clip, not half-size. Premium-selling structures get the same notional you'd run in any benign regime; there's no VVIX-driven haircut to apply, and the carry geometry behind iron condors at 30-45 works without a vol-of-vol discount.

That said, tail hedges remain warranted. Charm pivot bias reads Destabilizing with the pivot at 733.5397900204 - VVIX won't warn you before dealer flow flips. Keep wing protection on; the regime is calm, not bulletproof.

What it means for your trading

VVIX/VIX at 5.32 is Normal - full-size short-vol structures, but keep wings on given the Destabilizing charm pivot.

Dispersion Spread

Index ATM IV at 12.76% trades a clear notch beneath QQQ at 18.8% and IWM at 20.15% - single-name vol is doing the heavy lifting on premium while the index complex screens cheap on a relative basis. Cross-strike dispersion at 47.43 versus cross-expiry at 2.69 says the smile is the dispersion engine, not the term curve - idiosyncratic tails are bid, the index isn't.

IWM's premium over SPY directly prices small-cap fragility - consistent with the Negative Gamma backdrop and elevated 0DTE share 41.2%. That gap is structural, not a fade. Cross-asset tone reads Unknown with regime divergence Qqq Heavier, reinforcing that the dispersion premium reflects breadth weakness rather than index complacency.

Trade implication: sell index vol, not single-name. SPY/SPX short-premium captures the cheap leg of the dispersion trade while leaving idiosyncratic convexity intact at the names where it's actually paying. Index hedges underprotect against name-level shocks here - pair short index vol with selective single-name long convexity rather than raw index puts.

What it means for your trading

Index ATM IV at 12.76% trading below QQQ 18.8% and IWM 20.15% flags an active dispersion premium - sell index vol, hold single-name convexity. Cross-asset divergence Qqq Heavier confirms the gap is structural, not noise.

Liquidity & Microstructure

Open interest clusters at 700 while the gamma flip 733.54 sits essentially on top of spot - this is the level where dealer flow direction reverses. Above 735.00 dealers fight rallies; below 733.00 they amplify selloffs. There is no cushion either side of spot today.

The top strike at 735.00 concentrates $1.25B of net GEX - magnetic enough to pull tape into close if spot drifts that way. Call wall 735.00 caps upside while put wall 733.00 is the immediate downside trigger; the band between them is the entire battleground.

0DTE share at 7.1% of total gex is manageable - today's tape is term-driven, not pin-driven. Trade the band, fade strength into 735.00, but respect the flip: a clean break flips dealer flow from suppressive to accelerant.

What it means for your trading

Spot pinned at the gamma flip 733.54 with no dealer cushion either side - fade rallies into 735.00 and treat a break of 733.00 as a flow-acceleration trigger, not a dip-buy.

Trading readGamma stacks heavily on the call side from 735.00 upward, meaning dealer dampening kicks in above spot - but with spot pinned at the flip 733.54, there's no cushion below today. Trade the band, don't fade the breakout.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order greeks are pulling in the destabilizing direction. Net VEX prints -$286.49B - deeply negative - meaning any vol bid forces dealers to sell delta into the move, the classic accelerant. Net CHEX at -$10.4M compounds the problem: time decay drags the desk progressively shorter into the close, so passive flow is one-way.

Trade implication: do not fade range extensions intraday. Defined-risk only, and keep tail hedges on through the close - the greeks are telling you the desk has no incentive to stabilize the tape from here.

What it means for your trading

Vanna and charm both negative with the pivot at 733.5397900204 tagged Destabilizing - dealer flow amplifies any directional break, so size for momentum continuation, not mean reversion.

Cross-Asset Confirmation

Cross-asset tape confirms the equity-internal read: MOVE at 70.63 stays muted, telling you bonds are not pricing credit or rates stress, while Fear & Greed prints Greed at 68 - risk-on tone intact, contango regime supported, no macro divergence flag firing.

The lead anomaly is intra-equity, not macro. QQQ at 696.29 sits in Positive Gamma above its flip while SPY drifts onto its own and IWM at 283.39 trades Negative Gamma - large-cap tech is doing the carrying, small-cap breadth is fragile. Regime divergence direction reads Qqq Heavier, mega-cap gamma is the cushion, and the cross-asset tone scans Unknown.

Net: instruments are Qqq Heavier on the macro layer, diverged on the equity layer. Express short-vol where the gamma underlay supports it (QQQ), fade strength where dealers are pinned (SPY into 735.00), and avoid IWM directional bets - the chop trap lives in the small-cap negative-gamma backdrop.

What it means for your trading

MOVE muted and Fear & Greed at Greed rule out a macro shock signature, leaving the SPY/QQQ regime split (Qqq Heavier) as the actionable story. Trade the divergence - QQQ short-vol over SPY, sidestep IWM.

Scenario EV

The scenario engine prints Iron Condor at score 59, clearing the put-spread alternative at 49 by a margin that reflects the regime, not noise. With VRP 2.52% active against ATM IV 12.76% and HV20 10.24, premium harvest is paid on both wings - and forward vol from 22.0486756972 into 24.6148593333 carries the curve into the optimal window.

The 30-45 DTE band is the sweet spot: long enough that charm acceleration at the 733.5397900204 pivot doesn't drag P&L, short enough that contango carry compounds before the next macro window. Front-week structures expose you to the destabilizing flow flagged at the pivot; far-dated bleeds the carry edge.

Put spreads rank below because 3.06% with smile ratio 1.22% isn't steep enough to demand a directional skew trade - the tail is ordered, not bid. Express on QQQ given Positive Gamma underlay; size standard per Standard Size.

What it means for your trading

Engine favors Iron Condor at 59 over put spreads at 49; 30-45 DTE harvests VRP 2.52% without crossing the charm-acceleration zone.

Actionable Summary

Bottom line: the scenario engine flags Iron Condor in QQQ at the 30-45 window as the cleanest expression - positive-gamma underlay above 689.23 plus active VRP at 2.52% pays the carry without the pin risk SPY is dragging at 733.54. Fade SPY rallies into 735.00; dealers are short gamma above and net VEX -$286.49B amplifies any vol bid into selling.

Avoid IWM naked structures outright - regime tags Negative Gamma with 0DTE share at 41.2%, a chop trap that punishes directional conviction. Watch 733.5397900204 as the dealer-flow pivot: above it mean-reversion bid holds, below it charm flips destabilizing into the close.

Size standard per Standard Size - VVIX/VIX at 5.32 sits Normal, no jump-risk premium demanding half-size. Regime Elevated / Watchful with half-life 15 sessions - sticky enough to lean into, not against.

What it means for your trading

Trade structure: Iron Condor on QQQ at 30-45, fade SPY into 735.00, sidestep IWM. The pivot at 733.5397900204 is the single level that flips dealer flow direction today.

UAE moving hidden tankers through Hormuz signals Iran-conflict supply dynamics still in flux - keeps oil and geopolitical risk tail alive even as peace talks progress.

Gold's continued rally with peace talks ongoing tells you the inflation/sanctions hedge bid hasn't unwound - vol sellers should respect tail-risk premium even with VIX contango.

Wall Street bonus expectations flat-to-slightly-positive for 2026 with Iran war and private credit cited - confirms macro uncertainty hasn't been priced out of risk premia.

US-Iran short-term deal exploration is the single biggest vol-crush catalyst on the board - explains why front-month IV is suppressed despite tail risk.

China asking banks to pause loans to US-sanctioned refiners is a credit-channel escalation - watch MOVE and HY spreads for confirmation.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.32 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 733.54 against a spot of 733.37. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.76% with a volatility risk premium of 2.52%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.45. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime