Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

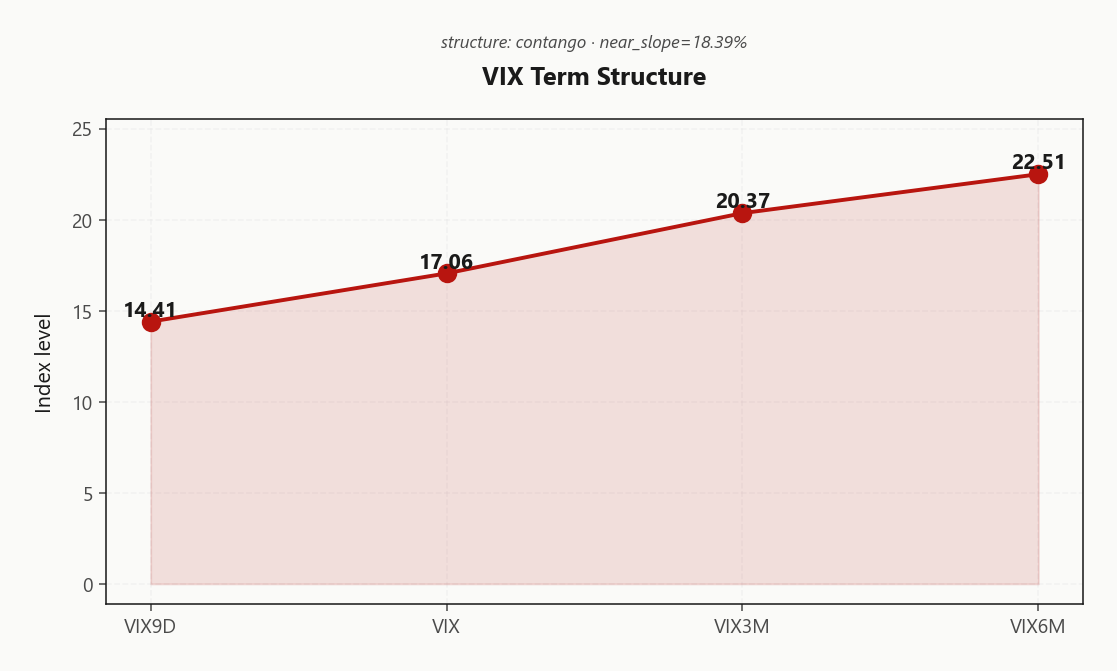

SPY closes at 732.09 sitting just above the gamma flip at 730.76 - dealers net long gamma at $2.59B, the classic mean-reversion cushion. Call wall 731.00 and put wall 730.00 bracket spot tightly; this is a pinned tape, not a trending one. Charm flow into the close was hostile (CHEX -$311.5M), and net VEX at -$271.71B means any vol pop forces dealers to sell delta - downside accelerant if VIX breaks higher. VIX prints 17.08 with VIX9D 14.41 below VIX3M 20.37 - steep contango, near-slope 18.39%%, VRP at 2.46% keeps short-vol carry alive. VVIX 94.27 sits in normal range, sizing standard. Watch IWM at 282.59 - it flipped into Negative Gamma and is the canary if risk cracks. Bottom line: 30-45 DTE iron condor centered on SPY with put spread tilt is the setup; avoid chasing breakouts above 731.00 or panic-selling below flip until small caps confirm.

SPY closes pinned just above the gamma flip with dealers long gamma, while IWM has slipped into Negative Gamma - that small-cap break is the day's tell. VIX term structure remains in Steep Contango with VVIX at 94.27, keeping vol-sellers in control. Iran headlines bleed in but credit (MOVE 70.63) refuses to confirm a stress regime.

Regime Assessment

The regime classification reads Elevated / Watchful with VIX anchored at 17.06 - neither a low-vol grind nor a panic regime, but the watchful middle where carry still works and complacency does not. Half-life of 15 sessions tells you this state is sticky enough to trade but not entrenched enough to fade aggressively; the regime can shift, just not on a single headline.

The transition matrix is the tell. Probability of escalation to panic over the next five sessions sits at 0.05 - negligible, with credit (70.63) and vol-of-vol (94.27) both refusing to confirm stress. Probability of drift back to a low regime over ten sessions runs to 0.45, an order of magnitude higher. The asymmetry is unambiguous: mean-reversion lower is the base case, panic is the tail.

Translation: stay short premium, size standard, and let the regime decay toward calm rather than betting on the jump. The yellow signal is a watch, not a warn - IWM's slip into Negative Gamma is the only thread worth pulling, and only if SPY follows below the flip at 730.76.

What it means for your trading

Regime is Elevated / Watchful at VIX 17.06 with drift-to-low probability 0.45 dwarfing panic-transition odds of 0.05 - the math favors mean reversion, not escalation.

Trading readVIX, VVIX, SKEW and MOVE all confirming a non-stress regime - no divergence flagging an imminent shift. When all four agree, the regime tends to persist; the warning sign is when one breaks ranks.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve prints textbook Contango with VIX9D at 14.41 well below spot VIX at 17.06, which itself sits beneath VIX3M at 20.37. The full stack ascends in order - Steep Contango - and the near-slope at 18.39%% leaves vol sellers firmly in the driver's seat with roll-yield intact.

The richer pocket sits in forward 30-to-60 vol at 21.8376635655, materially above spot VIX and the sweet spot for short-premium structures. The market is paying for forward vol it isn't pricing in spot - that's the carry. No backwardation kink anywhere on the curve means no event premium is being demanded; the tape is not bracing for a near-term shock.

Translation: 30-45 DTE captures the forward-vol reset without paying up for the front. Sell the wing where forward resets richer than spot implies; the curve would need to flatten or invert before this trade goes offside.

What it means for your trading

Steep contango with VIX9D under VIX under VIX3M means short-premium carry is fully open, and the 30-45 DTE pocket is where forward vol resets richest relative to spot. No event premium is being priced - vol sellers stay in control until the curve flattens.

Trading readSteep contango (Steep Contango) - vol carry trade fully open, market is not pricing near-term stress. Roll-yield favors short-vol; the curve would need to flatten or invert to flip the trade.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.88% trades meaningfully above realized at 10.42, leaving VRP at 2.46% - positive across the curve and harvestable. Short premium is being paid; long premium needs an exogenous shock to monetize.

The sequencing matters: HV20 at 10.42 sits below HV60 at 15.02, so recent tape has compressed off the three-month memory. Options screen modestly rich, not euphorically so - the spread is wide enough to fund condor wings without paying up for tail convexity that the realized print isn't validating.

Net: VRP is alive but not extreme. Systematic short-vol carry scores cleanly against this backdrop, and the IV-over-RV cushion absorbs ordinary intraday churn before the trade goes underwater. Size standard, lean into the belly of the curve, let the decay work.

What it means for your trading

VRP at 2.46% with HV20 10.42 below HV60 15.02 means options are paid against a compressed realized regime - short premium gets carry, long premium needs a shock.

Skew Convexity

Quarter-delta skew prints 2.32% with the smile ratio at 1.18% - downside is bid, but the demand profile is ordered, not frantic. Put-side IV at 15.05% sits a clean step above ATM at 13.68%, while the call wing at 12.73% prints below ATM. That asymmetry is the tell: hedgers are paying for protection, but no one is chasing upside convexity.

Read it as protection bid, not panic bid. A capitulation tape inverts call skew or rips smile ratios well past structural levels; this one does neither. With cross-asset tone Aligned and forward vol in Steep Contango, the steepness is harvestable - not a warning to flatten into.

Structure accordingly: put spreads dominate naked tail buys here. The richer put wing finances the further OTM leg cleanly, and the flat call skew makes the upside short of an iron condor cheap to layer on. Naked long puts pay full freight against a smile that is steep but not dislocated.

What it means for your trading

Quarter-delta skew at 2.32% and smile ratio 1.18% signal ordered hedging - put spreads beat naked tail buys, and the flat call wing keeps iron condor upside legs cheap to deploy.

Vol-of-Vol Structure

VVIX prints 94.27 against VIX at 17.06, leaving the ratio at 5.53 - squarely inside the Normal band. The market is not pricing a bimodal jump regime; there is no convexity bid screaming for protection on the protection.

That matters operationally. With vol-of-vol benign, the engine flags Standard Size - no haircut required, no half-clip on systematic short-premium. The absence of a jump-risk premium is the green light to deploy carry without paying up for second-order tail.

The watch is for VVIX leading VIX higher: a ratio breakout would re-introduce gap risk into the book and force a sizing rethink before the spot tape cracks. Until then, the vol-of-vol channel confirms the contango carry trade rather than warning against it.

What it means for your trading

VVIX at 94.27 versus VIX at 17.06 keeps the ratio neutral and sizing at Standard Size - no jump premium being demanded, systematic short-premium runs full clip.

Dispersion Spread

Index ATM IV at 12.88% sits in the moderate band while cross-strike dispersion at 70.95 stays wide - correlation is not crashing into this tape. Single-name gamma is moving (NVDA leads the rank at 2330394444%, AAPL behind at 2035229931%) without dragging the index basket into a unified bid for vol. That gap between elevated component dispersion and a contained index print is the trade.

Express the regime by selling index vol against single-name vol rather than naked shorts on individual tickers. The condor on SPY collects the index VRP cleanly while leaving idiosyncratic moves in TSLA, MSFT, AMZN to dissipate into their own gamma books. Avoid being long correlation here - a flat-to-rising dispersion print with Aligned large-cap regimes means an index correlation rip is the low-probability path.

Cross-strike dispersion supports the wings: condor strikes get paid without forcing the trader to reach for tail richness that isn't being offered.

What it means for your trading

Index IV elevated but not extreme at 12.88% with cross-strike dispersion at 70.95 - sell SPY/SPX vol against single-name vol, avoid being long correlation.

Liquidity & Microstructure

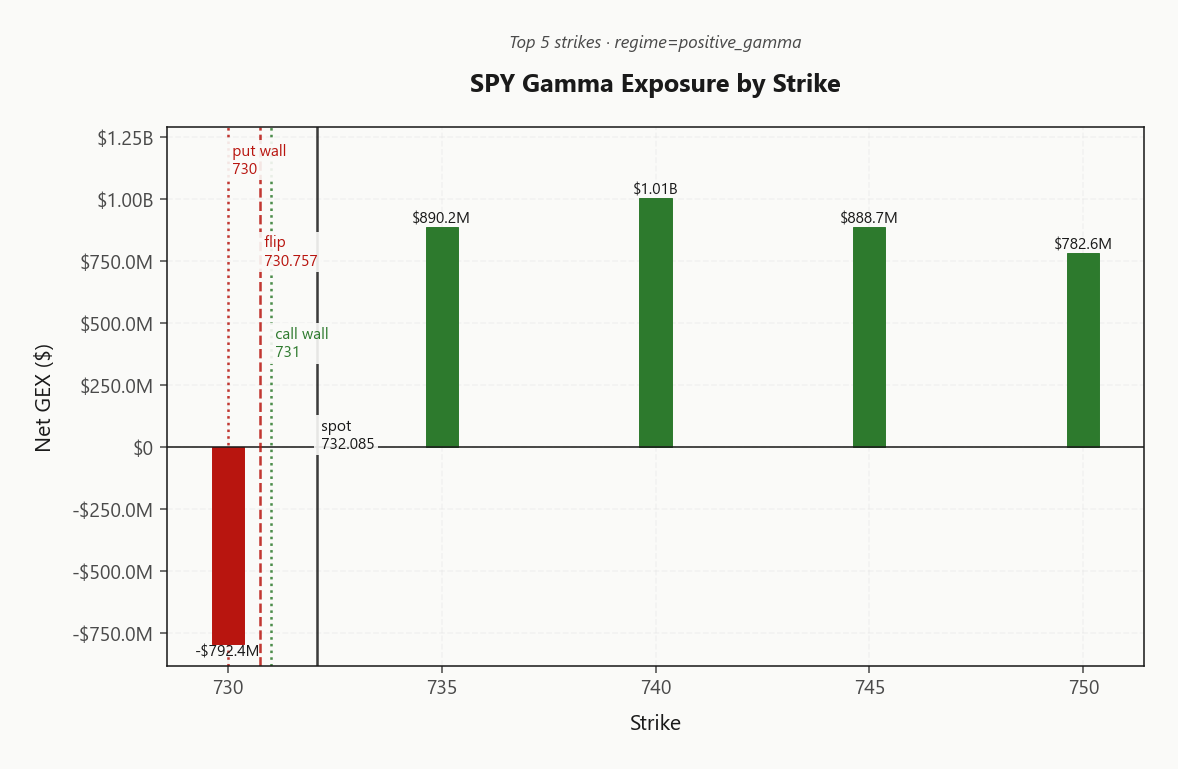

Open interest is concentrated in the 740.00 cluster well above spot, with net gamma at that strike printing $1.01B - that's the magnet zone, not a wall to fade. The highest OI strike at 700 anchors the term-structure narrative below, while the call wall at 731.00 caps near-term upside extension and the put wall at 730.00 sits flush against the regime line.

Spot trades a hair above the gamma flip at 730.76, leaving the tape in Positive Gamma by the thinnest of margins. Above flip, dealer hedging dampens - buy dips, sell rallies, the classic mean-reversion mechanic. A single-tick break below flips the entire microstructure to amplifier mode: dealers chase down, liquidity thins, and the 730.00 put wall becomes the next gravity well rather than support.

Trade the bracket while it holds; respect the flip when it doesn't.

What it means for your trading

SPY microstructure is constructive but knife-edge - the 740.00 OI cluster magnetizes upside while the gamma flip at 730.76 is the single line separating stabilizer from accelerant. Position for the range above flip; flatten or flip directional on a confirmed break below.

Trading readMassive call-side GEX cluster sits above spot at the 735-750 zone, with the put wall just under spot at the gamma flip - dealers dampen any push toward calls and amplify any break below the flip. Trade the range; don't fade it once flip breaks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

The second-order book is where the bull case frays. Net VEX prints -$271.71B - deeply negative - meaning any uptick in implied vol forces dealers to sell delta, not buy it. That's the classic accelerant: a benign VIX pop stops being benign once vanna flow joins the move. The positive-gamma cushion above the flip is real, but it is conditional on vol staying pinned.

Charm is the other tell. Net CHEX at -$311.5M means time decay is bleeding hostile into the close - dealers are not getting the supportive pin you'd want from a Friday-bias tape. The charm pivot sits at 731, classified as a Call Wall, with current bias Neutral. That single level is the regime switch.

Trade it accordingly: a clean break above the call wall flips charm flow from drag to tailwind and unlocks the upside chase. Until then, dealer mechanics are stabilizing on the gamma axis but actively fighting you on the vanna and charm axes - short premium works, but stay sized for a vol pop that the second-order book will not absorb gracefully.

What it means for your trading

Vanna is a coiled accelerant at -$271.71B and charm is hostile at -$311.5M; the call wall at 731 is the binary level that flips dealer flow from headwind to support.

Cross-Asset Confirmation

Credit refuses to confirm the equity wobble. MOVE prints 70.63 - benign by any post-2022 standard - even as Iran headlines bleed across the tape. When rates vol stays anchored while equity desks chase headline premium, the signal is unambiguous: this is an isolated equity event, not a credit-channel transmission.

Fear & Greed sits at 68 in Greed territory - sentiment is constructive, not defensive. Cross-asset regime reads Aligned at the index level, with QQQ at 695.57 tracking SPY's positive-gamma cushion. The lone fracture is IWM at 282.59 in Negative Gamma - small-cap fragility, not systemic stress.

The trade implication is mechanical: geopolitical shocks mean-revert when credit stays quiet; they compound only when MOVE breaks ranks. Until rates vol confirms, fade the geopolitical premium rather than hedge it. The canary is IWM losing its bid and MOVE breaking higher in the same session - absent that pair, the headline tape is noise the carry trade can absorb.

What it means for your trading

Credit's refusal to confirm - MOVE at 70.63, F&G at Greed, cross-asset regime Aligned - frames Iran headlines as isolated equity noise, not macro shock. Watch the IWM-plus-MOVE pair for a regime change; until then, geopolitical premium fades.

Scenario EV

The scoring engine returns Iron Condor as the preferred structure with a composite score of 52, edging out the put-spread alternative at 41. The combined read - VRP active at 2.46%, VVIX benign at 94.27, charm pivot neutral at 731 - is the textbook setup for symmetric short-premium income rather than directional skew.

The optimal window sits in the 30-45 DTE pocket: far enough out to clear the 0DTE charm grind around -$311.5M, close enough in to harvest the richer forward-30-to-60 vol at 21.8376635655 against spot VIX of 17.08. Strikes anchor on the 731.00 call wall and 730.00 put wall - the dealer book draws the lines, the trader collects the rent.

Put-spread runner-up at 41 stays viable for desks wanting directional asymmetry into the Negative Gamma small-cap divergence, but the symmetric condor is the cleaner expression while VVIX prints normal - standard size, no haircut.

What it means for your trading

Iron condor wins at 52 versus 41 for the put spread; deploy 30-45 DTE around the 731.00/730.00 wall pair at standard size.

Actionable Summary

Primary structure:30-45 DTE Iron Condor on SPY, centered between the 730.00 put wall and 731.00 call wall. VRP at 2.46% and VVIX at 94.27 (Normal) green-light Standard Size - no haircut warranted. Alternative: put-spread tilt for traders wanting directional asymmetry over symmetric income, scoring just behind the condor.

Watch levels. SPY gamma flip at 730.76 is the regime line - spot sits a hair above, and a clean break flips dealer flow from dampener to amplifier given net VEX at -$271.71B. Charm pivot at 731 is the second tell. The canary is IWM at 282.59, already in Negative Gamma while SPY/QQQ hold Aligned; small-caps crack first.

Avoid: chasing 0DTE breakouts above 731.00, panic-selling below the flip until IWM confirms, and naked tail buys at this VVIX level. Regime read: Elevated / Watchful - sticky, not entrenched, mean-reversion bias intact.

Iran-US peace-proposal status is the single biggest macro overhang - any breakthrough collapses the geopolitical premium baked into vol; any breakdown spikes oil and bleeds into MOVE.

$7B in oil bets ahead of the news tells you institutional money has been positioning for resolution - if the headlines disappoint, the unwind is sharp and reflexive into equities.

Software-stock comeback is the rotation tell - sector leadership shifting back to growth/software while value/cyclicals digest the Iran shock; relevant for QQQ vs SPY relative-vol trades.

McDonald's flagging Iran-war cost pressure on long-term demand is the first major-cap consumer admission of geopolitical drag - watch for follow-through in consumer staples earnings revisions.

Chinese-owned tanker hit near Hormuz with US ship-protection paused is the tail-risk re-escalation headline - if this thread expands, MOVE breaks higher and credit confirms a stress regime.

Wall Street bonus pool flat-to-slightly-positive flags institutional risk appetite is muted - relevant context for why VRP can stay rich without immediate compression.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.08 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 730.76 against a spot of 732.09. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.88% with a volatility risk premium of 2.46%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.06. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime