Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

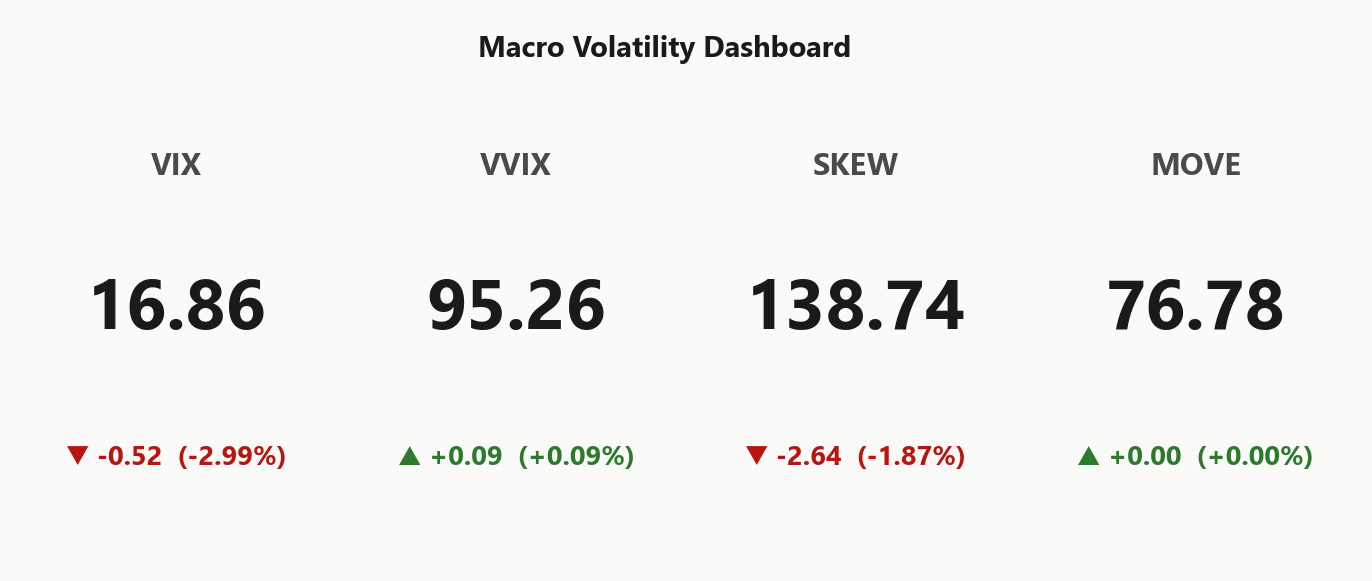

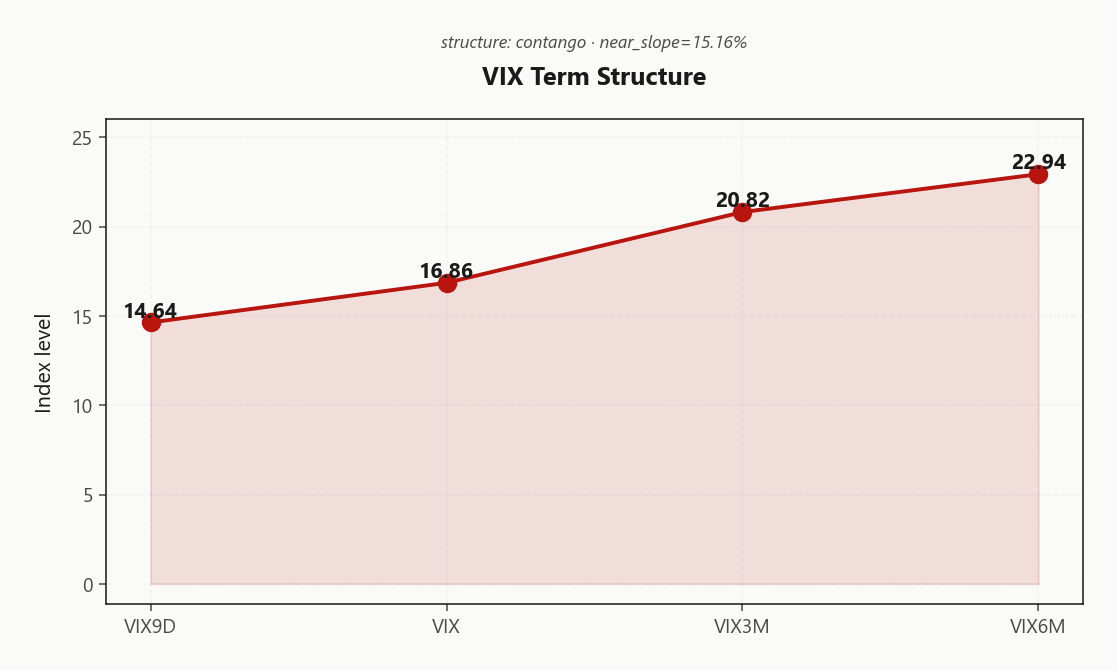

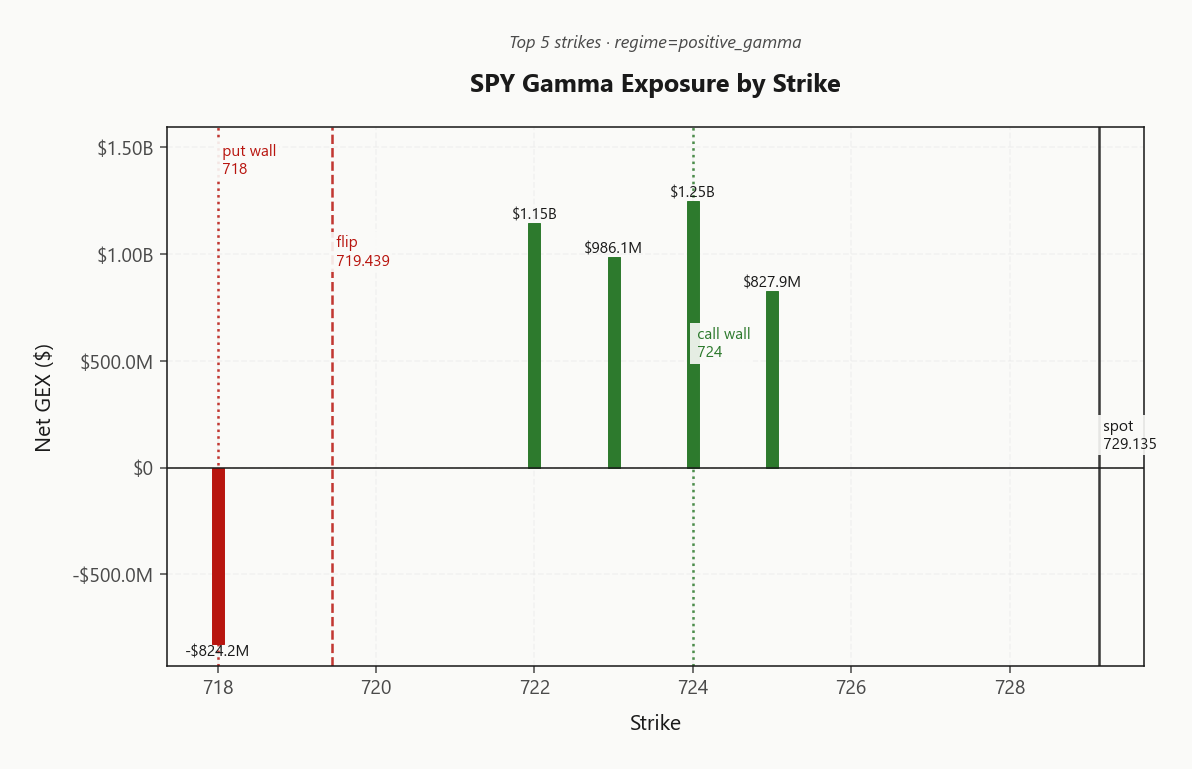

SPY at 729.14 with net GEX $3.06B firmly in positive-gamma territory - dealers long gamma, moves get dampened, mean reversion is the path of least resistance. Call wall 724.00 is acting as the upside magnet and put wall 718.00 as the floor; gamma flip sits at 719.44, putting spot comfortably above the regime line. Net vanna -$490.7M and net charm -$1.65B are negative - that means a vol spike would force dealers to sell delta into weakness, and time decay leans dealers short into the close. VIX at 16.86 with VIX9D at 14.64 and 3M at 20.82 = steep contango, term slope 15.16%% - vol carry trade is live and paying. VVIX at 95.26 is normal, VVIX/VIX ratio 5.65 = standard sizing, no jump-risk hangover. Bottom line: iron condor regime per Iron Condor, optimal DTE 30-45, fade strength into the call wall and buy weakness above the gamma flip - only AVOID is chasing breakouts above 724.00 where dealer sell flow accelerates.

Positive gamma across index complex with VIX in steep contango - mean reversion regime, vol sellers favored

SPY trades above the gamma flip at 719.44 with dealers deep long gamma, dampening realized vol while VIX sits in steep contango at 15.16%% slope. Iran peace deal headlines lift risk and crush front-end vol, leaving the 724.00 call wall as the magnet and 718.00 as the cushion. The setup favors carry - sell premium, fade extremes - but VIX itself sits in negative gamma so a vol spike would reflex faster than usual.

Regime Assessment

Regime reads Elevated - Elevated / Watchful - with VIX at 16.86 sitting clear of the low-vol cutoff but well shy of panic. The complex is positive-gamma aligned across SPY, QQQ, and IWM with VIX itself in negative gamma and term structure in Contango, the textbook backdrop for harvestable carry rather than tail-hedge accumulation.

Transition probabilities frame the durability: a move to panic over the next five sessions sits at 0.05 - tail risk is priced cheap and the market agrees the Iran de-escalation tape is real. Glide-path probability into low-vol over ten sessions runs 0.45, a realistic relaxation if the framework agreement closes. Regime half-life of 15 sessions confirms the setup is sticky enough to underwrite 30-45 DTE structures without overpaying for theta you won't collect.

Bias: sell premium via Iron Condor, respect 719.44 as the regime trip-line, and pre-place stops above 724.00 where vanna reflexivity bites. Headline-driven repricing remains the asymmetric risk - durable, not bulletproof.

What it means for your trading

Elevated / Watchful regime is sticky for roughly 15 sessions with panic priced cheap at 0.05 - long enough to run 30-45 DTE iron condors, short enough to demand stops at the gamma flip.

Trading readVIX, VVIX, SKEW, MOVE all behaving consistently - no divergence flagging hidden stress. SKEW soft = no crash bid, MOVE flat = no credit shock, VVIX normal = no jump panic. Confirming environment for carry.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

Term structure prints Contango from the front through the back, with VIX9D at 14.64 sitting well below spot VIX at 16.86 - front-end crush is real, courtesy of the Iran de-escalation tape compressing near-dated premium. Slope qualifies as Steep Contango, the cleanest carry signature this complex prints.

The VIX3M anchor at 20.82 and 6M at 22.94 are not selling cheap - back end is pricing structural risk premium, which is why naked front-end shorts give up convexity. Forward 30-to-60 vol at 22.5406033637 sits above spot VIX, telling you the curve expects mean reversion up, not down - calendar long-vega against short-dated condor is the cleanest expression.

Signal reads Green: vol sellers favored, but the edge concentrates in the 30-45 band where contango pays without absorbing event-risk premium loss. Watch for slope flattening - that's the backwardation tell if Iran headlines reverse.

What it means for your trading

Steep contango with VIX9D crushed under spot VIX and VIX3M anchored makes the 30-45 DTE band the structural sweet spot for carry. Front-end shorts paired with back-dated long vega capture the curve without taking the headline-reversal hit.

Trading readSteep contango with VIX9D well below VIX and VIX3M anchored - this is THE classic vol-carry setup, sellers are paid for sitting in the front while back end prices structural risk; flag if slope flattens, that's the reversal tell.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.28% trades comfortably above HV20 at 9.56, leaving a clean 2.72% VRP cushion that qualifies as Moderate Premium on the harvest scorecard. Spot has been delivering RV5 of 8.68 - well under what front-month options are charging - the textbook footprint of dealers long gamma damping intraday range.

The deceleration is real, not a head-fake. HV60 sits above HV20, so vol is cooling rather than coiling, and the Positive Gamma backdrop with spot above the gamma flip at 719.44 keeps the suppressive bid on realized intact. Options remain priced for a tape that isn't showing up.

The edge is short-strike condor structures that monetize VRP without renting jump risk while VVIX sits Normal at 95.26. Sizing is Standard Size - standard, not half - but pre-place stops at the flip because negative net vanna at -$490.7M means a vol pop reflexes harder than the carry math suggests.

What it means for your trading

IV at 12.28% over HV20 at 9.56 prints a harvestable 2.72% cushion - short-vol carry is paid here, with sizing constrained only by the vanna reflex below the gamma flip.

Skew Convexity

The quarter-delta put wing prints 15.03% against an ATM mark of 13.2%, a 3.24% skew that screens steep but the smile ratio at 1.28% reads as ordered protection demand - hedgers renting downside into headlines, not a crash bid. The section signal trips Skew Steep: priced for protection, not panic.

The call wing tells the other half of the story. Quarter-delta calls at 11.79% sit flat to ATM, so upside convexity is optically cheap but there is no chase bid building underneath - consistent with dealers pinned long gamma into the 724.00 wall. Net VEX -$490.7M means a vol pop reflexes through dealer delta sales, which is precisely why the put wing keeps a bid even with realized compressed under positive gamma.

Trade expression: harvest the put-wing premium via short put spreads rather than naked shorts. The wing pays you for protection that Positive Gamma dealer flow already provides through the 718.00 cushion, and capping the short leg sterilizes the vanna asymmetry if VVIX rerates higher.

What it means for your trading

Skew is steep but contained - ordered hedging at 1.28% smile ratio, not panic - so the trade is short put spreads to collect the wing premium, not naked shorts that take the full vanna reflex if vol pops.

Vol-of-Vol Structure

VVIX prints 95.26 against VIX 16.86 - squarely Normal. No bimodal jump premium is being demanded; the tape is digesting Iran headlines as a repricing, not a binary event.

The VVIX/VIX ratio at 5.65 sits proportional - vol-of-vol is tracking spot vol cleanly, no second-order panic bid layered on top. That keeps sizing guidance at Standard Size with section signal Green, the green light to run full premium-selling size rather than half-clip.

Watch trigger is mechanical: a ratio rerate through the seven-handle would force an automatic size cut and flip the carry thesis. Currently well clear, but vanna posture is negative - if VVIX bids on a headline reversal, the iron condor regime cracks before the print does. Run standard size, pre-place stops at the gamma flip.

What it means for your trading

VVIX Normal with ratio 5.65 clears full-size short premium under Standard Size; the ratio crossing seven is the only pre-committed size cut.

Dispersion Spread

SPY ATM IV at 12.28% sits middling - index vol is not the cheap leg, and that matters for structure selection. Cross-strike dispersion prints 32.24 against a tighter cross-expiry read of 2.86, qualifying the smile as contained - single-name correlation is unchallenged and the index surface is doing the work it's supposed to.

Section signal lands at Moderate - neither cheap dispersion nor a correlation breakdown, just an ordered tape. With earnings season layering idiosyncratic risk on top of the Iran headline regime, pairing an index hedge against single-name short strangles invites uncompensated dispersion drift.

Preference: SPY iron condor over single-name structures while the headline tape runs. Index dealer depth absorbs the carry; single-name vol stays the speculative leg, not the harvest leg. Re-rate only if cross-strike dispersion compresses meaningfully into a flatter smile - that's the tell that single-name premium starts paying better than index.

What it means for your trading

Index ATM IV at 12.28% with cross-strike dispersion 32.24 keeps single-name correlation unchallenged. Run SPY iron condors over single-name strangles while the regime signal sits Moderate.

Liquidity & Microstructure

Open interest is stacked at 710 with the dominant gamma anchor sitting at 724.00 carrying net GEX of $1.25B - that strike is the magnet for intraday hedging flow. The 724.00 call wall caps near-term upside as dealer sell flow accelerates into strength, while the 718.00 put wall offers a buy-flow cushion on weakness.

The regime trip-line is the gamma flip at 719.44. Spot trades comfortably above it, leaving dealers long gamma and the tape in mean-reversion mode - moves get dampened, ranges compress, and fade-the-extreme is the path of least resistance. Lose the flip and that flow inverts: dealers turn pro-cyclical and amplify direction.

Trade the structure: fade strength into the call wall, accumulate near the put wall, and treat the flip as a hard regime line rather than a soft pivot.

What it means for your trading

Dealer book is deep and orderly with gamma stacked at 724.00; mean reversion stays the dominant mode while spot holds above the 719.44 flip.

Trading readHeavy positive gamma stacked at the call wall says dealers will sell into strength and buy weakness - fade rallies into 724.00, accumulate near the put wall, and respect the gamma flip as the regime trip-line.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$490.7M and net CHEX -$1.65B - both negative, and that asymmetry is the trade. Vol-up forces dealers to sell delta into weakness; the gamma cushion that flatters this tape reverses character the moment VVIX rerates. Charm flow tilts dealers short into the close, layering late-session pressure on top of the vanna reflex.

The flow-inversion line sits at the Call Wall pivot of 724, with current pivot-distance bias reading Neutral. Above it, dealer hedging dampens; through it, the same book amplifies. Vanna read: Vol up = dealers sell delta - downside amplified if vol spikes - run standard short-vol size while VVIX/VIX stays at 5.65, but cut to half-size the moment the ratio reprices higher.

What it means for your trading

Negative vanna and negative charm make this a benign-until-it-isn't carry tape: dealer flow caps moves now, but a VVIX rerate flips the book to seller-into-weakness. Watch the Call Wall pivot at 724 as the regime trip-line.

Cross-Asset Confirmation

MOVE prints 76.78 and refuses to confirm any equity stress - bond vol is asleep while the front of the VIX curve gets crushed by Iran de-escalation headlines. That asymmetry is the tell: this is a geopolitical risk-premium unwind, not a credit event, and the simultaneous bid in stocks and bonds traces back to the same peace-memo catalyst.

Cross-asset tone reads Unknown with the SPY/QQQ divergence flag False - regime-aligned across the complex, no lead-story split to drive a rotation sell-off. QQQ at 689.91 and IWM at 284.91 both sit above their gamma flips, so breadth confirms the dealer-suppression backdrop rather than leaning on mega-cap concentration.

Fear & Greed at 67 (Greed) tilts the read contrarian-cautious - sentiment is leaning into the rally but VIX hasn't fully capitulated, leaving the carry trade live without the euphoric overshoot signature.

What it means for your trading

Cross-asset signals are Aligned with bond vol quiet and index gamma cohesive - confirms the iron-condor regime, with IWM as the canary if breadth cracks first.

Scenario EV

Scoring across the structure book lands on Iron Condor as the cleanest expression at 61, edging the put-spread alternative at 52. Positive gamma anchors the tape above the flip at 719.44, VRP carries cleanly with ATM IV at 12.28% over HV20 at 9.56, and VVIX/VIX at 5.65 green-lights Standard Size rather than haircut sizing.

Optimal tenor band sits at 30-45 - far enough out to harvest the contango from VIX9D at 14.64 through VIX3M at 20.82, close enough to avoid the back-end risk premium parked at VIX6M. VRP read prints Unknown on the framework but the IV-RV cushion at 2.72% keeps the short-vol thesis intact.

Avoid 0-DTE chase - gamma coils too tight against the 724.00 wall to pay edge. Pre-place stops at the flip; vanna at -$490.7M turns reflexive on a vol pop.

What it means for your trading

Run Iron Condor in the 30-45 band at standard size, with hard stops at the gamma flip 719.44 to neutralize the negative-vanna reflex. Skip 0-DTE - score advantage evaporates against the 724.00 wall.

Actionable Summary

The book is set up for carry: SPY anchors a Positive Gamma regime with net GEX $3.06B and spot pressed against the 724.00 call wall, while VIX sits in Contango at a 15.16% term slope. Scoring favors Iron Condor in the 30-45 DTE band, sized standard per VVIX/VIX at 5.65.

The regime line is the charm pivot at 724 (Call Wall) - above it dealer flow dampens, below it the entire mean-reversion thesis flips to trend. Net VEX -$490.7M and net CHEX -$1.65B tilt asymmetric: a vol pop forces dealer delta selling into weakness, so use spreads, not naked puts, to cap vanna risk while harvesting the bid put wing.

Avoid chasing strength above 724.00 where dealer sell flow accelerates. Context: regime reads Elevated / Watchful with half-life 15 sessions - durable, not bulletproof; headline-driven repricing risk persists.

What it means for your trading

Sell the Iron Condor in the 30-45 band while spot holds above the 724 pivot; flip defensive if that line breaks or VVIX rerates higher.

Gold breaking out alongside the equity bid is the classic 'liquidity unlock' signal - not a flight-to-safety bid, but rates-and-real-yields easing into a peace memo, supportive of duration AND risk simultaneously.

Dollar weakening with the yen surge ignites intervention chatter - a softer DXY removes a key headwind for multinationals and supports the SPY positive-gamma thesis via cleaner cross-asset carry.

The peace memo report is THE driver crushing front-end VIX and explaining the simultaneous stocks-and-bonds bid; if the deal slips, expect VVIX to rerate and the iron condor regime to flip backwardation.

Stocks and bonds rallying together post-Axios is the cleanest tell that this is a geopolitical-risk repricing, not a credit event - favors carry trades and disqualifies tail hedges as the dominant trade.

Confirms the framework agreement is real, not just trial balloon - reduces probability of a vol-spike reversal in the next 5 sessions, anchoring the elevated-but-glide-lower regime read.

Global stocks surging while oil slides is the structural sign of a risk-friendly de-escalation - short-vol carry stays alive as long as oil doesn't reverse on a deal breakdown.

Trump pausing Hormuz operations is the operational confirmation behind the headlines - material because it shifts the supply-disruption tail risk lower, directly suppressing implied vol.

Occidental cutting production guidance shows the corporate fingerprint of Iran disruption - even with peace hopes, Q1/Q2 earnings have already been hit, watch for energy-sector vol divergence.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.04 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 719.44 against a spot of 729.14. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.28% with a volatility risk premium of 2.72%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.86. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime